DLX - Deluxe Sees Payments Deceleration So Watch The Debt

Summary

- Deluxe's results are confounded by the First American acquisition, all that matters is the Q4 figure.

- Deceleration is visible in the payments business, but there's at least better performance in the other segments.

- Checks have lapped unusual growth started in late 2021, and this has been bad for margins.

- Next year, macro matters for growth, and also investors need to realize divestitures are hitting ~6% of EBITDA.

- Data Solutions is getting leaner, and we're glad to see a lack of interest exposure, but DLX stock is likely going to have a 'managed decline' year in 2023 while heavily indebted.

Deluxe ( DLX ) recently reported its earnings. We are seeing signs of macro pressure on the payments business, which isn't growing much in Q4. Other businesses are doing well in the face of divestitures, and direct exposure to interest rates isn't too high in their businesses despite Deluxe's traditional exposure to financial services. The divestitures garnered really poor multiples, probably worse than they should be, but they can do things with the cash like deleverage as interest expense is an issue, and those businesses did not provide growth. Overall, tough comps but macro pressure is going to mean a less exciting 2023, but Deluxe is a much safer company than it was a year ago despite everything - although they still have a lot of debt and investors need to pay attention.

Negatives

Let's start with the negatives we see in this quarter:

- They divested their web hosting and logo business which used to be in promotional services and their data segment. The multiple they're getting on these businesses are really quite low. The Web Hosting business and the logo business which is being sold together is getting $42 million and the EBITDA was around $20 million , meaning a 2x. The business was in decline at around 8% YoY and it is supposedly capitally intensive, but it is profitable and the 2x EV/EBITDA is a low multiple. About 6-7% of EBITDA is going to be affected in the run-rate results for next year, so this amount of declines should be expected assuming no other negative EBITDA effects.

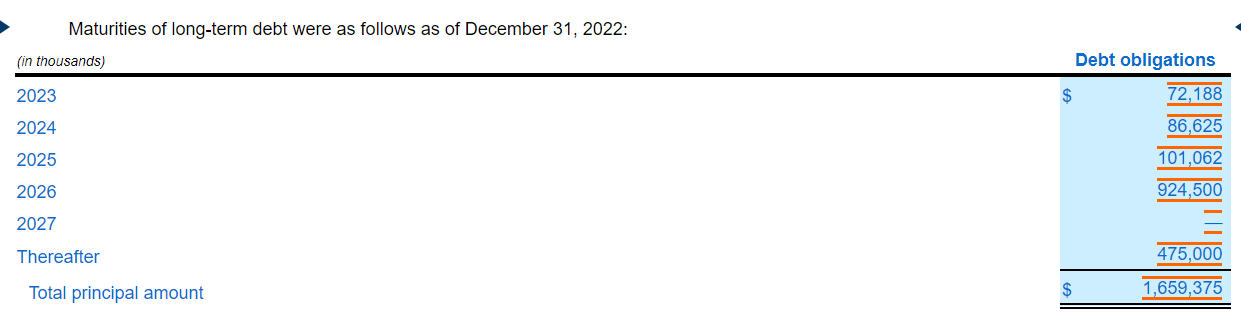

- At least they'll get some cash, because Deluxe is suffering from higher rates due to substantially variable rate debt on its balance sheet . EPS is down 17.5% on an adjusted basis in Q4 as interest expenses have doubled in the full year, and are up 50% in Q4 due to higher base effects than the FY 2021. They have not improved their financial position and maturities are coming in. Thankfully, they are generating enough cash to pay the 2023 and 2024 maturities as it stands, but the leverage is quite serious and a recession could be a problem for the company on account of this. While refinancing is likely it is an undesirable option in the current rate climate.

{kind=link}

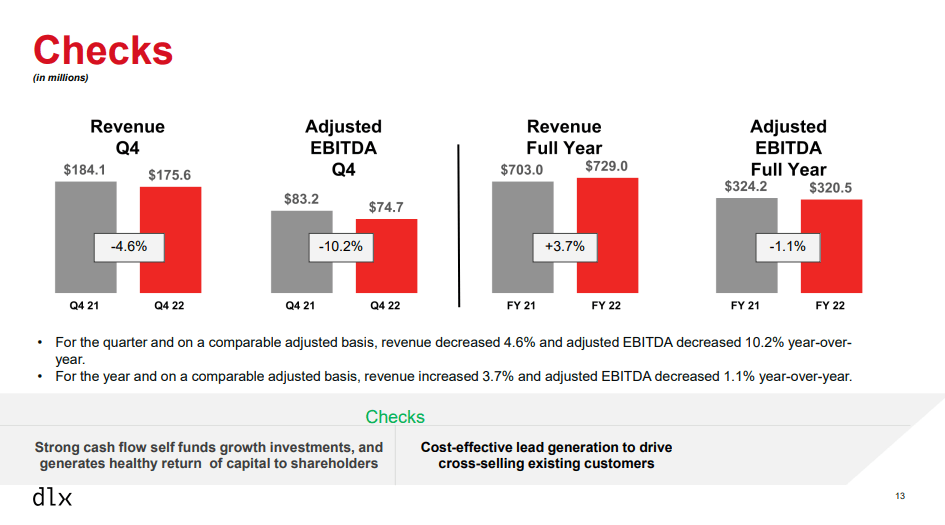

- Also there are going to be more EBITDA pressures as checks declines again in the mix. Checks had a peculiarly growing year in 2022 due to specific contract wins, but those have passed and the business is going back into managed decline. Since checks margins are double the rest of the businesses, the mix effects when it declines in share of revenues are quite nasty.

{kind=link}

- In the Q4 we also see deceleration of the payments business. Partially this is due to difficult comps, but it is also due to macro pressure. Merchant volumes are leading the growth at 3.3% YoY with the overall segment up 2.5%.

Positives

- If you add back the effects of the divestitures, the company is guiding for EBITDA growth and thanks to the payments segment we think they can deliver, even if it is very slight EBITDA growth. Since management is required to be conservative when making these judgements, it's good to see given increasing concern around the economic climate. Deluxe especially needs to be concerned due to its debt.

- Also, within their data solutions business, they have proven to not be that exposed to volumes in business within their traditional financial services clientele that would be negatively affected by the higher rates. These businesses are growing organically.

- Inflation elements are also calming down, in particular logistics costs.

Bottom Line

The dividend isn't bad at 6.54%, but it's for a reason and that's the leverage pressure. Income investors need to consider that if the economic climate deteriorates, although it does look stable for now and also given their guidance, the dividend will be threatened as debt takes obligatory priority. They are likely going to lose cash flow from businesses that they just sold at very impaired values, although management claims they weren't cash generative and that's helpful for dealing with debt.

For further details see:

Deluxe Sees Payments Deceleration, So Watch The Debt