DSG:CC - Descartes Systems Group: A Top-Tier Compounder

2023-07-20 11:56:27 ET

Summary

- Descartes Systems Group, a Canadian supply chain and logistics software provider, has seen significant growth through its strategy of acquiring smaller software companies.

- Using a SaaS-like business model, Descartes has been able to compound cash flow per share from $0.41 in 2011 to $2.21 in 2023, for a 15+% CAGR.

- Despite its premium valuation, Descartes' strong cash flow, high growth rate, and lower valuation compared to its peers make it a Buy.

History & Background

Descartes Systems Group ( DSGX ) was founded in 1981 and is based in Ontario, Canada. The company is best known as a provider of supply chain & logistics software that links retailers and large buyers of good with air freight, ocean freight, railroad, and trucking companies through its Global Logistics Network (GLN). Their most recent 10K describes their business best:

Our solutions are predominantly cloud-based and are focused on improving the productivity, performance and security of logistics-intensive businesses. Customers use our modular, software-as-a-service (“SaaS”) and data solutions to route, schedule, track and measure delivery resources; plan, allocate and execute shipments; rate, audit and pay transportation invoices; access and analyze global trade data; research and perform trade tariff and duty calculations; file customs and security documents for imports and exports; and complete numerous other logistics processes by participating in a large, collaborative multi-modal logistics community.

The company went public in 1998 during the heyday of the dotcom bubble and primarily sold its software through one-time deals where a user buys it and has perpetual access to the software. Once the dotcom bubble burst, sales dried up and the company teetered on bankruptcy until 2004 when CEO Arthur Mesher came in and began turning the company around. Instead of selling one-time licenses, they started selling recurring subscriptions utilizing a SaaS-like business model. This business model endures to this day with their recurring services revenue comprising 90% of total revenue.

Current Business Model

Utilizing the SaaS-like business model, Descartes is able to obtain strong cash flow and uses that cash flow to buy up smaller software companies that it adds to its GLN to augment its offerings. It listens to its customers' needs and can buy companies that fulfill those needs.

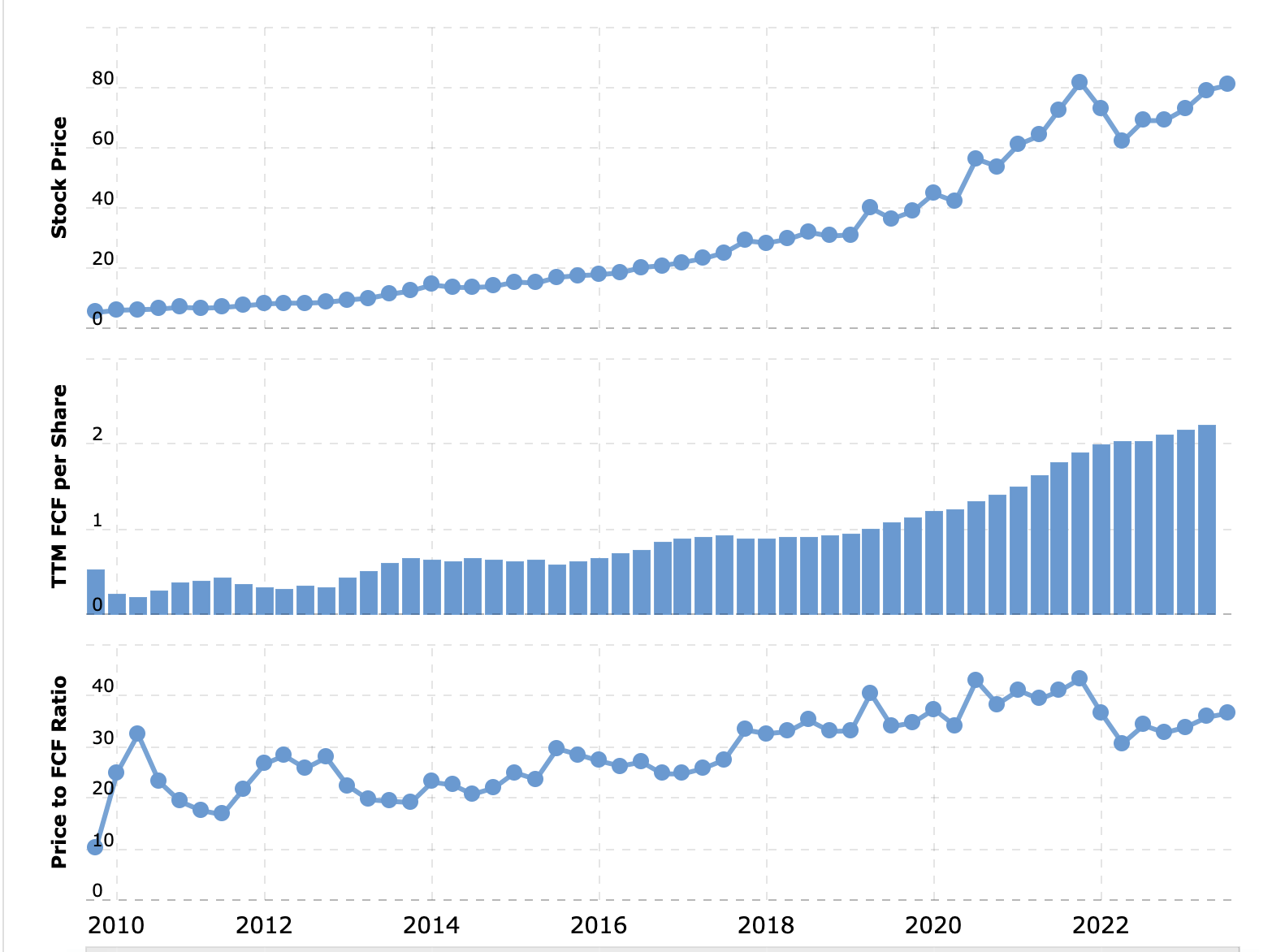

By buying up smaller companies at about a rate of 3-4 per year, Descartes has successfully grown its business and compounded FCF per share from $0.41 in 2011 to $2.21 in 2023 or about a 15% CAGR.

Descartes FCF Growth (Macrotrends)

{kind=link}

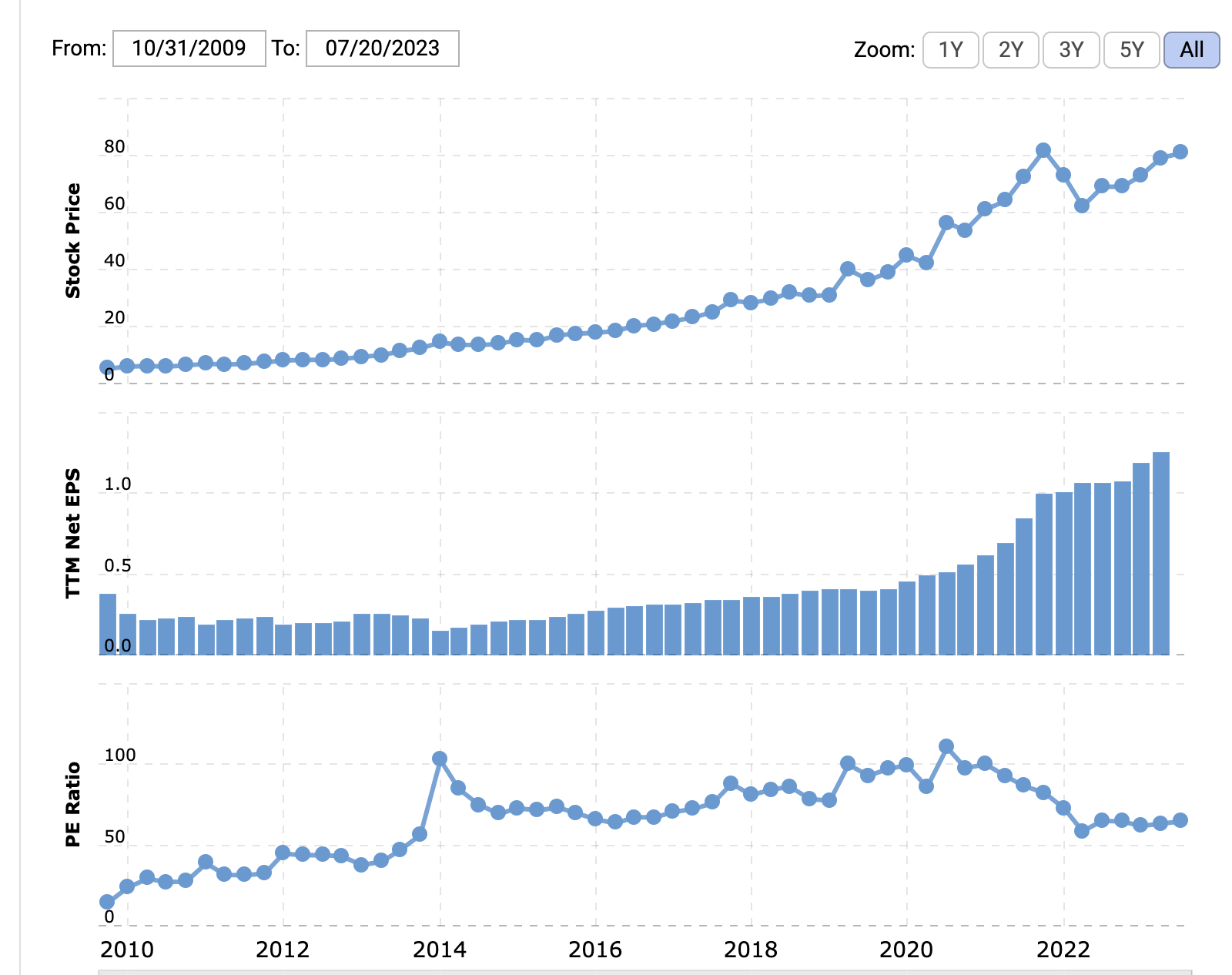

Earnings have also grown massively from $0.22 per share in 2011 to $1.25 per share in 2023 for a CAGR of 15.6%

Descartes EPS Growth (Macrotrends)

{kind=link}

In fact, they have acquired over 53 companies since 2006. Growth by acquisition can be a red flag due to the risk of overpaying and the difficulties with integrating companies. Yet, despite being so acquisitive, Descartes has been able to create shareholder value as evidenced by its superb cash flow and earnings growth. Additionally, Descartes mostly uses a combo of cash and stock to buy companies without having to utilize any debt. Its balance sheet is pristine with $182 million in cash and 0 long-term debt. This means Descartes has plenty of dry powder to go after more companies for its GLN.

Once Descartes buys a company, the capex requirements are quite low, which is why Descartes can convert most of its operating cash flow and adjusted EBITDA into free cash flow, while amortizing the cost of previous acquisitions.

The current management at Descartes is experienced with their CEO Edward Ryan being part of the company in various roles since 2000. He has a long-term oriented vision and has consistently said that their goal is to grow steadily, profitably, and within their means. In their most recent earnings call he said:

We're a "slow and steady wins the race" kind of company. I think we proceed cautiously all the time. If we over perform, that's great news. But I don't know that we see what's going to happen out 5, 10 years. And so we think, hey, this is the rate that we think this market may grow at. Maybe we're doing a little better than that right now. But we're going to continue to run our company like that. So if something bad happened in the future, we're not dramatically impacted by it. We've seen a lot of people roll by us over the years, screaming from behind them, "We're going to the moon and we'll see you later." And then in the next couple of years, they implode and we quietly come behind them and pick up all the pieces. And the reason those things happen is because they overinvest in sales and marketing as they start making promises they're going to grow faster than they can in the long run. And when something goes bad, they implode. Everyone gets fired. The customers get forgotten. And they probably get sold to somebody else. And that's a disaster that we don't want to be a part of.

Such management helps shareholders sleep well at night, knowing that the company is focused on the long-term.

It would be remiss of me not to mention the similarities that Descartes possesses compared to another Canadian company that is also a serial acquirer of software: Constellation Software ( CNSWF ). In fact, Descartes and Constellation have similar business models, but Descartes is focused on a specific niche where it has built its own network of trusted customers.

Constellation has created tremendous value for shareholders over the years with a TSR of over 15,000% since 2006 providing evidence that the business model is a viable one. Both companies are able to generate free cash flow in excess of their earnings through depreciating & amortizing their acquisitions, which acts as a way to reduce taxes and helps compound cash flow.

Valuation & Peer Comparison

Descartes is expensive. It is currently trading at about 64x P/E, but when looking at cash flow it is cheaper at about 35x FCF. Still quite expensive. However, the recurring nature of its revenue and its ability to grow that revenue both organically and through acquisition ( It had 9% organic growth last quarter and 17% total growth ) are worth the premium to me.

Historically, Descartes has traded more expensively than it is currently priced. It traded with a P/E of over 70x almost continuously from 2014 to 2021 and a P/FCF of over 40x between 2019 to 2021.

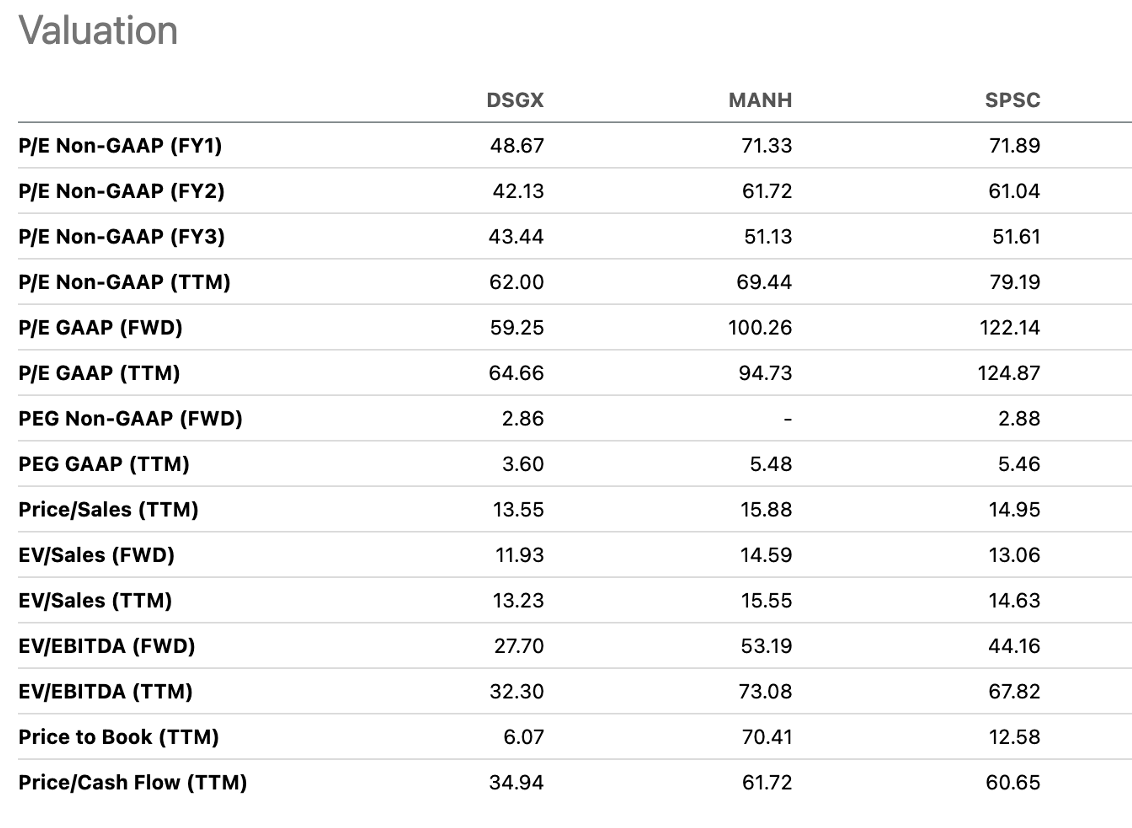

Descartes has several peers & competitors within the supply chain software industry with the closest peers being Manhattan Associates ( MANH ) and SPS Commerce ( SPSC ).

Peer Comparison Valuation (Seeking Alpha)

{kind=link}

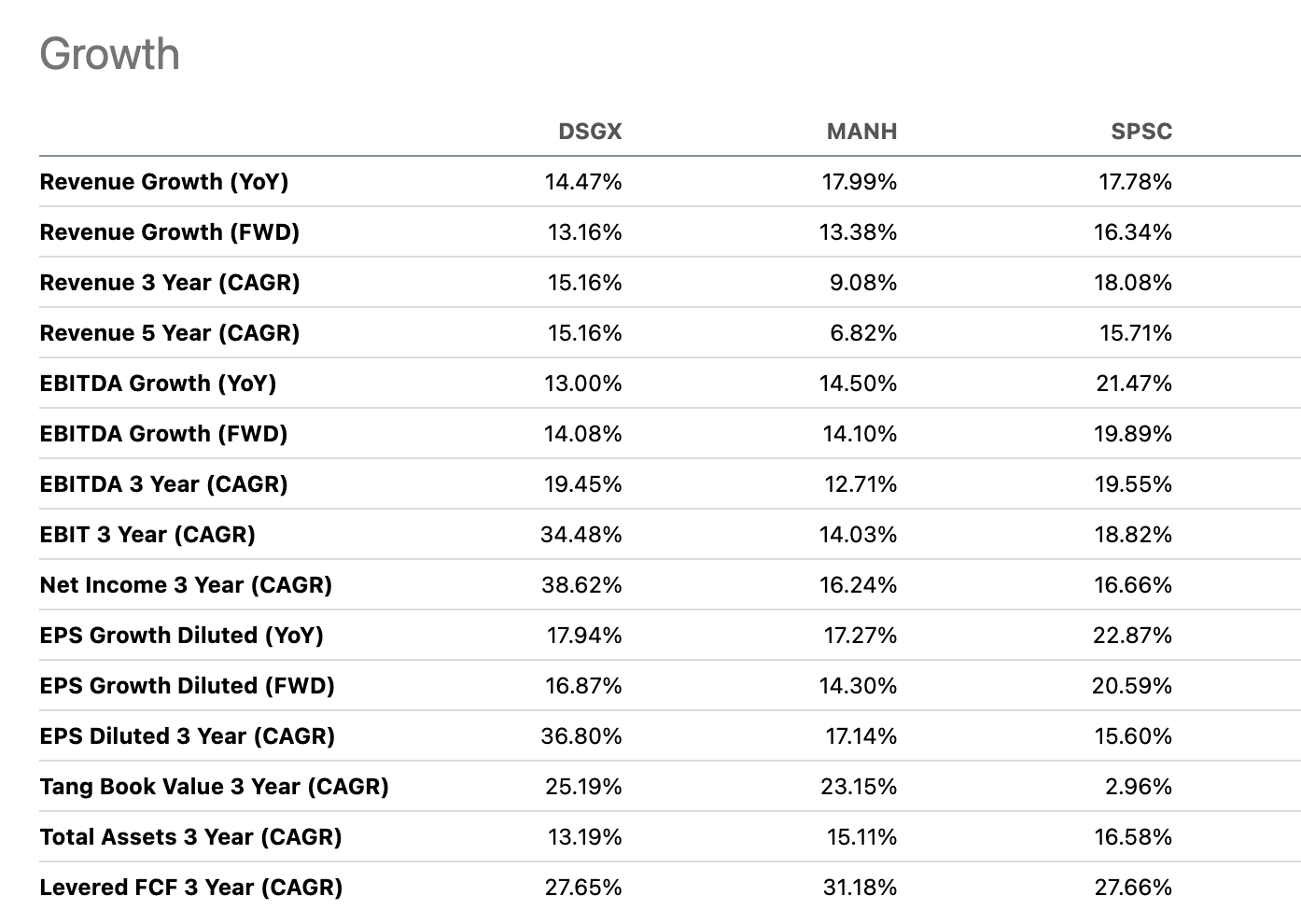

Descartes is significantly cheaper than both of its peers on earnings and cash flow metrics. This may be due to its slower growth in recent years as evidenced by its revenue growth which has lagged its peers over the past year. However, over a 5 year period, Descartes has grown almost as fast as SPSC, and yet it trades at half the valuation. If Descartes can return to grow faster than its peers, there is some room for multiple expansion as well.

Peer Comparison Growth (Seeking Alpha)

{kind=link}

While all 3 of these companies have outstanding balance sheets, profitability metrics, and growth profiles, I still prefer Descartes due to its lower valuation.

Risks

There are several key risks to my thesis. While Descartes has been compounding shareholder value for the past decade, past returns are no indication of future performance and if the compounding engine stops because of a lack of possible acquisition targets, competitive threats, or a slowdown in global supply chain growth, the stock price may be beaten down due to a combo of slower growth and a decreasing multiple.

Descartes has a premium valuation, which means that valuation compression is a real risk. While the company could grow, shareholders may not benefit as the multiple compresses. This happened to many software companies after the dotcom bubble, most notably to Microsoft ( MSFT ), which was stagnant for a decade despite improving fundamentals.

There is key man risk as current CEO Edward Ryan has been part of Descartes for over 20 years and his departure could have a negative impact on Descartes’ business.

Growth by acquisition is fraught with risks such as overpaying and risks of poor integration of acquired companies. A series of ill-timed or highly-valued acquisitions could negatively impact Descartes’ business.

Conclusion

Descartes Systems Group is a great business trading at a premium price. Its history of compounding cash flow and generating shareholder value is superb. It has a pristine balance sheet, is still growing at a high rate, and is cheaper than its peers. I believe the history of value creation can continue for the foreseeable future and rate the company a buy.

For further details see:

Descartes Systems Group: A Top-Tier Compounder