DLX - Deluxe Corporation: Updated Outlook And Q3 Momentum Results In Rating Upgrade

2023-12-08 14:15:05 ET

Summary

- DLX's restructuring efforts have negatively impacted earnings, but full-year guidance has been raised and revenues are expected to be between $2.1 - $2.2 billion.

- The company provides innovative technology solutions across four segments, including Payments, Data Solutions, Promotional Solutions, and Checks.

- The Q3 earnings report showed a slight decline in total revenues YoY, but the Solutions segment saw strong growth in revenues and adjusted EBITDA. The Checks segment has the highest margins.

Investment Rundown

Back in September this year, I covered Deluxe Corporation ( DLX ) and the stock price has not moved that much since, so a hold rating seemed like the right choice looking back. It did briefly dip down to under $16.2 but has since recovered quite well. Since my last article, there has been a new earnings report released by the company, so I figured a new update on my views was in order here.

The restructuring of the company seems to have been a thorn in the side of earnings, as it was negative by $8 million, as opposed to a positive $14.7 million the year earlier. These moves seem like they are having a positive effect though on the company, as the full-year guidance was raised and revenues are estimated to land between $2.1 - $2.2 billion. With the adjusted EPS in mind, it puts DLX at an FWD multiple of 5.5 on the higher end. With a dividend yield of over 6% and with the company trading at a discount to its historical levels, I think investors are faced with a pretty solid opportunity here right now. One of my issues in the previous article was the lack of growth the company had, but right now I think we are looking at a slight reversal as the outlook improves. I will be raising my previous rating to a buy.

Company Segments

DLX provides innovative technology solutions to a diverse clientele, spanning large enterprises, small businesses, and financial institutions in multiple regions, including the United States, Canada, Australia, South America, and Europe. The company's operations are structured across four distinct segments: Payments, Data Solutions, Promotional Solutions, and Checks. Within these segments, DLX delivers a comprehensive suite of services, including treasury management solutions such as remittance and lockbox processing, remote deposit capture, and receivables management, among other cutting-edge offerings.

{kind=link}

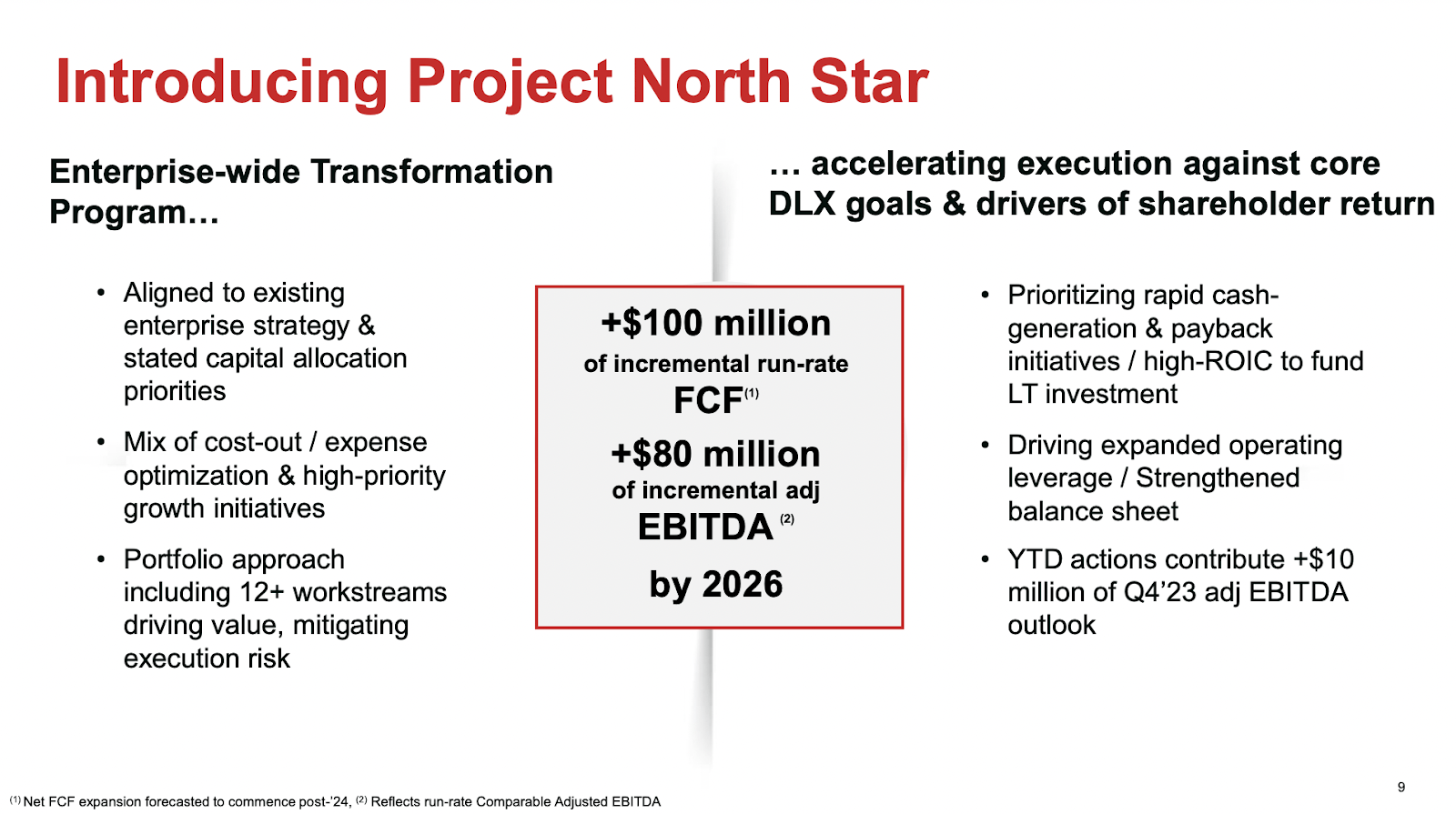

Another key point from the last report was the announcement of Project North Star, which is expected to add $100 million of incremental run rate FCF by 2026. With the 2023 guidance of FCF at $60 - $80 million, that means by 2026 it could double essentially and provide DLX with a great opportunity to pay down debt quickly or finance new business ventures. The project is an enterprise-wide transformation program which is likely to cause some higher restructuring costs in the coming quarters on the reports. What I find the most positive about this move is the project is in line with already existing capital allocation priorities, meaning that shareholders continue to receive the generous dividend the company has right now.

The long-term goal of the business is now to prioritize rapid cash generation and drive a high ROIC which will fund LT investments. That is a fantastic cycle to be in as a company, as it becomes an almost snowball effect eventually. With this, the company will also be strengthening the balance sheet further and I will be looking at an increasing cash position and rapid debt repayments.

Earnings Highlights

{kind=link}

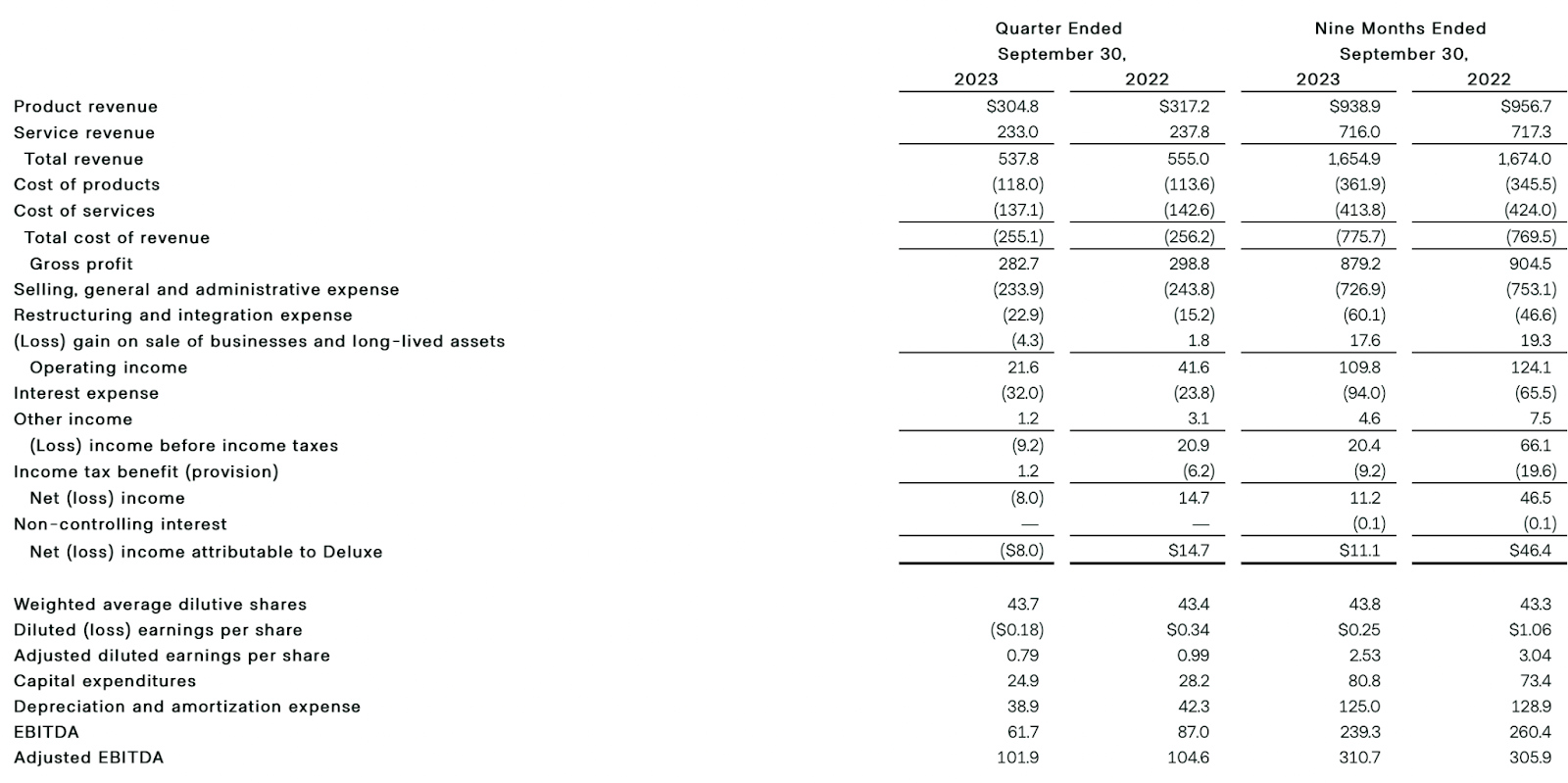

Looking closer at the last income statement by DLX which was released on November 2, 2023 we see a slight decline in the total revenues YoY. It's not a large amount, only down 3.3% YoY and in the face of rising interest rates it could have been a lot worse as a lot of companies are trying to cut down on expenses these days. With DLX working as a solutions provider, though, I think they are in a position where they offer enough positives for companies like improved business operations and margin retention that they have a sticky enough product.

{kind=link}

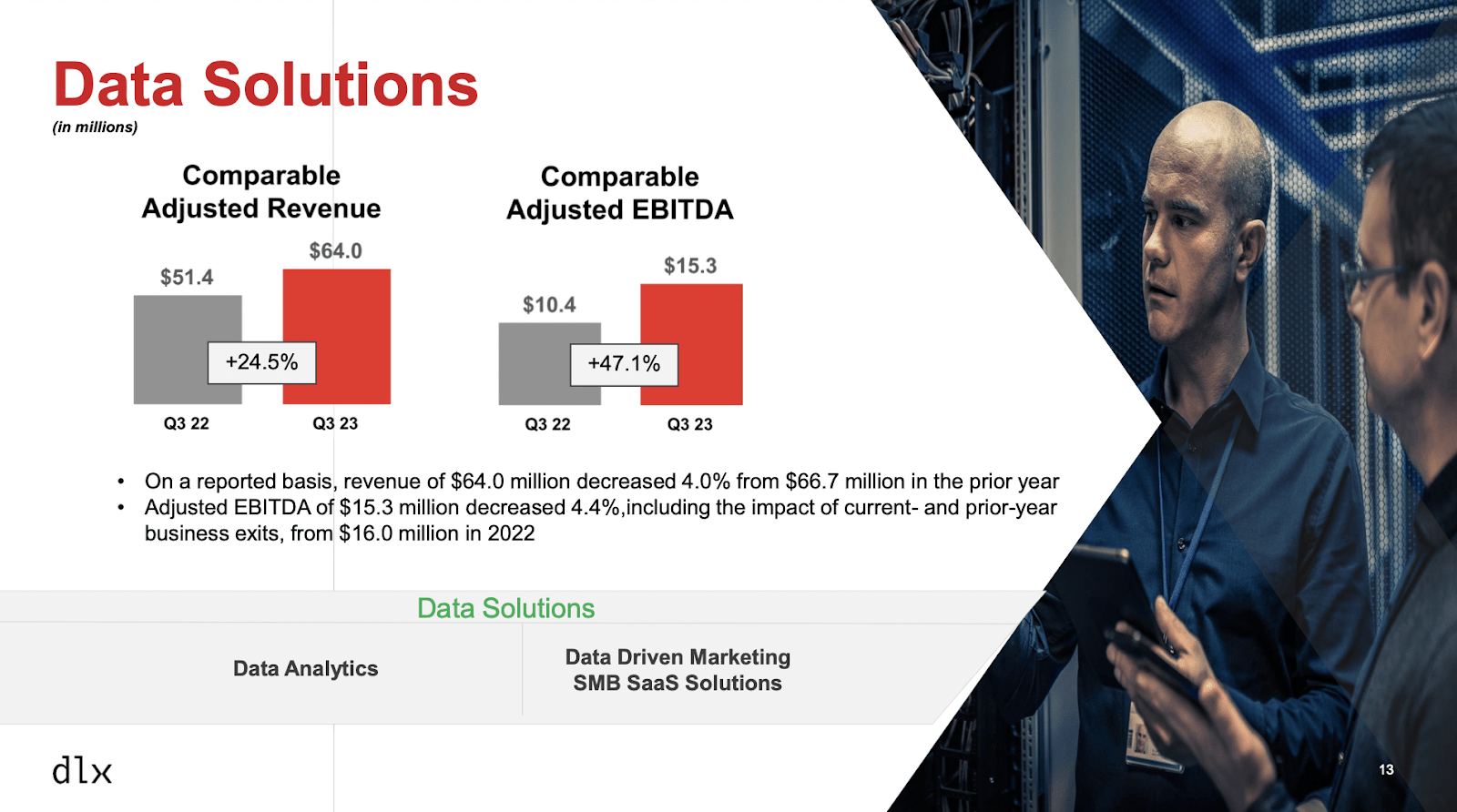

Supporting this assumption about improved retentions in solutions is the fact YoY the segment grew by 24.5% in revenues and 47.1% for the adjusted EBITDA. These are very strong growth numbers, and the solutions program is approaching the third-largest segment quite quickly. I think this is an area that a lot of investors should be looking at in the next few quarters. It will be a great indication of the potential market opportunity for DLX.

{kind=link}

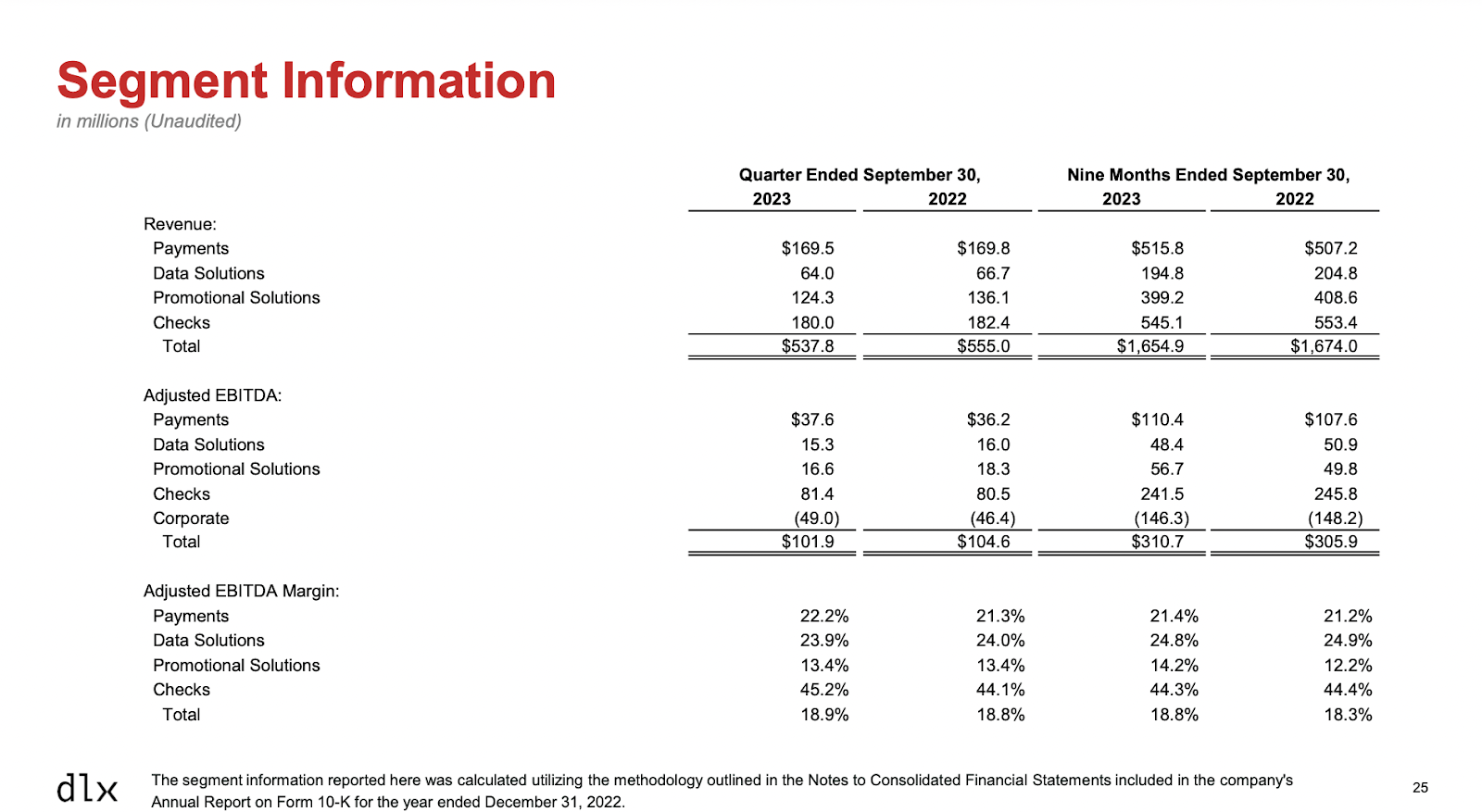

As far as the segment with the highest margins right now, it continues to be the Checks segment at adjusted EBITDA of 45.2%, up from 44.1% a year prior. What was quite interesting was that the data solutions segment which I praised as a significant growth driver for the company was the only one to lose margins YoY, going from 24% - 23.9%. It's not a significant amount but monitoring the margin losses as the revenues expand could be crucial, and a reversal might trigger a quick rise in the stock price for the short term.

{kind=link}

In terms of growth, I think that DLX can deliver a CAGR for the EPS up until 2030 of about 4 - 5% based on the fact some of its segments are growing quite quickly, and with the restructuring of the business I have strong conviction will result in a positive outcome. During this period, investors will also be able to collect the over 6% dividend as well, which I find very appealing. On a p/e basis, I think DLX can trade at its 5-year average of 6.5 which leaves an upside of 10.5% right now. I think investors should brace for some potentially volatile earnings in 2024 as a result of the restructuring. YoY it went from $15.2 million to $22.9 million. Once they are done, however, that is an additional $100 million of net income essentially to the business on an annual basis, which is an additional EPS boost of $2.2. With the 2022 results of $60 million in earnings in mind, that leaves a potential 2025 annual EPS of $3.4. A 6.5 multiple gets us to a target price of $22, enough to warrant a buy here.

Risks

The company is grappling with considerable challenges stemming from the upward trajectory of interest rates. The situation is anticipated to worsen as specific derivatives, utilized to hedge against interest rate risks, are set to expire in March 2023. Furthermore, the company's cash flows have felt the effects of asset disposals, and an ongoing technology overhaul is exerting pressure on both cash flow generation and overall profitability. Collectively, these factors present a complex and challenging scenario for DLX at the present moment. In the last report, for example, the company revised the FCF for 2023 downwards to $60 - $80 million. This still doesn't put DLX at a rich p/fcf, as it's just 4.2 and 18% below its 5-year average.

{kind=link}

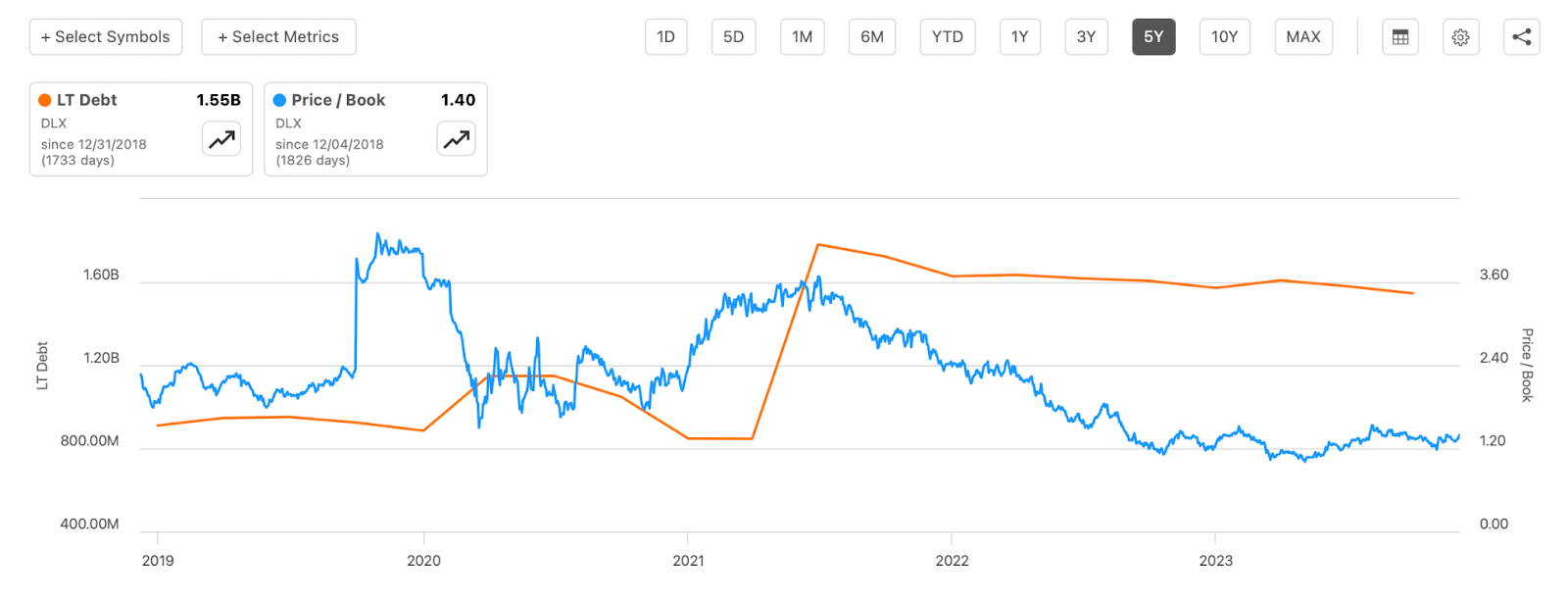

What could be a cause for the low valuation that DLX is receiving right now is the taking on of more leverage on the balance sheet. With a rising debt level now over $1.55 billion, it seems to have been causing the p/b to slowly decline from its highs back in 2021 of over 3.6. I think that should DLX be very proactive in the next couple of quarters and even years in paying back debt quickly, then the market will likely see that as a reason to value the business higher as less risk will be present.

Final Words

The state of DLX I think has improved since my last coverage of the company. In that article, one of my issues was the lack of growth the business has had. Now I think with the project North Star announced there is a more concrete path for DLX to raise its margins and bottom line again and run more smoothly as well. The additional FCF the company is anticipating I think is reasonable and puts it in a position where it can quickly fund future business ventures and drive more revenue growth. My target price is at $22 for DLX right now and leaves a decent amount of upside, along with the benefit of a 6% dividend yield. I am upgrading my previous rating of DLX from a hold to a buy.

For further details see:

Deluxe Corporation: Updated Outlook And Q3 Momentum Results In Rating Upgrade