DLX - Deluxe Corporation: Appealing Valuation But Looking For EPS Growth

2023-09-20 12:22:44 ET

Summary

- Deluxe Corporation's share price remains attractive with a low P/E ratio and over 6% dividend yield.

- DLX operates through four segments, offering technology-driven services to various clients.

- Rising interest rates and cash flow challenges pose risks, but improvements in cash flows and interest rate decreases could lead to higher valuations.

Investment Rundown

The share price of Deluxe Corporation ( DLX ) continues to look very appealing in my view, even after the significant run-up it has had just the last couple of months. With a p/e under 6, I think a lot of the potential risks have been enabled already and investors are now left with the option of getting in at what I think is a great price point. Besides this, DLX is also offering an over 6% dividend yield that is supported by strong net incomes. The payout ratio is quite low at around 30%, but I wouldn't expect any raises to it in the short term, as the last time it was raised was back in 2014. With nearly a decade of no dividend growth, the company may not look like a good dividend income opportunity, I have to admit. But when comparing the growth of the business to the valuation, I think it still offers a good risk/reward scenario. I will be rating the company a hold as I await the next few quarterly reports and hope for further improvement in the volumes and EPS for the company.

Company Segments

DLX offers technology-driven solutions to a wide range of clients, including large enterprises, small businesses, and financial institutions across various regions, including the United States, Canada, Australia, South America, and Europe. The company operates through four distinct segments: Payments, Data Solutions, Promotional Solutions, and Checks. Its services encompass treasury management solutions such as remittance and lockbox processing, remote deposit capture, and receivables management, among others.

Q2 Highlights (Investor Presentation)

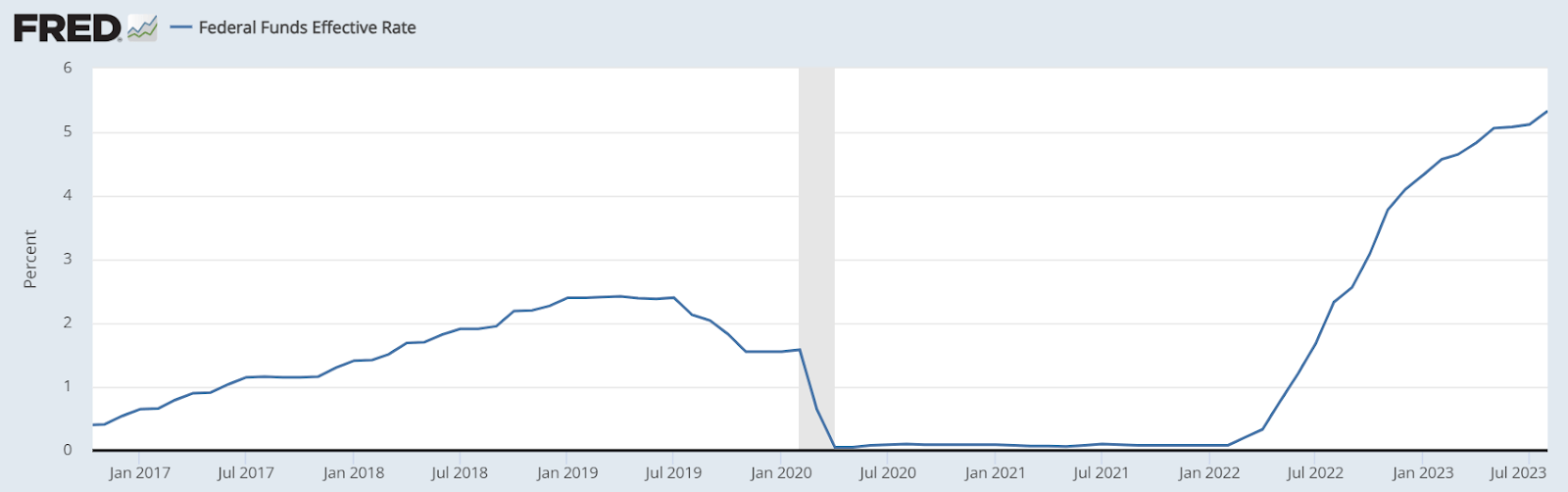

For the last quarter, the company continued to see a good amount of growth as an increase was seen across all the segments of the business. What I think could be a reason for the lower p/s that DLX receives is the soft revenue increases it's seeing right now. Compared to the broader sector, DLX has a p/s that's over 70% lower. But I think with revenues only increasing 1.5% YoY, that seems like a reasonable price point. DLX needs to pick up the space if they want to be considered a growth company. As I said before, they offer a lot of payment services like treasury management solutions and payment exchanges. The increase in interest rates of the last year has been a key contributor to the softer activity seen across the economy, and that has for DLX meant lower revenue growth I think. I tend to hold the view that in the second half of 2024, we will at least start seeing the first few step-downs in the interest rate. That could potentially set off a rally for the market, and DLX could tag along as their activity may drastically increase. Up until then, though, I think that investors are still far better off holding shares.

Earnings Highlights

2023 Guidance (Investor Presentation)

In the last report, the company provided some more updates on its guidance for 2023. The revenues are now estimated to be between $2.18 billion and 2.22 billion, a pretty tight window that I think they can achieve if they see similar growth as the last quarter. The FCF is to be between $80 - $100 million. The dividends paid out the last 12 months have amounted to $52.9 million, so the anticipated full-year FCF can supply this with ease and leave some to better the financial position of the business by increasing the cash position, for example.

Risks

The rising interest rates have posed significant challenges for the company, and the situation is expected to further deteriorate with the expiration of certain derivatives used to hedge against interest rate risks in March 2023. Additionally, the company's cash flows have been impacted by asset disposals, and a technology overhaul is currently affecting cash flow generation and overall profitability. These combined factors paint a challenging picture for DLX at the moment. Looking at a quarter-over-quarter basis, the last report did show improvements of $10.2 million as the result landed at $23.7 million for DLX. What could worry some is that this will be short-lived and DLX will return to posting poor or decreasing FCF once again. What I can see causing this is persisting interest rates which are hurting the economic activity, and therefore lowering the earnings potential of DLX.

{kind=link}

Going into the next few quarters for the company, I think we need to see a clear improvement in the cash flows if we are going to consider the company valued higher. The interest rates are taking a toll on the activity and once they start decreasing I think a reasonable result will be higher volumes for DLX and other payment solutions companies too.

Financials

{kind=link}

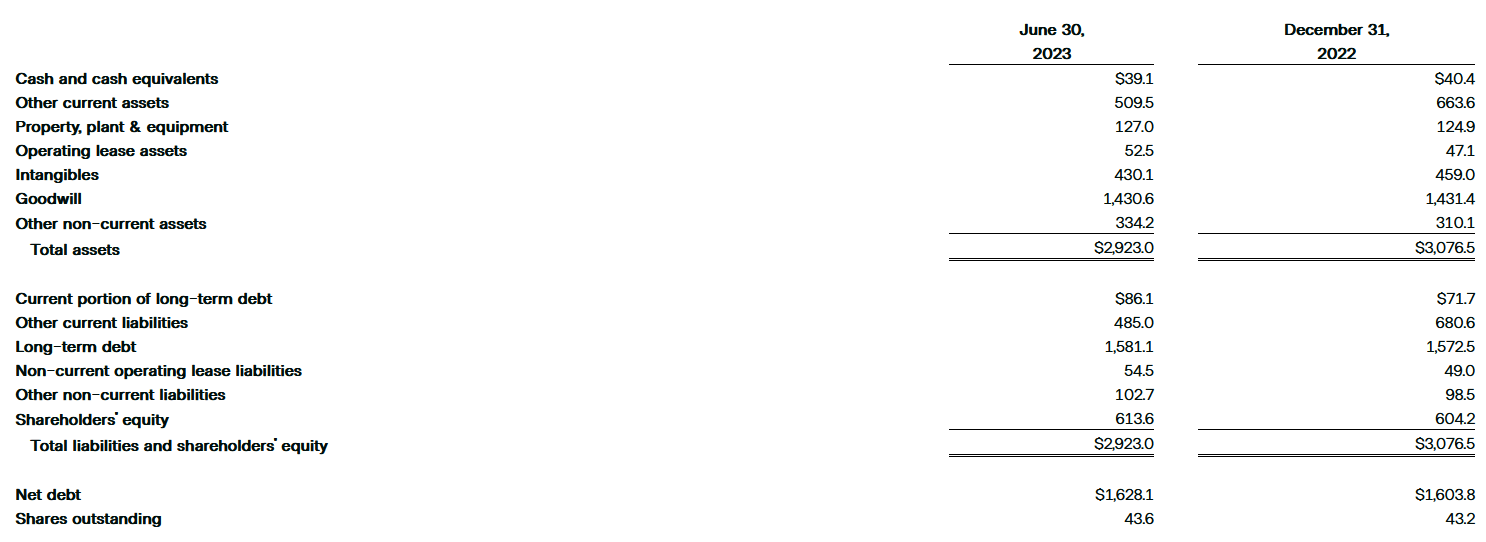

Looking at the balance sheet of the company, not been that much change since December 31, 2022. The cash position has barely moved, and the net debt for the company has increased by $25 million. With a net debt position of over $1.6 billion, the company has a net debt/EBITDA ratio of 4 right now, which I think is quite high. I usually prefer something under 3. I think this could be a factor as well, for the market valuation of the company is lower than the sector and peers. If DLX decides to start improving the debt position, though, perhaps the run-up can be sustained and a higher price achievable.

Final Words

DLX has a volatile last few months as the share price has gone from the lows of $14 per share back in May this year to over $20 recently. The drawdown seems to have come partly from a broader decrease in activity, and the revenue growth for DLX has been far from impressive, I think. With sales growth of just 1.5% YoY, I can see why the market has put DLX at such a low valuation. I do however think that most of the risks are baked in now in the price and the downside is limited. Instead, investors can capitalize from the over 6% yield. This leads me to right now rate DLX a hold.

For further details see:

Deluxe Corporation: Appealing Valuation But Looking For EPS Growth