KMPR - Depressed Valuation And Strong Guidance Enable Growth For Kemper Corporation

2023-11-13 15:22:37 ET

Summary

- Kemper's presence in high-volume markets is driving profit restoration.

- Wall Street consensus on Kemper's valuation and financial performance is positive.

- There are potential risks and challenges that Kemper may face in the future.

Kemper ( KMPR ) is a Chicago, Illinois-based multiline, P&C, auto, and life insurance provider to individuals, families, and businesses across the US. The company maintains a large focus on a volume-based approach, targeting lower to middle-income Americans in underserved, often urban or Latino markets.

{kind=link}

Throu gh these actions, Kemper has seen a Q3'23 revenue of $1.20bn, a 13.38% YoY decline, alongside a net income of -$146.30mn- a 91.99% decline- and a free cash flow of -$52.30mn, a 37.37% increase driven by increased investing cash flows, largely due to rising treasury yields.

Introduction

Although, as aforementioned, Kemper does engage in a diverse range of insurance services such as P&C, the company principally maintains a dual focus on mass-market insurance policies surrounding Auto Insurance and Life Insurance products. Kemper's currently poor financial outcomes are derivative of this dynamic, with other major auto insurers such as Allstate ( ALL ) also seeing drawdowns.

More broadly, though, Kemper's modest income and underserved market approach enable a larger TAM, reduce competitive pressures, and enable long-run growth capabilities as these markets mature and incomes grow.

{kind=link}

Due to these strategic factors, Kemper's strong asset positioning, and a steep undervaluation- but still fundamental risk at play- I rate Kemper a 'buy'.

Valuation & Financials

Trailing Year Performance

In the TTM period, Kemper's stock- down 28.61%- has experienced poorer price action to both TradingView's Insurance Index- up 5.06%- as well as the broader market, as represented by the S&P 500 ( SPY )- up 11.63% in the same period.

{kind=link}

I believe this reflects Kemper's overall financial performance decline, missing targets or seeing real declines in revenue and profit in the trailing few quarters, as well as the general underperformance of auto insurance companies.

Despite this, I believe the market is underpricing the potential for Kemper's operational and financial reversion, driven by a stabilizing monetary environment, with interest rates seeming to reach their ceiling and inflation slowing.

Comparable Companies

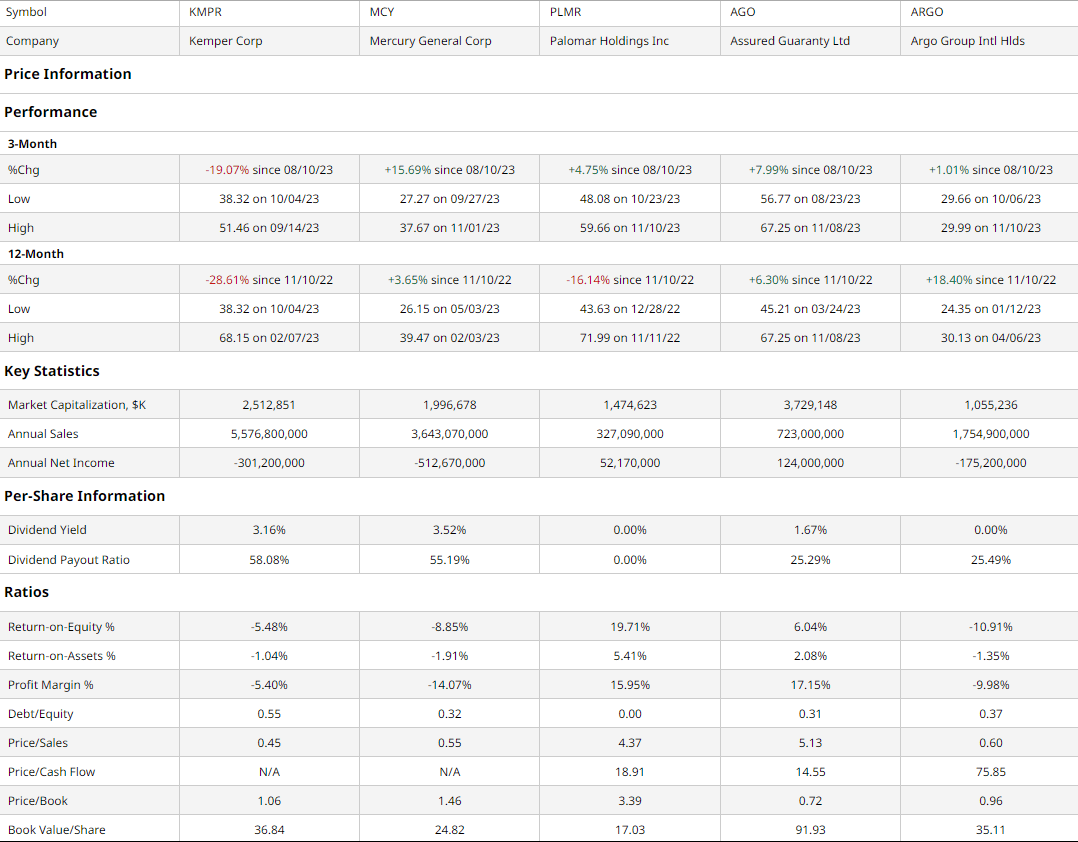

Since most direct competitors to Kemper are larger, multi-sided insurance companies, it makes more contextual sense to compare Kemper to more similarly-sized insurers. This group, chosen from Seeking Alpha's 'Peers' tab on Kemper's stock page, includes the following: the Los Angeles, California-based multi-line insurer, Mercury General Corporation ( MCY ), the La Jolla, California-based residential and commercial specialty insurer, Palomar Holdings ( PLMR ), the Hamilton, Bermuda-based muni bond, infrastructure, and structured financing insurer, Assured Guaranty ( AGO ), and Bermuda-based specialty insurance underwriter, the Argo Group ( ARGO ).

{kind=link}

As demonstrated above, in both the past quarter and the TTM period, Kemper has underperformed relative to the peer group. This likely relates both to Kemper's outsized auto-insurance focus in addition to the greater elasticity of demand for its products since Kemper's target market is of more modest incomes. Despite this, assessing Kemper from a multiples-based value perspective, the company remains fundamentally undervalued.

For instance, the company maintains the lowest P/S in the peer group, emphasizing Kemper's scale-driven focus. Moreover, the company maintains the second-highest book value per share, demonstrating underlying balance sheet strength and security for investors.

Furthermore, investors can expect not only price appreciation due to the company's undervaluation, but also strong income prospects, with a solid 3.16% dividend.

Valuation

According to my discounted cash flow model, at its base case, the net present value of Kemper should be $46.31, meaning, at its current price of $39.17, the company is undervalued by 15%.

My model, calculated over 5 years without perpetual growth built-in, assumes a discount rate of 9%, integrating Kemper's high- relative to other insurers- equity risk and the company's healthy balance sheet. Additionally, remaining conservative, I assume a forward annual revenue growth rate of 7%, lower than the trailing 5Y average revenue growth rate of 16.65%, which was heavily skewed by Kemper's M&A activities during the more relaxed monetary era.

{kind=link}

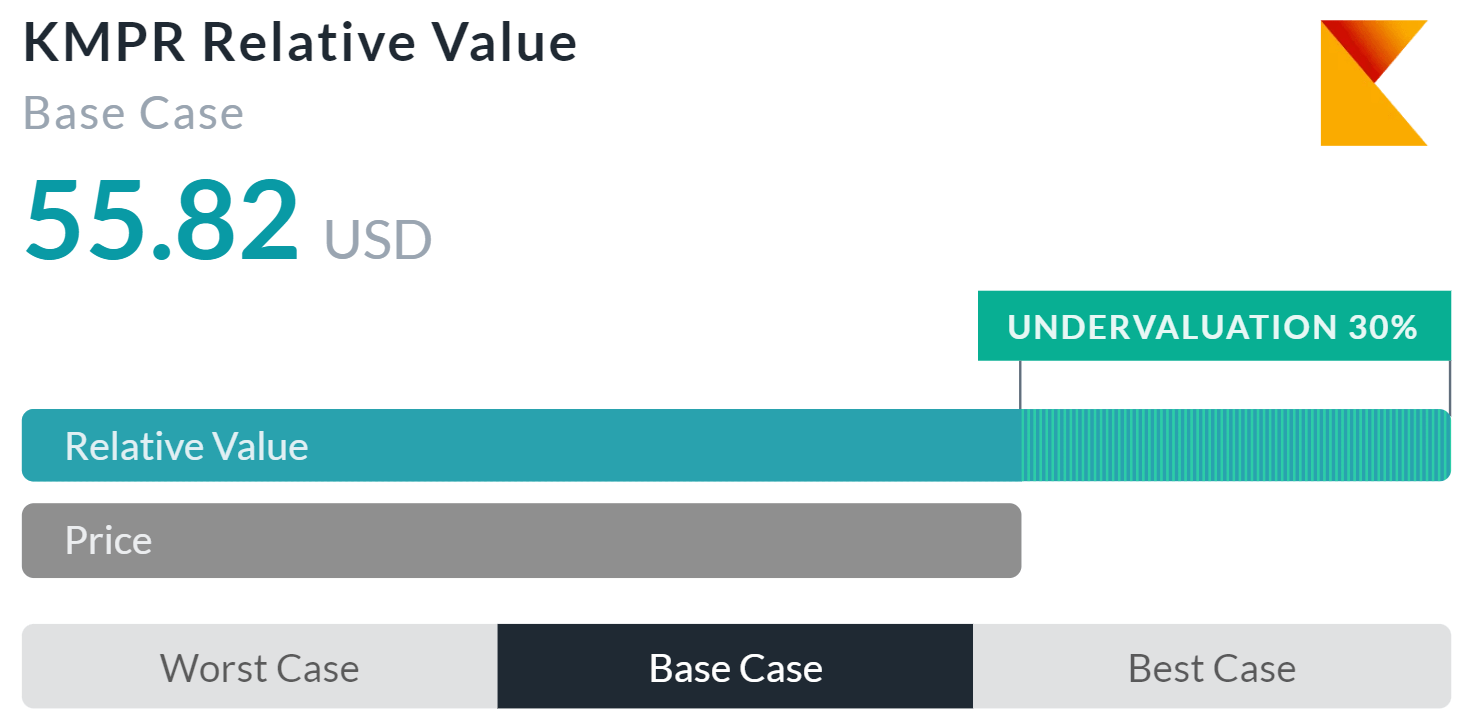

Alpha Spread's multiples-based relative valuation model more than corroborates my thesis on undervaluation, estimating a base case relative value of $55.82, a 30% undervaluation.

Thus, taking an average of my NPV and Alpha Spread's relative value, the fair value for Kemper should be $51.07, or a ~22.5% undervaluation.

While Kemper's Profit Restoration Strategy is Strong, Its Greatest Strength is Excellent Balance Sheet Positioning

As illustrated below, Kemper maintains excellent risk-based capital ratios- which, in the insurance industry, measure the risk from the declining value of insurance subsidiaries and other off-balance sheet assets. Moreover, the company, while seeing growth in debt-to-capital, maintains a relatively conservative debt level, with high overall liquidity across the board. This enables Kemper's eminent inorganic growth strategy of expanding its insurance base through acquisitions and the like.

{kind=link}

In addition to general balance sheet capabilities, Kemper maintains a high-quality, diversified portfolio, with baked-in stability and income facilities, maintaining a 4.6% annualized book yield and experiencing higher yields in real-time. As such, Kemper has seen significant net investment income growth, from $98mn in Q3'22 to $107mn in Q3'23. Additionally, Kemper effectively spreads risks, from government bonds to corporate bonds to muni bonds, most of which at high credit grades mixed with a smaller amount of lower grade bonds to enhance yields.

{kind=link}

Wall Street Consensus

Analysts generally echo my positive view on Kemper, estimating an average 1Y price target of $60.25, a 53.66% price increase.

{kind=link}

Even at the lowest projected price target of $47.00, analysts expect a price incline of 19.87%, with net returns enhanced by the firm's dividend.

I believe that Wall Street understands that the market has underpriced Kemper and overreacted to temporary headwinds related to rates and inflation.

Risks & Challenges

Persistent Rate Hikes or Inflation May Drive Down Policy Demand

A major factor in Kemper's poor price action and financial results in the past year has been declines in the demand for new policies and higher margin policy underwriting services. As such, in either or both a persistent inflationary or recessionary environment, wherein consumer spending is squeezed, Kemper may experience a continued decline in both margins and scale until a trough or reversion in the macroeconomic situation.

Increased Competitive Intensity May Compress Profits

As the industry continues to face headwinds across its portfolios and primary demand points, many larger insurers are likely to leverage their capital reserves for expansion across insurance products and target markets, rather than rely on organic market growth. As such, Kemper may face competition from better-financed rivals, which may lead to a level of price or product competition which would either increase costs or reduce profitability for Kemper.

Conclusion

Looking forward, I believe that Kemper's long-run operational opportunities, combined with its present strength in portfolio management and its discounted price present a buy opportunity for investors.

For further details see:

Depressed Valuation And Strong Guidance Enable Growth For Kemper Corporation