DAL - Delta Air Lines: Input Cost Rising Summer Travel Over

2023-09-21 11:34:46 ET

Summary

- Delta Air Lines is pushing away customers with its management decisions, such as charging different amounts for various seating options.

- Delta's expenses and costs are unpredictable, making it a risky investment.

- The stock has underperformed the market historically and I don't view DAL as a good long-term investment.

Investment Thesis

Delta Air Lines ( DAL ) was my favorite airline to fly for the past five years. They have the cleanest planes, the nicest staff, TVs on the back of every seat, and the best amenities. However, I would still not want to own the stock. In fact, I believe Delta is pushing away customers with some of its management decisions.

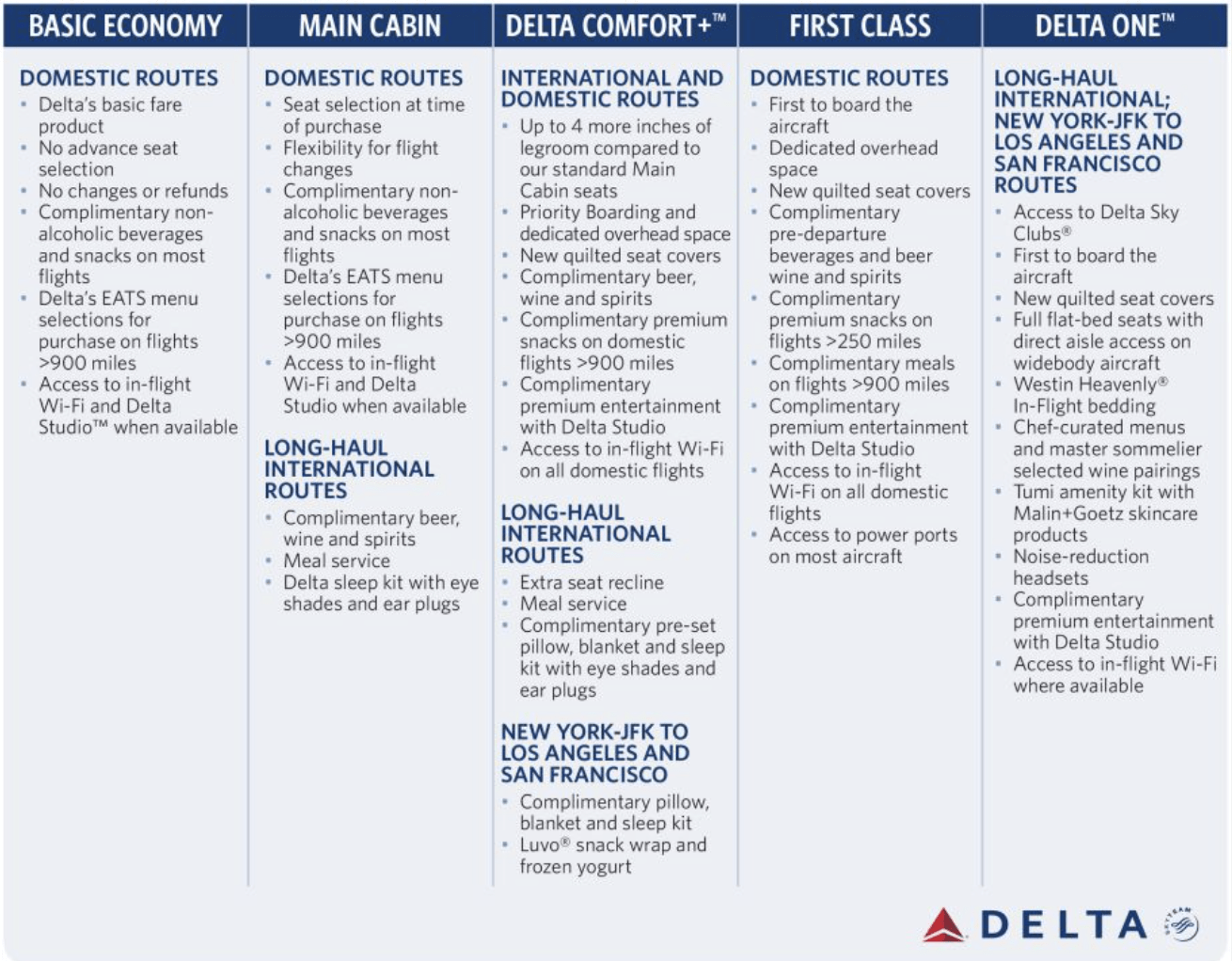

They primarily make money off their unnecessary extra offerings. It is no longer just first class and everyone else. They now charge different amounts for levels of seating : Delta One, Premium Select, First Class, Comfort+, Main Cabin, and Basic Economy.

{kind=link}

They have even added a charge to pick what seat you want, with higher costs for aisle seats compared to window or middle seats. Some investors may see this as a boost to reoccurring sales helping earnings, but I see it as likely to frustrate customers, possibly pushing them to cheaper competitors. When I buy a $500+ airline ticket, I would assume that I would get to choose what seat I want (from available seats) and that cost was built in. Not anymore-that would be too kind to its customers.

Delta continues to innovate and apply additional usage fees on its services, simply because it can. This may enhance top-line and bottom-line growth, but it could also alienate middle-class to lower-class fliers. Delta is one of the four major US airlines (Delta, Southwest, United, and American), which account for 74% of US airline tickets. This shows the companies' pricing power, which can be advantageous, but may seem exploitative to some. This could ultimately drive customers away or cause them to fly less frequently.

Delta's financials are not strong. Expenses and costs are always varying, which causes their earnings to fluctuate.

Delta EPS History (Koyfin)

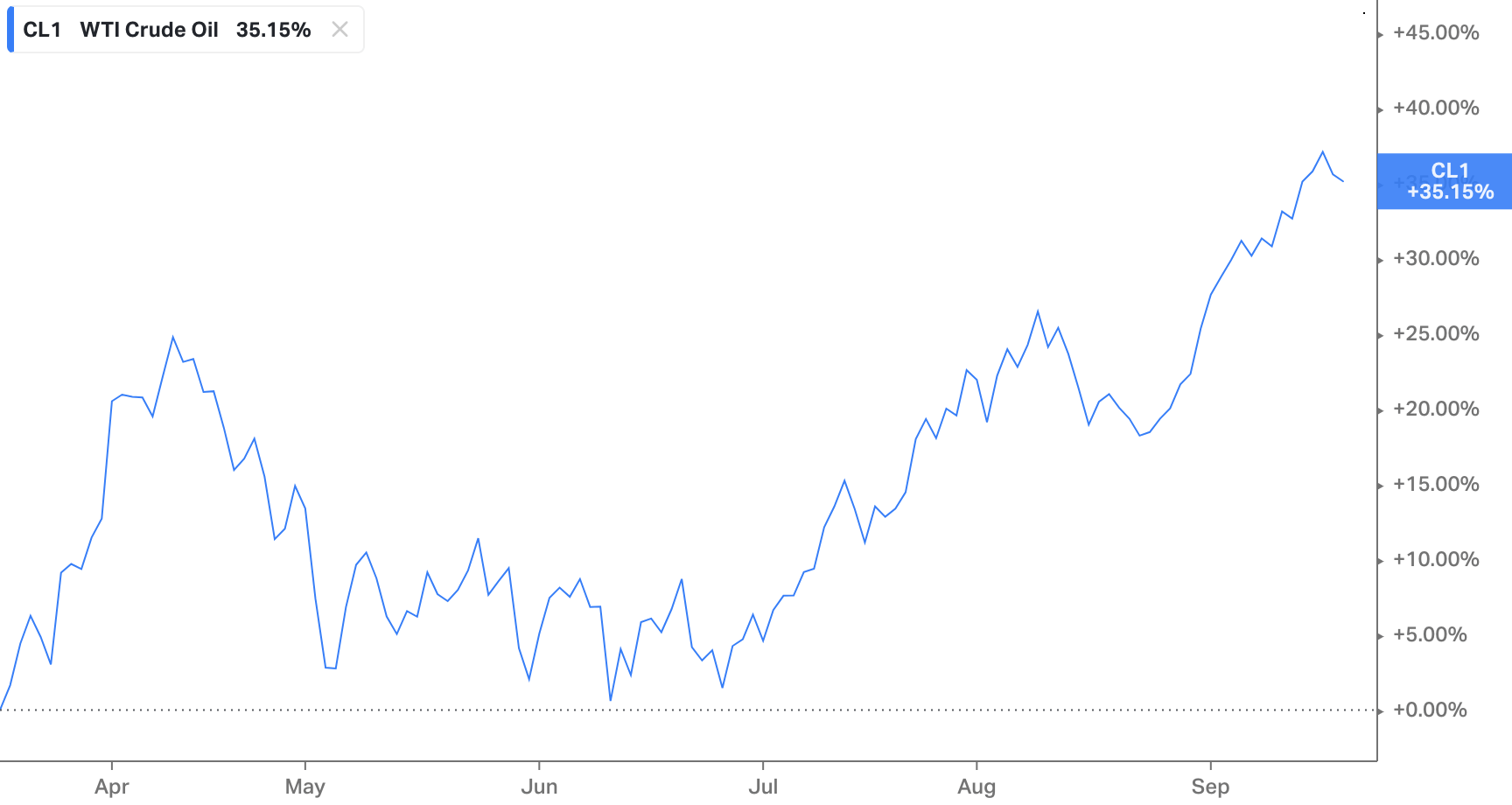

Delta has too many operating cost factors to make them a safe investment for me. Employee costs are rising and always changing, oil looks like it is heading to $100 a barrel (oil prices are up 35% in the last 6 months), planes are aging and being recalled due to Raytheon ( RTX ), which caused engine issues .

The recall issue affects the Airbus A320neo family of narrow-body airliners. Delta happens to be one of the largest customers of Airbus. A Bloomberg Intelligence analyst George Ferguson said in an interview "U.S. airlines with the largest fleets in service using the affected engine include Delta Air Lines and the ultra-low cost Spirit Airlines Inc. ( SAVE ).

All of this will affect bottom line profits. DAL now expects lower Q3 earnings per share of $1.85-$2.05 (prior expectation $2.20-$2.50) versus consensus of $2.32. Plus, operating margins are now expected to be approximately 13% (previous expectation was in the mid-teens).

{kind=link}

DAL is down roughly 6% in the last three months, but is still up 20% year-to-date (YTD). There is no doubt that demand has been high, with tailwinds pushing the company higher post-pandemic. This has allowed Delta to charge higher prices, but that will not last much longer. Credit card debt is rising, rates are still high and possibly still going higher, and inflation is still looming, all showing that the economy is still not in a good place.

With summer 2023 now over and trips to Europe and the lake/beach slowing, I expect DAL shares to continue their pullback. Just look at Southwest, which hit a 52-week low a week from today (9/13/2023). I know the holiday season is just around the corner for the airline, which historically sees high demand for air travel. However, I don't think this catalyst will be enough to push DAL to a new 52-week high. Costs are still going up, especially oil, and I think customers will turn to cheaper airlines with lower costs when flying. Not to mention those who may just choose to wait until next year.

DAL loves to find new ways to charge customers, and eventually, their customers will be tapped out. Airlines in general generate little cash flow, and that is why I suggest staying away from Delta as a long-term investor.

Fundamentals

Right off the bat, I want to emphasize that Delta and airlines do not generate a lot of cash. This makes the stock a wild ride (1.3 beta) with a lot of added risk with little reward.

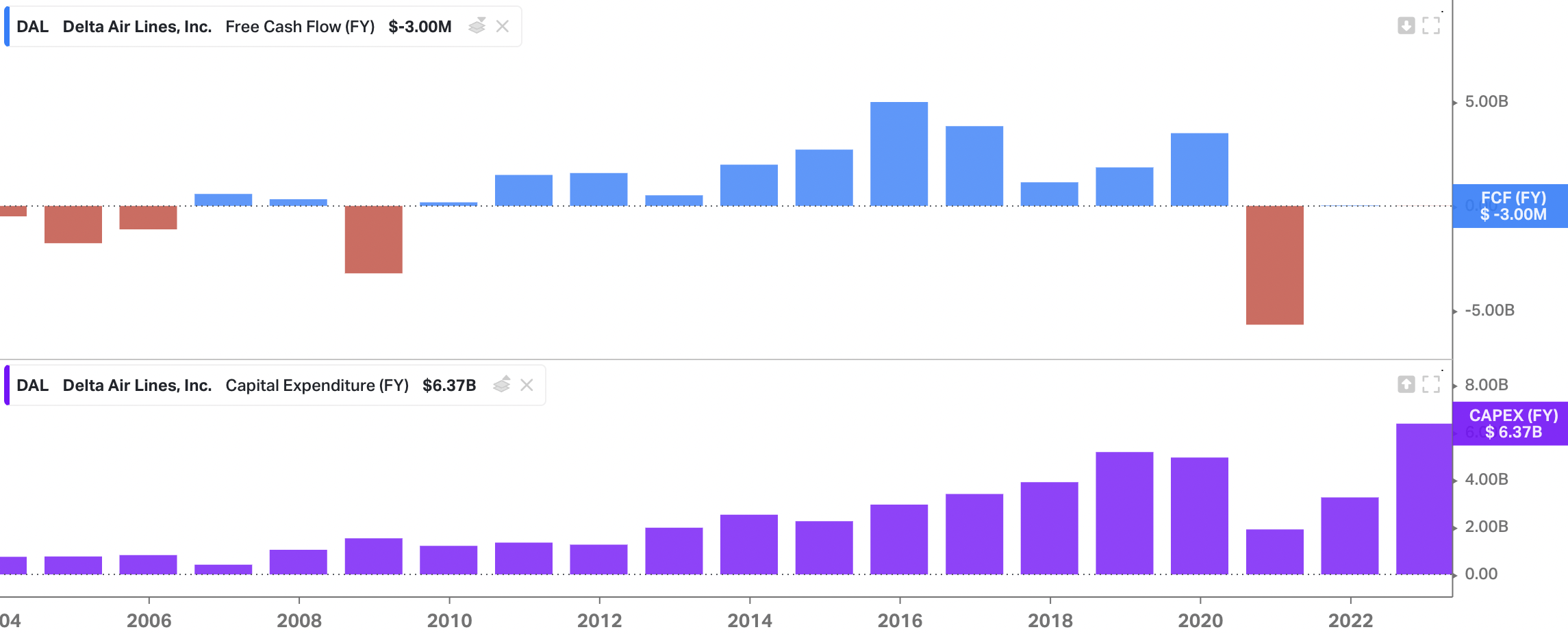

According to my calculations, DAL has a 3.18% free cash flow ((FCF)) yield, well below the 8% I look for (trailing twelve months ((TTM)) FCF of $806 million). Capital expenditures have been greater than net income every year since 2016 for Delta, meaning they are spending more money on operations and expansion than they make each year. They have little money left to return to shareholders.

{kind=link}

Their lack of cash flow has also been evident in their weak dividend. I know the pandemic had a big effect on the stock and cash flow, but I am still not impressed. From 2013 to 2019, Delta raised its dividend per share ((DPS)) each year at a respectable rate. However, they cut it in 2020 and canceled it in 2021 and 2022. They have reinstated the dividend at $0.40, which is where it was cut to in 2020 wiping all the DPS growth away from 2014 on. I expect them to try to grow their DPS over the coming years, but may be tough given the low amount of cash flow and high CAPEX. They will have to continue to invest in the newest and best fleet of planes along with satisfying customers and staff.

Investors hoping to get a better dividend and that DAL will be a safe bet are hoping in vain, which is not an investment strategy. DAL is a cyclical stock that people can invest for mid-term time ranges with the movement of the economy. Buy DAL in the low 30s, and sell in the high 40s.

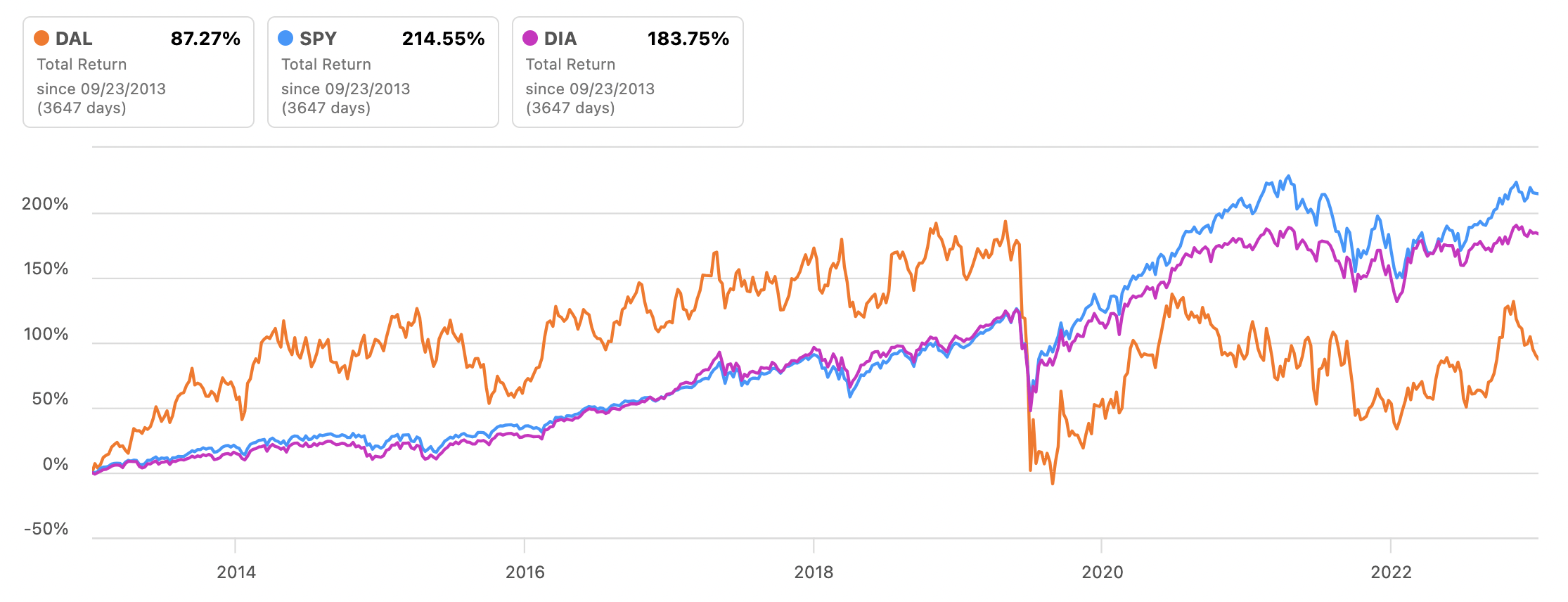

Long-term, DAL has failed to live up to expectations so far. You can look at DAL on a 3-year, 5-year, 10-year, or even since its inception, and it still underperforms the S&P 500 and Dow Jones. Delta is a utility, a necessity for our lifestyles, but that does not make it a good investment. I like flying with them, but I hate the stock.

DAL Total 10 Year Return Comparisons (Seeking Alpha)

{kind=link}

My Price Targets and Stock Range

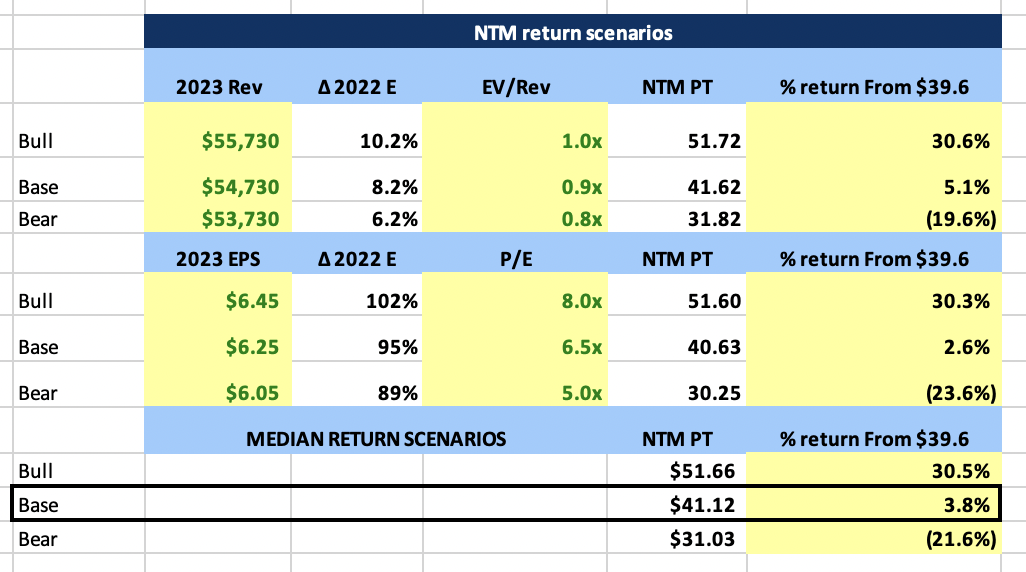

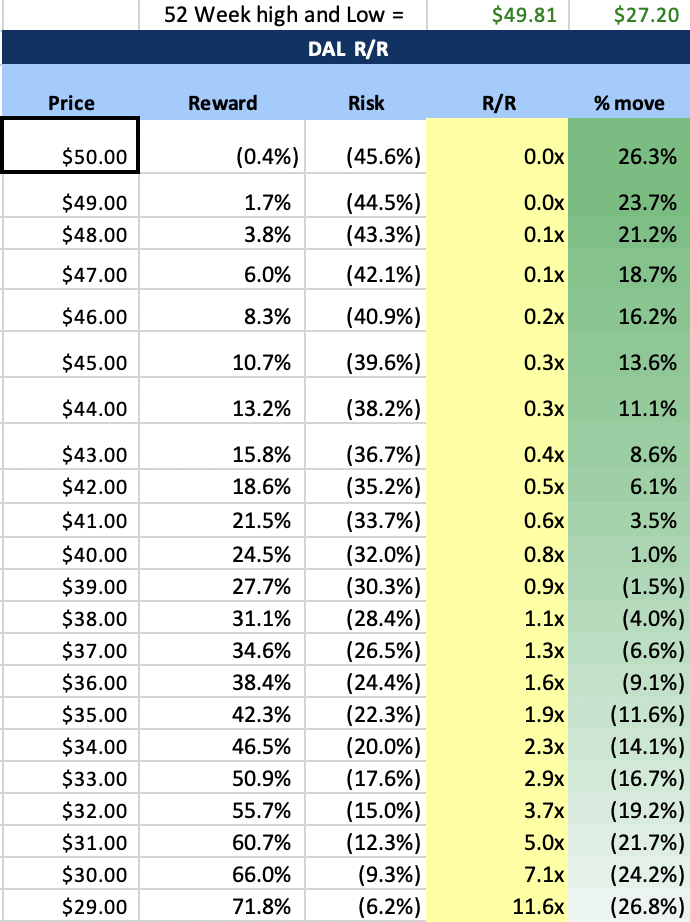

Based on current analyst estimates and valuation, I rate the stock as fairly valued. My fair value NTM price target is $41 a share, a 4% upside. DAL is trading at 6x price to earnings, which I believe is reasonable given the risk and uncertainty around the industry and demand. My risk-to-reward (R:R) for the stock is 0.9x, which isn't appealing and below the 3x R:R I prefer and see as a safe investment. DAL is roughly 20% from its 52-week high, but 30% away from its 52-week low.

Again, I want to emphasize how important the timing of any DAL investing is. Long-term, DAL has really gone nowhere, but you can find pockets in time and catalysts when the stock outperforms. Earlier in 2023 was one of those times, as demand was booming post-pandemic. Now life and trends have caught up to DAL, and that is why I suggest not owning the stock.

I have attached my NTM price target scenario below, along with my risk-to-reward chart. As you can see, R:R drastically increases as the stock falls. Long-term investors should stay away, but traders may look to enter as the stock moves down to the low $30s.

DAL NTM Price Target Scenario Table (Author Calculations Based on Analyst Estimates From Koyfin Data) DAL Risk to Reward Chart (Author Calculations)

{kind=link}

{kind=link}

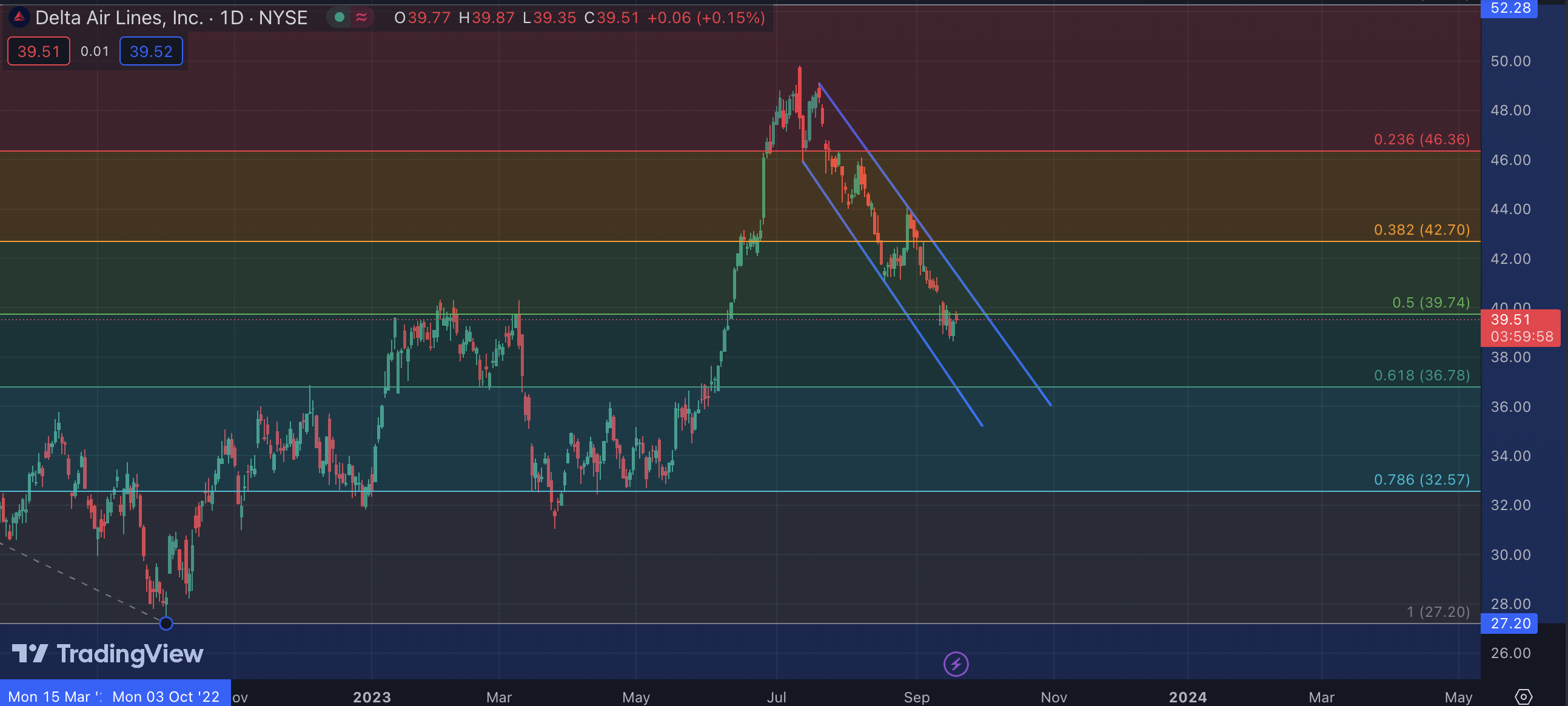

Looking at the stock's chart now, DAL is in a steep downtrend. It is currently testing a crucial support/resistance level at $39.74, and if it closes well below that, I believe $36 will be in play in the next week or two. Until I see the stock making higher highs and lower lows, I will continue to stay away from the stock and not even suggest it to traders. In my opinion, DAL is headed lower through September and October. The next big catalysts to watch for the stock are Q3 earnings (which I don't expect to be strong) and the holiday season starting with Thanksgiving at the end of November. Until then, I suggest staying away.

DAL Stock Chart (Technical Analysis) (TradingView)

{kind=link}

Article Takeaways

Delta is a phenomenal airline with great services that meet customers' needs. However, I believe they may be pushing their luck with customers with add-on fees. They are finding new ways to charge customers, which I believe will backfire and drive customers to competitors. American ( AAL ), Southwest ( LUV ), and United ( UAL ) all offer nearly identical offerings, which gives Delta no moat.

Airlines as a whole are not very profitable, with low cash flow and high operational expenses. DAL has underperformed the market as a whole in the past, and I expect that to continue into the future. They are simply a utility with low margins and little cash generation. I can think of more than a dozen better investment ideas that are safer and offer more risk-adjusted returns than DAL. There is a time to trade DAL in certain economic conditions, but now is not the time to own the stock.

For further details see:

Delta Air Lines: Input Cost Rising, Summer Travel Over