XRAY - Dentsply Sirona: Consumables Growing Still Too Pricey

2023-06-07 19:03:45 ET

Summary

- DENTSPLY SIRONA Inc. faces challenges in its technologies and equipment business, and valuations seem unsupportive at current levels.

- The company is building momentum in its higher-margin consumables segment, but more time is needed to observe its direction.

- We reiterate a hold stance on XRAY and recommend watching the firm's consumables segment closely and observe any changes in trend.

Investment Summary

As we stroll through the year, investors have a full suite of macro-data to sift through: surging rates, sticky inflation, weak market internals, narrow market breadth, and earnings pressures. For listed companies, it is the same.

It has been equally as challenging for DENTSPLY SIRONA Inc. ( XRAY ) to navigate, evidenced by its financial and equity stock performance since FY'20. I had reiterated a hold stance on XRAY last June , and following its run from October-May, it was necessary to revisit the investment thesis.

Looking at the latest data, there doesn't appear to be a change in the forward estimates for XRAY in my view. For one, there is still mud to sift through in its technologies and equipment business, not to mention cost challenges in decompressing its gross margin. As a positive, it is building momentum around its higher-margin consumables segment, but I'd like more time on this to observe where XRAY is going with the division. That, and valuations are entirely unsupportive at the current levels, asking 20x forward earnings when you can simply buy the benchmark indices at a discount to this (and participate in the H1 FY'23 rally, mind you).

For the company, that rhymes with The Knack song, "My Sharona", it will be a challenging FY'23 and there's not yet the data to suggest XRAY warrants immediate investment in my view. Net-net, reiterate hold.

Figure 1.

{kind=link}

Q1 Earnings - Full Dissection

It was a decent start to the year for XRAY. It clipped organic sales growth of 5.1%, ahead of the management's guided 1%. Consumables continue to lead the growth charge, posting reasonable incremental gains on an incremental basis, as discussed later.

In that vein, the 3 critical factors going forward in my opinion are:

- Core business growth-- It was a pleasure to observe the revenue upsides, that came ahead of consensus. This was a critical result in my view, and sets the company up to do c.$3.9Bn in business for FY'23. You're getting XRAY back towards pre-pandemic turnover at this range.

- Strategic commercial investments-- As you'll see here XRAY is winding up the growth portion of its SG&A spend. This is to be primarily driven by increased headcount and attendance of trade events. This use of capital signals a focus back to long-term growth. Naturally, you'd expect the investment into its sales force to drive sales performance if successful.

- Capital return to shareholders-- The return of cash to shareholders through the firm's dividend and the accelerated share repurchase program is notable and must be heavily considered in the investment debate as well. You've got a 1.4% forward yield at the time of writing.

Turning to the financials . XRAY booked Q1 revenue of $978mm, a marginal growth of 0.9% YoY. However, it's worth noting the $40mm FX headwind during the quarter. Excluding this, core business turnover grew by 5.1%, as mentioned. Moving down the P&L, it pulled the top-line to 54% gross on core EBITDA margin of 16.4%, after a 2.2% increase in SG&A spend, as mentioned.

Sales were driven by geographic performance in its U.S., Europe, and Latin America markets, and if you exclude China from the mix, XRAY's core sales were actually up 6.6% for the period.

This is integral to XRAY's re-rating moving forward in my view. For one, it attracts stronger hands into buying the stock, given the fundamentals. It also may justify a higher market valuation. Most importantly, however, it is the major catalyst to suggest XRAY has successfully embarked on its new voyage to create shareholder value, a voyage that could see its stock price trace back toward May FY'21 highs.

Divisional highlights

Critically, growth percentages in XRAY's consumables division are leading the charge as part of the firm's rebuilding phase. In contrast, the technologies and equipment ("T&E") business continues to lag.

Comparative segment analysis reveals that:

- Q1 organic sales in the T&E segment grew by 1.7% YoY [Figure 2]. T&E was driven by a substantial increase in Aligners sales, exceeding 25% compared to the previous year. Furthermore, XRAY reported growth in its U.S. CAD/CAM business.

- In contrast, consumables grew 9.8% to $430mm in sales and $131mm in quarterly operating income.

The consumables-led growth has been one major takeout for XRAY over the last 3-years. Distribution of income has transitioned towards this division at the expense of T&E, a clear indication of management's priorities. It is growing at multiples, based on the following record:

Figure 2 .

Data: Author, XRAY SEC Filings

From the data, several observations are made:

- Whilst quarterly turnover in T&E has shrunk from $565mm-$548mm in the last 12 months ($17mm decrease), revenue generated via consumables sales has made up the shortfall with another $26mm in incremental turnover from last year.

- In terms of absolute profitability, the weighting is all consumables as well, producing $131mm in operating income last quarter, vs. $67mm for the T&E division (30.5% operating margin vs. 12.2%, respectively).

- Subsequently, looking back to FY'20, XRAY has added another 13 percentage points in operating margin to its consumables segment, whilst growing quarterly pre-tax earnings by 111% from Q1 FY'20-FY'22. In contrast, you'll note the 9 percentage point and c.40% decrease in the T&E division in the record below:

Figure 3.

Data: Author, XRAY SEC Filings

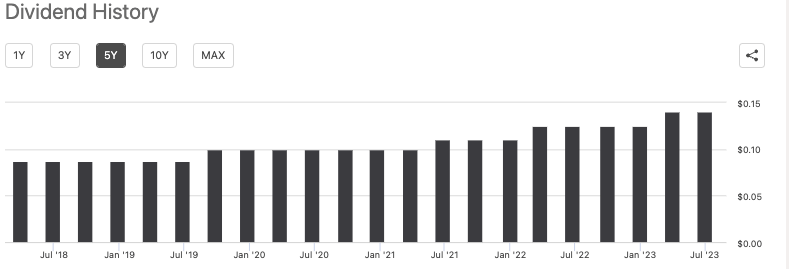

I'd finish dissecting the quarter by noting the firm's $27mm dividend payout and $150mm authorized buyback program, which are notable features in the debate here. Nothing outstanding on the yield front, however, that XRAY remains committed to adding value for shareholders is worthy of noting. Five years of steady dividend growth attest to this [Figure 4].

Figure 4.

{kind=link}

Guidance upgrades telling on forward momentum

Extending from the points on top-line growth above, the firm has revised FY'23 guidance to the upside. It now calls for $3.95Bn at the upper range, around 200bps core business growth. You'd expect a c.100bps FX headwind baked into these assumptions.

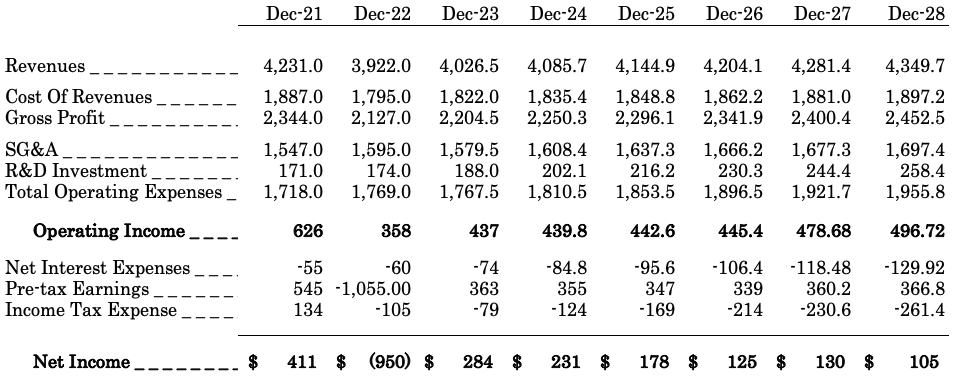

My numbers have XRAY to do $4Bn in business this year and I pull this down to $437mm in core EBIT and $284mm in earnings. Notably, this is above management's estimates, and also above what the consensus of sell-side analysts have forecasts (in my view, there is also a discrepancy between these projections, my own, and the market's consensus, discussed later in the valuation section). I would call for $440mm in EBIT in FY'24, and in my view, the company would need to do at least $4.08Bn in turnover to get to this number. It could do $4.2Bn by FY'26 on these assumptions, and this would make XRAY a company doing $340mm in pre-tax earnings once more. You can observe my FY'23-'28 forward estimates for XRAY in Figure 5 and visually in Figure 6.

Figure 5.

{kind=link}

Figure 6.

Data: Author's Estimates

Market generated data

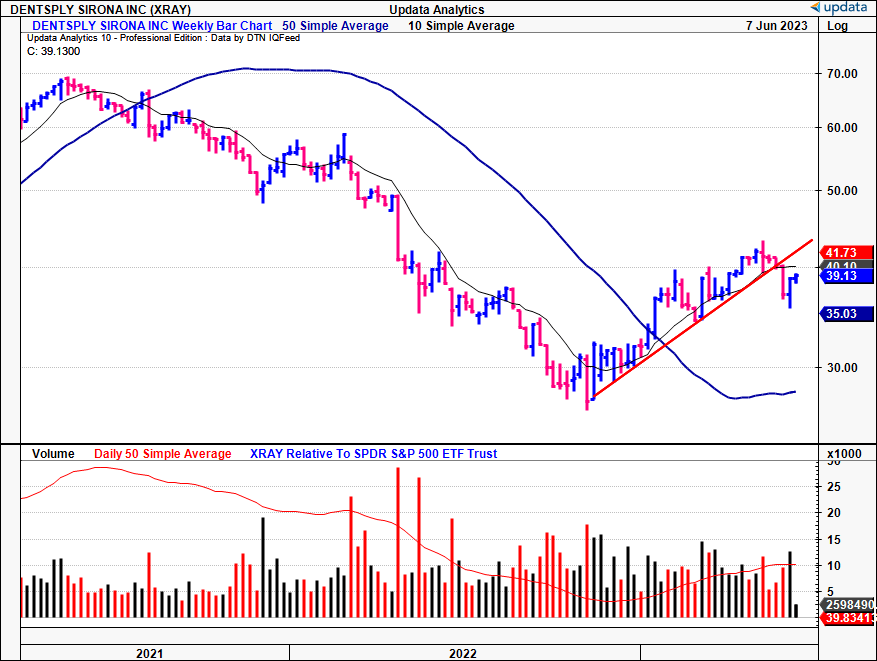

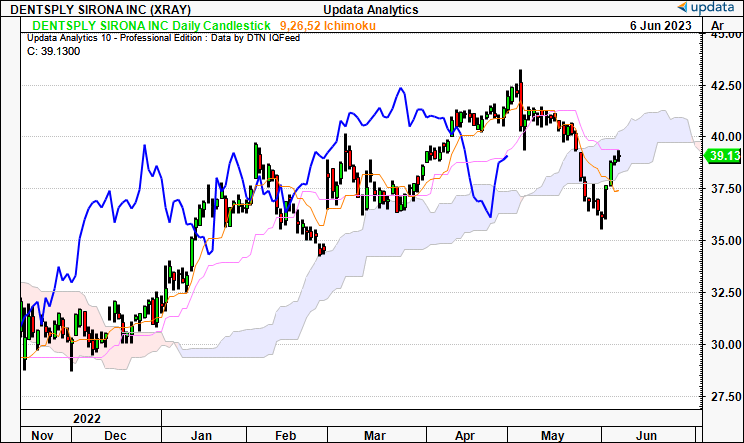

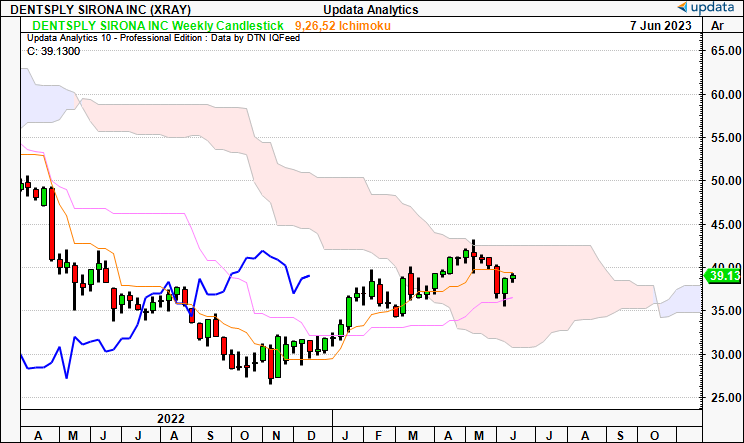

Additional technical information is required in order to decipher the current state of the trend. Looking at the daily and weekly cloud charts below, you can see that XRAY has yet to break above the cloud into bullish territory. The daily chart, looking to the coming weeks, has the company within the cloud, and it must break $42 by the end of June in order to attract demand in my view.

Meanwhile, the weekly chart suggests were are still in the neutral zone, with the lagging line still in bearish territory. It would need to break $42-$43 by August in order to be bullish on this time frame in my opinion. Collectively, these two trend indicators support a neutral view.

Figure 7.

{kind=link}

Figure 8.

{kind=link}

Consequently, we have downside targets to $31 on the point and figure studies listed below. This is telling, as the previous targets were to $43 - critical inflection zones as described above. However, a break lower would activate the $31 target. So it is critical for the bulls to drive XRAY to $42 in order to justify a buy rating in my opinion. Until there's confidence around that happening, it is best to wait on the sidelines in this instance, waiting for the signal to enter.

Figure 9.

Data: Updata

Valuation

Things begin to change when looking at the valuation picture. Investors are paying no more than 20x forward earnings to buy XRAY as I write, that on 17x forward EBIT and 2.2x book value. These aren't cheap multiples at all, and are all above the sector by a small, <2% amount.

Still, you'd expect plenty of growth and/or value to be had if paying these kinds of multiples. For one, the firm's negative 24% trailing ROE doesn't cover the premium to book value, and the major growth in operations is falling on just 1 segment, that being consumables. I'm just not seeing it.

At the current market value of $8.3Bn, and considering a 12% discount rate (long-term market averages), the market values XRAY's future cash flows at $996mm (996/0.12 = $8,300), and expects ~13.5% compounding growth in pre-tax earnings over the coming 5-years (647x(1+0.09)^5/0.12 = $8,295). The question is whether there is any reason to deviate from these expectations. My numbers have the company doing $765mm in FY'23 EBITDA and $896 by FY'28, suggesting just a 3-4% growth rate, and thus behind the market's expectations.

Just to clarify, there is a difference between what the market expects, and what the 'consensus' of analyst expectations is. The market's expectations are reflected directly in the stock price, whereas consensus expectations are shown via the consensus price targets posted by sell-side analysts. This is very important to know, because ''[t]he one job of an equity investor is to take advantage of gaps between expectations and fundamentals" (Mauboussin & Callahan 2020) . Further reading on expectations-based security analysis can be found here . In that vein, I believe the market may have correctly discounted XRAY at its current market cap, and there to be no gap between expectations and fundamentals.

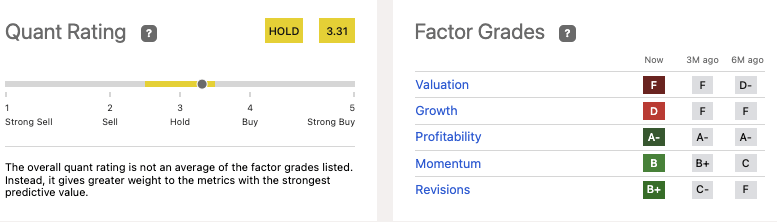

This is supported by findings in the Seeking Alpha quant system, rating XRAY low on factors of valuation and growth, consistent with my own findings. That quant data supports my internal findings and adds a layer of confidence around the estimates, plus, findings obtained from the quant system are well-supported empirically. Hence, this rounds out my reiterated hold thesis.

Figure 10.

{kind=link}

In short

There's not too much left to say on XRAY other than there's a lack of identifiable near-term catalysts, that its financials are mixed, with a push towards consumables, and that valuations are unsupportive at the current multiples. Collectively, these points have dampened sentiment in terms of market price in my view.

As such, I am reiterating XRAY as a hold on fundamental, sentiment, and valuation grounds. Moving forward, I would recommend watch the firming's consumables segment closely, to observe further growth percentages, and also take note of the price charts to observe a change in trend. Net-net, I a reiterate hold.

For further details see:

Dentsply Sirona: Consumables Growing, Still Too Pricey