DSG:CC - Descartes Systems: An Attractive Risk-Reward Opportunity

Summary

- Descartes Systems is a leading logistic management software company operating in a fragmented industry.

- The company is set to benefit from strong tailwinds, thriving in a tough macro environment while capitalizing on its strong fundamentals.

- I believe the stock's valuation remains reasonable compared to industry peers, leaving important upside potential and an attractive risk-reward opportunity.

Investment Thesis

In an environment where the market is strongly penalizing growth, attractive opportunities appear. Despite a tough macroeconomic context characterized by higher interest rates and inflation, Descartes Systems ( DSGX ) appears to stand out. Indeed, the stock held up quite well on a year-to-date basis, with only a -15.55% correction vs. -18.5% for the SP 500 and -33% for the Nasdaq 100. Being very profitable and having an impressive track record, whether in terms of execution, financial resources management and M&A, I expect Descartes to deliver a strong performance in the upcoming year. In my view, a context of strong inflation with rising rates will give plenty of opportunities to this Canadian leader, be it in terms of organic or inorganic growth. I initiate coverage on DSGX with a Buy rating and a target price of $84 representing a 20% potential upside.

Company Presentation

Descartes Systems is a leading logistic management software company. Based and created in Ontario, Canada, in 1981, the firm provides federated network and inter-enterprise software for the execution of supply-chain management through a software-as-a-service (SaaS) platform. These products are especially useful for delivery-intensive companies. By combining innovative technology, powerful trade intelligence and its network, Descartes Systems delivers a complete offering of cloud-based logistics and supply chain management solutions focused on productivity, performance, and security. By positioning itself as a pure player on SAAS solutions for logistics-intensive business, the group managed to attract 24,000 + customers worldwide spread over 160+ countries, with some major names belonging to various industries such as American Airlines ( AAL ), FedEx ( FDX ), DHL (DPW), Home Depot ( HD ), and Coca-Cola ( KO ).

{kind=link}

Industry-leading Customers (Descartes)

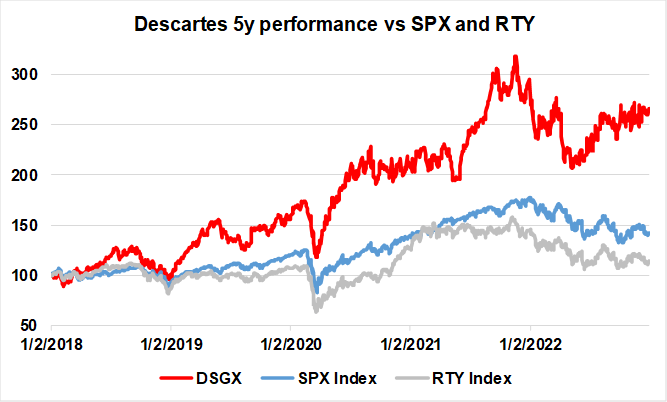

Since 2018 Descartes Systems has been a strong compounder generating a 166.01% return w hile the Nasdaq 100-Index ( NDX ) returned 42.78% and the Russell 2000 ( RTY ) 13.95%.

{kind=link}

Bloomberg

Financials and Valuation

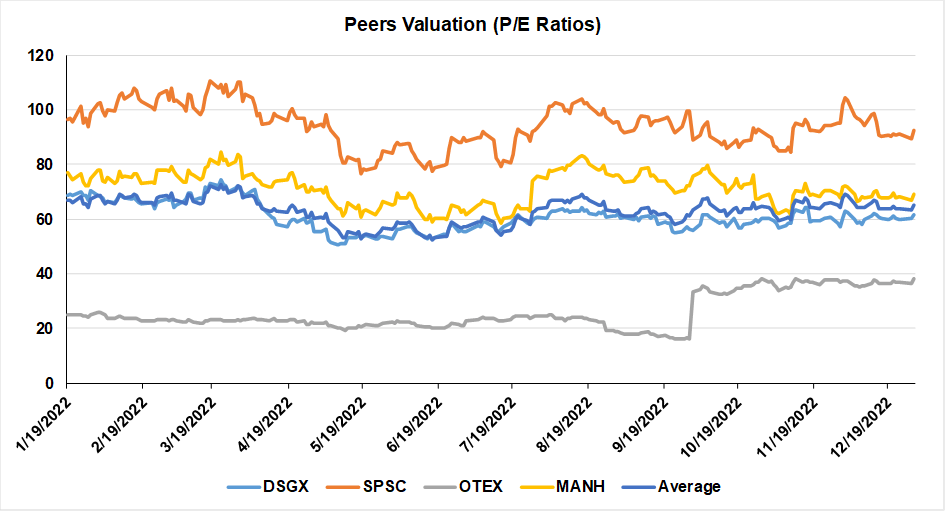

Despite a complicated year for markets and especially for growth stocks, Descartes System achieved a P/E ratio of 61.5. This might look expensive on a standalone basis. However, it is still cheaper than many of the company's peers. This valuation gap is not justified in my view, and leads me to believe that there is an opportunity to grab.

{kind=link}

Bloomberg

In a very fragmented industry, Descartes Systems has to face many competitors. I selected several major ones having a similar size in terms of market capitalization. The peer group comprises Open Text Corp. ( OTEX ), SPS Commerce Inc. ( SPSC ), and Manhattan Associates Inc. ( MANH ).

When looking at the financial strength of Descartes, it appears that the company has a very low debt level, especially amongst its peers. Indeed, current assets are covering more than twice the short-term liabilities (2 nd in the ranking), while debt represents only 96% of the firm’s assets (1 st in the ranking). The most impressive is the Debt/Equity ratio which stands only at 1.1, while the peer average is at 32.08 and the median at 8.10. Such low levels of debt make Descartes a very attractive play compared to its peers in an environment of rising interest rates. As debt is inherently risky, I tend to favor businesses with lower D/E ratios. It represents a lower risk of loan default and still gives room for Descartes to borrow money if needed. I expect Descartes to keep such low levels of debt as it has an important amount of cash (cash ratio =1.6).

{kind=link}

Created by author using data from Bloomberg

In an industry where the valuation might seem expensive, especially in an environment of rising rates, we have to focus on the most profitable company. Here again, Descartes stands as the leader among its peer group having very strong bottom- and top-line margins. The focus on profitability makes it a very attractive play. Management has always considered profitability and FCF generation as priorities (87% TTM EBITDA to FCF conversion). Even in a context where the transaction volume may slow down, I expect cash flows to remain resilient. The CEO of Descartes Mr. Ryan recently highlighted that during the 2008 Recession, the group was able to increase adj. EBITDA by 15% per year which is reassuring in the case of a “hard landing” scenario. I expect the management team to reach its goals of keeping margins at the current level for the next year.

For all these reasons, my most conservative scenario is a 10% upside for Descartes Systems in 2023. That is based on the idea that DSGX's 10% discount compared to its peers' P/E average is unjustified.

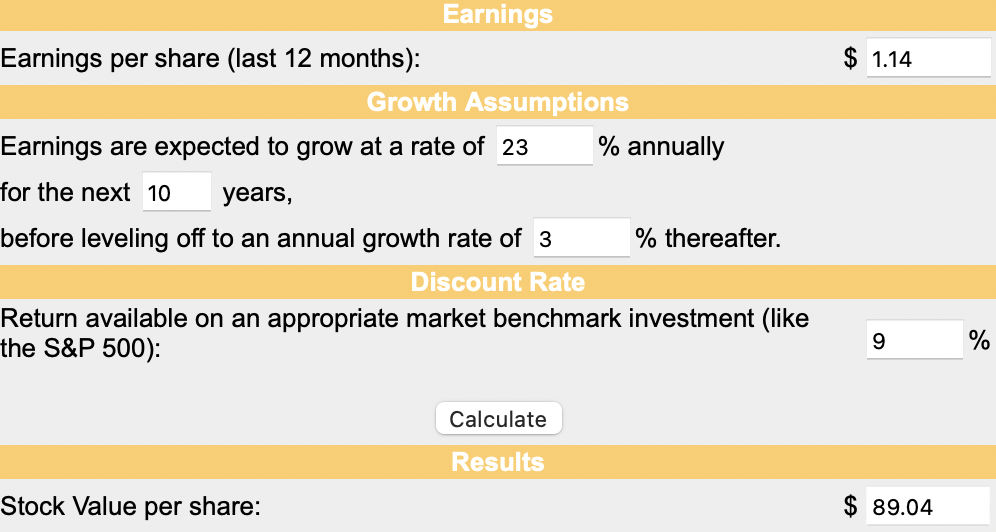

During the last 10 years, the company managed to increase its EPS by 25% on average. I expect Descartes Systems to deliver strong growth during the next 10 years. However, this growth should slow down a bit due to the deceleration of the so-called "COVID Effect". Thus, I assumed a 23% growth rate.

Starting from a trailing 12 month EPS of $1.14, I choose a 3% perpetual growth rate based on the average US GDP Growth rate during the last 10 years. This has been combined with a 9% discount rate being our firm's WACC. With such assumptions, we reach a target price of $89.04 representing a 27% upside potential.

{kind=link}

Moneychimp

After aggregating these two assumptions and computing the average of these, I expect a 20% upside potential for Descartes Systems for the year 2023, representing a $84 target price.

Catalysts

Aside from its strong financials, Descartes is also benefiting from major tailwinds. Since the COVID crisis, many economic actors have been impacted by logistic/supply chain issues which have endangered their activity. This situation has increased the logistics/supply chain solutions needs of these companies.

According to Edward Ryan , Descartes CEO, "The COVID pandemic forced every business to change its supply and delivery practice. Whether it be where they got their supplies, what companies they work with, or how they would remotely get visibility to their shipments and deliveries. That change in complexity drove demand for our products and services."

Thus, this “COVID Effect” combined with an increasing demand for digitalized and automated solutions will continue to relatively drive the demand for Descartes' solutions. According to Mr. Ryan, this acceleration is just the beginning of a “long-term trend”.

Furthermore, I believe that the current context of strong inflation will benefit Descartes as potential customers might be seeking solutions allowing them to reduce their cost structure. Thus, by improving Logistics, Supply Chain Productivity, Performance, and Security, Descartes Systems is clearly in a great position to take advantage of this macro environment.

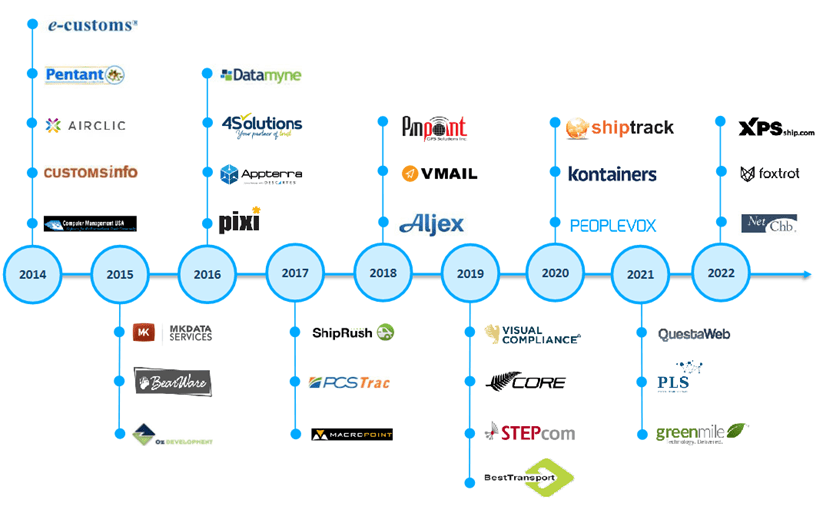

Since 2014, Descartes Systems made 31 acquisitions for an amount of $1.04 billion. The firm focuses on M&A targets that are profitable, growing rapidly, and having recurring revenues. The company targets small competitors while focusing on complementary technologies favoring industry consolidations. In this large and fragmented market, Descartes Systems has many potential targets to synergize with. The Canadian firm made the wise decision to accumulate an important amount of cash in its balance sheet. This gives a counter-cyclical opportunity to acquire competitors of bigger size, in an environment where valuations have particularly decreased.

{kind=link}

M&A is a Core Competency for Descartes (Descartes)

Risks

I see three potential risks that might affect Descartes Systems. The first one is linked to trade volume which accounts for 30% of Descartes' revenues. If we are expecting a hard landing scenario, then Descartes might be strongly impacted. Secondly, Descartes has 50% of its revenues coming from Europe. As Europe is one of the most impacted zones by the Ukraine-Russia war, it could weigh on the company's profitability with slower growth and forex risks. Finally, despite an impressive M&A track record, we should not exclude the risk of Descartes making a bad acquisition whether in terms of price or synergy.

Conclusion

The quality of Descartes Systems is not in doubt in my view. Indeed, it combines several key factors that every growth investor should be looking at in these tough times to find attractive long-term, risk-reward opportunities. With its high-recurring revenue profile, its profitable growth and solid free cash flow generation, its proven "Total Growth" model supported by a disciplined acquisition strategy and a healthy financial position, Descartes Systems hold all the cards to outperform in 2023. I expect a 20% upside for 2023 and initiate on DSGX with a Buy rating with a target price of $84.

For further details see:

Descartes Systems: An Attractive Risk-Reward Opportunity