DLX - Deluxe Corporation: Too Much Debt And Financials Are Not Improving

2023-09-14 08:25:41 ET

Summary

- Deluxe Corporation's financial health is in a downtrend, with high debt and deteriorating financials.

- The profitability and efficiency ratios are mediocre at best.

- The company is seeing deteriorating competitive advantage and moat.

- I won't touch it until financials improve significantly.

Investment Thesis

I was going through my stock screener and Deluxe Corporation (DLX) popped up with its FW PE ratio of around 6, which is much lower than its TTM PE of around 16. So, I decided to look into the company's financial health to see if it would be a good time to invest in the company at this time. The debt is slightly too high for me, and the financials are in a downtrend, therefore I give the company a hold rating until we see improvements.

Briefly on the Company

Deluxe Corporation is a provider of solutions to enterprises, SMEs, and financial institutions in the US and abroad. It provides treasure services, receivables management, fraud and security devices, marketing solutions, and many other services in the 4 reportable segments: Payments, Data Solutions, Promotional Solutions, and Checks.

Financials

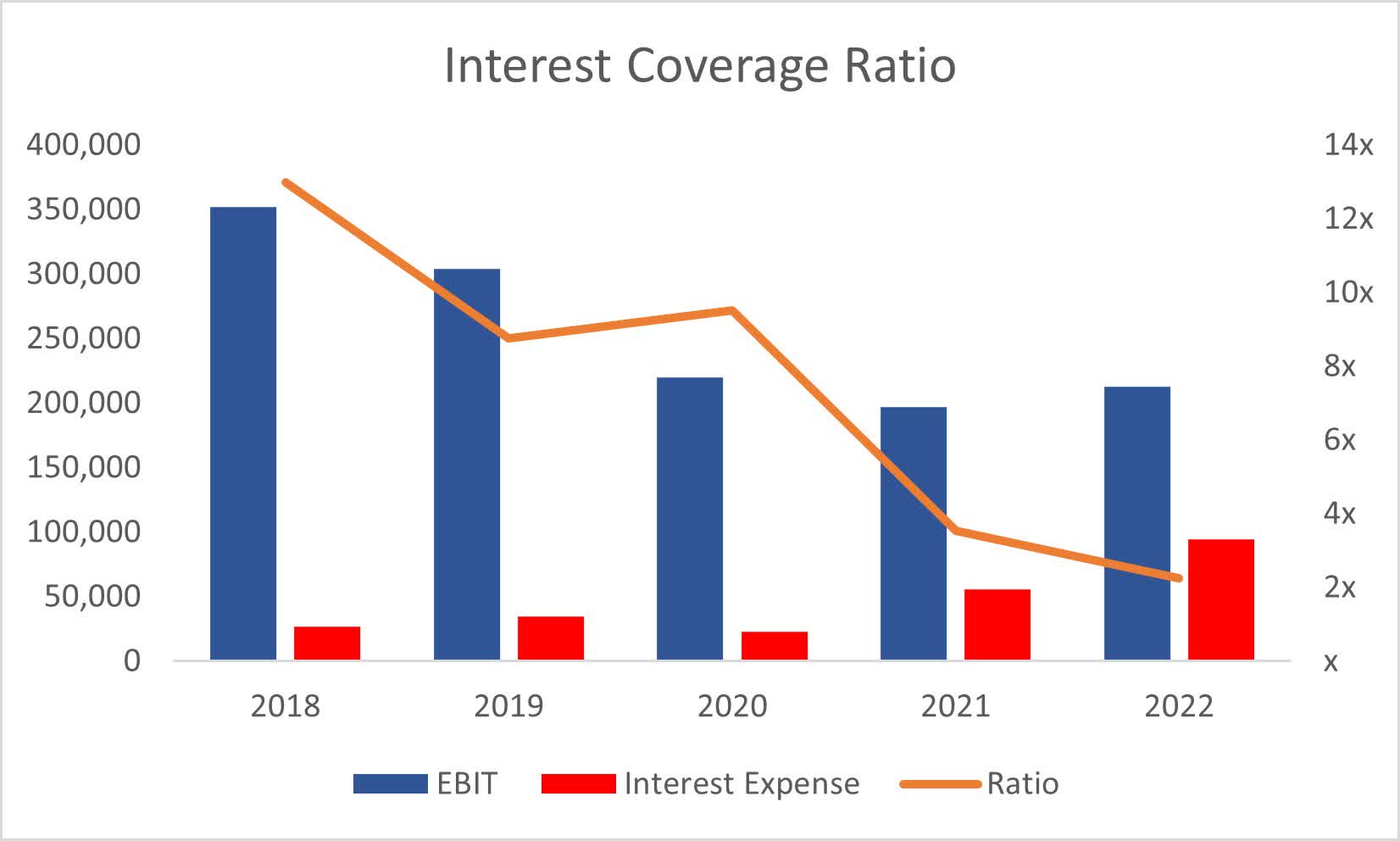

As of Q2 '23 , the company had $39m in cash against $1.58B in long-term debt. This usually wouldn't be too worrisome; however, this seems like a lot for such a small company as DLX with a market cap of $850m. I usually have no problem with companies acquiring debt to fund their operations if the management is using the debt smartly. By that, I mean, the company can easily cover the interest expense on debt. The historical interest coverage ratio was much better than it was in FY22, which stood at around 2x. Now, a lot of people say 2x is a healthy ratio to have, however, I usually look for a company's ability to cover interest expense on debt around 5 times over. This means EBIT is 5 times higher than the interest expense. As of Q2 '23, the ratio is even below that healthy reference of 2x, it stood at around 1.4x, which is a little alarming and will be something to take into account when deciding the company's margin of safety.

{kind=link}

We can see the company's operations have been going down over the last 5 years because of a combination of lower revenues in some years and higher operating expenses in others. That is not the trend I would like to see. I wouldn't be surprised if we see further deterioration in FY23.

The company isn't at risk of insolvency, however, it's a bit worrisome if things don't turn around.

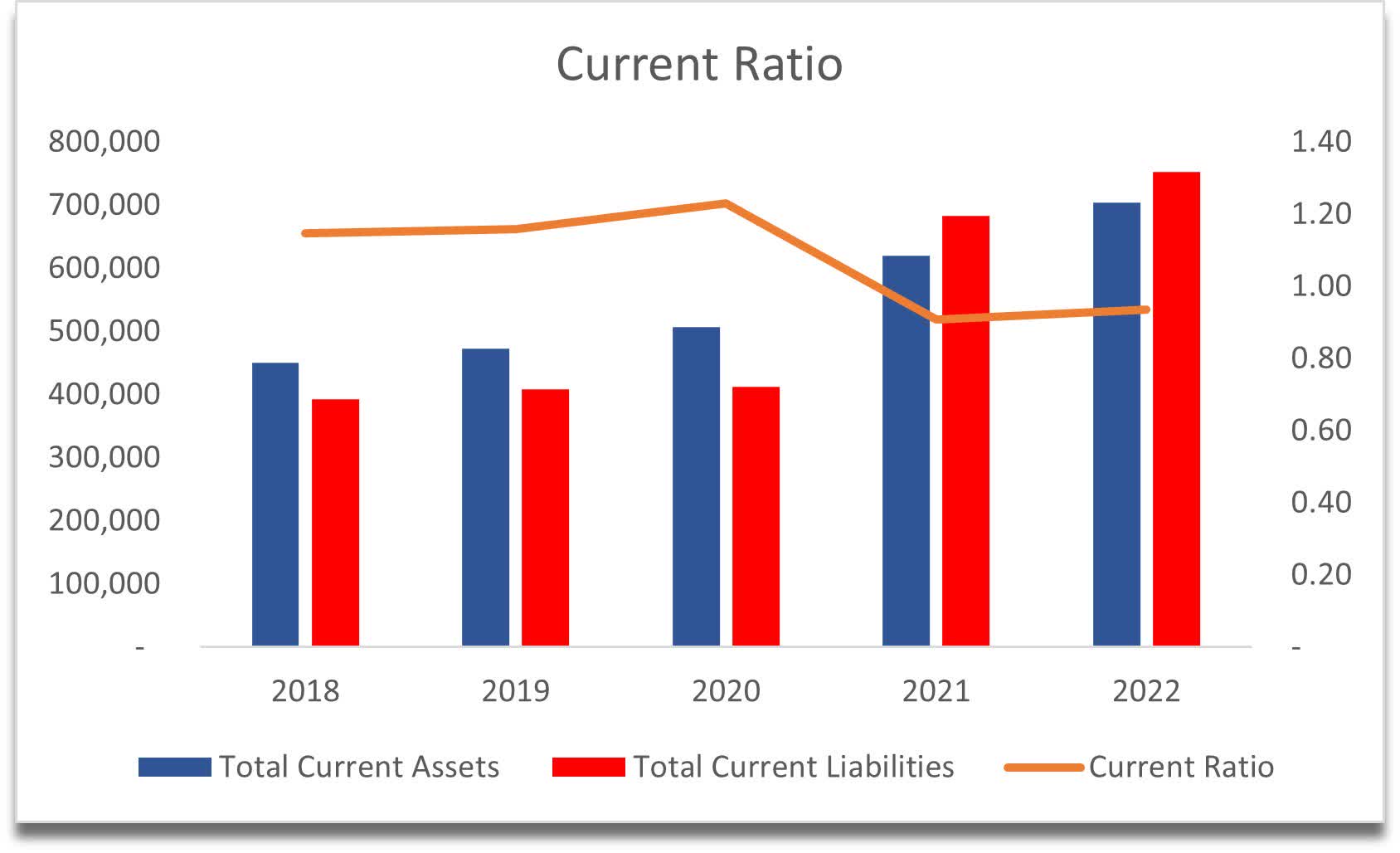

The company's current ratio historically has also been on the lower end of what I usually look for in companies. For the last couple of years, the ratio has been under 1, which signals to me that if push comes to shove, the company wouldn't be able to meet all its short-term obligations. Q2 '23 did not see an improvement in the ratio either, which isn't a good look for the company and shows no improvement in operations.

{kind=link}

There may be a time in the future when the company isn't able to pay off its short-term obligations, and it may have liquidity issues, but only time will tell. I look for companies that can achieve at least a 1.5 current ratio and ideally 2.0 as I believe this to be an efficient current ratio. A good balance between being able to pay off ST obligations and utilizing assets such as cash to further the growth of the company.

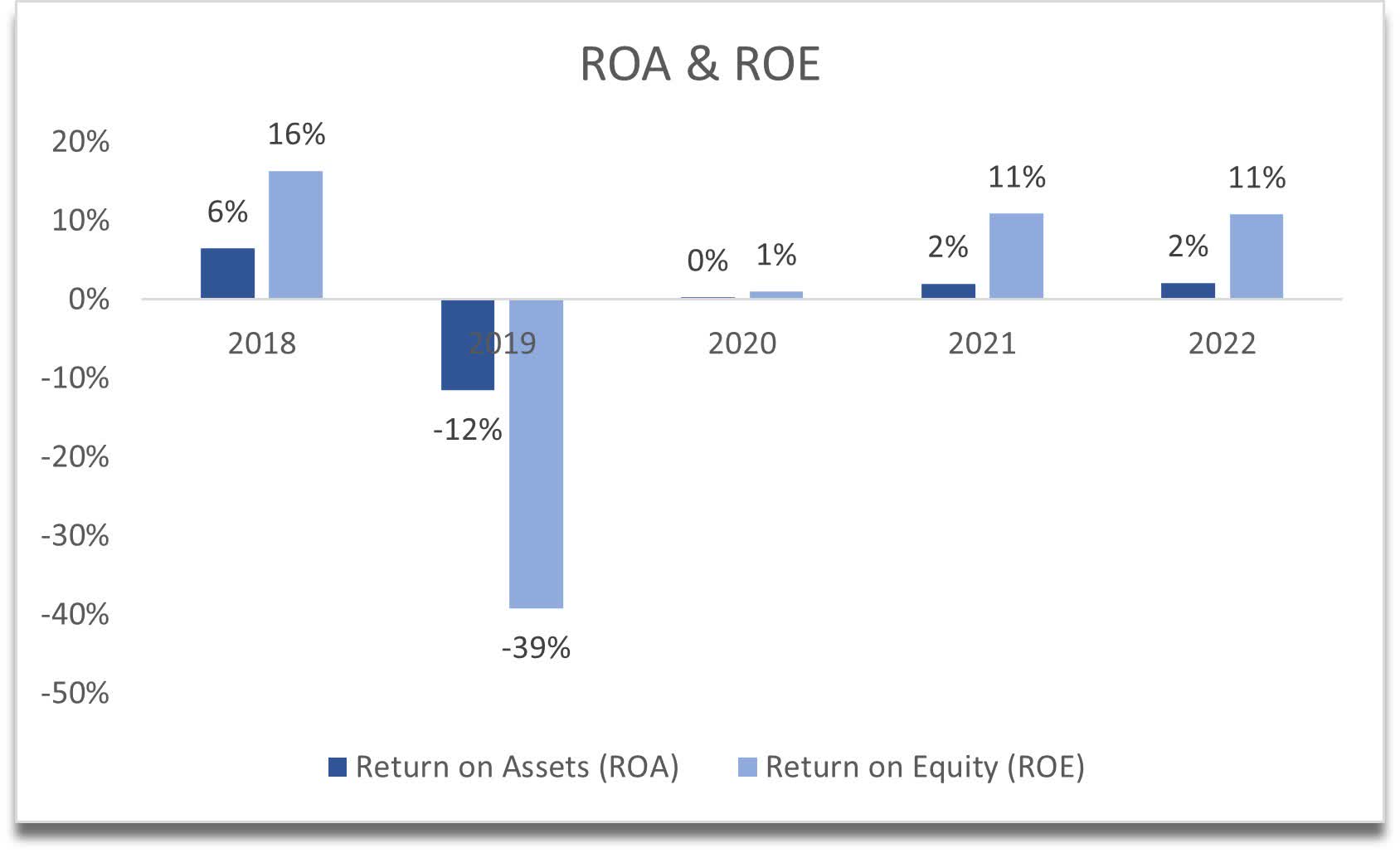

Speaking of efficiency, the company's ROA and ROE are also mediocre at best. A big improvement from FY2019, however, it seems that the management isn't utilizing the company's assets very efficiently, and as for ROE, it's at around the minimum I'd like to see a company achieve, which is also nothing to write home about. My minimums are 5% for ROA and 10% for ROE.

{kind=link}

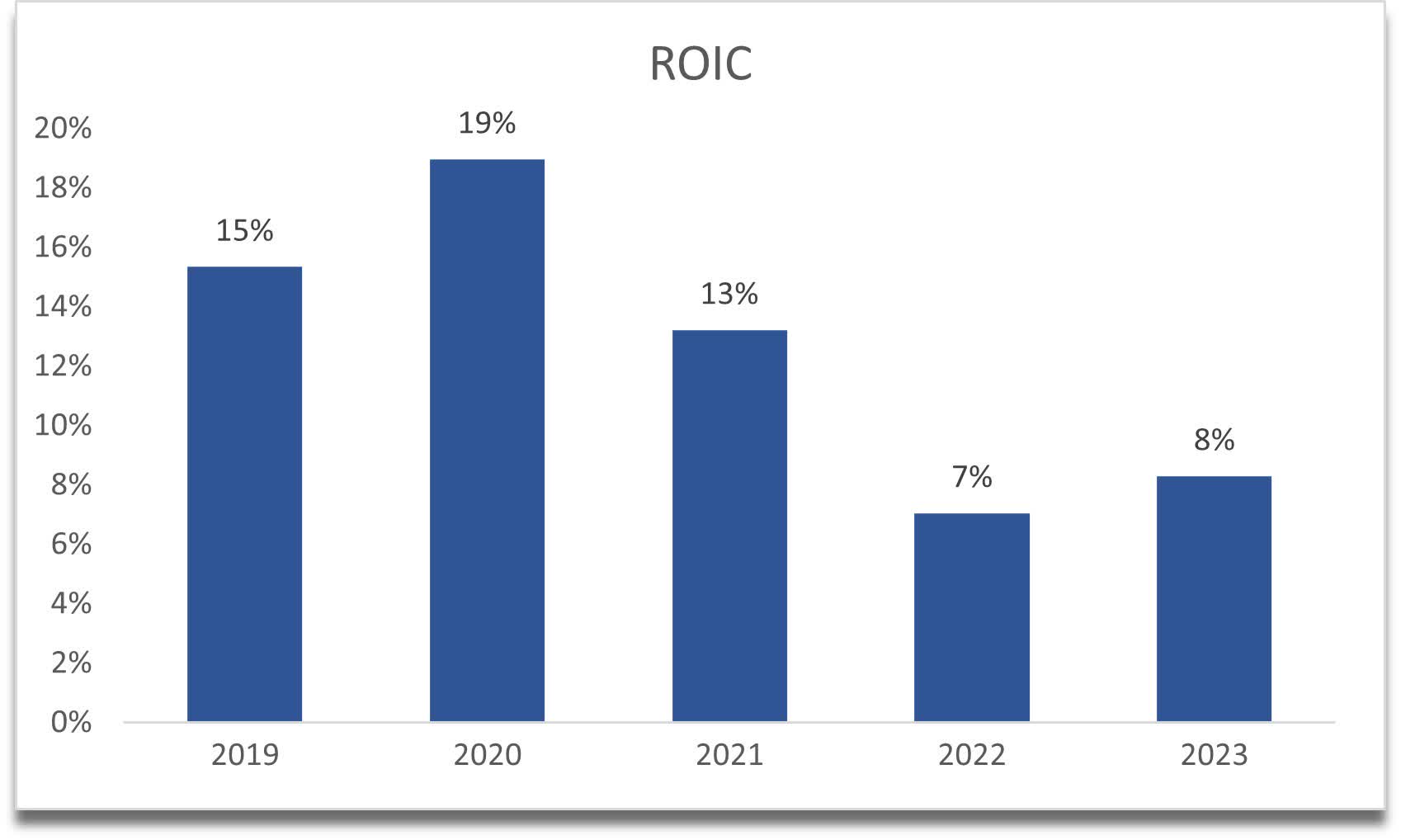

I can see the company has been losing its competitive edge and its moat over the last few years as the return on invested capital has been coming down significantly since FY20 and that is also not the long-term trend I like to see, which is also below my 10% minimum for ROIC.

{kind=link}

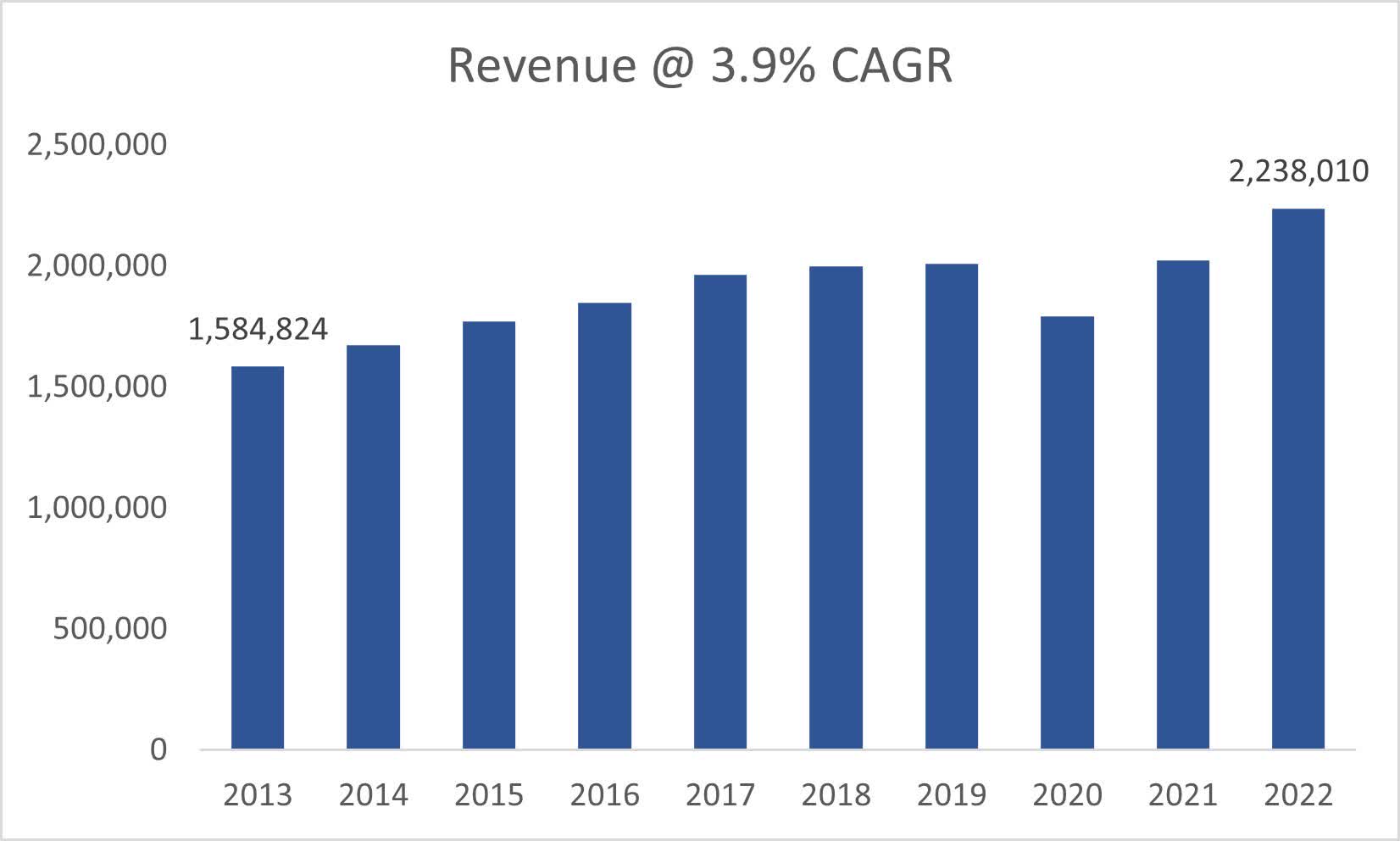

Revenue growth has been rather slow too over the last decade, with a slight pickup in the last 2 years, with around 0% growth guided for FY23 and no growth for FY24 according to analysts . There is also no indication the company will be able to achieve above-average growth in upcoming years.

{kind=link}

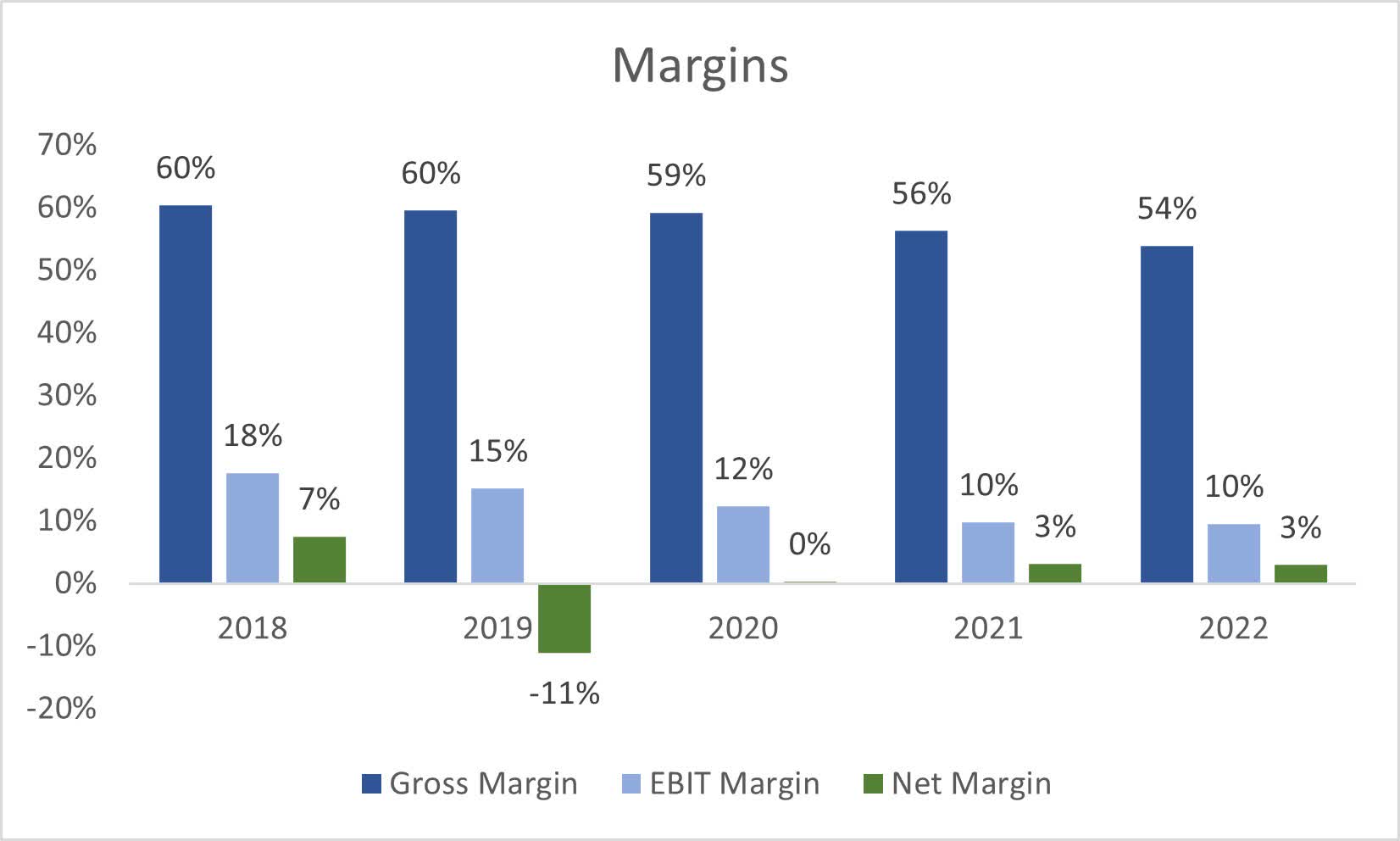

In terms of margins, these have also deteriorated significantly in the last couple of years, which is another red flag in my book.

{kind=link}

Overall, I did not find anything I liked about the company's financials, so I will have to apply a larger margin of safety to match my risk/reward profile. Everything seems to be in a downtrend and that is not what I like to see in a company's long-term picture. Let's see what I would be willing to pay for this company to take on the risks.

Valuation

So, let's take a simple and conservative approach to the company's revenue growth. For my base case, I decided to go with around 3.7% CAGR over the next decade, which matches what it did over the last decade. For the optimistic case, I went with 7.5% CAGR to take into account acquisitions, shifting its business operations towards digitization, and some other unforeseen force that would help it grow at that pace. For the conservative case, I went with around 1.7% CAGR. This way I get a range of potential outcomes that all seem to be reasonable enough to me. Maybe the optimistic one is a little too optimistic, but I'll stick with it.

For the margins, I think I'm being on the generous side here, as I decided to improve gross margins by around 600bps or 6% over the next decade and improve operating margins by around 300bps or 3%. I believe that companies do tend to become more efficient as time goes by due to technological advancements and cost-cutting measures that make the company more profitable in the end.

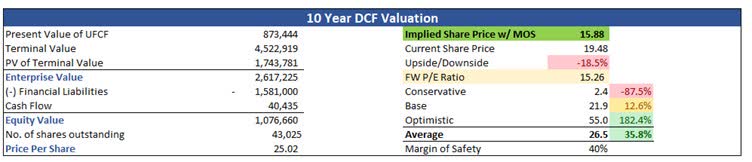

As for the margin of safety, I decided to apply a 40% MoS because the financials were not good at all with no turnaround in sight in my opinion. For me to take on the risk, I need to be compensated appropriately, and I believe a 40% discount is appropriate. With that said, Deluxe Corporation's intrinsic value is around $16 a share, implying the company is trading at a premium to its fair value and a FW PE ratio of 15 which is a far cry from the FW PE ratio of around 6 found on different websites, which leads me to believe these sites are using non-GAAP EPS. I chose to stick with GAAP measures, to be on the conservative side because the company has a lot of red flags for me.

{kind=link}

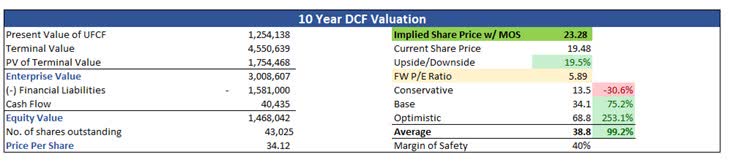

Just to give a full analysis, I went ahead and used adjusted numbers with the same MoS as before and yes, there is quite a difference to the GAAP valuation figures. Do whatever you'd like with this information, however, the financials of the company are too risky in my opinion.

{kind=link}

Closing Comments

I'd like to see a pullback towards my PT, but even if it does come to it, I believe that there is too much risk on the books for me to start a position here. All the metrics I deem necessary to decide whether the company is a good investment or not are trending downward and looking at the most recent quarter, the metrics are not getting better either. The revenue growth is non-existent for the next couple of years, the company insists on using non-GAAP measures, and I just don't like that too much.

One thing on the dividend side also, since it is paying a whopping 6.13% yield. If we look at GAAP measures, the company is basically paying out all its earnings in dividends. It had zero growth in the dividend and with such a high interest on debt, I wouldn't trust the dividend to remain here, and I would rather the management cut the dividend and pay down the debt, and just focus on improving the financials going forward.

For further details see:

Deluxe Corporation: Too Much Debt And Financials Are Not Improving