DBI - Designer Brands: A Soft Market Or Company?

2023-12-19 22:50:21 ET

Summary

- Designer Brands reported poor Q3 results with a very significant FY2023 guidance cut.

- Designer Brands' retail chain DSW's new President Laura Denk acknowledges the need to optimize the retail chain's assortment to improve the financial performance.

- The post-pandemic revenue performance and the long-term margin performance are poor, making the assortment changes seem critical in my opinion.

- The current stock price seems to fairly reflect Designer Brands' struggles.

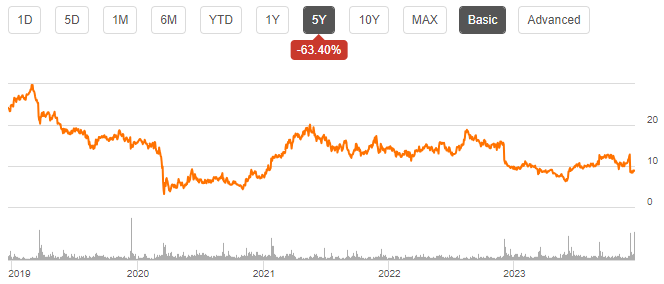

Designer Brands ( DBI ) manufactures and retails footwear in North America. The company operates retail chains called DSW Designer Shoe Warehouse and The Shoe Company, and shoe brands such as Jessica Simpson, Vince Camuto, and Lucky Brand, along with the recently acquired Topo Athletic and Keds. The stock hasn’t had a very good performance in recent years – the share has lost the majority of its value, and the current dividend yield of 2.26% doesn’t salvage the return. In addition to weak past years, the recently reported Q3 results plummeted Designer Brands’ stock even more with a one-day fall of 33%.

{kind=link}

A Q3 Disaster

Designer Brands reported its Q3/FY2023 results on the 5 th of December. The reported result and guidance came as a shock to the market, as can be seen on the stock chart – Designer Brands’ stock fell by 33% in a day due to the report.

The reported results were very poor compared to expectations – revenues missed by $36.4 million, corresponding to around 4.4% of expected revenues. Comparable sales decreased by 9.3% year-over-year, reflecting a poor macroeconomic situation for Designer Brands. With the lower-than-expected sales, the company’s earnings also took a great dive – the reported normalized EPS came in at almost half of the expected value, with a reported normalized EPS of $0.24 compared to an expected $0.46.

In addition, Designer Brands’ outlook for the entire FY2023 was lowered, also casting shadows on the fourth quarter of the fiscal year. Designer Brands’ prior guidance included and EPS guidance of $1.2 to $1.5, and was updated to $0.4 to $0.7 with the Q3 report, more than halving the middle point EPS of the guidance. The revenue outlook was also updated, with Designer Brands’ organic sales growth guided down high-single digits instead of the previous mid- to high-single digits, and the Keds acquisition’s revenue attributions guided down to $60 million to $70 million from a previous estimate of $75 million to $85 million. In my opinion, the Keds guidance coming down by a whopping 19% seems very concerning; such a guidance drop doesn’t seem reasonable, and casts doubt on the current management.

The company’s Q3 earnings call provides some context to the weak financial performance. Same as many other companies currently, Designer Brands outlines the macroeconomic pressures as a negative factor, affecting consumer purchasing significantly. Along with a warm weather, the pressured consumer purchasing has put pressure on the footwear market, which Designer Brands saw in the weak topline; DSW’s seasonal footwear performance in the quarter was mostly in line with the struggling industry.

Designer Brands also acknowledges that the company needs to optimize its retail assortment – the weak performance is also partly due to a weak focus on the retail offering. DSW’s new President Laura Denk focuses a lot on the DSW offering in the earnings call, and mentions Nike returning to the retail chain’s offering with a strong start in sales. In my opinion, the Laura Denk’s focus on the assortment seems great for the company’s financial future. I would hope that the greater focus will improve Designer Brands’ profitability and sales trend, although I expect that the adaptation is likely to take a good amount of time before materializing in the financials.

Long-Term Financial Trends

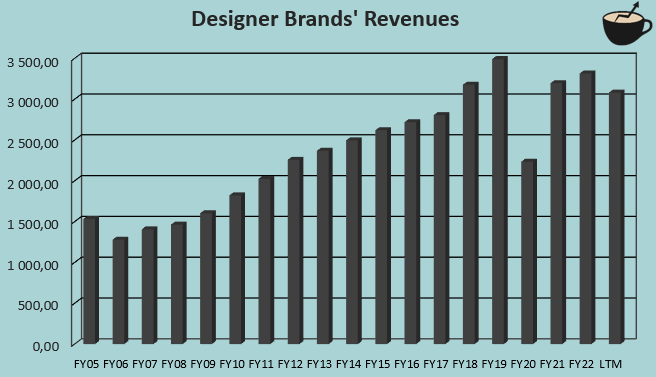

Prior to the Covid pandemic, Designer Brands managed to consistently grow revenues – from FY2005 to FY2019, the company achieved a revenue CAGR of 6.1%. After the pandemic, though, Designer Brands’ operations seem to have taken a more permanent hit. Revenues haven’t climbed back to pre-pandemic levels despite new acquisitions. I believe that the revenue level likely signals a poor fundamental performance in the operations; Designer Brands acknowledging issues with the assortment seems like a good first step for improvement.

{kind=link}

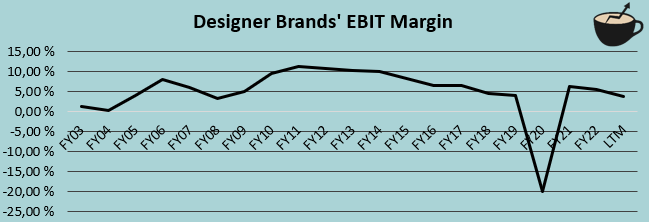

Even prior to the pandemic, Designer Brands margin performance was poor. The growth was largely achieved at the cost of margins in the decade prior to the pandemic, as EBIT margins consistently fell from 11.3% in FY2011 to 4.0% in FY2019. The margin trend is very alarming in my opinion, as the consistent annual margin fall has resumed after FY2021 – the fundamental problems in Designer Brands’ shoe brands and retail assortment are likely to be quite persistent troubles that the company’s management needs to address.

{kind=link}

A Chance to Buy Cheap, Or Not?

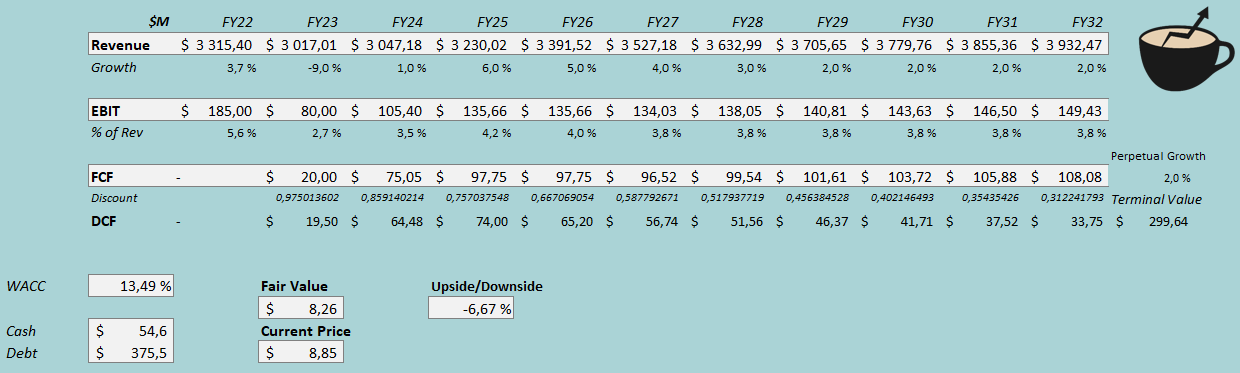

The deteriorating earnings seem to have created a cheap stock assuming that the earnings trend recovers; the trailing P/E of 8.0 at the time of writing already seems quite cheap. Still, I don’t necessarily think that the price dip is yet a very appetizing chance to load up on the stock, as fundamental concerns around the earnings recovery seem very reasonable. To better demonstrate the valuation, I constructed a discounted cash flow model.

In the DCF model, I estimate the company’s future to be mostly in line with the long-term past after the current macroeconomic pressures subside – after a FY2023 revenue drop of 9%, I estimate Designer Brands to still struggle with only a 1% growth in FY2024. After the year, I estimate a recovery back into modest growth with a FY2025 revenue growth of 6% that slows down in steps into a perpetual growth rate of 2%.

As for the margins, I wouldn’t expect too high scaling even as the macroeconomic situation improves. Designer Brands’ long-term margin deterioration seems worrying, and although Laura Denk’s focus on the DSW assortment could turn the trend around, I don’t expect too much as a baseline scenario before the better financial performance is shown. With the improvement of the macroeconomic situation, I estimate the company’s EBIT margin to improve from a FY2023 estimate of 2.7% into 4.2% in FY2025, but to fall back into a sustainable level of 3.8% afterwards. With the low overall growth, Designer Brands’ cash flow conversion should be fairly good.

With the mentioned estimates along with a cost of capital of 13.49%, the DCF model estimates Designer Brands’ fair value at $8.26, around 7% below the stock price at the time of writing. The DCF model could still vary a lot in the actual financials, though – the assortment focus is the most notable variable in my opinion, that could improve Designer Brands’ EBIT margins from my estimates. With the currently weak financials, I still proceed with caution.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3/FY2023, Designer Brands had around $8.8 million in interest expenses. With the company’s current amount of interest-bearing debt, Designer Brands’s annualized interest rate comes up to 9.34% - Designer Brands’ interest rate seems to be quite high. Still, the company utilizes quite a high amount of debt, and I estimate a long-term debt-to-equity ratio of 40%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.90% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Designer Brands’ beta at a figure of 2.01 . Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 16.08% and a WACC of 13.49%.

Takeaway

Designer Brands reported a weak Q3 result. Although a good part of the result can be attributed to pressured consumer spending and a warm weather lowering seasonal footwear sales, the company does also seem to be struggling with company-specific issues. The current focus on DSW’s retail offering could potentially improve the long-term trend of margin deterioration with a successful relaunch of Nike, but until the better performance is shown in financials, I remain cautious. At the moment, I believe that the stock is priced fairly as the DCF model mostly suggests with the small downside – for the time being, I have a hold rating.

For further details see:

Designer Brands: A Soft Market Or Company?