GE - Delta Air Lines Is Still Head And Shoulders Above The Rest

2023-10-24 01:16:38 ET

Summary

- Delta Air Lines stock has outperformed its competitors in the U.S. airline industry, holding onto gains over the past year.

- Delta is building on a long list of successes to transform its business and further distinguish itself from the industry.

- Delta's success can be attributed to its strategic focus on increasing premium revenue, improving operational reliability, and diversifying revenue sources.

- A major widebody aircraft and engine maintenance decision remains as Delta keeps its customers, employees and stakeholders on its side.

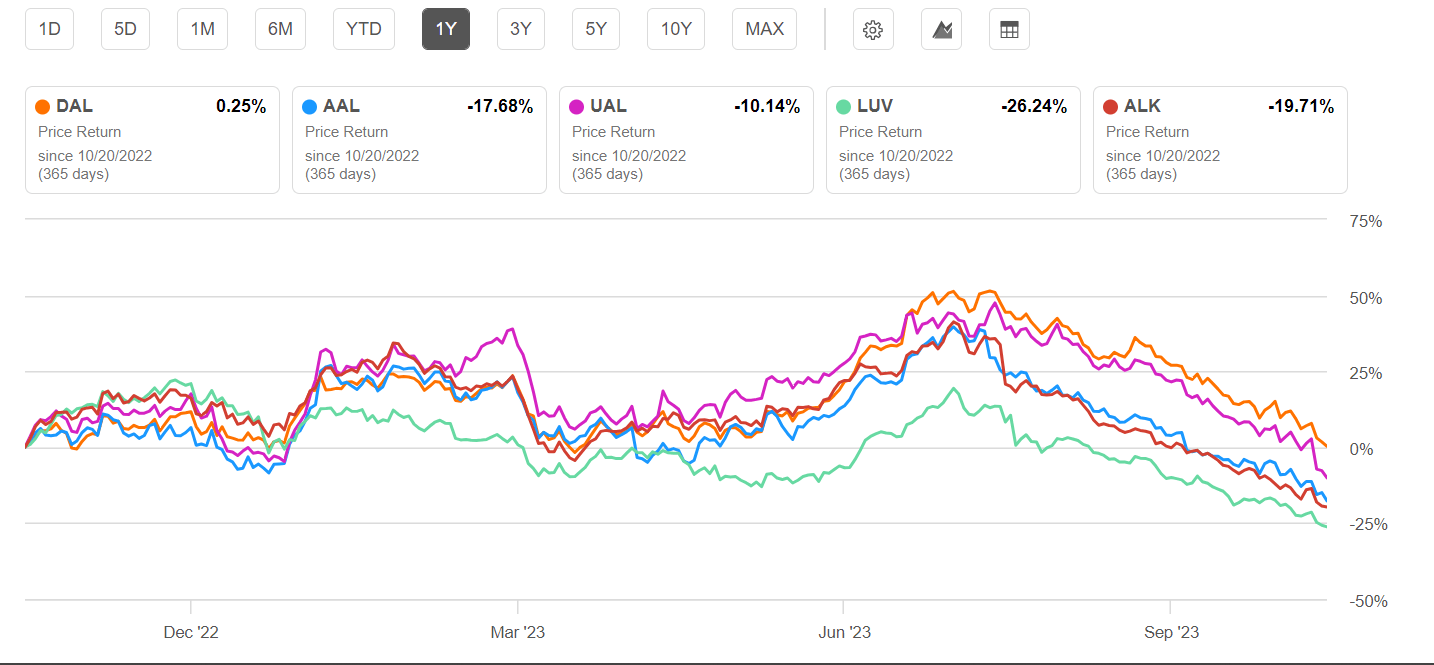

Airline stocks have seen a very turbulent 2023. After low fuel prices early in the year and the promise of a strong summer, macroeconomic fears which included increasing fuel prices and weakening domestic demand began to rattle airline stocks. By late summer, most of the U.S. airline industry had given back all of its gains over the past year. Delta Air Lines ( DAL ) is one of the last U.S. airline stocks to hold onto any gains over the past year, up fractionally as of market close on Friday 20 October 2023. In this article, I will examine why DAL stock has outperformed its direct competitors, dynamics that are influencing the industry, and how DAL will be able to keep its momentum going in the midst of performance declines for certain U.S. airlines. I last reviewed DAL in July 2023 in this Seeking Alpha article . Given the challenges the industry has faced and in light of the third quarter 2023 earnings releases from the big 3 U.S. global airlines, it is worth asking if the "Strong Buy" from July is still warranted.

DAL to industry 1 y4 chart 22Oct2023 (Seeking Alpha)

{kind=link}

United Airlines ( UAL ) CEO Scott Kirby grabbed the headlines when he stated in that company's 3rd quarter earnings call that the low-cost carrier model was broken and unsustainable and that the majority of U.S. airline industry revenue and profit growth would come from Delta and United. Scott Kirby's style has long included comparisons of UAL's performance to other airlines; when he took the helm at UAL seven years ago, he said his goal was to deliver performance comparable to DAL which has been regarded for years as the industry's financial leader. Not only did Kirby take a swipe at the low-cost carrier segment but also at American Airlines ( AAL ) where Kirby was employed before heading from N. Texas to Chicago to lead United.

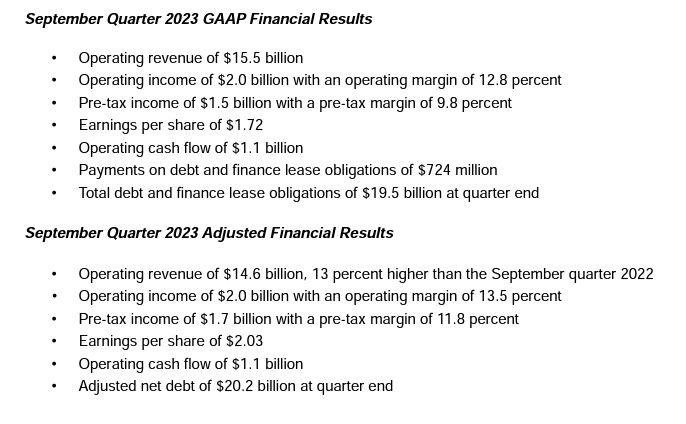

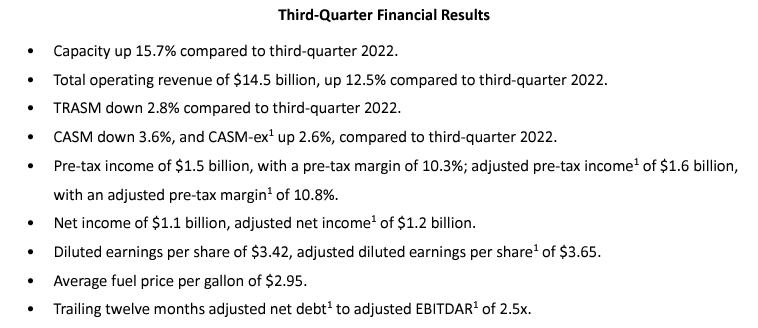

United's strategies over the past year have been very similar to those which Delta implemented over the past 15 years: increase premium revenue, improve operational reliability, improve the customer experience and onboard product, reduce the reliance on regional jets while growing the mainline (large jet) fleet, and increase aircraft gauge or the average number of seats per flight. United has its own distinctives including a historically larger percentage of revenue from large coastal markets than Delta and a larger percentage of revenue from international markets but the two posted not only the closest revenue and profits the two have recorded in years but also similar bottom line results. The following data highlights the revenue performance between the two megacarriers from DAL and UAL 's 3rd quarter earnings releases.

DAL 3Q2023 summary results (ir.delta.com) UAL 3Q2023 summary results (ir.united.com)

{kind=link}

{kind=link}

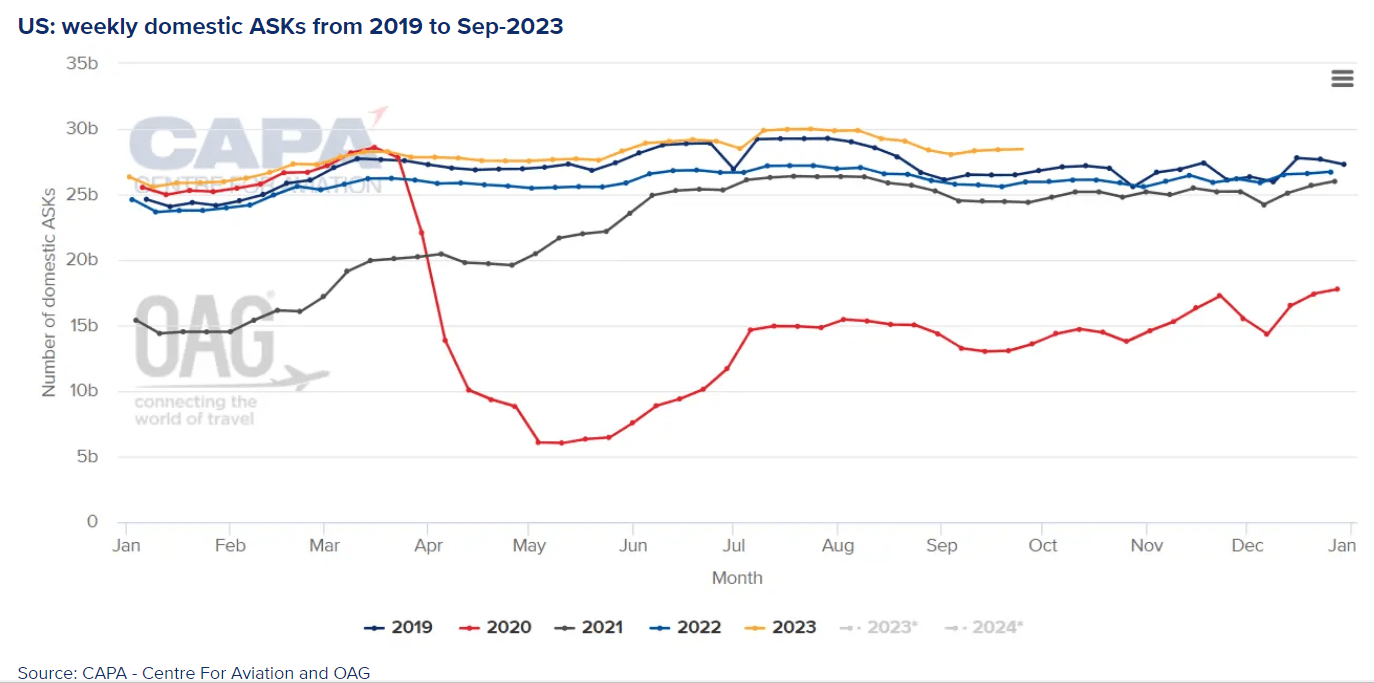

While Delta and United notched similar impressive results, competitor American didn't fare so well while smaller Alaska ( ALK ), also a legacy (pre-1978 interstate) airline had a decent 3rd quarter. The low-cost carriers including Southwest ( LUV ) have yet to report but are not expected to come close to the strength which Delta and United showed. The factors which have helped Delta and United outperform in the current environment include being able to grow revenue and profits in an aviation system that is heavily constrained due to new aircraft delivery delays esp. from Boeing ( BA ) as well as Air Traffic Control staffing shortages which have cut the capacity which a number of U.S. airports can handle. Add in soaring labor costs and growing shortages of skilled aviation labor and the ability of the low-cost carrier model to effectively compete against legacy carriers has never been more challenging.

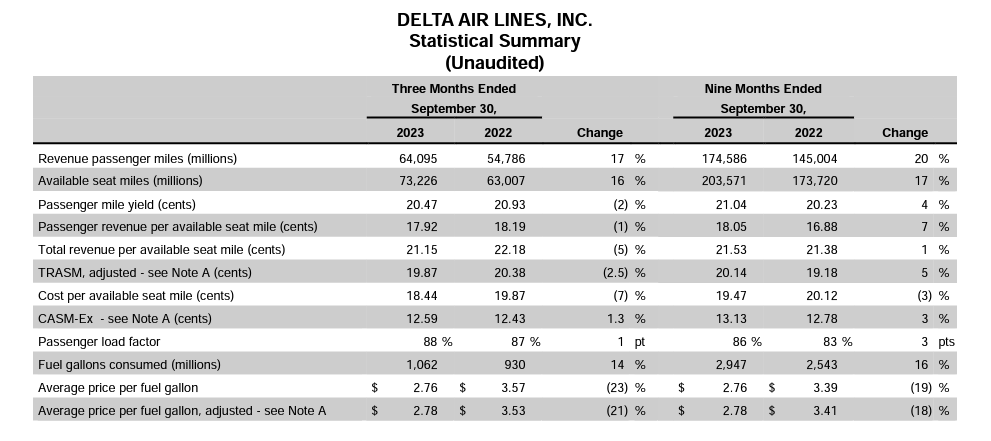

US domestic airline capacity (OAG/CAPA) DAL 3Q2023 regional revenue (ir.delta.com) DAL 3Q2023 statistical summary (ir.delta.com) UAL 3Q2023 revenue and statistical summary (ir.united.com)

{kind=link}

{kind=link}

Delta and United 's guidance and full year 2023 earnings highlight some of the distinctives between the two companies. It is clear that, while United had a strong summer season, they underperformed Delta earlier in the year and are expected to do so in the winter as they usually do; United has one of the smallest positions in Florida among U.S. airlines and has a smaller Caribbean operation than American or Delta. In addition, Delta earns far more revenue in the "other" category than any other U.S. airline and likely any other airline in the world. We'll get into what is in that "other" category but it is clear that a big part of Delta's financial difference with United, even as well as United is operating right now, is due to a much greater level of revenue diversification which is a key driver behind Delta's higher profits.

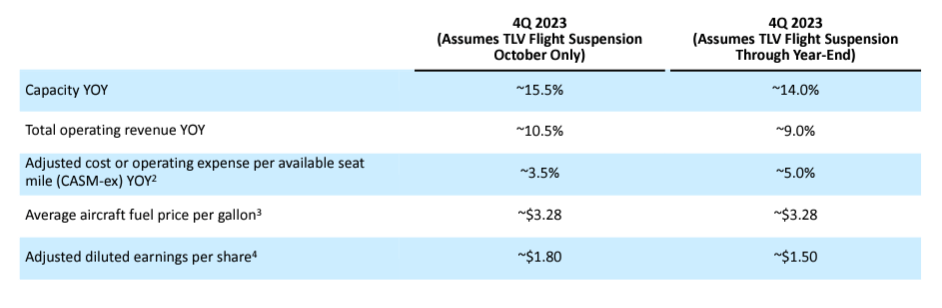

DAL 4Q2023 guidance Oct2023 (ir.delta.com) UAL guidance 4Q2023 as of Oct (ir.united.com)

{kind=link}

A Growing List of Delta Successes

With an understanding of current industry dynamics, let's look at Delta's distinctives and how they position that company to remain financially at the top of the industry. The underlying principle that underlies Delta's financial success is that it has spent decades, esp. the two decades since 9/11 reshaping itself and thinking much further out strategically than any other airline. It has also intentionally articulated its goals and strategies to investors and has executed them to a level of consistently that has been rare in the airline industry. While Delta has had changes in leadership over the near century that it has been flying, there is a strategic consistency that is rare at a public company that has operated that long.

- Although it was not one of the original "chosen" airlines by the U.S. government and did not win the early airmail contracts that shaped the industry, Delta has grown from a small player in the then-insignificant U.S. South to the most profitable and highest revenue airline in the world.

- Delta was financially conservative and outperformed its peers financially long before the U.S. domestic airline industry was deregulated - and that continues today.

- Delta has long had well above average employee relations and below average rates of unionization in the transportation sector which has been plagued by labor unrest. In many years, Delta has paid more profit sharing than any other company in the U.S. and has paid more profit sharing than any other airline in the world over the past decade.

- Delta has long been more efficient and enjoyed better consumer relations as measured by the U.S. DOT.

Within the past 20 years, Delta recognized that:

- The profitability of regional jets would fall even though Delta then had the most regional jets under contract of any U.S. airline. Delta worked to reduce its reliance on regional jets and has now eliminated 50 passenger regional jets even while adding larger, more efficient mainline jets including the highly efficient Airbus A220 and the Boeing 717. Delta contracts for hundreds fewer regional jets than American or United.

- Delta recognized its lack of presence in major coastal markets and its overreliance on its hubs in the interior U.S. and has grown to be the largest airline at Boston, both New York LaGuardia and Kennedy airports as well as Los Angeles.

- Delta recognized the importance of long-term strategic partnerships and of having an influence on the operation of those airlines and has acquired equity stakes in seven major airlines around the world; those equity stakes often come with board seats and most of those partnerships are also part of antitrust immunized joint ventures, incentivizing the maximization of both airline's networks and operations, a more in-depth approach than is taken by other airlines.

- Delta recognized the value of operational reliability and customer-friendly service and consistently performs at the top of the industry in those areas, translating that into brand preference by business travelers; Delta carries more contracted business travel revenue than any other U.S. airline.

- Delta recognized the power of non-transportation revenue and now receives more revenue from its loyalty program and credit card partnerships than any other airline. Delta has also transformed its aircraft maintenance division, Delta Tech Ops, so that Delta has one of the lowest unit costs for maintenance among large global airlines but also making Delta Tech Ops the largest provider of maintenance services to other airlines in the Americas.

- Delta purchased a refinery which is tuned to maximize jet fuel production, consistently reducing Delta's four billion gallon/year fuel bill by a minimum of a couple cents per gallon and resulting in fuel cost savings over $1 billion in some years.

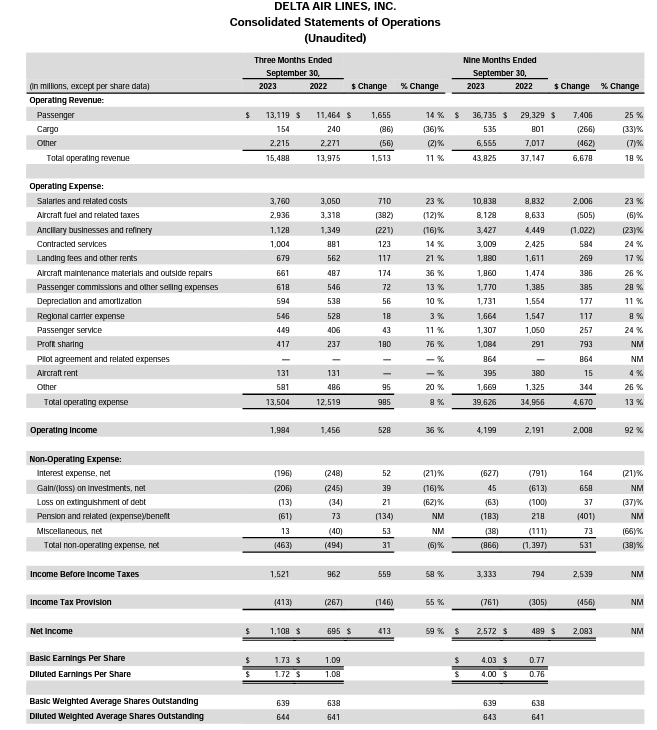

DAL income statements 3Q2023 (ir.delta.com)

{kind=link}

Delta used the covid pandemic to further strengthen its competitive and financial position relative to its competitors.

- Delta retired a couple dozen aircraft during the pandemic and now has the most fuel-efficient fleet among the big 3 U.S. global carriers with fuel efficiency more than 5% higher than American and United.

- Delta acquired dozens of used aircraft during the pandemic so that it has been able to pay down debt even while growing as travel demand has returned, a strategy no other U.S. airline has used to the same degree.

- Delta has enhanced its individual seatback entertainment system to customize the content for each passenger including features such as allowing a movie to be started on one flight and completed on another, all part of individualizing the travel experience and building a direct and personalized customer relationship, the opposite of the commoditization of air travel that is the approach some airlines use.

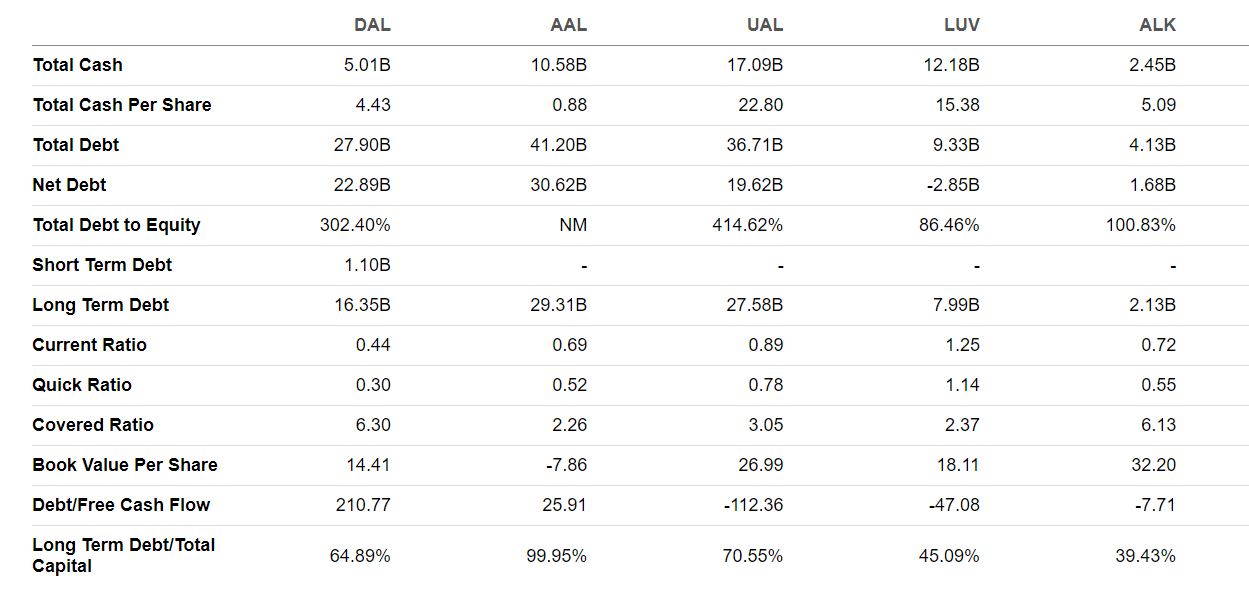

DAL to industry balance sheet 22Oct2023 (Seeking Alpha)

{kind=link}

In the coming months and years, Delta's revenue and profit growth will be supported by:

Delta will continue to maintain a strong domestic presence although international has been particularly strong; in 3Q2023, 67% of DAL's 2023 passenger revenue came from domestic and 33% from international markets. In contrast, only 58% of UAL's revenue came from domestic markets, making it the most vulnerable to global downturns.

Delta will continue to develop its relationship with its global alliance partners. Its largest and longest partnership is with Air France-KLM ( OTCPK:AFRAF ) which faces the challenge of an increasing restless Dutch populace and government that wants to limit the size of Amsterdam airport where Delta operates more flights to the U.S. than KLM. Delta and Air France have shifted some flights to Paris. Delta is already reaping the benefits of its young joint venture with Latam, the multi-country S. American airline. Aeromexico is rapidly expanding after the U.S. lifted restrictions on Mexican airlines due to safety concerns. In Asia, Korean Airlines' merger proposal with Asiana, facilitated by the Korean Development Bank, appears less and less likely ; Delta execs said they expect to announce new Delta routes to Seoul where expansion has been on hold as Delta has tried not to negatively impact negotiations with regulators in the U.S. and the EU.

Delta's purchase of a refinery in 2012 raised a lot of skepticism within the business community. Delta bought its 185k bbl/day Trainer refinery outside Philadelphia from Phillips 66 and tuned it to maximize jet fuel production using incentives from the state of Pennsylvania. Delta's intent was always for the refinery to reduce its jet fuel bill rather than be a to be profitable on a standalone basis; as a wholly owned subsidiary of Delta, the standalone financials of the refinery have to be reported to investors and yet in 2022, Delta saved 23 cents/gallon off of each of the 3.5 billion gallons of jet fuel its aircraft used, saving the company nearly $1 billion. While the savings are not expected to be as high in 2023, the refinery is now consistently saving Delta double digit cents per gallon. Although United considered buying its own refinery, that effort was not successful and Delta remains the only airline in the world that uses its own refinery, rather than crude oil hedges, to reduce its fuel bill. Since part of the savings that Delta gains via the refinery is attributable to the cost to refine crude oil into jet fuel, the reduced refinery capacity in the U.S. Northeast and the growing number of electric vehicles will likely ensure that Delta's cost advantage is not diminished and has the potential to grow even further.

Delta will continue to grow its loyalty program and American Express ( AXP ) revenue from $7 billion to $10 billion.

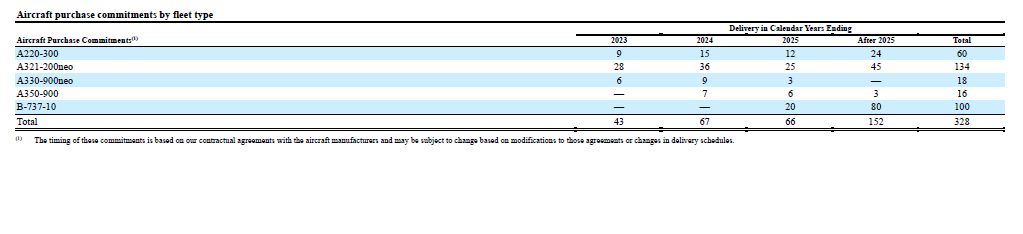

DAL aircraft commitments by type 31Dec2022 (ir.delta.com)

{kind=link}

Fleet-Related Decisions Remain

Two other major strategies that are still under development and awaiting public decisions are both fleet related.

Delta is still expected to announce an order for new widebody international aircraft, one year after Delta executives told employees that they were seeking board approval for the purchase of approximately 20 Airbus ( OTCPK:EADSY ) A350-1000s and additional A330-900s. Delta operates nearly every model of commercial aircraft flown by western airlines with the exception of the Boeing 777 and 787. Delta retired its fleet of 18 777s, composed of both the 777-200ER and the very long range and highly capable -LR model, during the pandemic. The A350-900 became Delta's flagship and primary long-range aircraft. However, as I have noted in other articles, airport boarding data shows that Delta has likely experienced significant payload restrictions on some of its A350 routes which include 8000 mile segments from Atlanta to S. Africa and S. Korea. It should not be surprising if Delta does experience payload restrictions; the majority of its current two dozen plus A350-900s are early production, less capable models, with a second set of more capable models, and just two of the newest and most capable models. Delta has 16 more A350-900s due for delivery over the next 3 years and all are expected to be the most capable models which should eliminate any payload restrictions as the airline can use its "best" aircraft on the longest and most challenging routes. Its "less capable" A350s still can comfortably fly 12-14 flights, comparable to routes the 777-200ER did, but with fuel savings of 25%. The A350-1000 is an even larger version of the A350 model and both operate some of the longest routes in the world.

Delta also operates a fleet of 65 A330s including the -900NEO. Airbus re-engined its best selling widebody (second in sales only to the Boeing 777 family) with new generation engines similar to those found on the B787 but is able to build the A330-900 for much less than other new aircraft because the A330NEO is a derivative aircraft. Slightly smaller than the A350-900, the A330-900 is used by Delta for flights of 12-13 hours or less, leaving the A350s to focus on longer routes.

Because Delta chose the A350/A330NEO combination, it has not ordered the 787, Boeing's popular new generation aircraft which, like the A350, is made of lightweight carbon fiber reinforced polymers. As Delta's decision nears regarding another widebody aircraft order to extend its deliveries past 2026, the Boeing 787 might be a consideration at Delta even though Delta has not bought a widebody aircraft from Boeing in 20 years.

DAL aircraft commitments 31Dec2022 (ir.delta.com)

{kind=link}

Resolution of the aircraft order appears to be centered around Delta's ability to overhaul the engines on its new widebody aircraft in its own shops instead of sending those engines out to other facilities. Delta noted that the deciding factor in its decision a decade ago to buy its widebody aircraft exclusively from Airbus was being granted engine overhaul rights by Rolls-Royce ( OTCPK:RYCEY ) which exclusively powers all new-generation powered Airbus aircraft including the A330-900 and A350. The A350-1000 is powered by a modified version of the engine that powers the A350-900 which Delta operates; Delta has the rights to not only repair its own A350-900 engines in-house but also to sell its engine maintenance services to other airlines. Aircraft engine overhauls typically are required every 5-10 years but cost millions of dollars per engine; highly skilled work, engine overhauls command healthy double digit profit margins. The engine makers themselves operate their own engine repair shops but have a network of authorized shops, often affiliated with or derived from some of the largest global airlines. Delta had expected to be able to win the engine overhaul agreement for the A350-1000 but Rolls-Royce has apparently not been willing to grant Delta those rights.

Sensing opportunity, General Electric ( GE ), which has the largest sold engine share on the Boeing 787, has agreed to grant Delta rights to overhaul the GEnx engine that powers the Boeing 787 family. General Electric and Safran (SAFRF) granted Delta overhaul rights for the LEAP engine that exclusively powers the Boeing 737MAX order, leading to a 2022 order for the MAX 10, the largest member of Boeing's narrowbody aircraft family. Delta also won engine overhaul rights for the Pratt and Whitney RTX narrowbody domestic Airbus aircraft that Delta has on order. In total, Delta has rights to maintain the engines on every new aircraft it has on order as well as sell those services to other airlines.

Delta's choice for its widebody order appears to be either for the A350-1000 but without engine overhaul rights or for the B787 or for more A350-900s, the latter two with engine overhaul rights. The A350-1000 is the largest and most capable new generation aircraft under consideration by Delta, carrying up to 350 passengers on 16+ hour flights. The largest version of the Boeing 787 family, the -10, is highly fuel efficient and seats about 315 passengers in a configuration that Delta might use and can fly 12-13 hour flights but Delta would be giving up the opportunity with that aircraft to operate very long flights that are essential for many routes to Asia/Pacific destinations. With the 787-10 and without the A350-1000, Delta would rely on its A350-900s, smaller than either the B787-10 or the A350-1000, for very long flights. The mid-size 787, the - 9, has range slightly less than either version of the A350 and seats approximately 25 fewer passengers in a comparable configuration to Delta's A350-900s; since larger aircraft size helps offset the higher operating costs of long flights and Delta already operates the similarly sized A330-900 but which is less capable than the B787-9, there are few reasons why Delta would order the 787-9 unless they completely walk away from Rolls-Royce - powered aircraft.

Given that even some of Delta's Rolls-Royce powered engines have suffered from reduced time between overhauls and operational issues which have reduced the usefulness of the airplane, Delta's best bet to gain manufacturer credits such as are commonly given in the aviation industry when a product fails to perform as guaranteed is by continuing to order some Rolls-Royce aircraft. In addition, Airbus is undoubtedly fighting to not lose even part of a major order from a blue-chip company like Delta and could offer further incentives or even further reduce the price of its aircraft to compensate for Rolls-Royce's unwillingness to negotiate an engine overhaul deal on the A350-1000 which carries a list price of almost $400 million. Delta is the largest customer of the slow-selling A330NEO so Airbus has plenty of reasons to ensure Delta keeps ordering the A330-900 which could be a very suitable replacement for Delta's fleet of 66 Boeing 767s which will come to the end of its life over the next decade.

Delta could also be telling Airbus that it will order A350s and more A330NEOs for delivery after 2030 when Rolls-Royce's exclusivity ends and GE can provide an engine.

Delta appears set to gain not only a cost advantage in the acquisition of its new aircraft but also further develop its engine overhaul business revenue which they have said should increase to $5 billion over the next decade, further growing DAL's profits using unique strategies. While Delta execs downplayed that it might profit from the massive number of inspections and repairs to other airlines' Pratt and Whitney Geared Turbofan engines, it is clear that Delta's maintenance services will increasingly grow even indirectly from work done for its competitors and those services could deliver $1 billion more in profits for DAL in the next 5-7 years.

Delta's most recent employee communications indicate that a widebody decision should come before the end of the year.

Keeping Stakeholders on Delta's Side

Delta's final challenge is to continue to manage and grow the loyalty of its stakeholders including its customers, employees, and stakeholders. As previously noted, Delta's loyalty program, SkyMiles, has been extraordinarily profitable for the company and is closely tied to its relationship with American Express. Delta says it is on target to exceed $6 billion in revenue from SkyMiles this year and believes it can attain $10 billion in revenue by the end of this decade. Part of the benefit of airline-affiliated credit cards is increased accrual of elite benefits as well as access to Sky Clubs, DAL's airport lounges. Although all mainline and regional aircraft under its control offer premium cabins and Delta has more square feet of airport lounge space than any other airline, Delta has increasingly seen customer to enter Sky Clubs and long waitlists for elite upgrades. Recognizing that it doesn't have the ability in its system to serve the number of elites it has, Delta implemented a number of changes to increase elite qualification and limit Sky Club access that it hoped would end the multiple piecemeal attempts it has tried over the past couple years. The points and miles blogosphere registered large levels of discontent although Delta says, predictably, that it has received it has also received much positive feedback. Nonetheless, Delta announced revisions to some of the changes it previously made while also noting that it is comfortable that it is moving in the right direction but moved too quickly. In its earnings call, Delta execs affirmed they are on track to reach their SkyMiles revenue goals, indicating that they and AXP not only were closely monitoring a number of indicators and decided, at the least, that modest revisions could help calm social media - and that has been the case since the revisions were announced. As the big 3 U.S. global airlines become stronger relative to their competition and as affinity credit cards are as heavily used by American consumers, it is not unreasonable to think that further revisions will be coming not just at Delta but also at other airlines.

The second stakeholder group which Delta must ensure remains on its side is its employees. Delta led the industry with post-covid pay raises, first for its pilots and then for its non-union employees including pay during boarding for its flight attendants, a first for a large U.S. airline. In addition, Delta execs noted on its recent earnings call that it had accrued $1 billion in profit sharing for the first nine months of 2023, setting Delta employees up to receive a profit-sharing check on Valentine's Day 2024 amount to a healthy double-digit percentage of their 2023 earnings. Based if nothing else on Delta's earnings leadership in the industry, Delta employees will remain some of the best compensated airline employees in the world. Delta's founder has long recognized that paying and treating its employees well encourages them to take good care of Delta's customers. Given that Delta consistently ranks at the top of industry customer service metrics, Delta revenue and profits benefit from the company's generous compensation. Still, keeping 80,000 employees happy and engaged involves more than just money. The entire airline industry, like many American companies, continues to deal with higher levels of attrition, changed mindsets about work, and a greater desire to work from home, an option that most airline jobs do not afford. Nonetheless, Delta employees have put the company on Glassdoor's list of Best Companies to Work for seven years.

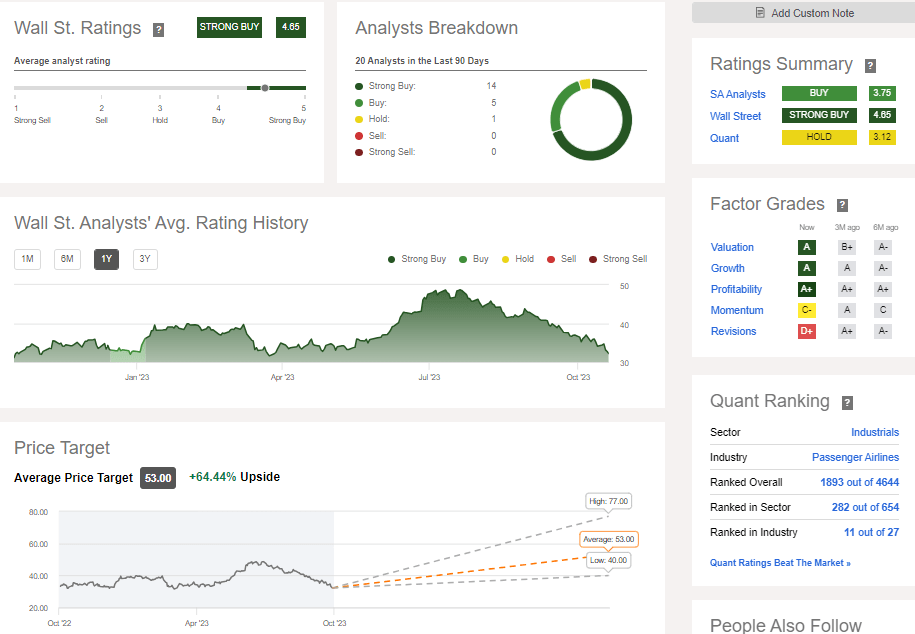

DAL Wall Street ratings 22Oct2023 (Seeking Alpha)

{kind=link}

The final stakeholder group that Delta must satisfy is its investors. Delta remains at the top of the global airline industry in terms of market cap, profitability, and total revenue. DAL reinstituted a dividend which sports a 1.24% FWD yield, just under half the level for Southwest.

DAL's balance sheet looks healthier than its global competitors but not as healthy as stalwart LUV which is posting much lower profits both than Delta and what LUV historically has reported.

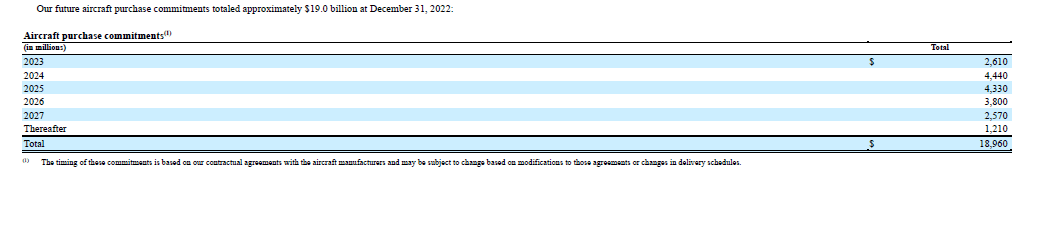

DAL's aircraft capex of $19 billion is modest and should allow the company to not make incremental aircraft orders, particularly considering that DAL's aircraft spend is half of UAL's at its highest levels and one-third of UAL's levels in total. DAL generates sufficient cash to opportunistically reduce its debt and continues to pursue a return to investment grade credit ratings.

Wall Street analysts still collectively rate DAL a strong buy with an average price target of $53 for a 66% upside.

Airline Stocks are Not Fan Favorites

Although airline stocks including 2023 enjoyed a healthy first half of 2023, the selloff in the 2nd half of the year highlights that airlines are rarely viewed as long-term investments by most retail investors. Delta's risks include:

1. Macroeconomic factors including inflation and high interest rates appear to be impacting low cost carriers more than legacy carriers but Delta is not immune to travel reductions which might come from tighter business travel budgets.

2. Jet fuel remains DAL and most airline's second largest expense. While Delta has strong fuel cost containment strategies, a sustained spike in fuel prices has been highly destructive to airline stocks and the same would be true today, esp. if it is part of global conflicts.

3. Delta has led the industry in labor cost increases but the revenue generation that supports those higher labor costs could quickly reverse, esp. if legislation is implemented that reduces the ability of card issuers including AXP to pay rich rewards.

4. While Delta has tried to diversify its fleet purchases from multiple manufacturers, production and durability issues in any model could quickly erode profits and Delta's operational reliability such as been seen impacting some low-cost carriers.

5. Customer backlash to Delta's SkyMiles changes could turn out to be much more significant than the company believes so far, eroding loyalty program revenues and creating opportunities for competitors.

While I believe that Delta has managed each of these risks, the historic swings in the airline industry indicate that managements rarely can accurately predict and manage all risks they face.

Rating and Price Target

In the midst of an uncertain world and economic environment and in an industry that rarely holds onto success, Delta Air Lines stock continues to earn a STRONG BUY rating, one of the very few in the industry.

I believe a $43 price target for DAL is possible within the next year and $55 within three years.

For further details see:

Delta Air Lines Is Still Head And Shoulders Above The Rest