DNN - Denison Mines: Leverage To Future Uranium Prices At A Reasonable Valuation

2023-06-15 16:05:18 ET

Summary

- Uranium prices are rising, and sentiment might quickly improve among uranium equities.

- Denison Mines has a world-class asset in its Wheeler River project, potentially one of the lowest cost uranium mines globally.

- Denison also has several potential catalysts on the horizon, such as Phase 3 of the Feasibility Field Test and the release of the updated Phoenix Feasibility Study.

The big picture: uranium and uranium equities

Uranium prices are quietly rising, but it remains unclear whether this recent movement is driven by speculators front-running the launch of the Zuri-invest Uranium Actively Managed Certificate , or if it signifies a more significant structural change in the uranium market. However, investment vehicles like the Sprott Physical Uranium Trust (SPUT) are not responsible for this price increase, as SPUT has been trading at a discount to NAV since March.

Therefore, we are observing an interesting divergence at the moment. Sentiment in the uranium sector is low, as evidenced by the 50% correction of many uranium equities from their previous highs. However, simultaneously, both the uranium spot price and long-term price are showing an upward trend. If we are indeed at an inflection point where the uranium market is returning to being production-driven, an opportunity presents itself for investors in uranium equities. A rising uranium price has the potential to increase the valuation of uranium equities, particularly when sentiment shifts and capital flows back into the sector.

Investing in uranium equities presents a challenge due to the limited size of the investment universe and an even smaller investable sub-universe. Valuations of uranium equities have generally been unattractive for some time, particularly considering the inherent risks associated with most companies in the sector. As a result, a more favorable risk/reward profile can generally be found in physical uranium investments.

Among the equities, Kazatomprom stands out as it is currently undervalued and offers significant leverage to uranium prices. However, it is affected by a rising geopolitical discount. On the other hand, Cameco is arguably the primary beneficiary of the ongoing changes in the uranium market. Nevertheless, it is trading at a relatively high valuation.

Additionally, there are numerous exploration and development companies operating in the uranium sector, providing further investment options, but these companies come with their own set of risks and considerations.

About junior uranium companies, I was writing back in March :

I would be interested in re-entering the uranium juniors space in case of a market sell-off event, as I believe the easy money has probably already been made in this sector (the best moment to buy was when it was left for dead in 2020) and that the current margin of safety is not enough for most names.

Despite the absence of a market sell-off event, there has been a departure of speculative money from the uranium sector. Therefore, although not as inexpensive as in 2020, I believe that many junior uranium companies present again the potential for substantial gains from the current price levels.

Denison Mines: attractive uranium assets at a reasonable price

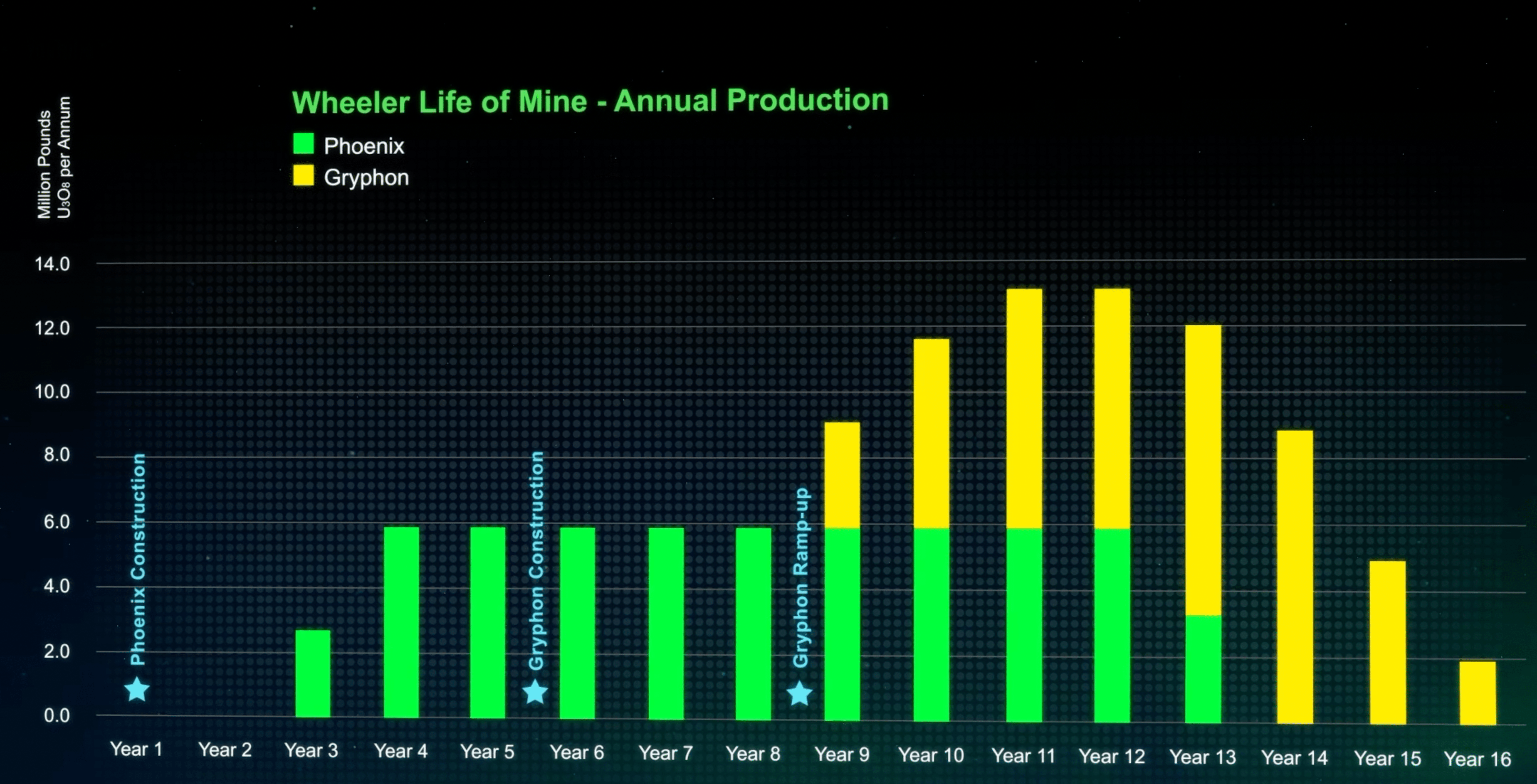

Denison Mines ( DNN , DML:CA ) is one of a handful of reputable junior uranium companies. Its flagship Wheeler River project, in the renowned Athabasca basin , is world-class. The project has robust economics, thanks to its high grades and low operating costs. It also has the advantage of being a large deposit, with projected cumulative production of around 100 million ounces over a life of mine of 14 years.

According to the NI 43-101 Prefeasibility Study conducted in 2018, development at Wheeler River is anticipated to occur in two separate stages. The Phoenix deposit, larger in size, will be developed initially as an in-situ recovery (ISR) operation, while the slightly smaller Gryphon deposit will be developed as a conventional underground operation.

Let us remind the reader that ISR is a method for extracting uranium by injecting a leaching solution into the ore deposit by means of injection wells. The resulting uranium-rich solution is then pumped to the surface, where impurities are removed, and the uranium is extracted through chemical processes, resulting in the production of yellowcake . Uranium is therefore pumped out of the ground, not too differently from oil.

One advantage of ISR is that it minimizes the environmental impact compared with conventional mining methods. In many cases, ISR can be more cost-effective, as it requires fewer infrastructure investments, which reduces capital costs. Additionally, operating costs are typically lower since development can be ramped up more gradually and requires less labor. The lowest-cost uranium mines in the world, owned by Kazatomprom, all used ISR.

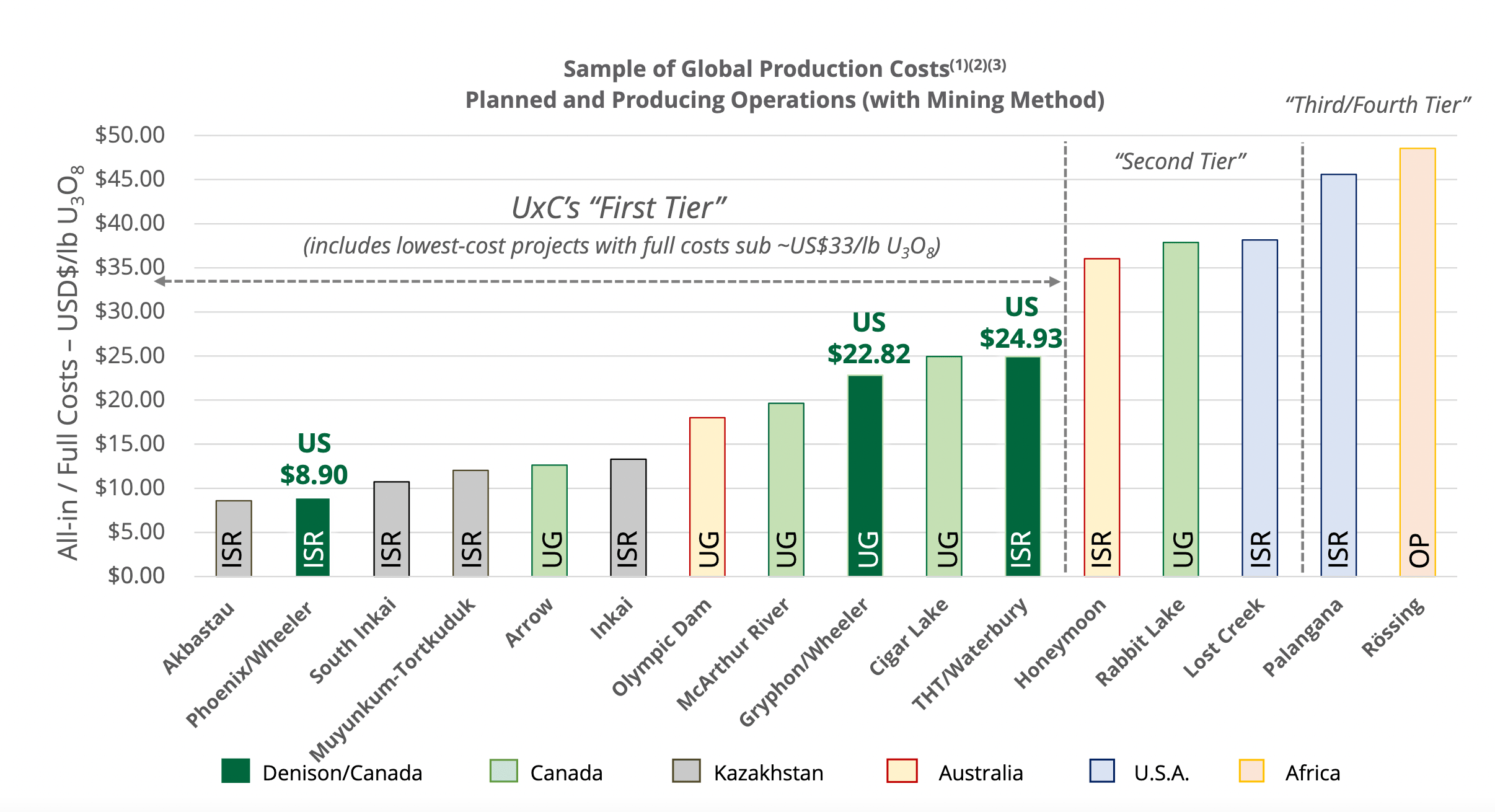

By leveraging ISR methods, Phoenix has the potential to become one of the lowest cost uranium mines in the world. It could produce an estimated 6 million pounds of uranium per year, over a life of mine of 10 years. Cash operating costs are estimated to be around $3.33 per pound, and all-in sustaining costs around $8.90 per pound. With $240 million of initial capex, the pre-tax NPV 8% comes out at $1.43 billion. For comparison, the company current market capitalization is around $1 billion, and Phoenix is just one part of Denison's portfolio. All numbers are taken from the 2018 Prefeasibility Study , assume a uranium price of $65 per pound (a realistic target for when Phoenix could enter into production), and are given on a 100% basis (this does not change much the bottom line since Wheeler River is 95% owned by Denison).

Gryphon is a potential second operation that could be developed conditional on market needs. It would produce 7.6 million pounds over a shorter life of mine of 6.5 years. As a conventional underground operation, both capital and operating costs would be higher: initial capex is estimated at $470 million, cash operating costs at $11.70 per pound, and all-in sustaining costs at $22.82 per pound. The pre-tax NPV stands at $750 million.

The combined NPV of the Wheeler River project exceeds $2 billion. Additionally, Denison holds participating interests in several development-stage assets operated by major uranium companies. These include interests in McClean Lake (22.5%) and Midwest (25.17%), both operated by Orano, as well as a 15% effective interest in Millennium operated by Cameco. This portfolio provides potential value and exploration catalysts. Denison also holds a 67% interest in the Waterbury project, a smaller deposit with an estimated production of 10 million pounds over a 6-year mine life, representing an NPV of $118 million (on an attributable basis).

In conclusion, Denison has a world-class portfolio of uranium assets. Its Wheeler River project could turn into one of the highest-grade, lowest-cost uranium mines globally. In addition, it is trading at a more than 50% discount to NPV, even excluding its smaller investments in uranium equities. The management team is top-notch. The balance sheet looks solid.

Denison Mines currently maintains a debt-free status and holds $43 million in cash and cash equivalents as of Q1 2023. Additionally, the company possesses 2.5 million pounds of physical uranium as a long-term investment, with a market value of approximately $140 million. However, to proceed with the development of the Phoenix deposit, Denison will need to secure additional funding, considering the estimated capital expenditure of $240 million from the Prefeasibility Study. It's worth noting that this estimate may require revision due to inflation.

One notable advantage for Denison is the favorable jurisdiction of Saskatchewan, Canada, known for its mining-friendly environment. Tier-1 mining jurisdictions generally command a premium. In the case of uranium, geopolitics can be expected to play an even more significant role. Given the concentration of uranium resources in countries such as Kazakhstan, Russia, and Namibia, along with the ongoing Russo-Ukrainian conflict, concerns about supply security have risen to the top of the agenda. This situation may lead to a potential division within the uranium market, with the West aiming to achieve independence from Russia and its political allies. Developers located in Western-friendly jurisdictions are anticipated to benefit from this trend. Their deposits will be in demand since the uranium market faces a structural deficit, and new mines are required to address the shortfall. Denison is well-positioned in this regard, as it holds interests in three of the six lowest-cost projects within Tier-1 jurisdictions, excluding Kazakhstan.

Sample of Global Production Costs (Company's Presentation)

{kind=link}

At the same time, as a development-stage company, investing in Denison remains highly speculative. Therefore, it is important to consider also the potential risks associated with this investment thesis. Firstly, the Prefeasibility study will require updating. While the release of the Feasibility Study is expected soon and could act as a near-term catalyst, there is a risk that cash costs may experience a significant increase, leading to downward revisions of NPV estimates due to inflation. Secondly, as previously mentioned, Denison will need to raise additional funds, making some degree of dilution unavoidable. Thirdly, there are technical risks involved in the development of the Phoenix project. Although ISR techniques are utilized globally, the specific solution proposed for Phoenix is considered technically challenging and has limited prior testing, introducing a clear risk factor.

On paper, the development of a Feasibility Field Test (FFT) has mitigated a significant portion of the risk. The FFT, designed to validate production and remediation profiles of ISR techniques at Phoenix, is being conducted in three phases, with the first two phases successfully completed. The company has expressed confidence in the success of the third phase, which involves the final separation of uranium mineralized precipitates from the recovered solution. Denison also claims that a new "freeze wall" design at Phoenix, to be disclosed in the upcoming Feasibility Study, will result in a 50% improvement in ISR uranium head-grade. However, I lack the expert knowledge to evaluate the reliability of these claims.

Wheeler River life of mine (Company's website)

{kind=link}

Conclusions

Denison Mines presents a speculative investment opportunity, particularly given the recent movement in the uranium market. If uranium continues to gain momentum, it could lead to improved sentiment within the uranium equity sector. Denison stands out as one of the top-quality companies among junior developers, with its flagship Wheeler River project being of world-class caliber. Despite its strong potential, the company currently trades at a notable discount to its net present value. Denison also has several potential catalysts on the horizon, such as the testing of Phase 3 of the Feasibility Field Test (FFT) and the release of the updated Phoenix Feasibility Study. However, it is important to acknowledge that investing in Denison carries high risk, as first production is still several years away, and the development of Phoenix is expected to be technically challenging.

For further details see:

Denison Mines: Leverage To Future Uranium Prices At A Reasonable Valuation