DNLI - Denali's New Summit: Changing Hunter Syndrome Landscape

2023-10-02 05:26:09 ET

Summary

- Denali Therapeutics shows promising early-phase data with DNL310 in Hunter syndrome, alongside robust Q2 financials, including $183.4M net income.

- Despite a strong cash position and revenue diversification, Denali's stock underperformed the S&P 500; due diligence on clinical and fiscal fronts is imperative.

- Upgrade Denali to "Buy" for risk-tolerant investors; compelling early clinical data and financial stability suggest an undervalued opportunity ahead of key milestones.

At a Glance

Denali Therapeutics ( DNLI ) is approaching a defining moment with its upcoming COMPASS trial for DNL310 in Hunter syndrome—a therapy with the potential to redefine the standard of care in an area of significant unmet need. Simultaneously, the firm’s improved financial metrics, including a net income of $183.4M and liquid assets sufficient to maintain current R&D activities, present a compelling financial landscape. However, investors should remain vigilant, scrutinizing upcoming clinical data and management’s fiscal conduct, while also monitoring the firm’s operational spending. Denali's market positioning, weighed against its recent stock performance, alludes to an interesting investment calculus, especially for those tolerant of the inherent risks in biotech ventures.

Q2 Earnings

To begin my analysis, looking at Denali Therapeutics' most recent earnings report for Q2 2023, the company showcased significant gains in collaboration revenue, spiking from $52.5M to $294.1M YoY, primarily attributed to related-party collaborations. Operating expenses increased modestly, with R&D costs rising to $97.5M from $92.7M, and G&A to $26.1M from $21.2M. Dilution impact was minimal, evidenced by an increase in weighted average shares outstanding from 123M to 137M YoY. The net income stood at an impressive $183.4M, contrasting sharply with the $58.8M loss in the same period last year. Overall, robust revenue growth coupled with controlled operational spending translates into an improved financial outlook.

Financial Health

Turning to Denali Therapeutics' balance sheet as of June 30, 2023, the company holds $131.9M in cash and cash equivalents and $1,059.0M in short-term marketable securities, combining for a total of $1,190.9M in liquid assets. The current ratio, calculated as total current assets of $1,224.1M divided by total current liabilities of $69.4M, stands at a robust 17.6. Over the last six months, the net cash used in operating activities amounts to $171.9M, translating to a monthly cash burn of approximately $28.7M. The monthly cash runway, calculated as $1,190.9M divided by $28.7M, equates to around 41.5 months. It's essential to note that these figures are based on past performance and may not indicate future sustainability.

The company's strong current ratio and cash runway of over three years lessen the immediate necessity for additional capital infusion. However, biotech firms often face unpredictable R&D expenditures, which could necessitate financing. Given the positive net income of $73.6M over the last six months, the company appears less reliant on external financing. Therefore, the likelihood of Denali raising equity in the next twelve months seems relatively low, unless undertaken for strategic initiatives or unforeseen operational demands.

Equity Analysis

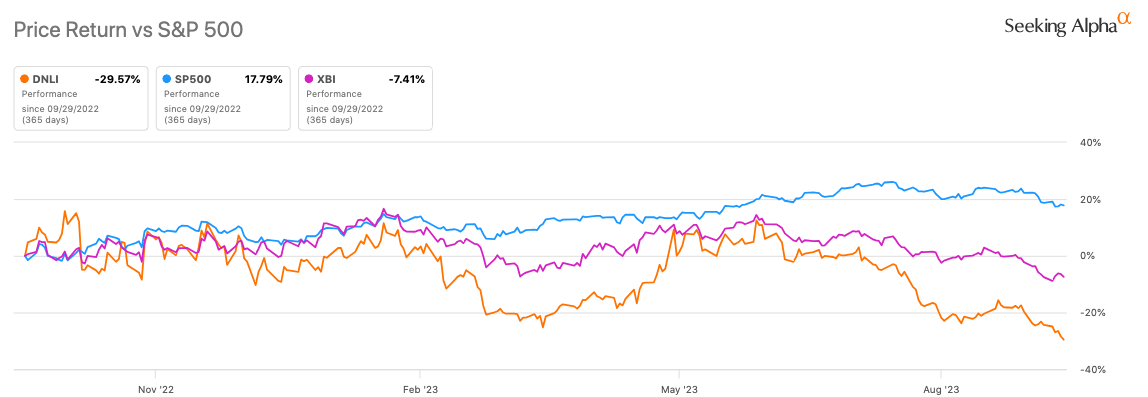

According to Seeking Alpha data, Denali Therapeutics commands a market capitalization of $2.84B, signaling moderate market confidence given its strong clinical pipeline. Analysts project a spike in 2023 revenues to $350.49M, followed by a contraction in 2024; this volatility underlines the company's dependency on its late-stage trials. DNLI underperformed against the S&P 500 across all timeframes, most strikingly over a one-year period (DNLI: -29.57%, SPY: +17.79%), indicating bearish stock momentum. The 24-month beta of 1.38 suggests the stock is more volatile than the market.

{kind=link}

Short interest stands at 7.57%, with a days-to-cover ratio of 15.58, signaling some skepticism about near-term growth. Institutional ownership accounts for 74.26% of shares, consolidating decision-making among a few key players. Insider trading reveals a trend towards automatic sells , though the volumes aren't large enough to signal a mass exodus.

Addressing CNS Impact in Hunter Syndrome with DNL310

The COMPASS trial is a critical inflection point for DNL310, a front-running therapeutic candidate targeting Hunter syndrome, a lysosomal storage disorder caused by a deficiency in iduronate-2-sulfatase (IDS). Current standard-of-care options like enzyme replacement therapy [ERT] fall significantly short in addressing the CNS manifestations of the disease, owing to their inability to cross the blood-brain barrier. DNL310 has shown promise in this unmet need by normalizing cerebrospinal fluid [CSF] heparan sulfate levels—a key biomarker indicating disease severity—sustained at weeks 49 and 104 in all participants. Notably, this was true even in patients with high levels of preexisting antidrug antibodies, underscoring the therapy's durable efficacy.

The normalization of CSF lysosomal lipids observed in most participants suggests a broader correction in lysosomal function, crucial for a disease driven by intralysosomal accumulation of glycosaminoglycans (GAGs). With 33 patients having a median treatment duration of 91 weeks, the safety profile remains favorable, characterized mainly by mild-to-moderate treatment-emergent adverse events (TEAEs) and declining incidences of infusion-related reactions (IRRs), lending further credence to DNL310's potential as a long-term treatment option.

The upcoming global Phase 2/3 COMPASS trial aims to enroll 54 participants and will include cohorts both with and without neuronopathic complications. This Phase 2/3 study not only aims to substantiate the preliminary efficacy seen in Phase 1/2 but also serves as a pivotal trial for regulatory submissions. Given the high unmet medical need in Hunter syndrome, particularly in mitigating neurological impact, DNL310 could swiftly ascend to market leadership if the COMPASS trial data align with early-phase outcomes.

The stakes are high, and investors and clinicians alike should closely monitor the forthcoming data from the COMPASS trial for definitive validation of DNL310's efficacy and safety profile.

My Analysis & Recommendation

In closing, Denali Therapeutics appears to be on the cusp of a transformative phase. With pivotal COMPASS trial data on DNL310 for Hunter syndrome on the horizon, the stakes are undeniably high. But it's worth reiterating that the early-phase data indicate an ability to normalize key biomarkers like cerebrospinal fluid heparan sulfate levels, addressing a significant unmet need. Considering Hunter syndrome's neurological impact, the implications for DNL310 extend beyond merely incremental improvements in existing treatments; we're potentially talking about paradigm shifts in the standard of care.

The company’s improved financials—showcasing a net income surge to $183.4M and robust liquid assets—mitigate the near-term risk of dilutive equity raises, a crucial point for existing shareholders. Additionally, the substantial gains in collaboration revenue underscore a diversification in income streams, reducing the dependence on single-product success.

However, investors should be keenly aware of certain vital metrics in the coming weeks and months. Monitor the progress of the Phase 2/3 COMPASS trial and scrutinize any interim analyses; pay close attention to safety profile nuances, especially with prolonged treatment durations. Keep an eye on management’s use of accumulated capital, especially in fostering pipeline diversification. Weigh the company’s performance vis-à-vis operational expenses, as cost creep could erode the solid financial standing. Finally, stay attuned to the broader biopharmaceutical market trends, especially around neurodegenerative and lysosomal storage diseases, where Denali has the potential to carve out an even larger market share.

Having weighed all factors, including the 33% stock drop since July—which appears to be an overreaction relative to the firm’s intrinsic value and growth potential—I'm adjusting my previous stance. I recommend upgrading Denali Therapeutics to a "Buy" for risk-tolerant investors. Given the positive early data in Hunter syndrome and the broad applicability of their proprietary Transport Vehicle technology, this could very well be a discounted entry point before a series of value-inflection milestones.

In the spirit of superforecasting, this recommendation is contingent on a continued trajectory of positive clinical data and prudent financial governance. Admittedly, biotech investments are fraught with risk, but Denali offers a compelling risk-to-reward ratio that is too persuasive to ignore at this juncture.

Risks to Thesis

While the investment thesis for Denali Therapeutics appears robust, several counterpoints could challenge my "Buy" recommendation. First, regulatory risk is ever-present. The FDA or other regulatory bodies may require additional data, delaying DNL310's time-to-market and giving competitors a window. Second, Hunter syndrome is a rare disease, and pricing pressure could severely impact revenue, particularly if payers push back on costs. Third, the COMPASS trial's success is not a given. Failed endpoints could plummet the stock. Fourth, the heavy reliance on collaboration revenue exposes Denali to counterparty risk. Finally, the market has priced in some future success; any setbacks could lead to a revaluation downward. These variables necessitate a conservative yet vigilant investment approach.

For further details see:

Denali's New Summit: Changing Hunter Syndrome Landscape