DBI - Designer Brands: Cautiously Facing Challenging Market

2023-04-09 03:21:02 ET

Summary

- Designer Brands reported a decline in customer demand which negatively impacted the top line, however own brand growth strategy leads to a positive EPS of $0.07, beating expectations by $0.09.

- Own brand strategy continues to improve gross margins and Designer Brands has a goal of increasing its own brand sales to one-third of total sales by 2026.

- Cautious of high debt, volatile market and decreasing consumer demand.

In a fiercely competitive market, Designer Brands Inc. ( DBI ) is beating earning expectations due to a successfully owned brand growth strategy which saw sales increase by 31% YoY. While the company has seen a decline in consumer demand, negatively impacting top-line growth in Q4 2022 , and net sales only increased by 3.7% YoY for FY2022 , its owned brand growth ensures more generous profit margins. DBI has downgraded its forecast for FY2023 amidst market headwinds. However, EPS is expected to remain positive between $1.65 and $1.75. Although cautious of market uncertainty and a decline in consumer demand across the luxury market , I remain bullish on the stock due to its growing profit margins, product diversity, direct-to-customer sales approach and low price point compared to larger competitors.

Competing against direct-to-consumer brand sales

Seven years ago , DBI took two critical steps to ensure its place in a cutthroat retail industry by extending its sales scope into international markets and initiating an owned brand growth strategy. This has allowed the company to compete against the growing trend of direct-to-customer sales by the same brands the company offers. Since 2019 the company has grown its online presence from one to five e-commerce sites, with a sixth to be added later this year . DBI has three brands in its portfolio, as shown in the image below.

Brand portfolio (designerbrands.com)

Earlier this year, DBI increased its owned brands product range by acquiring Keds business, a casual and athletic footwear company, which builds onto the earlier acquisitions of Le Tigre and Topo Athletic LLC in 2022. Through Keds, DBI's owned brand business enters the children's footwear segment for the first time. Over the last three financial years, we can see the growing importance of its owned brands on total net sales. The company aims to generate one-third of total sales through owned brands by 2026.

Revenue national brands versus owned brands per year (sec.gov)

DBI has stayed relevant by moving into casual footwear in a timely fashion and its seasonal and fashion footwear through direct-to-consumer channels. The casual category has grown into 47% of its assortment. Furthermore, like many luxury companies, DBI has taken actions to streamline the business, such as labour cuts , to control rising costs and continue to tackle the market headwinds.

Financial overview

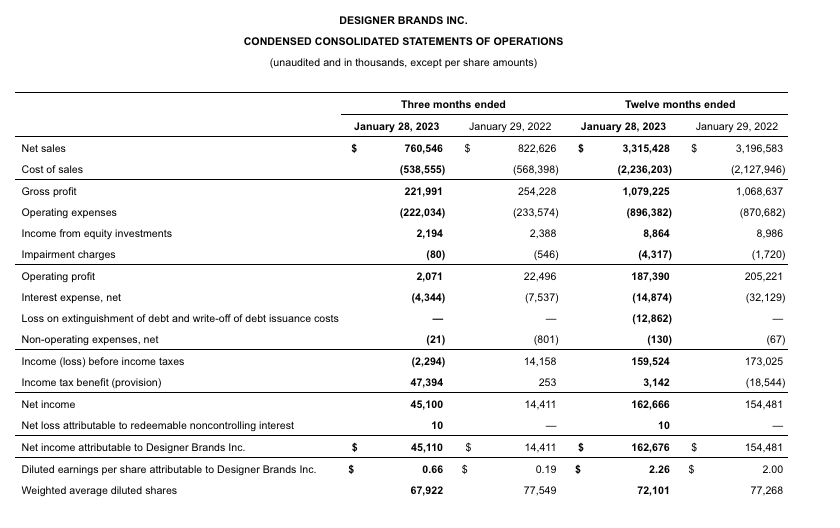

DBI posted mixed results in its Q4 2022 and full fiscal year earnings report due to the market headwinds, promotional environment and customers looking for value. We only saw total revenue increase in the low single digits by 3.7% to reach $3.3 billion, its net income was $133.7 million, and DBI reported an EPS of $1.86. One of the significant highlights is the growth in net sales from its owned brands which were up by 32.1% YoY to reach $569.7 million. This has had a positive impact on gross profit margins YoY.

{kind=link}

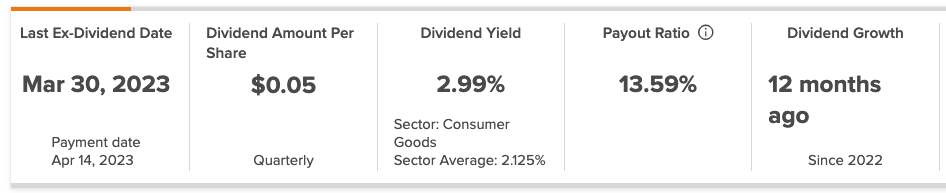

Due to the promotional market, the company continues to operate in a high inventory market. In Q4 2022, inventory ended at $605.7 million compared to $586.4 million in the prior year. However, inventory management is said to be better or more typical to the current industry trends. DBI has a consistent and positive levered free cash flow at $160.77 million TTM, and its cash from operations was $201.43 million TTM. DBI has a dividend program and pays out a dividend yield of 2.99% at a reasonable payout ratio of 13.59%.

{kind=link}

A potential reason to avoid this stock is the high debt intake compared to its cash. We can see that DBI has a cash balance of $58.77 million; however, its total debt is $1.1 billion. This is due to the number of acquisitions onboarded quickly to build its owned brand strategy. DBI has a revolving credit facility, meaning its total liquidity, including cash, was $302.7 million. The company had $243.9 million available from the credit facility. It has a current ratio of 1.24; however, its quick ratio decreases to 0.21, making the stock riskier as it doesn't have sufficient liquid assets to pay off short-term liabilities.

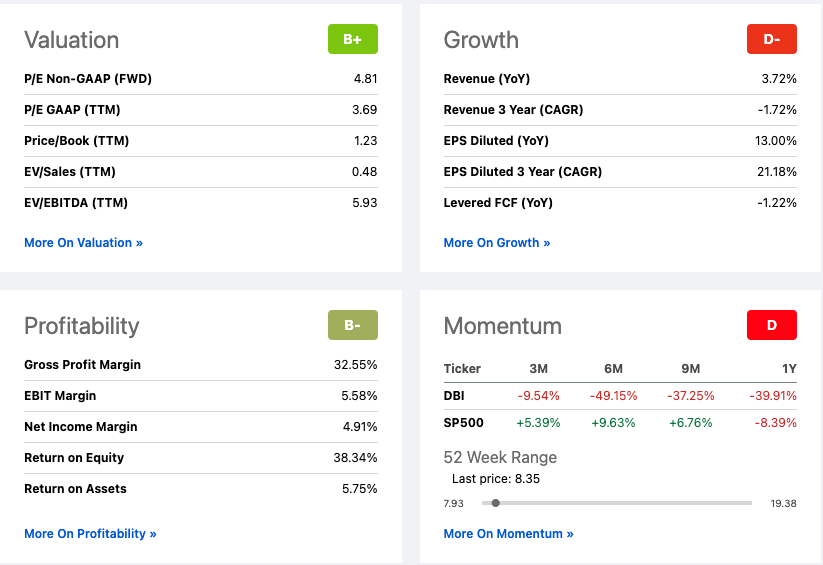

The average target price for DBI is $12.67, well above the current stock price. However, various analysts have recently trimmed their price targets, such as UBS, from $11 to $10 and the stock is rated as a Hold status on Market Screener and by Wall Street at a value of 3. The stock has underperformed the S&P Index over the short and long term, and we can see unimpressive top-line growth. However, its growing profit margins have significantly improved its EPS this year. Due to the recent drop in stock price, DBI has a desirable FWD price-to-earnings ratio of 4.81.

{kind=link}

Final thoughts

DBI has reported impressive bottom-line growth and better inventory management than some competitors and has significantly grown its owned brand segment. However, it has forecasted a weaker performance for its FY2023 due to the prediction of current market pressure to continue to impact customers negatively for the first part of the year. Management cautiously remarks that by Q4 2023, sales may see a slight improvement. Although we should remain cautious of the downward trend in consumer demand over the short term, the high debt intake and the fiercely competitive retail environment, I believe its owned brand strategy, direct-to-consumer sales channels and growth into sportswear and casual shoes will benefit the business in the long run. Therefore I remain bullish on this stock.

Forecast for FY2023 (Investors.designerbrands.com/press-releases)

For further details see:

Designer Brands: Cautiously Facing Challenging Market