DAL - Delta Air Lines: Likely To Get Through Macro Turbulence

2023-11-07 11:33:51 ET

Summary

- Delta Air Lines stock has declined over 30% from its summer highs, being dragged down by its peers.

- Factors contributing to the decline in airlines are due to higher oil prices, inflation/interest rates, and geopolitical threats.

- Despite the industry challenges, Delta released strong Q3 numbers and is expected to perform well in Q4, making it an attractive investment opportunity.

Delta Air Lines (DAL) is just getting beaten up right now and for no good reason. The stock is actually less than 1% down over the last year. But, it has given all the gains back from earlier in the year and is down over 30% from the highs in the summer. Delta is one of the lucky ones. Some of their competitors find themselves down over 30% in the last year. Rising costs and economic headwinds are going to lead to changes in the airline framework. When an industry that isn't going anywhere is getting hammered, it's time to pick the best companies in that industry and ride the wave back to some form of normalcy. In this race, my horse is Delta. They just released strong Q3 numbers and expectations are rising for Q4. It is time to buy the dip.

Is It Just Delta?

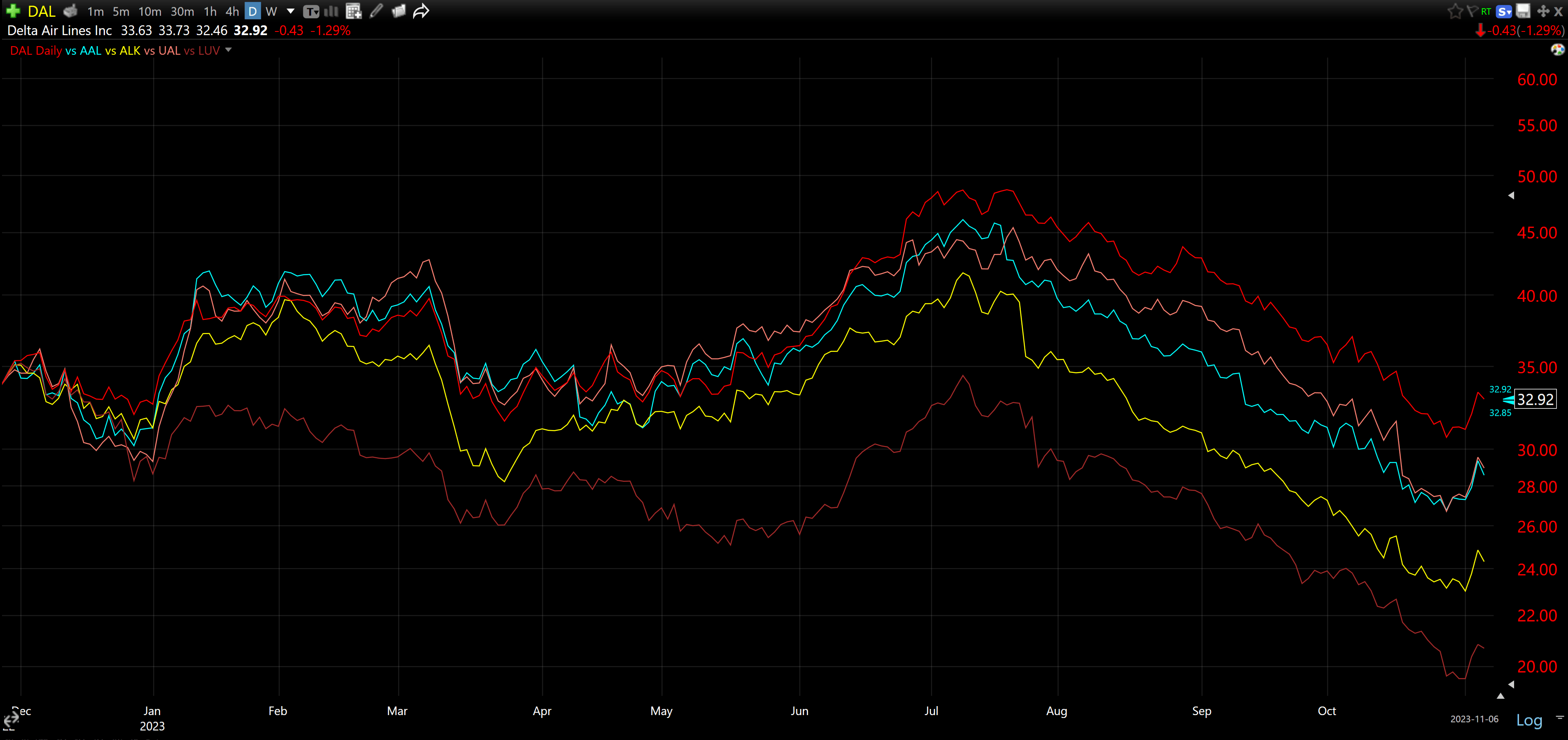

The good news here is that it isn't just Delta. Looking below you can see the entire basket is just getting hammered in the last few months. I have included American Airlines ( AAL ), Alaska Air Group ( ALK ), United Airlines ( UAL ), and Southwest Airlines ( LUV ). The positive I draw from this chart is that Delta is the best of the bunch.

{kind=link}

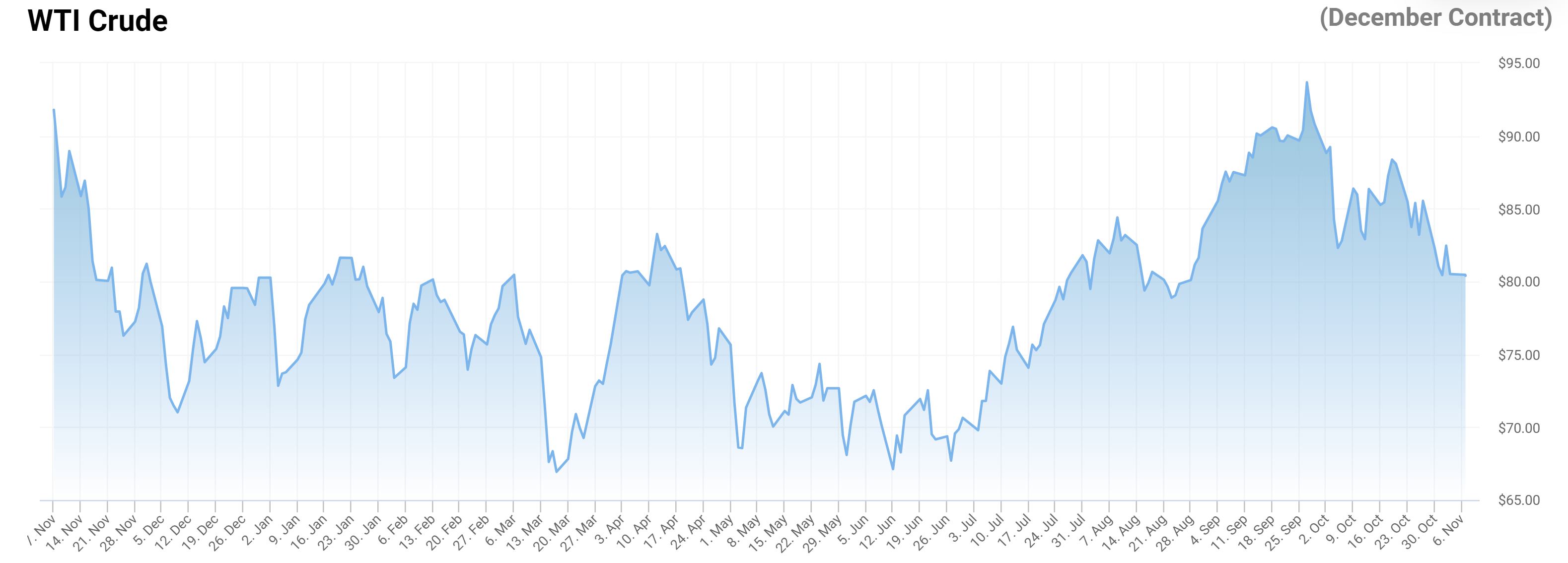

So what's going on here? In no particular order, I believe it's a combination of airline strategy change, higher oil prices, inflation/interest rates, and geopolitical threats. Starting with the most recent headline, which pertains to what's going on in Israel. We saw Delta fall up to ~5% on the 9th of October after the attacks began. With flights suspended, the immediate reaction is usually an overreaction. The stock continued to fall another 12% to lows of $30.60. Is this an overreaction? Yes. I don't think the flights to Israel will affect the bottom line as much as the initial fears indicate. I'm going to loop in oil prices with inflation and interest rates. The reason is that the two are related. Looking at WTI pricing below, we can see that it was relatively stable, nearing year lows in late June and early July. Shockingly, or not.... Delta hit highs in early July!

{kind=link}

As the price of oil increased quickly, Delta's share price went in the other direction. When oil moves quickly, jet fuel prices follow. All in all, we saw WTI pricing jump over 38% in just over two months. Higher input costs across the board squeeze airline margins. Tie that in with high inflation and the highest interest rates we have seen in years, and you get a fragile market that is going to react poorly to news that will affect the bottom line for any company. Concerning the inflation and high interest rates, we could continue to see the economy tighten which will impact travel, specifically business travel.

Last but not least has to do with the dynamic in the industry between low-cost airlines and your big fish which I think will benefit Delta in the long run. With the costs being what they are between labor and fuel, it's becoming harder and harder for the low-cost carriers to operate efficiently. In fact, United Airlines CEO Scott Kirby didn't hold back during their 3rd quarter earnings call in saying that the low-cost carrier model was broken and unsustainable. Kirby said that Delta and United are going to account for about 98% of the revenue growth and 90% of the total expected industry pre-tax profit.

Why I'm Buying Delta

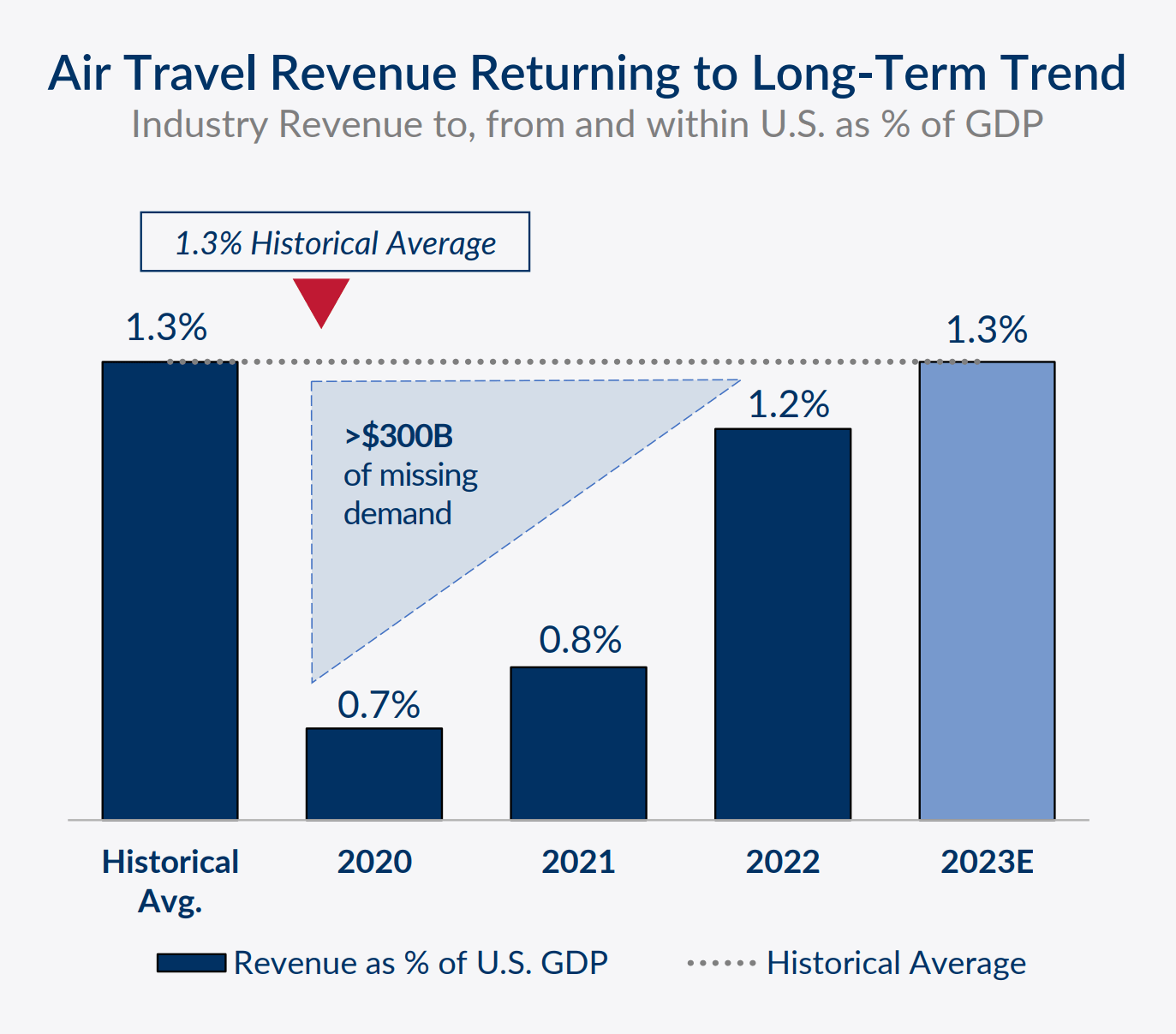

So we have established that the industry is hurting. The industry and the market will figure this all out. That I have zero doubts about. People need to travel and were on pace to get back to pre-covid numbers this year. In 2019, according to the TSA checkpoint data , we saw 840 million passengers. In 2022, we saw 759 million. As of 11/5 in 2023, we were at 723 million. Assuming we just do the same volume as 2022 (it's expected we see higher numbers) we will finish at over 840 million passengers travel in 2023. Much like Covid-19, the current conditions are temporary. In the modern world, travel is a necessity for many. If airlines are forced to close their doors, Delta will be one of the airlines that pick up the slack.

{kind=link}

Just under a month ago, we saw Delta beat Q3 expectations on both EPS ($2.03 beats by $0.08) and Revenue ($15.49 billion beats by $354.00 million). Ed Bastian, Delta's CEO had the following to say:

Thanks to the outstanding work of our entire team, Delta delivered record September quarter revenue and a double-digit operating margin. Our operational reliability continues to strengthen, thanks to our people, and I'm pleased to recognize their outstanding efforts with over $1 billion accrued year-to-date towards profit sharing...

Some of the nonfinancial Q3 highlights :

- Took delivery of 28 aircraft year-to-date and 10 this quarter

- Operated the most on-time airline in the quarter, leading our competitive set in July through September

- Ranked No. 12 in TIME Magazine's World's Best Companies of 2023 based on revenue growth, employee satisfaction, and sustainability profile

While this is great, I am more concerned with what happens in Q4. A strong Q4 will be a great catalyst to turn this slump around. Even with the great results in Q3 from both Delta and United, both companies are still falling with the rest of the industry. That just goes to show this is more of a throw-the-baby-out-with-the-bathwater kind of rinsing in the market right now.

{kind=link}

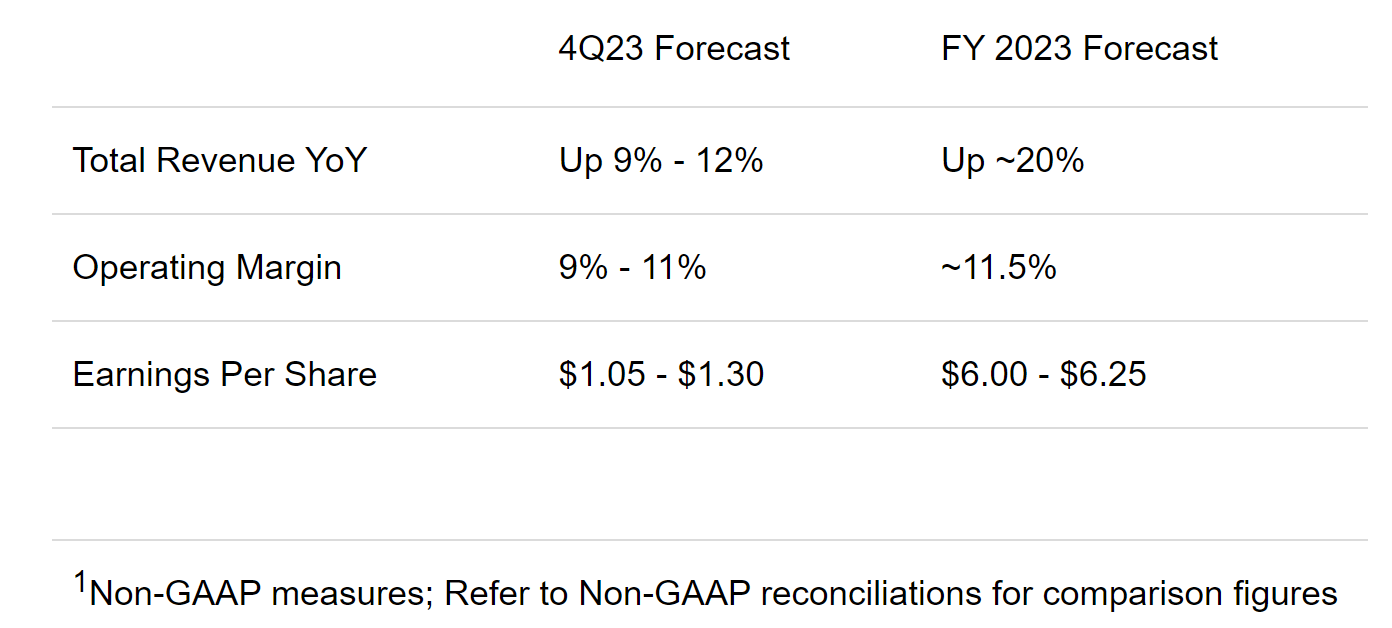

What we have seen here is an increase in what's expected with respect to the FY23 forecast. Is that something you would expect from a stock down over 36% in the last few months? I sure wouldn't. It will be interesting to see how the current situation in the Middle East affects their international travel, but I do not expect that this will cause them to miss the mark. I guess this is more of a "time will tell" situation than anything.

What Does The Price Say?

It goes without saying that the stock is currently undervalued. Delta is being punished for being an airline stock. We recently saw the chairman of the board pick up 20,000 shares. He wouldn't be doing that if he expected Q4 to tank. This is just another reason I am dipping my toes into the Delta pool. Let's look at what we could see in price action.

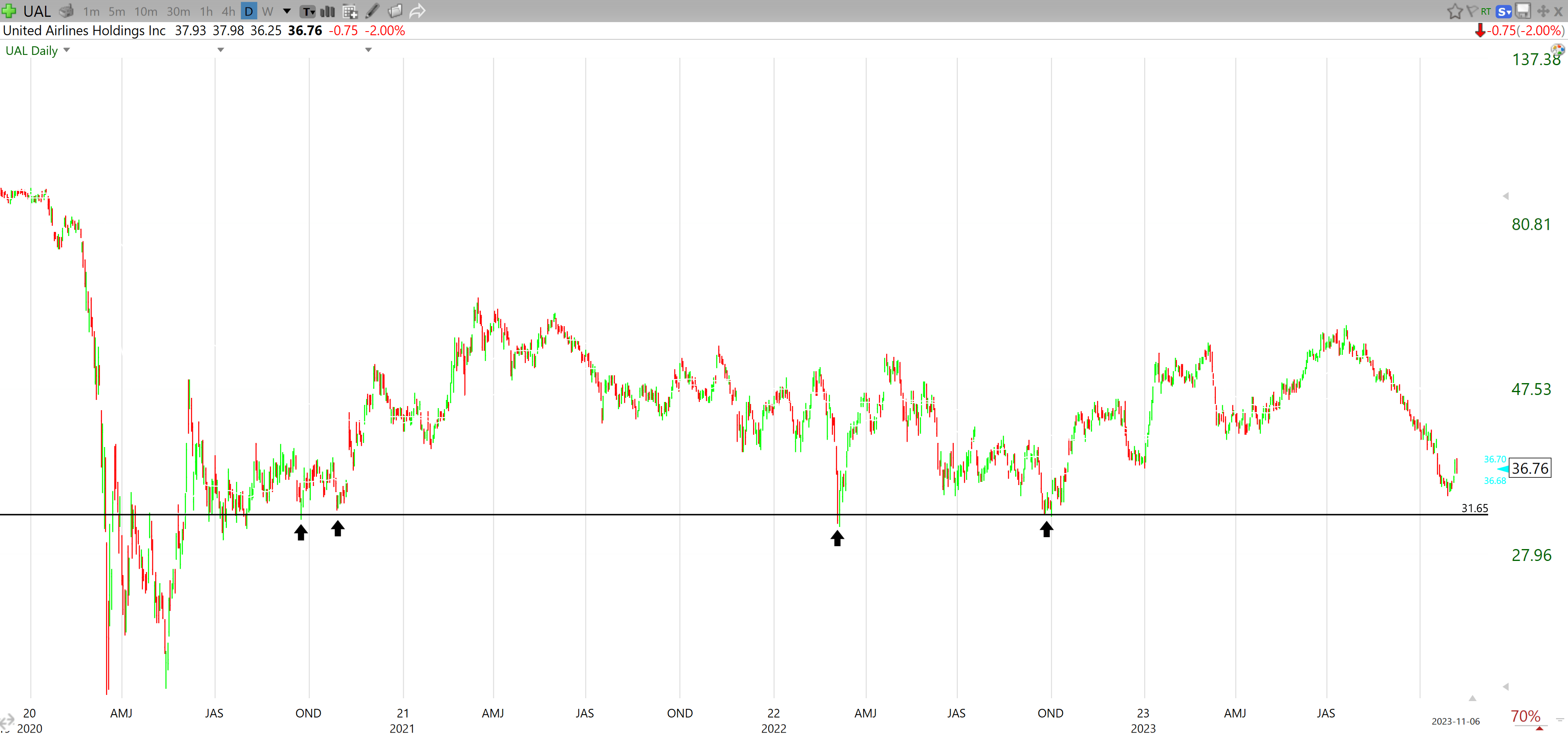

First and foremost, you must have a stop in place when buying a stock that is getting beat up for what appears to be the wrong reason. It's very easy to get blinded and keep praying for that bounce. Know when you're wrong, and protect capital. My stop on Delta is currently $31.65. Looking below, you can see that there is plenty of price support here. Keep in mind if you get stopped out, you can always get back in. Getting stopped out just allows you to reconsider your investment thesis. It is not goodbye forever. I have often been stopped out and re-entered a day or two later. Do I end up paying more to get back in? Yes. But stops have saved me far more than they have cost me.

{kind=link}

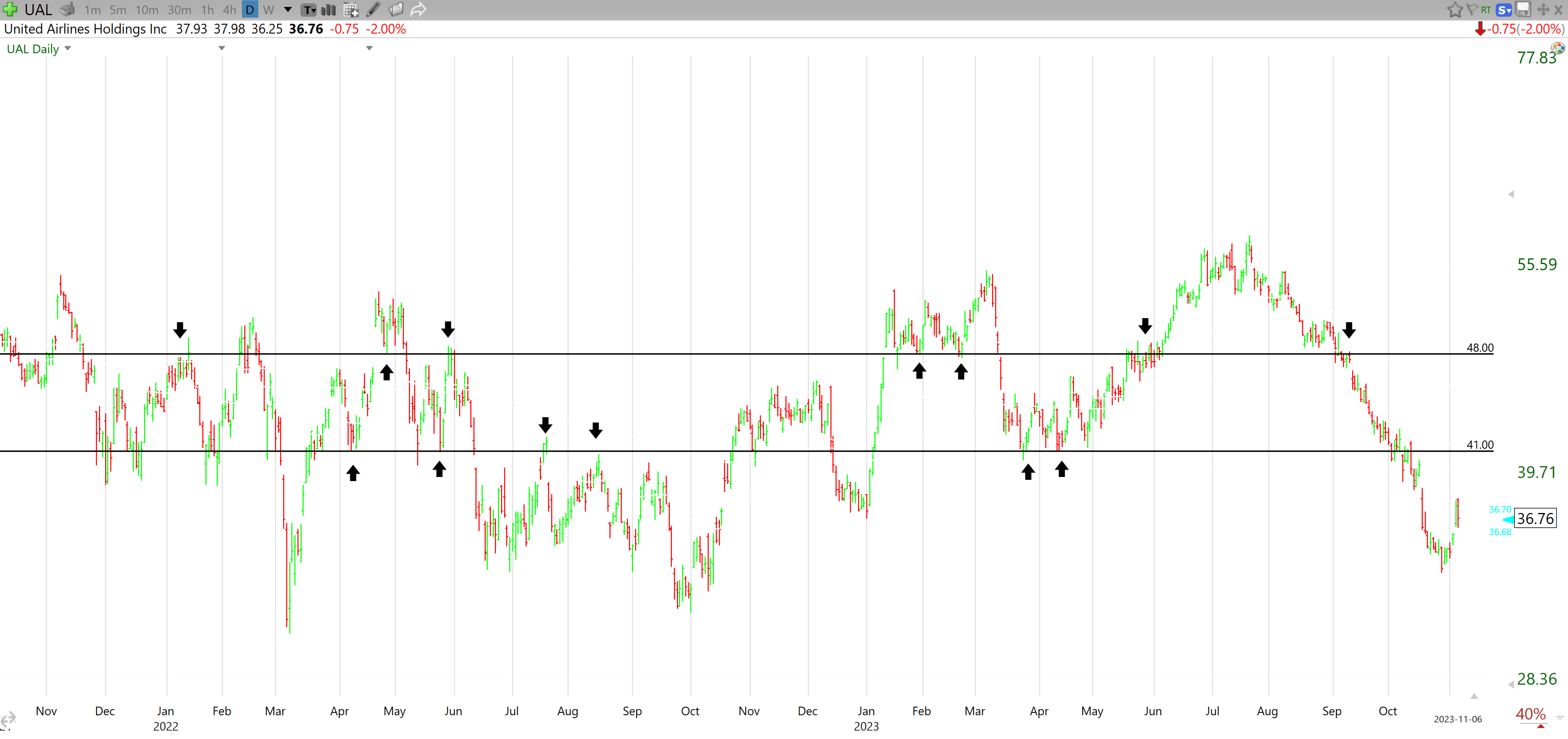

As for where we could be headed concerning the positive, I am looking at two levels. $41.00 and $48.00. Looking below, you can see both have been points of support and resistance over the last few years. I do not anticipate a V-shaped recovery here, and I think it will be choppy as any news of other airlines struggling could negatively impact Delta, which is the whole reason they are in this situation, to begin with.

{kind=link}

That said, I do think we see the reversal and the stock will make its way back up to $41.00 and beyond. Of course, the airline industry is very volatile and any sort of news could entirely derail my thesis. Based on the current market evaluation, I believe Delta is being unfairly punished and view this as a great buying opportunity.

Wrap-Up

As you can see, this is an airline's problem. Not a Delta problem. Delta continues to outperform and is going to get through this one way or another. The million dollar question is what is the share price in a year? As mentioned, I am taking this step by step. I look forward to seeing the stock get back to $41.00 and get through some resistance. I will re-evaluate if that happens. This is definitely not a risk-free investment, and if you do choose to take the plunge, keep an eye on the news and watch for Q4 results in a couple of months. Delta seems to be doing everything right, I'm banking on the market realizing that as the environment in which airlines operate changes due to increasing costs. I'm buying the dip.

For further details see:

Delta Air Lines: Likely To Get Through Macro Turbulence