DAL - Delta: Watch For Potential Pension Problems

2023-12-13 14:28:36 ET

Summary

- Delta Air Lines has a high exposure to private fund investments, posing significant risks to its pension fund in a challenging market for private equity.

- The airline industry is facing potential headwinds in travel, with signs of softening domestic demand and a need to cut capacity.

- Private equity has experienced a slowdown, with declining deal-making and negative returns, which could impact Delta's pension fund and overall operations.

Investment Thesis

While I believe Delta Air Lines ( DAL ) has historically demonstrated robust operational performance and done a good job of capturing strong demand in the travel-leisure sector, I believe significant concerns could arise from its pension fund allocation and the broader market dynamics affecting private equity.

Specifically, and central to my bearish stance, is Delta Air Lines' high exposure to private fund investments. This allocation, notable for its size and the largest allocation among large public companies in the US, I believe poses unique, substantial risks in the context of the challenging market conditions for private assets in 2023. The performance of these investments, particularly in a year marked by inflation and rising interest rates, and less liquidity, could create a problem for the airline's pension in my view, as the vehicle has to continue to pay out to pension holders. I believe the slowing liquidation process typical of private equity funds could further compounded this by creating the risk of a liquidity crunch necessitating additional cash allocations to cover pension deficits, impacting Delta's financial strength??????.

In my opinion, Delta Air Lines is a 'hold' until management is able to clarify. While the company's operational capabilities and market position are strong, the significant uncertainties associated with its pension fund investments, amidst a challenging macroeconomic environment, warrant a cautious approach.

Background

Delta is Off to a Good 2023 but Headwinds Emerge in Travel

In the world of airlines post COVID, Delta Air Lines has been able to show strong resilience in its recovery from the pandemic, continuing through 2023. The airlines had reaffirmed its forecast for the year in late 2022, expecting profits in the range of $6 to $6.25 per share and total revenue to be up about 20%. Since then, estimates are showing the company to come right in line at $6.13/share in 2023 EPS. The company also expects an operating margin forecast of about 11.5% for 2023. This positive outlook is tempered by the fact that Delta's profit goal for 2023 is about 20% below what the company earned in 2019, which indicates a cautious approach amid a larger economy. However, the airline industry faces challenges, including potential headwinds in travel.

Specifically, analysts have noted early signs of softening domestic demand and have been urging airlines, like Delta Air Lines, to cut capacity to protect their pricing power. One analyst from Jefferies (Sheila Kahyaoglu) noted: "Demand is flashing warning signs." Likely partially in response to this, the company has done some limited layoffs on their corporate side to manage costs.

Private Equity is Off to a Bad Year

On the other hand, the private equity sector entered 2023 with some turbulence, faced with a significant slowdown after an unprecedented surge in the post-Covid period. This shift is primarily due to rising interest rates, which have led to a sharp decline in deal-making, exits, and fund-raising activities. This change in the macroeconomic environment ended a long up-cycle in private equity that started in 2010 after the global financial crisis, much of this due to low interest rates??.

As a result, private equity fundraising dropped by 15% from its all-time high in 2021. Private equity returns also suffered, recording negative returns for the first time since 2008, ending a five-year run as the top-performing asset class??.

The impact of these market conditions has been broad, affecting fundraising efforts, deal-making, and overall performance in the private equity sector. For instance, the time required to close new private equity funds has increased, and the volume of exit activity has declined significantly from the previous year. This trend is expected to continue, potentially impacting the ability of firms to recycle sale proceeds into fundraising efforts?? and for limited partners to exit their investments in private funds.

How This Affects Delta

In my opinion, Delta Air Lines' significant exposure to private equity (and alternatives as a whole) in its pension fund presents a potential headwind to the pension fund and something that could spill over into Delta’s normal operations.

In a recent Wall Street Journal article , the paper noted:

Delta Air Lines had 79% of its pension assets in investments that weren’t traditional stocks or bonds in fiscal 2022, the highest percentage of any large U.S. corporate pension according to Milliman. The company’s $12 billion portfolio of hedge funds, private equity and other nontraditional investments hadn’t changed much in size from the previous year. But a 2022 market selloff resulted in the alternative category gaining share for many large pensions. -WSJ 9/29

According to Delta Air Lines, their approach to pension fund management aims for a long-term return that meets or exceeds its annualized target while balancing risk and liquidity. The company's pension plan includes a globally diversified mix of public and private equity, fixed income, real assets, hedge funds, and other instruments, with an expected long-term return on assets of 7.00% as of the end of 2022 ( 10K )??.

The strategy carries certain risks. Recent research has shown that Pension funds have had a real negative alpha in their returns of about -1.2% per year since 2008 . While private equity funds have been a net neutral to this figure (I read this as they also had about a -1.2% alpha drag for these funds), Hedge Funds and Real Estate funds hurt this average.

With many of these private funds being known for their slow liquidation process, this could pose potential challenges for Delta in case of urgent liquidity needs?? in my view.

How Will This Impact Valuation?

While Delta Air Lines scores well with most Quant Ratings provided through Seeking Alpha’s proprietary system, scoring an ‘A’ or higher on most metrics, I think the price to book ratio for the company is a key metric here and part of the reason I’m a hold on the stock.

The company currently has a forward price to book of 2.36. While this is better than the sector median of 2.55, I think this doesn't incorporate the potential downturn Delta could have in their pension fund.

For example, as noted in the 2022 10K, the pension’s liabilities can increase by over $743 million per 50bps in discount rate decreases. The discount rate was at 5.62% at the end of 2022 and 2.97% at the end of 2021. If the discount rate simply drops to 5%, the pension fund could cause Delta Air Lines to accrue another $743 million+ in pension liabilities.

Delta Pension Sensitivity Assumptions (Delta 10K)

{kind=link}

Keep in mind this assumes that management values their pension assets correctly. When Delta filed their 10K for 2022, they noted:

...[for] the fair value of the Company’s benefit plan assets…$12.3 billion do not have a readily determinable fair value and are measured at net asset value per share ("NAV assets") as a practical expedient. -Delta 2022 10K

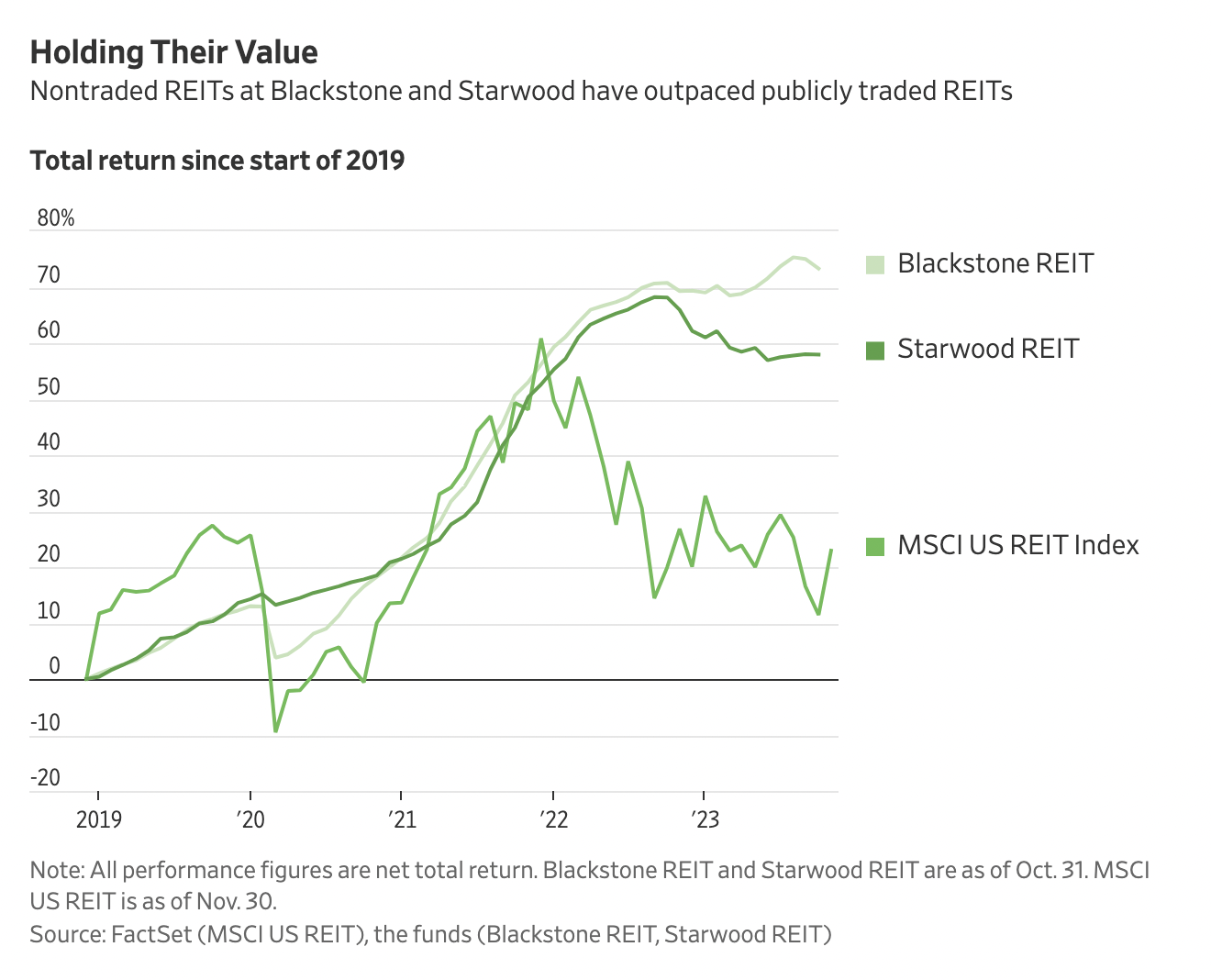

In essence, I believe they are taking the value from the private fund managers. While some of these funds have liquid investments (Hedge Funds) some do not (PE and Real Estate funds). Some of these private funds have come under question for how they generate their NAVs. In one recent example, the Wall Street Journal recently put out a report showing how some private Real Estate funds' NAV are showing a disconnect from similar public market ones. While this doesn't necessarily guarantee that these funds are mis-priced, it makes me question the fair value. Delta Air Lines is choosing to mark them at their NAV value.

Private vs. Public REITS (Wall Street Journal)

{kind=link}

While these liabilities, based on how pensions are calculated, tend to roll into the comprehensive income section of the balance sheet, examining this part of the balance sheet shows that Delta has billions of dollars in unrealized losses. Keep in mind this $743 million adjustment does not assume any change in the long term rate of return on these assets. If assets are overvalued based on their NAV, we definitely could see an adjustment in the long run rate of return.

Delta Tangible Book Value (Seeking Alpha)

Furthermore, the airline's tangible book value is negative (and has been since COVID started). In essence, the fair value of their company is based on the present value of the cash flows vs. the value of the assets. While most companies are valued on their cash flows (vs. book value), I think this pension liability question could make investors focus on the book value. Airlines are an asset heavy business.

So while their price to book value (non-tangible) is better than industry averages, this does not account for the losses that the pension fund could incur. With this I think the stock may be overvalued on a price to book ratio after accounting for the negative tangible book value and the potential shadow price to book figure which is likely now higher than the sector median.

What's the Bull Case I'm Missing?

The main bullish case (like I mentioned before) for Delta is supported by the current robust demand in the air travel sector. The International Air Transport Association (IATA) reported strong demand growth in air travel for March 2023. This growth indicates that air travel is now at 88% of March 2019 levels.

Separately, Bain & Company's outlook for air travel demand remains on track to surpass 2019 levels by the middle of next year . This trend could underpin strong cash flows for airlines, including Delta??.

However, I think it's important to note that there are emerging signs that this strong demand might start to weaken next year. According to Reuters, the current level of demand, boosted by pent-up travel needs, could start diminishing . Factors such as economic developments, rising costs, and geopolitical tensions (especially in the middle east) could potentially affect consumer spending and travel patterns.

Conclusion

While Delta Air Lines has exhibited strong operational performance, I’m concerned about the potential financial pressures the pension fund could have, making Delta a "hold.” Specifically, the airline’s pension fund allocation, with so much in non-traditional investments like private equity, exposes the firm to considerable risk in my view, especially given the challenging market conditions for private equity in 2023.

This overexposure is heightened by the potential liquidity issues due to the slow liquidation process of these funds (especially evident in 2023). Such a scenario could lead to underperformance in meeting pension obligations and necessitate additional resource allocation, potentially impacting Delta's financial health??????.

Delta is a strong airline brand and personally one I enjoy flying. I think, however, their balance sheet and pension liabilities require further clarification from management before investors take flight with this stock. In my opinion, the stock is a hold.

For further details see:

Delta: Watch For Potential Pension Problems