DSGX - Descartes Systems: Valuation Becomes A Question Mark (Rating Downgrade)

2023-12-12 18:01:20 ET

Summary

- The Descartes Systems Group Inc. reported its Q3 earnings, which were highlighted by solid growth, although EPS missed the consensus estimate.

- The company benefits from overall solid fundamentals as a category leader within logistics and supply chain management software.

- We like Descartes Systems stock, but sense a pricey valuation may limit the upside from the current level.

The Descartes Systems Group Inc. (DSGX) reported its latest quarterly results , highlighted by solid growth for its supply-chain management software platform. The company is capturing an ongoing digitization in the logistics sector globally, with customers from shippers, carriers, and transportation service providers investing in technology to enhance efficiency.

We covered DSGX with an article last year , citing several high-level themes supporting a positive long-term outlook despite the macro concerns at the time. Indeed, the backdrop has been a solid rally, with shares up nearly 25% this year and currently trading at their highest level going back to the late 2021 pandemic era high.

Our update today reaffirms a positive long-term view on The Descartes Systems Group Inc., but dials back the bullishness by noting the stock's pricey valuation trading at 50x forward earnings and 11x sales. The company is fine and benefits from overall solid fundamentals, but we see limited upside in shares from the current level.

DSGX Earnings Recap

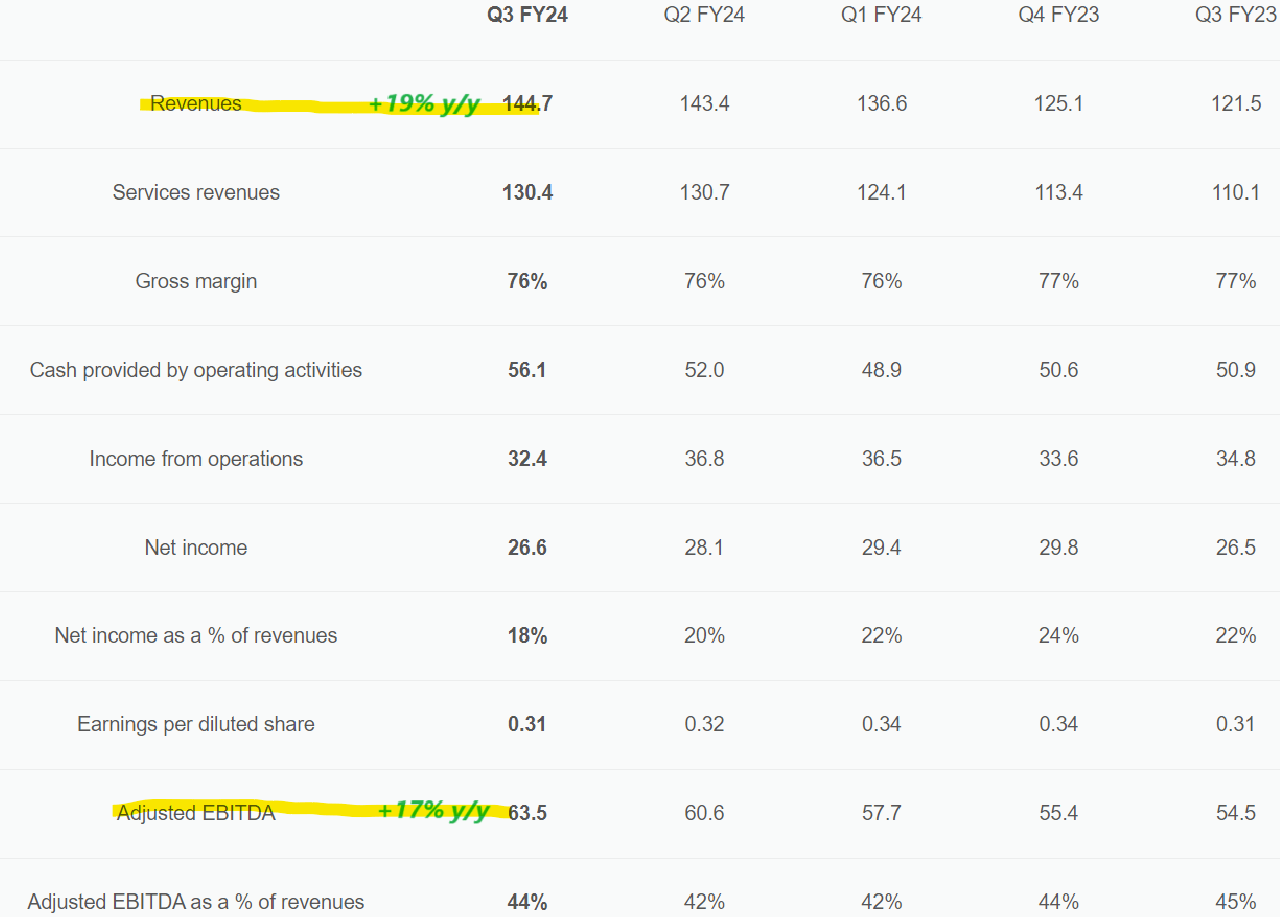

DSGX fiscal 2024 Q3 GAAP EPS of $0.31 came in below the consensus estimate of $0.34, and flat from the period last year. That said, the context here considers some contingent charges related to the acquisition of "GroundCloud" last year. The more normalized earnings measure with the adjusted EBITDA presented a stronger underlying momentum, reaching $63.5 million and up 17% y/y.

At the top line, revenue climbed by 19% to $144.7 million, a company record with organic growth of around 8% in addition to acquisition impact. At the same time, a shifting sales mix has added to some margin variance. The gross margin of 76% was down from 77% last year.

Similarly, the adjusted EBITDA margin at 44% ticked lower from 45% in Q3 fiscal 2023. Internal restructuring efforts and recently implemented cost-saving initiatives are expected to have a greater impact on supporting margins going forward.

{kind=link}

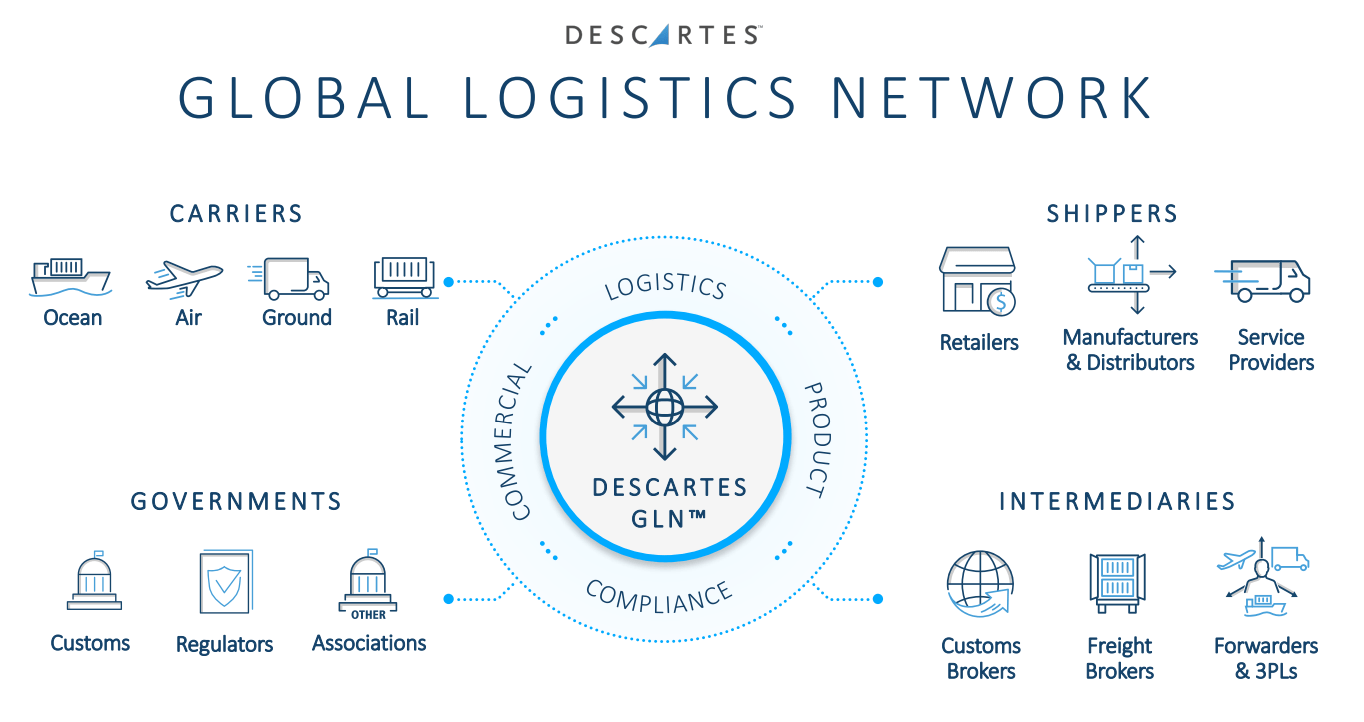

Operationally, the strong points of the business have been in products related to real-time visibility, global trade intelligence, routing, and scheduling solutions. The wide range of solutions covers everything from back-end enterprise systems, customs & regulatory compliance, trade intelligence, transportation management, and real-time telematics.

While Descartes is not issuing formal financial guidance, comments during the earnings conference call by management projected optimism for current growth trends to continue.

The company ended the quarter with $280 million in cash against effectively zero financial debt. We view the balance sheet as a strong point in the company's zero financial debt .

{kind=link}

What's Next For DSGX?

What we like about Descartes Systems is its position at the intersection of technology and industrials. The company counts on major corporations across various industries and end markets, as customers and those relationships support a runway for further growth as their business expands.

There's a clear "cyclical" exposure to the company in terms of capturing global macro trends as a demand driver, and that's good news considering the current market outlook. Heading into 2024, a backdrop of easing inflationary pressures and stabilizing interest rates is expected to support global economic activity.

Notably, the company notes that U.S.-bound import traffic ticked higher in September with a 0.7% increase in container volumes at the top 10 U.S. ports compared to August, suggesting a good read on global trade activity into the year end.

One area of concern is related to a weaker read on China, which has presented disappointing economic data in recent months, as a signal towards emerging markets. Overall, the big picture is that there are several moving parts, but the long-term trends are positive.

{kind=link}

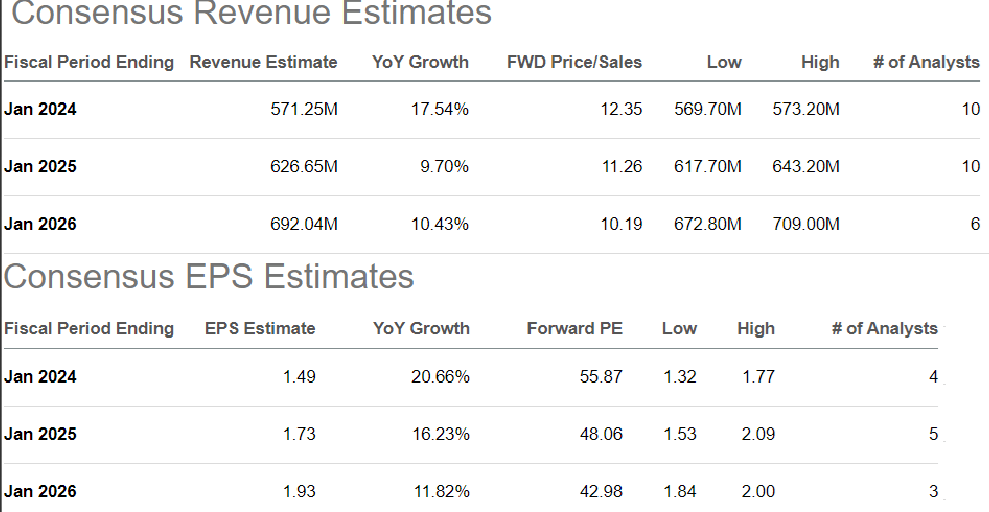

According to consensus estimates, DSGX is forecast to see revenue growth of around 10% over the next two years, while EPS runs a bit higher in the 14% range through fiscal 2026 with some upside to margins.

The bullish case for the stock is that the company will ultimately outperform these estimates. One catalyst for that on the macro front would be precisely a stronger rebound out of China as a tailwind for global trade as well as a weaker U.S. Dollar, supporting strength in international currencies for global clients.

{kind=link}

At the same time, the knock when looking at DSGX is that shares command an otherwise lofty valuation premium, currently trading at around 50x next year's consensus EPS. Recognizing that the company stands in a unique market position as the leader on this side of supply-chain software technology, the question becomes how much more upside it is for multiples to expand from the current level.

The rock-solid balance sheet with zero debt as well as the low variability of sales given the recurring revenue component of the platform makes the underlying cash flow from DSGX high quality. That said, DSGX at 11x fiscal 2025 sales is a pricey proposition.

{kind=link}

Final Thoughts

Overall, The Descartes Systems Group Inc. is a category leader well-positioned to consolidate market share over the long-run. DSGX is a quality stock with a positive outlook.

Considering the big rally this year, the next target becomes the all-time high of around $90, which is likely on the table for 2024. On the other hand, considering the valuation premium, we don't believe that a price target just 7% higher from here makes a compelling buying opportunity. We rate DSGX as a hold representing a neutral view over the next several months.

Monitoring points here include the adjusted EBITDA margin and cash flow trends. The risk of a deteriorating macro environment would open the door for a deeper selloff in shares if it begins to impact earnings estimates.

For further details see:

Descartes Systems: Valuation Becomes A Question Mark (Rating Downgrade)