DAL - Delta Air Lines: Value Play Or Value Trap?

2023-11-07 11:27:21 ET

Summary

- Delta Air Lines shares have underperformed compared to its peers and the S&P 500 since emerging from bankruptcy in 2007.

- The airline industry is a highly competitive, cyclical, and asset intensive industry which makes it difficult for airlines to generate profits.

- DAL is a best-in-class operator with a stronger balance sheet than most peers but still has a highly levered balance sheet.

- I believe DAL represents a value trap and I am initiating coverage with a sell rating.

Delta Air Lines, Inc. ( DAL ) emerged from bankruptcy in April 2007. Since then, DAL shares delivered a total return 65.5% and have proved a disappointing investment. Over the same time, the S&P 500 delivered a total return of 300% while peers such as Southwest Airlines ( LUV ) and Alaska Air Group ( ALK ) delivered total returns of 80.8% and 319.4% respectively.

By nearly any metric DAL is a cheap stock. DAL trades at just 6.3x trailing earnings, 5x 2024 consensus earnings, and an EV/ EBITDA of 5.9x. However, the stock is cheap for a reason and further analysis is required to determine if DAL is a value play or value trap.

Company Overview

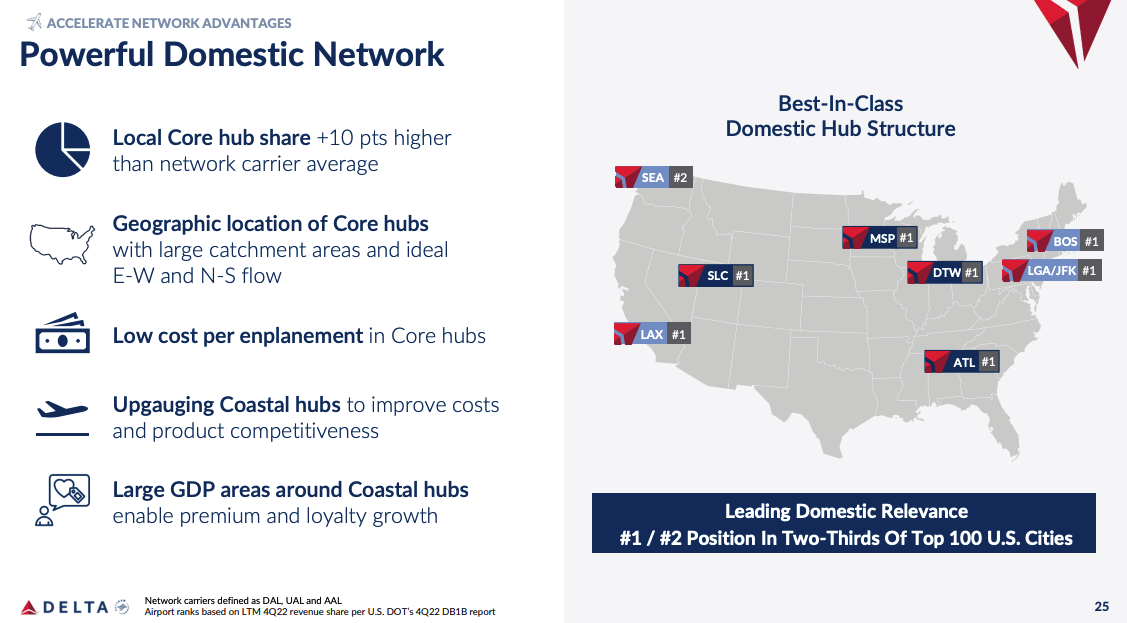

DAL is a leading U.S. based airline but has operations across the globe. DAL is based on Atlanta, GA and serves ~177 million customers annually. The company operates a hub and spoke network with hub locations in Seattle, Los Angeles, Atlanta, Salt Lake City, Minneapolis-St. Paul, Detroit, New York, and Boston.

DAL has partnerships with a number of leading global airlines including Air France KLM, Virgin Atlantic, Aeromexico, LATAM, and Korean Air. DAL owns a 2% equity interest and joint commercial cooperation agreement with China Eastern. In addition to these partnerships, DAL is also a member of the SkyTeam which includes a number of other airlines.

DAL's loyalty and credit card program known as SkyMiles also represents a key part of its business. Currently there are ~ 25 million active SkyMiles members and DAL is expected to receive ~$6.5 billion in remuneration from American Express ( AXP ) for FY 2023.

DAL Investor Presentation DAL Investor Presentation

{kind=link}

{kind=link}

Challenging Business Resulting in a Thin Moat

The airline business is highly competitive. DAL's domestic competitors include American Airlines ( AAL ), United Airlines ( UAL ), Southwest Airlines ( LUV ), Alaska Air ( ALK ), JetBlue ( JBLU ), and Spirit Airlines ( SAVE ). DAL also competes with large foreign based carriers offering service between the U.S. and other countries.

While airlines attempt to offer a differentiated experience by offering superior customer service or better loyalty programs, many consumers make their decision regarding which airline to fly with primarily based on price.

Barriers to entry in the airline business are fairly low and a number of smaller airlines have successfully launched in recent years including Breeze Airways which began operations in May 2021 and Avelo Airways which started flying in April 2021.

Airlines, including DAL, have very little bargaining power with their suppliers as a major input cost of jet-fuel is a commodity. Moreover, airlines have little bargaining power with airplane makers as the industry is dominated by just two players Boeing ( BA ) and Airbus. Another major cost driver for airlines is labor and airlines are also in a difficult place here given high labor unionization rates. ~20% of DAL's employees are represented by unions including ~15,040 pilots.

Demand for air travel tends to be highly cyclical and is driven by economic trends. This is challenging for airlines given their relatively high fixed cost structure (planes and labor) required to operate.

In addition to the challenges noted above, the airline business is also challenging due to significant levels of government regulation and operational complexity

The result of all this is that airlines have struggled to generate solid returns historically for investors.

Best In Class Operator

DAL has distinguished itself as a best in class operator over the past few years. This is important as it helps given the company slightly more pricing power than other carriers.

DAL's high level of service has also helped it to grow its SkyMiles offering into the leader in the loyalty space.

{kind=link}

Stronger Balance Sheet Than Peers But Still Highly Levered

DAL has one of the stronger balance sheets in the airline business but remains highly levered.

DAL borrowed a significant amount of debt in 2020 as a means to ride out the pandemic. While DAL has been focused on improving its balance sheet, the company remains highly levered.

This is problematic from an investing standpoint given the highly cyclical nature of the airline business. Any prolonged downturn could create a situation where DAL faces extreme financial challenges.

As of September 30, 2023 DAL reported a total of $7.8 billion in liquidity inclusive of cash, short-term investments, and undrawn credit facility availability which should provide cushion to ride out a moderate economic downturn.

{kind=link}

High Earnings Volatility

As shown by the chart below DAL has exhibited very high earnings and free cash flow volatility historically. This is due to the highly cyclical nature of the business and high degree of fixed costs.

Since exiting bankruptcy in 2007, DAL has generated an average profit margin of -1.3%

Small Dividend & No Buybacks

In June 2023, Delta resumed its dividend at $0.10 per share quarterly dividend that had been suspended in 2020 due to the COVID-19 pandemic. While I generally do not mind company's paying out dividends, I would prefer that DAL use any additional cash to reduce debt.

DAL has not repurchased any stock since suspending its share repurchase program in 2020.

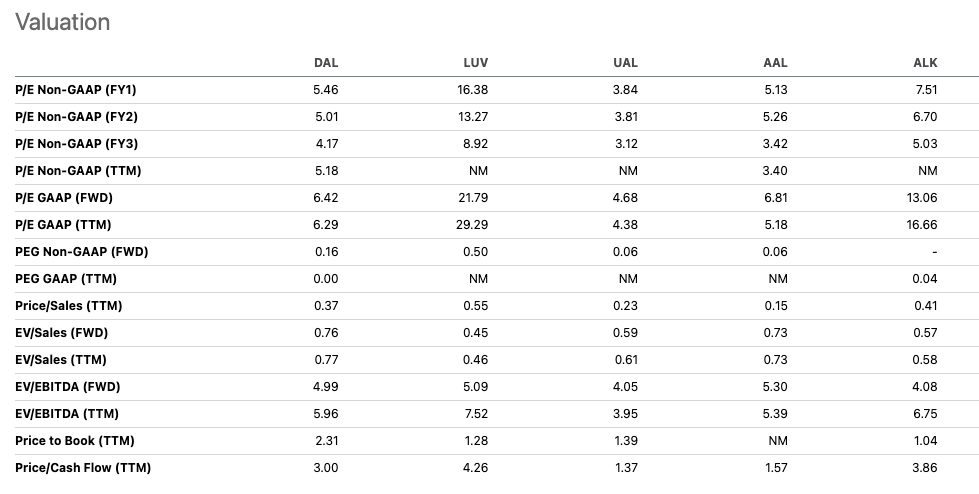

Valuation

DAL trades at 6.3x trailing earnings and 5x consensus 2024 earnings. Comparably, the S&P 500 is trading at ~17.4x 2024 consensus earnings. Thus, on a relative basis, DAL appears to be cheap.

However, the earnings outlook for DAL over the next few years is highly uncertain given the highly volatile nature the company earnings. Historically, DAL has not been able to drive consistent profitability and I believe that may be the case going forward.

In regard to trading levels vs comps, DAL is trading roughly in line with its peers. DAL, LUV, and AAL all trade at ~5x forward EV / EBITDA multiples. On a forward P/E basis DAL is trading in line with AAL, at a discount to LUV and ALK, and at a premium to UAL. While DAL is a strong operator I don't believe it should be trading at a material valuation premium to its peers.

While DAL is trading towards the cheaper end of its recent historical valuation range, I do not find this a compelling reason to believe the stock is undervalued given its historical performance.

Seeking Alpha

{kind=link}

Conclusion

In my view, DAL is a value trap.

While DAL is a cheap stock, I believe it is cheap for a reason. The airline business is characterized by high levels of competition, limited differentiation between carriers, and low bargaining power relative to suppliers.

Since exiting bankruptcy in 2007, DAL has been unable to generate reliable levels of net income for long periods of time. The result has been significantly below market shareholder returns.

While the company is experiencing strong profitability right now, I am not optimistic that will continue overtime given the industry challenges.

In response to the COVID-19 pandemic, DAL was forced to take on a significant amount of debt. The result is that despite some recent deleveraging, the company remains highly levered. This is particularly concerning for investors given the volatile earnings history of the company and industry more broadly.

Despite being one of the better managed airlines in terms of operational performance and current leverage levels better than most of its large peers, I do not believe DAL represents an attractive investment opportunity.

The primary risk to my negative view is a strong economic upswing which last for a long-time (5+ years.) If the economy were to stay strong for a number of years, then it seems possible that DAL and other airlines might be able to generate enough cash to pay down debt and achieve a more sustainable capital structure. However, given the high level of interest rates I am not optimistic that we are at the beginning of a long-lasting economic upswing.

I am initiating DAL with a Sell rating and would consider upgrading the stock if financial performance proves resilient in the face of economic headwinds going forward. I would also consider upgrading the stock if DAL is able to accelerate the space of deleveraging to achieve a stronger balance sheet.

For further details see:

Delta Air Lines: Value Play Or Value Trap?