CLMHF - Desert Lion Capital Q3 2023 Investor Letter

2023-11-08 03:50:00 ET

Summary

- Desert Lion Capital is managed by Rudi van Niekerk who is a South African citizen. Due to a growing interest from US and other international investors, Desert Lion Capital was launched to meet the needs of non-South African investors.

- South African equities are expected to bottom relative to the S&P 500 and the Nasdaq-100 within the next 12 months.

- Foreign selling of South African equities and bonds has accelerated, causing declining valuations and poor performance.

- Despite challenges in South Africa, there are signs of opportunity, such as positive earnings reports and low valuations.

Dear partners and friends,

Regular readers know that I am always measured in my commentary. Not this time. This letter is VERY different. I am sticking my neck out and unequivocally calling it:

South African equities are bottoming relative to the S&P 500 ( SP500 , SPX ) and the Nasdaq-100 ( NDX ).

I am framing this call within a 12-month window. The bottom may have been last week, or it could be next week, or next month, or in 6 months. I cannot be sure about the exact timing, but I am drawing a line in the sand. We are at or near the bottom in relative terms. I am not predicting the short-term direction of the JSE All Share Index. (In the long run, it should be up and to the right). What I am suggesting is the following: for a meaningful period over the next few years, South African equities will outperform the S&P 500 and the Nasdaq-100.

Audacious? Yes. The future is inherently uncertain. The best we can do is to think in terms of probabilities.

In this particular case, I calculate the probability as very high. My level of conviction is also very high. So, in my mind, the probability weighted outcome instructs me that it is rational to be unequivocal.

What is my responsibility as portfolio manager of Desert Lion Capital?

- Manage risk (i.e., protect the downside). In order to finish first, you have to first finish. If I am successful, I don’t impair our LPs’ long-term capital (or my own capital invested in the Fund), and we retain our LPs.

- Generate returns. If I am successful, I make money for our LPs and get rewarded in the form of performance fees, and the Fund gains quality LPs.

- Navigate, communicate, guide. Most of our audience are not intricately familiar with the nuances of investing in the South African equity market. I am your experienced local guide. It is my job to keep my feet on the ground, observe, interpret, and share my conclusions.

Today, in this letter, I am dealing with number 3. Markets ebb and flow. They move in cycles. An amorphous concoction of ever-changing fundamentals interpreted by irrational participants eventually manifesting as mass psychology trying to find consensus by printing squiggles on a chart. Yes, the market is a weighing machine in the long run. But, merde , sometimes the absurdity of the “voting machine” outcomes can be colossal and carry on much longer than most would expect. NFTs, USD 16 trillion of negative-yielding debt, oil trading negative, Gamestop ( GME ), the Macarena. Don’t tell me the market is always rational.

South Africa has challenges. Let’s get that out of the way before we proceed. The ruling government and local politicians in office are largely useless. Any progress in South Africa is made despite them, not thanks to them. Then again, looking around the world today, current political “leadership” is pretty hilarious in most places.

SA unemployment is amongst the highest in the world, around 32%. The state-run power utility is ailing, causing electricity shortages and scheduled cuts. In certain areas and sectors, crime and corruption are debilitating. I’d say the media (both conventional and social) does a sensational job in covering the negatives. Just open your browser and start doing some desktop research on South Africa. The headlines read like something out of a dystopian novel.

Here's the thing. We’re investing in bottom lines, not headlines. South Africa has always advanced politically by disasters and economically by windfalls and ingenuity. As your local guide, my reading is that the timing is now, or very close. I believe we are on the cusp of a multi-year opportunity to earn returns superior to U.S. equity index returns, in a less correlated way. Could I be wrong? Of course I could. Nothing is certain. Is this the hardest I have ever pounded the table? Yes it is. In more than 10 years of professionally managing this strategy, and multiple decades of study, I have never been so convinced. I am backing it up with all my capital.

Important note to our LPs: nothing changes regarding our investment approach. Number 1 and 2 remain front of mind, as always. Protect against the downside. Optimize for returns. We are not changing the approach or the risk profile.

I am talking about timing from an allocator’s perspective. I believe we have hit the point of max pain and capitulation.

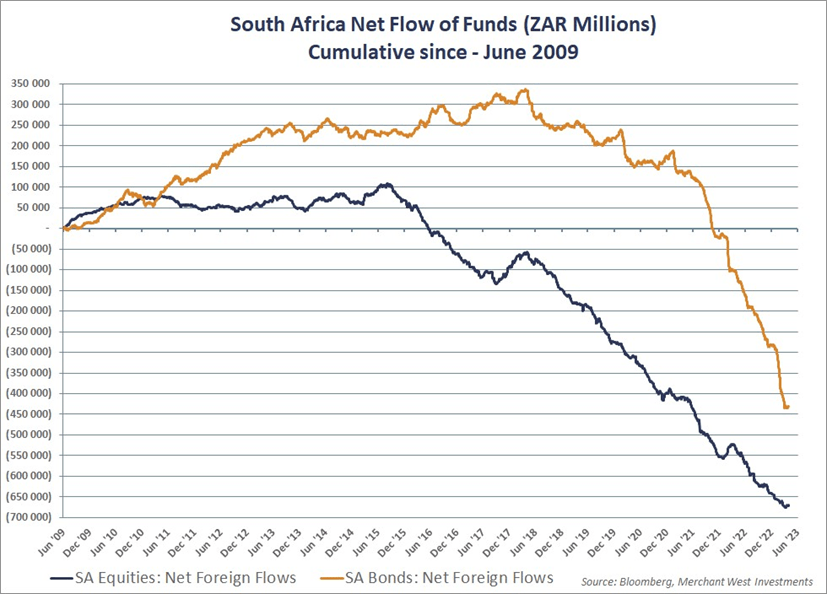

Foreign selling of South African equities and bonds have accelerated to a gushing waterfall.

{kind=link}

Foreign investors have sold local equities for 48 of the last 54 months and now are positioned at half the benchmark weight in South Africa within the emerging market index.

The indiscriminate selling triggers a vicious reinforcing cycle of declining valuations, begetting poor performance, causing yet further selling. For South African portfolio managers, the last 5 years went something like this…

{kind=link}

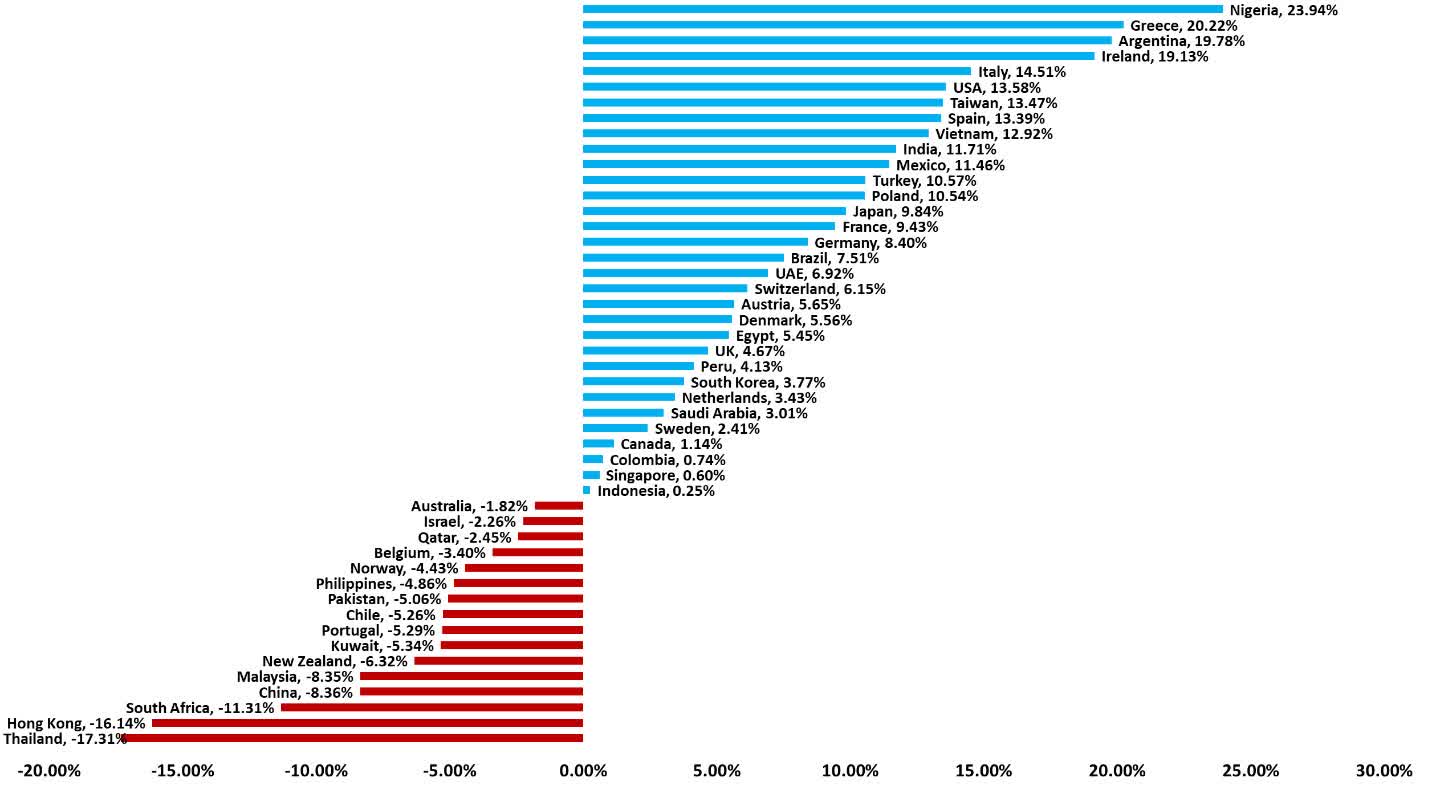

On a year-to-date basis, SA equities is now one of the worst performers globally.

{kind=link}

One would be excused to think this is Armageddon. And that is exactly my point. The consensus view is that this is the end for SA equities. Max pain. Max capitulation. Max stupidity. USD 16 trillion of negative yielding debt, oil trading negative, Gamestop, the Macarena.

Variant Perception

I am writing this on a Saturday. This morning, I walked from my house in the Cape Town suburbs to a nearby coffee shop. The homes are well maintained, vegetation is lush, gardens are manicured. The roads are pristine, infrastructure maintained. The South African private sector installed more electricity generation capacity in the last year than Eskom (the parastatal power utility) has in the last 10 years. Under the radar, power generation in SA is being privatized, just like happened successfully with health and education.

I arrive at the coffee shop, quaint and intimate, and am greeted by staff of all races with equal enthusiasm and friendliness all around. My eye catches a nearby newspaper headlining something about violence and racism. I see none of that here – the country is not homogenous. Bad incidents occur, but it’s not the norm. Most of society just want to work towards improvement, personally and collectively. I order a cortado. Cost: $2. Better than any cortado I have ever had in New York. Toasted sourdough with fresh avocado and two poached eggs. Delicious. Cost: $5.

I am reviewing the business news of the week. One of our companies, Karooooo ( KARO ), reported earnings this week. Their SaaS subscribers in SA is up +14% and management says they are on track to more than double the number of SA subscribers. That certainly does not confirm the narrative that there is no opportunity in the SA economy. Another one of our holdings, Calgro ( CLMHF ), released their earnings report. EPS is up +38%. Cash generation is strong. They repurchased 18% of their shares during the 6-month period. Not bad for a company operating in a country that is “doomed”. The valuation? Calgro is trading on a PE of less than 3 and a -60% discount to book.

David Einhorn recently mentioned in interviews that the traditional value formula seems to be in hibernation. It used to be: Buy a company with decent fundamentals at a 6 PE, wait for the market to recognize the price dislocation and the stock to reappraise to an 8 PE, sell, repeat. These days one cannot count on the market to recognize the mispricing. One must depend on low entry multiples (3-4 times cash flow), dividends, share buybacks, organic growth, and capital allocation to generate the required return – without any expectation for multiple expansion whatsoever. We are at that point. Any reappraisal from this point henceforth will just act as a massive boost to embedded returns.

My phone rings. It is the CEO and substantial shareholder of a small JSE-listed company. We’ve already had some exploratory discussions a few weeks prior. His company has never made a loss and generates ROE’s between 15-20%. Trading is strong and they are looking at another period of decent growth. The stock is trading at a 4 PE and -30% discount to book. He sees no merit in the company being listed anymore. We discuss his options in taking the company private.

Headlines. Versus. Bottom lines.

Why now?

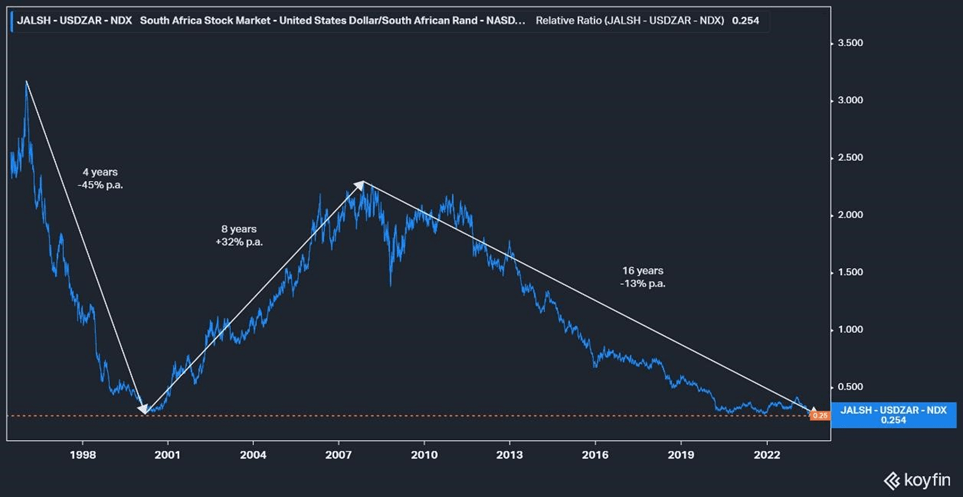

The following chart depicts the JSE All Share Index (in USD) relative to the Nasdaq-100.

{kind=link}

From January 1996 to March 2000 the JSE lagged the NDX by -45% per year. This is understandable given that we were dealing with the extreme denominator of the dotcom bubble.

Over the subsequent 8-year period, the JSE outperformed the NDX by +32% per annum. Keep in mind that we are not just dealing with the indexes and that there is a third variable – currency. Currency often serves as concomitant contributor during periods of under- or outperformance.

Over the last 16 years, the JSE trailed the NDX by -13% per year, one of the longest losing streaks on record. By historical performance measures, the JSE has never been cheaper relative to the NDX over the last 28 years.

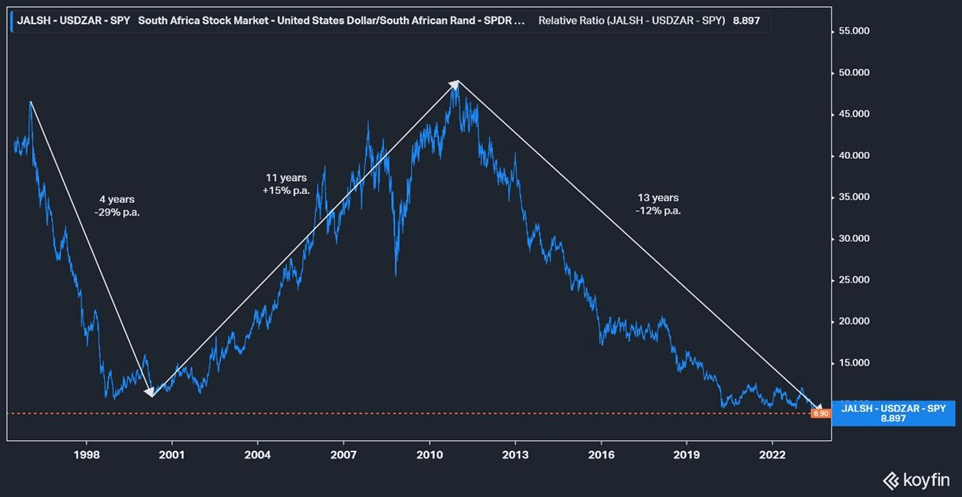

Measuring SA equities performance relative to the S&P 500 delivers the same conclusion (next page):

{kind=link}

April 2000 to December 2010 produced an 11-year cycle of the JSE outperforming the S&P 500 by +15% (all in USD terms). Over the last 13 years the JSE lagged the S&P 500 by -12% per annum. Recall that currency often overshoots one way or the other during these periods. SA equities have never been cheaper relative to the S&P 500 over the last 28 years.

History never repeats, but it often rhymes. We know that markets tend to move in cycles. The catalysts for turning points in cycles are extremely difficult to anticipate a priori. Ex post facto, there are always some rationalized arguments for why it turned on whatever exact date. Similarly, we may not be able to pinpoint the exact reason and timing of the turning at this moment. But the data and probabilities are on our side.

In the words of the legendary Charlie Munger:

It’s not given to human beings to have such talent that they can just know everything about everything all the time. But it is given to human beings who work hard at it – who look and sift the world for a mispriced bet that they can occasionally find one.

And the wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds.

That is a very simple concept. And to me it is obviously right based on experience not only from the pari-mutuel system, but everywhere else.

In Closing (and SA Investor Trip, April 2024)

One of Stanley Druckenmiller's key ingredients for success is to "Never invest in the present, always in the future."

Those investing in the present have reached max antipathy towards SA equities. 13 years of underperformance has flushed out the most resilient and independent minded of participants – if not due to liquidity reasons, then due to emotional capitulation.

Those investing in the future will recognize that the best time to allocate is when the odds are on their side. Right now, asymmetry is squarely in favor of the allocator who has the ability to put emotions and psychological biases aside to place a bet that others will not or cannot place.

At Desert Lion we are not advocating for a large allocation to our strategy. We are unequivocally suggesting that a non-zero allocation makes sense. The evidence available to us indicates that we are at the point in the cycle where an allocation to the Fund has high probability for enhanced returns combined with lower correlation.

We intend hosting a South Africa trip for current and prospective investors around April 6-13, 2024. We will travel throughout Cape Town, including a few company visits and some extramural activities on an opt-in basis. Part of the theme will be highlighting the role of the private sector in addressing public woes. Guests will have the opportunity to evaluate the challenges as well as the triumphs. The previous SA investor trip was a massive success and those who visited South Africa for the first time unanimously expressed (to their surprise) a positive paradigm shift. Space is limited to 10 people. Please get in touch if you are interested.

As always, I thank you for entrusting Desert Lion with your hard-earned capital. Personally, I am all in, in more ways than one. Our interests cannot be more aligned.

All the best,

Rudi van Niekerk

DisclaimerThis document (the “Document”) has been prepared solely for use by potential investors in Desert Lion Capital Fund I, LP (the “Fund”), which is managed by Desert Lion Capital Investment Management, LP (together with its affiliates, “Desert Lion Capital”), and shall be maintained in strict confidence. The recipient agrees that the contents of this Document are confidential, the disclosure of which is likely to cause substantial and irreparable competitive harm to Desert Lion Capital and or its investment vehicles and their respective affiliates. Any reproduction or distribution of this Document, in whole or in part, or the disclosure of its contents, without the prior written consent of Desert Lion Capital is prohibited. The information set forth herein does not purport to be complete and no obligation to update or otherwise revise such information is being assumed. Other events that were not taken into account may occur and may significantly affect the analysis. Any assumptions should not be construed to be indicative of the actual events that will occur. This Document shall not constitute an offer to sell or the solicitation of an offer to buy which may be made only at the time a qualified offeree receives a private placement memorandum describing the offering and related subscription agreement. Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. All information contained in this Document is qualified in its entirety by information contained in the Fund’s confidential private placement memorandum. An investor should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. This and other important information about the Fund can be found in the Fund’s offering memorandum. Please read the confidential private placement memorandum carefully before investing. The information in this Document is only current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which will fluctuate. No representation or warranty (express or implied) is made or can be given with respect to the accuracy or completeness of the information in the Document. Some of the statements presented herein may contain constitute forward-looking statements. These forward-looking statements are based on current expectations, estimates and projections. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Although Desert Lion Capital believes the expectations reflected in any forward-looking statements are based on reasonable assumptions, Desert Lion Capital can give no assurance that such expectations will be attained and therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. Desert Lion Capital undertakes no duty to update any forward-looking statements appearing in this Document. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Diversification does not assure a profit or guarantee against loss in declining markets. Investors should consider their investment objectives, risks, charges and expenses of the underlying funds before investing. The views, opinions, and assumptions expressed in this Document are as of the date of this Document, are subject to change without notice, may not come to pass and do not represent a recommendation or offer of any particular security, strategy or investment. The Document does not purport to contain all of the information that may be required to evaluate the matters discussed therein. It is not intended to be a risk disclosure document. Further, the Document is not intended to provide recommendations, and should not be relied upon for tax, accounting, legal or business advice. The persons to whom this document has been delivered are encouraged to ask questions of and receive answers from Desert Lion Capital and to obtain any additional information they deem necessary concerning the matters described herein. None of the information contained herein has been filed or will be filed with the Securities and Exchange Commission, any regulator under any state securities laws or any other governmental or self-regulatory authority. No governmental authority has passed or will pass on the merits of this offering or the adequacy of this document. Any representation to the contrary is unlawful.References to the MSCI Emerging Markets Index (“MXEF”) and the FTSE/JSE All Share Index (JSE alpha code “ALSH” or JSE index code “J203”) are based on published results and, although obtained from sources believed to be accurate, have not been independently verified. The MSCI Emerging Markets Index is referred to only because it represents an index typically used to gauge the general performance of the midcap and large caps in global emerging equity markets in more than two dozen emerging market countries including South Africa, China, India, Korea, Mexico, Taiwan, the United Arab Emirates and others. The returns for the MSCI Emerging Markets Index include realized and unrealized gains and losses plus reinvested dividends but do not include fees, commissions and/or markups. The FTSE/JSE All Share Index is referred to only because it represents an index typically used to gauge the general performance of the Johannesburg Stock Exchange as a whole. The returns of the FTSE/JSE All Share Index include realized and unrealized gains and losses, but do not include the reinvestment of dividends, and do not include fees, commissions and/or markups. The use of these indices is not meant to be indicative of the asset composition, volatility or strategy of the portfolio of securities held by the Fund. The Fund's portfolio may or may not include securities which comprise the MSCI Emerging Markets Index and the FTSE/JSE All Share Index, will hold considerably fewer than the number of different securities which comprise the MSCI Emerging Markets Index and the FTSE/JSE All Share Index and engages or may engage in Fund strategies not employed by the MSCI Emerging Markets Index and the FTSE/JSE All Share Index including, without limitation, short selling and utilizing leverage. As such, an investment in the Fund should be considered riskier than an investment in the MSCI Emerging Markets Index and the FTSE/JSE All Share Index. Furthermore, indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Desert Lion Capital Q3 2023 Investor Letter