DAL - Delta Air Lines: Going Long With Earnings Surge And Travel Demand

2023-12-08 03:43:42 ET

Summary

- Delta Air Lines gets Buy rating as of now, agreeing with consensus from SA analysts and quant system.

- Tailwind coming from top and bottom line growth, travel surge, lower fuel cost, lower debt levels and interest costs.

- Headwinds include a weak dividend yield and the risk of OPEC-related oil price spikes in 2024.

URL Stock Snapshot

In this research note I'm taking to the friendly skies again and covering an airline stock again.

Delta Air Lines ( DAL ) had its Q3 earnings release in early October, and now that we are knee deep in the holiday travel season already what better time than to talk about an airline.

A few quick facts about this company are that it is headquartered in Atlanta, trades its stock on the NYSE, boasts 4,000 daily flights and more than 280 destinations on six continents, and is a member of the SkyTeam airline alliance.

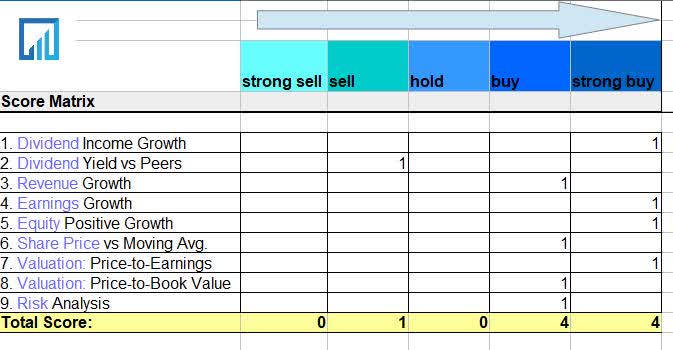

Scoring Matrix

This article uses a 9-point scoring matrix that holistically considers multiple angles of the stock, with an emphasis on cashflow potential for investors and fundamental trends from the key accounting statements publicly available such as the balance sheet and income statements, as well as a future-looking outlook on this stock.

Current's Rating

{kind=link}

In the case of my score matrix above, both the "buy" and "strong buy" rating scored the same number of points, while the "sell" side scored just one point.

So, to break the tie I will also include this stock's momentum vs the S&P500 index, which showed that its 1 year price return was a positive +15.13% but came just short of beating the index.

Therefore, I will call this a buy now.

Compared to the consensus rating on Seeking Alpha, my rating for now agrees with the sentiment from SA analysts and the SA quant system, but is just slightly less bullish than Wall Street who is very bullish on this stock as of now:

Delta - rating consensus (Seeking Alpha)

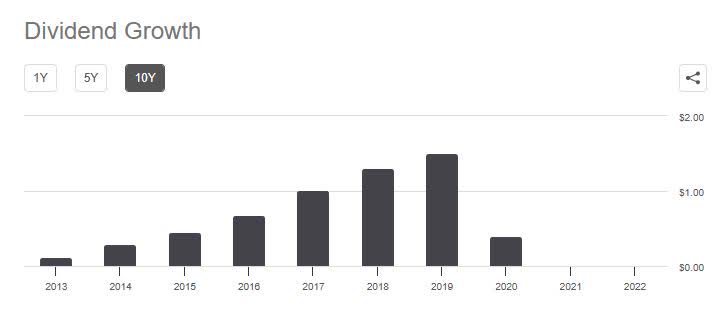

Dividend Income Growth

This section uses dividend growth data to explores the 10 year dividend income growth for a hypothetical investor owning 100 shares, to determine whether this stock is a great dividend income opportunity.

{kind=link}

Using the chart above for assistance, I can see that a 100-share investment in 2013 would have paid $0.12/share in annual dividends, generating $12 annual dividend income, although by 2022 there was $0 dividend income to be made as it appears from their history that they did not pay any that year. So, we can use the $0.10/share quarterly dividend they began paying again in 2023 to project a $0.40 annual dividend in 2023 ($40 dividend income).

That is over 200% growth in annual dividend income compared to 2013, despite the dividend slump during the pandemic years which is understandable considering that airlines took a huge hit.

Although dividends can always fluctuate and even be cut by the company anytime, for this example let's say we extrapolate to 2033 and assume another 200% annual dividend growth. That should get the dividend investor to $1.20/share ($120 annual dividend income on 100 shares).

Because the stock rebounded nicely after the pandemic to grow its dividend vs 2013 levels by 200%, I will go ahead and call it a strong buy in this category.

Dividend Yield vs Peers

This section uses dividend yield data to compare the trailing dividend yield vs 3 similar peers in the same sector, to determine if this stock presents the most competitive dividend yield on capital invested.

{kind=link}

In the chart above, I compared the dividend yield of my subject stock Delta vs US airline peers Southwest Airlines ( LUV ), United Airlines ( UAL ), and JetBlue ( JBLU ).

Of this peer group, only Southwest and Delta showed any dividend yield at all, and Southwest led the way with a yield of 2.65%.

Delta unfortunately is barely offering a 0.27% yield (as of the date of the chart) so I will pass on giving it a buy in this category, since there are much better yields I can get for my capital, and in this sector it would be Southwest.

Revenue Growth

This section explores this company's revenue growth trends over the last year, using data from the income statement.

The top-line growth story it tells us is that Delta saw $15.48B in revenue in Q3, vs $13.97B in Sept 2022, a nearly 11% YoY growth . What should be also noted is the airline seems to have made a huge rebound since the pandemic period when they only saw $4.15B in revenue in March 2021.

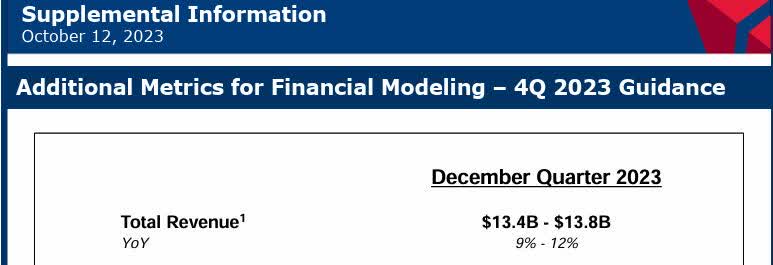

But wait, there is more good news. According to the Q3 earnings release , "expect full year adjusted revenue growth of 20 percent over 2022 with a double-digit operating margin."

Further, there is positive revenue outlook in Q4:

{kind=link}

What I can say is that increase in top-line sales usually points to increased demand for a product or service, and the company's results support this particularly in their key hubs and with corporate clients:

Coastal hub load factors expanded year-over-year, driven by growing demand in Boston and New York. Business travel continues to improve as corporates announce return to office initiatives.

So, when it comes to top-line revenue prospects, I am bullish on this stock.

Earnings Growth

This section explores this company's earnings (net income) growth trends over the last year, using data from the income statement .

What I can see is that the company achieved $1.1B in net income this Q3 vs $695B in Sept 2022, a +58% YoY growth.

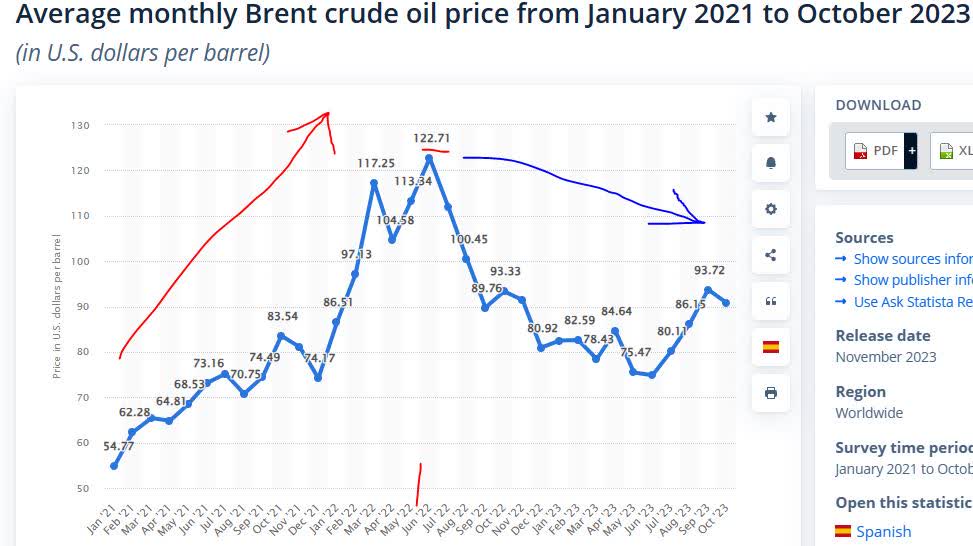

As we already talked about top-line revenue, let's mention a key item that impacts the bottom-line of airlines and that is fuel costs.

The good news is that it appears from their earnings data that this has been on the decline:

• Adjusted fuel expense of $3.0 billion was down 10 percent year-over-year • Adjusted fuel price of $2.78 per gallon declined 21 percent year-over-year and includes a refinery benefit of 11¢ per gallon.

Let's look at the following chart from Statista which shows a downward price trend for crude oil:

{kind=link}

Although geopolitical conflicts and political maneuvering as well as supply cuts by OPEC and others can impact future oil prices, and not exactly something we can predict with certainty, for now I think the existing trend of lower fuel prices will favor this airline and its sector.

In addition, their interest expenses on debt decreased to $196MM from $248MM in Sept 2022, a 21% YoY decline in interest costs and very relevant in the current high rate environment.

So, because of 58% earnings growth, declining fuel costs and interest expenses, I will be adding another point in the strong buy section of my score matrix.

Equity Positive Growth

This section explores this company's equity (book value) growth trends over the last year, using data from the balance sheet.

For one, the total equity in Q3 grew to $9.22B from $4.59B in Sept 2022, a +100% YoY growth in positive equity.

A key item impacting book value is debt, and the good news to report is that long-term debt dropped to $16.3B from $19.8B in Sept 2022, a +17% YoY decline in debt.

This is important to note considering the high cost of debt financing in the last year.

For this reason, I am highly bullish on their equity situation right now, considering their book value was around $480MM in March 2021 during the pandemic era when we did not know which airlines would make it. This one did.

Share Price vs Moving Average

This section explores the current share price compared to the 200-day simple moving average , to decide if it currently presents a buy, hold, or sell opportunity.

Though I would not call it a strong buy at this price, since that opportunity would have been during the autumn price dip you see in the chart. However, it is still only just 5% above the 200 day SMA and also well below its July peak.

I will call it a buy not because of a great dividend yield you will get but because of strong revenue and earnings, and dividend growth potential, as well as improved equity. More importantly, the projected demand combined with lower fuel costs should provide tailwind (literally) for this stock in Q4 and early 2024, if those conditions should continue.

I think it is too valuable to "sell" at this price, so if I was already owning this one in my portfolio and bought at the autumn lows I would probably hold on longer.

Valuation: Price-to-Earnings

This section uses valuation data to explore the forward P/E ratio and whether it presents an undervalued opportunity.

Important to note is the forward P/E ratio which is now 7.60, or +63% below its sector average.

Tying this multiple to the share price and earnings we talked about earlier, I would argue that this low multiple is being driven by the impressive earnings growth while the share price is only a few percents above the 200-day average, so in this situation I think this multiple of 7.6x is justified and provides an undervaluation opportunity.

Definitely another point in "strong buy" at this low multiple to earnings which are on the uptick.

Valuation: Price-to-Book Value

This section uses valuation data to explore the forward P/B ratio and whether it presents an undervalued opportunity.

What we can gather is that the forward P/B ratio of 2.27 is +10% below the sector average.

Tying this back to the equity/book value data earlier and the share price, what I think is driving this low multiple is the growing equity combined with a share price not far above the moving average, despite the recent price jump from its autumn low.

In this situation, I will call it more of a "buy" as I would like that multiple even lower, considering that peer Southwest has a forward P/B of just 1.46x, and their equity has also improved on a YoY basis.

Nevertheless, Delta's valuation is reasonably justified because of growth in book value.

Risk Analysis

This section identifies a key risk to consider about this company and what its probability and impact could be to the business.

With this type of business, we briefly mentioned that it can be impacted by volatility in global fuel costs as well as slumps in travel demand, along with the cost of debt. Because we already addressed the fuel and debt question, let's take a closer look at the risk of falling travel demand and the airline not being able to fill its seats this holiday season and beyond.

Here are what some sources external to Delta have to say on that lately, as well as what its airline peers said.

A headline today in Reuters read "Jetblue narrows loss forecast on healthy travel demand."

Today's Wall Street Journal article referred to Jetblue "lifting its outlook for fourth-quarter sales, saying that demand for travel is holding up and bookings have accelerated into the holidays."

Since Delta is much more global than Jetblue, though, let's also speak to global demand for a moment.

Here is what yesterday's article in financial media CNBC had to say about the International Air Transport Association (IATA) projections for global airlines:

Total revenues in 2024 are set to grow 7.6% year on year to a record $964 billion, with around 4.7 billion people expected to travel in 2024, a figure exceeding the pre-pandemic level of 4.5 billion seen in 2019.

However, the "headwinds" of oil prices that could impact the industry should not be ignored in 2024. According to the Dec. 1st article in CNBC , this could come down to OPEC decisions:

Oil prices are expected to rise in the new year after some OPEC+ oil producers voluntarily pledged to cut output.

So, I think the evidence shows that the risk of travel demand slumping has both low probability and will have low impact, while the risk of fuel costs rising could present perhaps a medium probability and medium impact, since revenue strength could offset the increased fuel costs.

On this category, I would go with a "buy" rather than a "strong buy" for the reasons mentioned.

Quick Summary

To summarize this note briefly, I am going long / bullish on this stock now and the tailwinds include really impressive top and bottom line growth numbers, dividend recovery and growth, and expected travel demand spiking along with fuel currently cheaper.

Possible headwinds to this sector could come from OPEC-related spikes in oil prices that could impact airline fuel costs as well as ticket prices. In addition, for a dividend-oriented investor the yield on this stock is far below average at less than 1% yield.

Holistically considering all the categories, this is an opportunity to add a strong global airline to diversify a portfolio consisting of other sectors, not so much for a great dividend yield but potential share price appreciation and capital gains.

For further details see:

Delta Air Lines: Going Long With Earnings Surge And Travel Demand