DENN - Denny's: Consistent Winner In A Period Of Consolidation

2023-05-03 03:53:10 ET

Summary

- Denny's Corporation is a restaurant chain operator that owns and franchises full-service restaurants under the Denny's and Keke's Breakfast Cafe.

- Denny's achieved 9 successive years of system-wide growth, which has continued following the covid-impacted FY20.

- Margin improvement has come from a strategic shift by the business, although inflationary pressures are mildly offsetting this.

- Denny's valuation does not imply an upside.

Investment thesis

Our current investment thesis is:

- Denny's is making the correct decisions to continue long-term growth, be it mild in size.

- Margin improvement through franchising and increasing ghost kitchen growth should help drive improvement.

- Large distributions have contributed to an overleveraged balance sheet in our view, suggesting focus must change in the near term.

- Markets have already priced in the improved Denny's, leaving little more to gain today.

Company description

Denny's Corporation ( DENN ) is a restaurant chain operator that owns and franchises full-service restaurants under the Denny's and Keke's Breakfast Cafe brands in the US and globally.

Share price

Denny's share price has performed relatively well in the last decade, especially when you consider the pre-covid period. The stock gained consistently from <$6 to over $20. Since then, the share price has been quite volatile, likely a reflection of the changing industry dynamics following the pandemic.

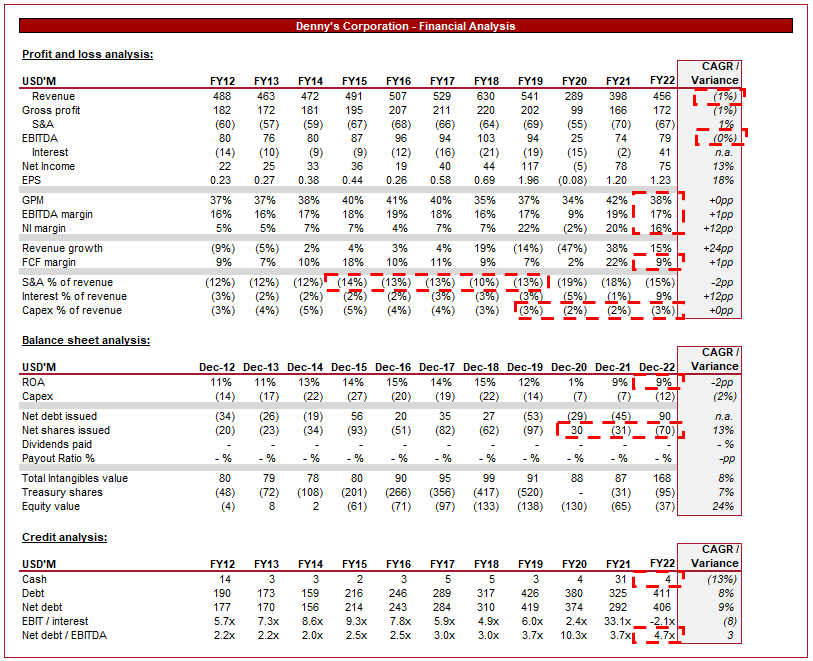

Financial analysis

Denny's financial performance (Tikr Terminal)

{kind=link}

Presented above is Denny's financial performance for the last decade.

Revenue

Denny's revenue has seemingly declined across the historical period, with a (1)% CAGR. This is a reflection of the company's franchising strategy, which has shifted the top-line performance in exchange for derisking and bottom-line gains.

We are bullish on the franchising that many US restauranteurs have been pushing in the last decade. The benefits are clear. Denny's no longer has to bare the risks of property ownership/leasing (reducing its balance sheet size), it does not need to employ the staff, and it reduces exposure to sales risk. While doing so, its cost base rapidly shrinks and allows the business to improve margins. Finally, the profits it moves into the hands of the franchisees are offset by the ability to grow at a faster rate. Multiple franchisees can open locations faster than a single corporate. This is why we have seen revenue decline despite the clearly improving profitability.

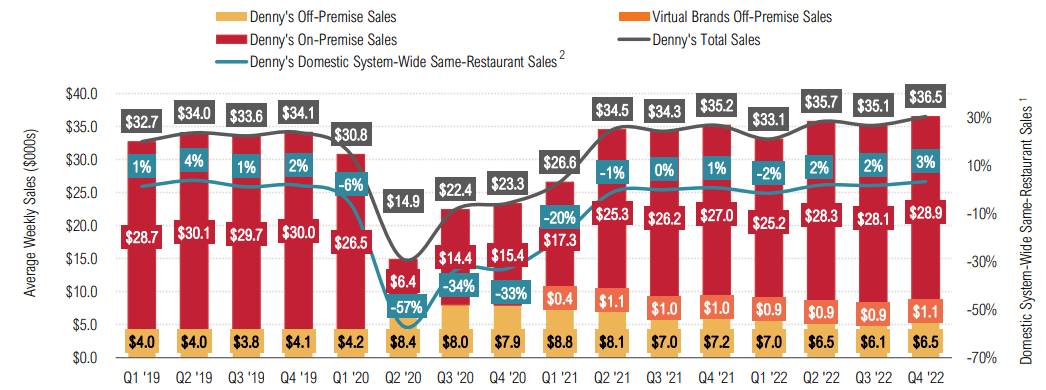

For this reason, assessing growth should be done by analyzing system-wide growth. Between Q1-19 and Q4-22, SW sales grew at an annual rate of 1.6%. This reflects the impact of the pandemic, with historical growth suggesting closer to 2-2.5% is achievable. This is a mild performance and a reflection of what is a mature industry. The consistency is key here, between 2010 and 2019, the company experienced consecutive same-store sales growth.

{kind=link}

Our view is that mild growth is a reflection of what has been a turbulent time for the restaurant industry in the US. We have seen the rise of delivery apps, such as DoorDash ( DASH ), taking over the country as consumers value the convenience and accessibility it offers, relative to alternatives. The pandemic accelerated this for many, acting as a successful "proof of concept". Those most negatively impacted in our view are the traditional leaders in the market and sit-down establishments. If this was a Venn diagram, Denny's would be squarely in the middle. The reason for the former is that these apps, and the digital revolution in general, have allowed consumers to far more easily discover new places to eat, no longer defaulting to the large chains. This is one of the primary reasons we think Wingstop (WING) is growing as it is. Consumers scrolling apps for where to eat are now subject to an algorithm/advertising spend. Regarding the latter, the argument is simple. It's extremely easy, nationally, to get access to all the best restaurants at home... so why would you drive to a location and eat in? The value proposition needs to be higher, consumers need it to be an occasion.

The good news for Denny's is that they are improving. Off-premise sales were c.$4m per quarter prior to Covid, now sitting in the mid-$6m. Further, the business has virtual brands, a fantastic strategic decision, which also contributes c.$1m. As the numbers above reflect, this digital penetration has allowed Denny's to exceed its pre-covid levels. The creation of these virtual brands (Ghost kitchens) gives consumers the impression they are trying something new, which is a key risk we suggested above, allowing Denny's to partake in the uptick use of apps disproportionately. The only concern with this strategy is that the portion of sales through delivery apps is increasing, which is a margin-slimming segment.

Channel for off-premises (Denny's)

Denny's has some overseas exposure, with 58 locations outside of the US, Canada, and Mexico (With a total of 1,602). Given how entrenched in American culture the brand is, we believe it's difficult for true global expansion to occur in the same way KFC, Subway, etc. have achieved. We highlight this because the current strategy of franchising and increasing restaurant locations works best when there is a large runway for openings.

Geographical footprint (Denny's)

Another factor impacting demand is an increased focus on healthy eating (as well as a change in dietary demands, such as Vegetarian and GF). Consumers are demanding healthier options on restaurant menus and generally looking to eat cleaner. This does not look to be a trend but recognition and understanding of dietary requirements and the impact of poor health. Denny's has responded to this by offering healthier menu options, such as low-calorie choices. The problem with this factor growing its customer base, as Denny's current clientele are not necessarily those who are extremely health conscious.

Economic considerations

Inflationary pressures are continuing to cause uncertainty economically, with slowing demand in some industries and surprising resilience in others. Theoretically, heightened inflation with rate hikes spells a disaster for demand, as consumers turn defensive with their cost of living rising. This has not occurred to the extent expected, but there is certainly a degree of weakness. Restaurant dining is discretionary in nature, and less cost-effective than cooking or cheaper take-out meals, which would suggest Denny's is positioned to suffer.

The restaurant industry is currently experiencing a labor shortage, making it challenging for businesses to find and retain qualified staff. This is partially a hangover from the pandemic, where many employees were let go or found better jobs, contributing to a rapid increase in wage inflation. Denny's has been forced to increase wages and improve employee packages in order to retain and acquire staff.

Margin

Denny's has seen its margins improving across the historical period, which reflects the franchising strategy in recent years and scale economies. In 2019, for example, 105 restaurants were franchised alone.

We have seen a dip in the most recent year, reflecting inflationary pressures, offsetting the high-margin ghost kitchen operations. Our view is that Denny's needs to be more aggressive with pricing for faces losing out of margins.

Balance sheet

Denny's balance sheet is less robust. The company's debt balance has rapidly accelerated in recent years, with a ND/EBITDA ratio of 4.7x. Our view is that a 3x level is an appropriate maximum. This is a reflection of Denny's investment in growth, but also why franchising is so attractive. Management has identified it has reached the maximum it can borrow, which could stifle distributions and/or growth.

Speaking of distributions, Management has been aggressive with buybacks, reducing share count by a 1/3 since 2014.

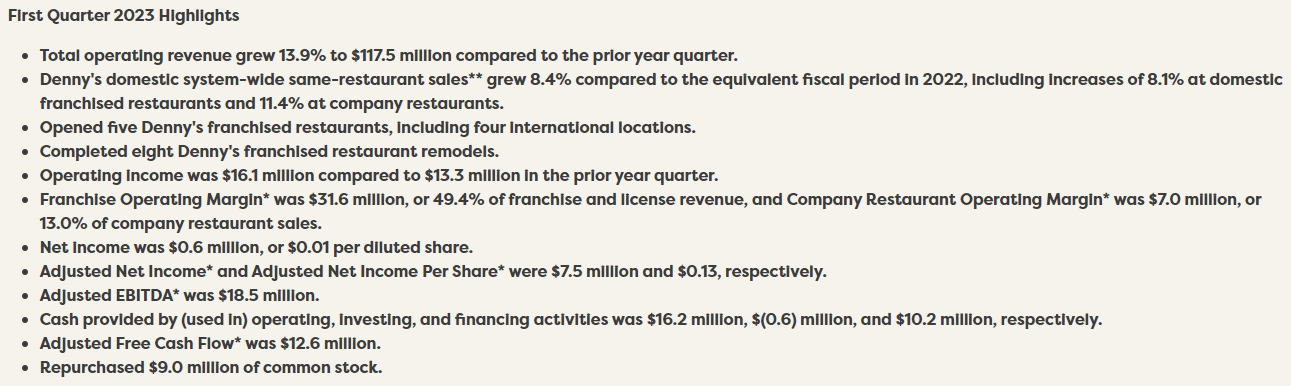

Q1-23 performance

{kind=link}

Denny's recently announced its first quarter performance , with no material movement in share price.

The company is flexing is resilience, with system-wide same-restaurant sales up 8.4%. This has come without a slippage in margins, with a slight increase compared to the prior year.

Further, the business is continuing its franchising push, which is improving the long-term returns for the business. This reflects that a Denny's franchise ownership remains attractive to investors.

Management's FY23 outlook is for 3-6% system-wide same-restaurant growth, during what should be a difficult year for the business. This is very impressive but will be materially offset by 4-6% forecast commodity inflation and 5% labor inflation.

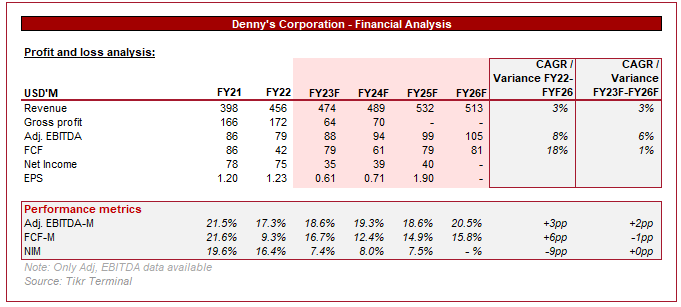

Outlook

{kind=link}

Presented above is Wall Street's 5-year forecast.

Revenue is expected to be reasonable at 3%, which looks appropriate based on the company's commercial profile. The digitalization of the industry will continue to be an issue, but Denny's is smart to offset the impact.

Margin improvement is forecast, although not to the level achieved in FY21. This is a reasonable view as it is based on the assumption that commodity prices decline somewhat once inflationary pressures ease, with some costs remaining at their new normal.

Valuation

Denny's is currently trading at 13x LTM EV/EBITDA and 12x NTM EV/EBITDA. This is above its historical average of c.9x for both. Our view is that this is warranted, owing to the company's improved profitability, expansion into ghost kitchens, and franchising effort. This said, we are struggling to see the upside opportunity here.

The company has increased its debt to a level where further raises will come at a significant cost to the business (Interest expense is already 9% of revenue). Therefore, distributions will have to slow, as will expansion. We see a period of consolidation, as the business deleverages and consolidates its post-Covid position.

Final thoughts

Denny's is a great business that has shown dine-in can still be an attractive business model. We like the strategic decision-making currently, be it franchising or the ghost kitchens and the consistent system-wide sales growth shows fundamental brand value. Our concerns are more near-term in nature, which will be compounded by the uncertainty of weakening performance in the coming year.

For further details see:

Denny's: Consistent Winner In A Period Of Consolidation