DAL - Delta Air Lines Stock: A Disastrous Buy With Upside

2023-10-05 08:30:00 ET

Summary

- Delta Air Lines stock has dropped 25% compared to a 5% loss for the broader market due to volatility and downward revisions in the airline industry.

- Airlines are facing pressure from increased labor costs, higher oil prices, and uncertain demand in certain markets.

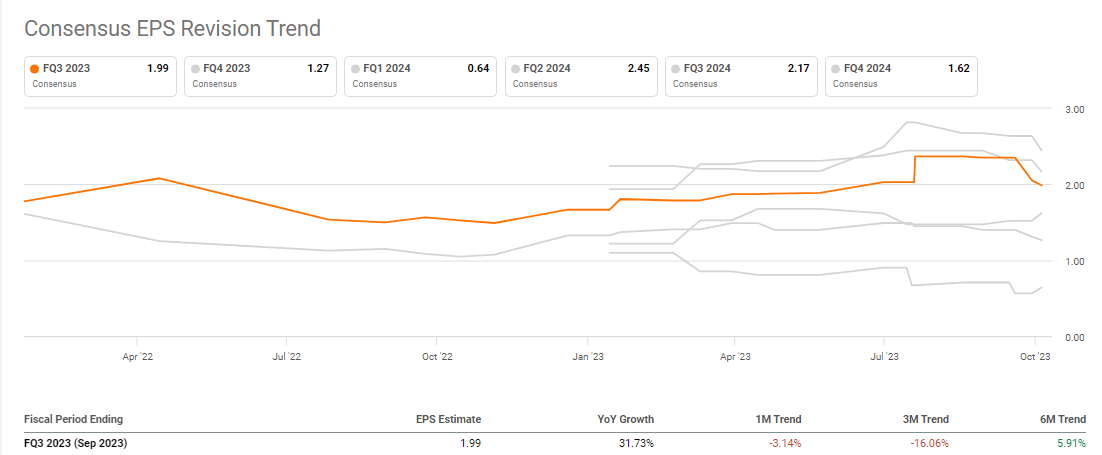

- Analysts expect Delta Air Lines to report Q3 revenues of $15.28 billion and earnings per share of $1.99, down from previous quarters. However, DAL's guidance suggests that demand remains strong.

In July, I marked Delta Air Lines (DAL) stock a strong buy, and that has been a disastrous call to date with the stock being down 25% compared to a 5% loss for the broader markets. I would say that is just the volatility of airline stocks and the impact of downward revisions that we have seen in announcements from airlines recently, as fuel prices headed higher. In this report, I will be looking at the updated guidance, a preview for Q3, and re-assess my rating on the stock.

Airlines Are Facing Pressure

For airlines, the current environment is a tough one to operate despite demand for air travel remaining high. Generally, we see that on the domestic market the recovery is complete which begs the question how much room there is to extract value from the domestic operations. International operations still have a lot of growth ahead, but we have also seen that oil prices have been lifted off their $66 per barrel lows of June to as high as $94 by the end of September with a current barrel price of $84. So, there is significant fuel price volatility, and while Delta has a unique set up with its own refinery, it is not completely shielded from fluctuations in oil prices. What also hurts airlines is that labor costs are increases as new labor agreements were announced. Bringing labor, oil prices, and demand together, the big question has become whether a weaker or normalized demand environment can carry the costs of higher oil prices and labor. And I would be inclined to say that that is not the case.

Airline crews have rightfully demanded higher pay amidst inflation with sky-high demand strengthening their position at the negotiating table, but those are multi-year agreements based on the strong business environment envisioned in the last years, and one can wonder how prudent those labor agreements will be going forward on a softer demand cycle.

When Will Delta Air Lines Report Q3 Financial Results?

Delta Air Lines will kick off the Q3 earnings season on the 12th of October before the opening bell. It will be the kickoff of earnings season for the airline sector and likely set the tone for stock price developments for all airlines, so it is definitely a watch item.

What Are Analysts Expecting From DAL's Q3 2023 Earnings Report?

{kind=link}

Analysts are expecting revenues of $15.28 billion down $300 million from the previous quarter but still pointing at a strong Q3 while earnings per share are expected to be $1.99, which is down significantly from the $2.68 reported in Q2. Looking at the Q3 2023 EPS estimate development, we see that it has been trending down from roughly $2.35. What we also see in the earnings estimate is that it is down to the range where analysts initially expected it before Delta upped its guidance for 2023 in July.

The revenue estimates have actually moved very little, indicating that demand is still robust as Delta alluded.

Delta Guidance Validates Strength

Delta Air Lines

While the guidance on earnings per share has been down, we do see positives. The total revenue guidance update and the TRASM range being narrowed are indications that the demand is strong. The CASM ex Fuel is now expected to be up 1 to 2 percent while the previous guide was for the costs to be down 1 to 3 percent. This flip is mostly driven by higher-than-expected maintenance costs resulting in operating margins of 13% compared to a mid-teens guidance prior. Earnings per share guidance has been brought down by $0.25 at the lower end and $0.45 at the higher end, indicating the mid-point going down from $2.35 to $1.95.

While the guidance is generally perceived as negative, we see the strong demand expectations reflected offset by higher fuel and maintenance costs. That is really all that is to it. It is not a major change in booking trends that we saw other airlines reporting . Delta Air Lines likely is less susceptible to this change in trends because it can lean on growth in the international and long-haul markets and is not solely dependent on the trends on the domestic markets. Another positive is that the company has maintained its full year guidance, which also indicates that the company expects persistent strength in the demand environment.

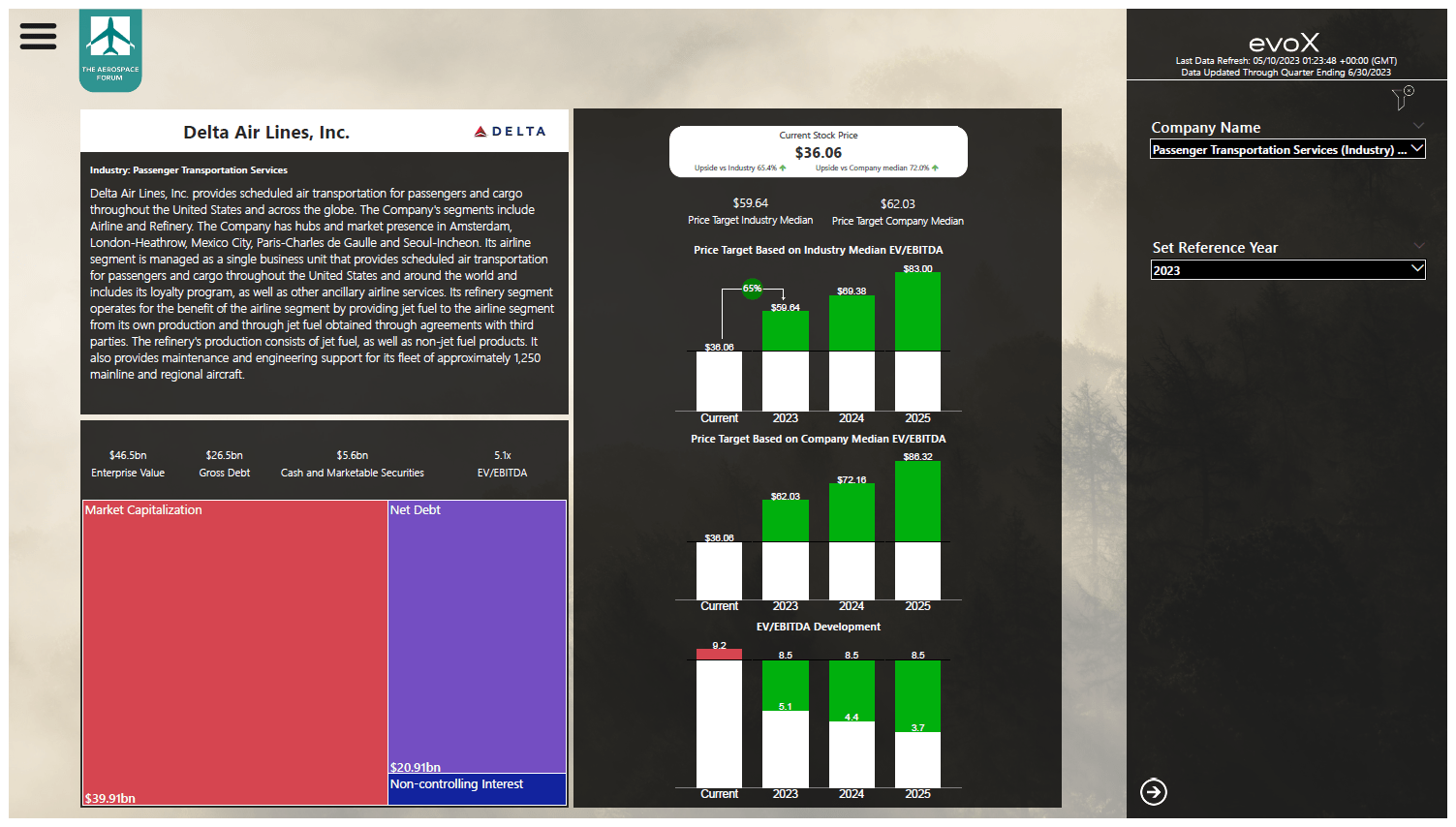

What Is Delta Air Lines Stock Worth?

Delta Air Lines stock price valuation using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

I previously had a $68.75 to $70.50 per share target earlier this year. With the latest guidance update, I have processed the numbers which anticipates EBITDA to be $800 million lower through 2025 than initially anticipated and higher debt repayments as well as dividend increases in the coming years. As a result, the share price estimate has come down to $60 per share which still provides 65% upside. While the price target has come down, Delta Air Lines stock remains a buy. In fact, since the sell-off in Delta Air Lines stock, the upside is even more profound.

Does Delta Air Lines Pay A Dividend?

Delta Air Lines provides a $0.10 quarterly dividend, providing a 1.1% dividend yield. And while I see chances for higher dividend payments in the future, the dividend itself is not what I would consider to be a nice risk offset as airline stocks tend to be extremely volatile.

Conclusion: Lower Target, But DAL Stock Remains A Buy

Delta Air Lines lowered its guidance, but overall that is mainly driven by higher fuel prices and higher than anticipated maintenance costs. Primarily, the higher oil prices are what keep airline stocks in their grip, but the positive is that the guidance suggests that the strong demand environment is persisting. After re-assessing the fundamentals and the updated expectations, I can conclude that the stock remains a buy. Delta Air Lines has also maintained its guidance for the full year, which provides some support to expectations of demand to remain strong throughout the year.

For further details see:

Delta Air Lines Stock: A Disastrous Buy With Upside