DBI - Designer Brands: More Profitable In-House Brand Growth Strategy

Summary

- Designer Brands stock took a tumble after its Q3 2023 results missed expectations as sales were impacted by drop off in consumer traffic and demand for discretionary products.

- The stock has long-term upside potential through an in-house brand growth strategy improving profit margins, new acquisitions in popular athletic, and outdoor footwear brand categories.

- Its long history in direct-to-consumer infrastructure benefits growing its own brands offline and online.

- Cautious of recessionary headwinds on discretionary spending, high debt levels, and short interest.

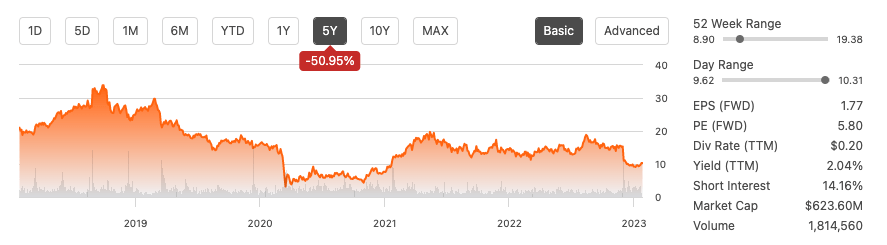

Designer Brands, Inc. ( DBI ) is the 20th largest global footwear company with a market cap of $623.6 million. It is an offline and online retailer of the most prominent brands and a growing number of owned brands. Although the stock had been recovering from its COVID-19 downfall, the value dropped significantly after reporting its Q3 2023 financial report that fell under analyst expectations.

Five-year stock trend (SeekingAlpha.com)

{kind=link}

Although we cannot ignore the reduction in consumer discretionary spending, DBI has been recovering its top and bottom line since COVID-19, with a TTM of $3.38 billion in revenue and a TTM net income of $131.98 million. It is strategically transitioning into a company with a higher number of Owned Brands with higher profit margins, has onboarded a new CEO with experience in vertical brand and direct consumer growth, and before COVID-19, the stock was comfortable trading above $15 since 2010. Although cautious of economic, supply chain and labour headwinds in a highly competitive retail market and the difficulties associated with a growing brand portfolio, there is a lot more upside for this company that sells successfully through stores and its e-commerce platforms. Therefore investors may want to take a bullish stance on this company.

Overview

DBI is a long-standing designer, producer and retailer of footwear and fashion accessories from diverse brands, with its origins in footwear dating back to 1969. More recently, it has and is transitioning into a brand builder, growing its in-house brand sales to 27% in Q3 2022, intending to double sales by 2026. It has a loyalty program with 30 million customers, over 700 stores and three online platforms. The company went public in 2005 and launched its first e-commerce site in 2008, and the portfolio is built up of the three brands described in the image below.

Brand portfolio (Company website)

{kind=link}

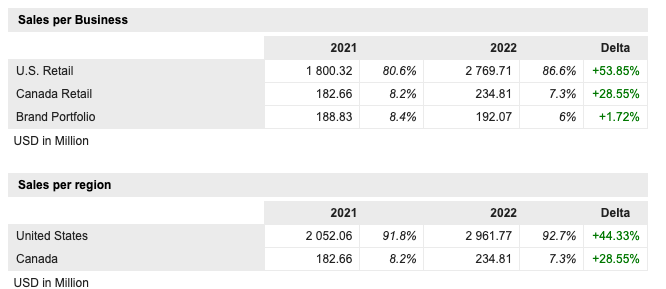

It generates revenue through three segments across the United States and Canada. Firstly, the US retail segment, accounting for 86.6% of FY2022 sales, operates DSW Designer Shoe Warehouse ((DSW)) and generates revenue through consumer stores and an e-commerce site. Secondly, the Canada retail segment, accounting for 7.3% of total sales, which is The Shoe Company and DSW, is sold through stores and online. Lastly, at only 6% of total sales, The Brand Portfolio segment does a variety of activities such as wholesale to retailers, receiving commissions as the agent, and selling branded products through vincecamuto.com.

Sales per business segment and region (marketscreener.com)

{kind=link}

DBI is focusing on vertical brand growth, which can lead to better margins, and more cost control and potentially speeds up the rate of bringing products to the market. One of its most recent efforts has been to acquire Topo Athletic, which puts them in the private athletic and outdoor footwear categories. It is also putting in place the leadership to run this transition. The current president, Doug Howe, who was only onboarded in May 2022, will become the company's new CEO. He has profound experience in growing vertical brands and direct-to-consumer sales.

Financials

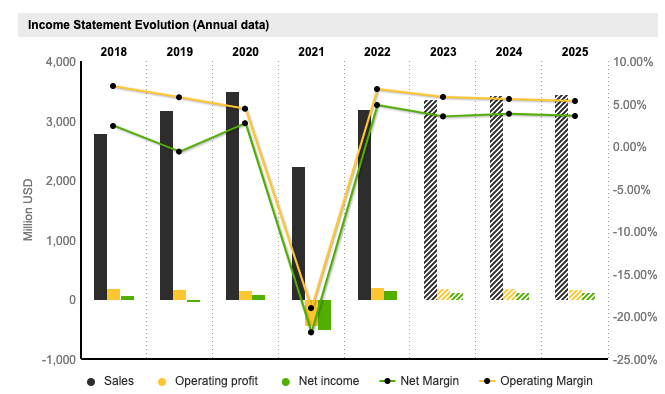

If we look at the trending financials, we can see that on trend with many retailers, COVID-19 put a considerable dent into the business, followed by a surge of demand in FY 22. The company has slowly been recovering. Its TTM revenue is at $3.377 billion, and the gross margin in FY22 was 33.43% was higher than the last four years; currently, TTM is slightly lower at 32.91%.

Financial overview (marketscreener.com)

{kind=link}

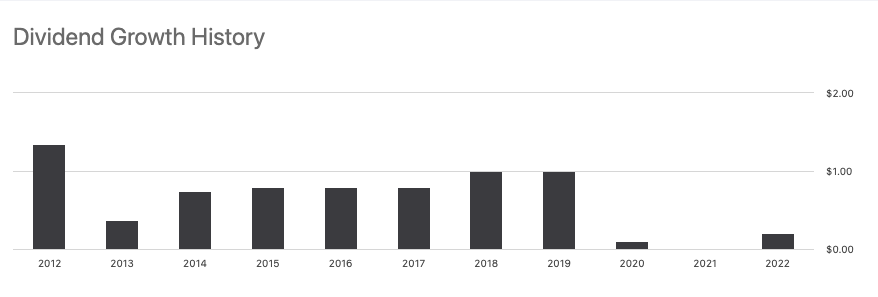

DBI made $45.08 million in cash from operations TTM, with a positive levered cash flow at $13.08 million. This cash could be used to pay dividends. The company has a dividend yield of 2.02%. Its last dividend was paid out on 28 December 2022 at $0.05 per share. The dividend program was severely impacted by COVID-19 business performance, as seen in the growth history below. In FY 2021, the company produced negative cash flow for the first time in over eight years at negative $195.6 million but is slowly recovering.

Dividend growth history (SeekingAlpha.com)

{kind=link}

On the balance sheet, we can see total cash of $62.51 million and a much higher total debt at $1.23 billion, giving us a dangerously high debt-to-equity ratio of 321.22%. Before FY19, the company was debt free. Since then, we have seen it make an acquisition , in addition to funding and managing operational losses in FY21. If we look at liquidity, it has a decent current ratio of 1.43. However, the quick ratio is well below one at 0.41, which makes the stock riskier as it doesn't have sufficient liquid assets to pay off short-term liabilities. Its inventory has also been increasing over the last three years, which we have seen across the retail industry, with a TTM of $681.8 million; however, through its clearance sales strategy, the business can self-liquidate.

Annual total debt (SeekingAlpha.com)

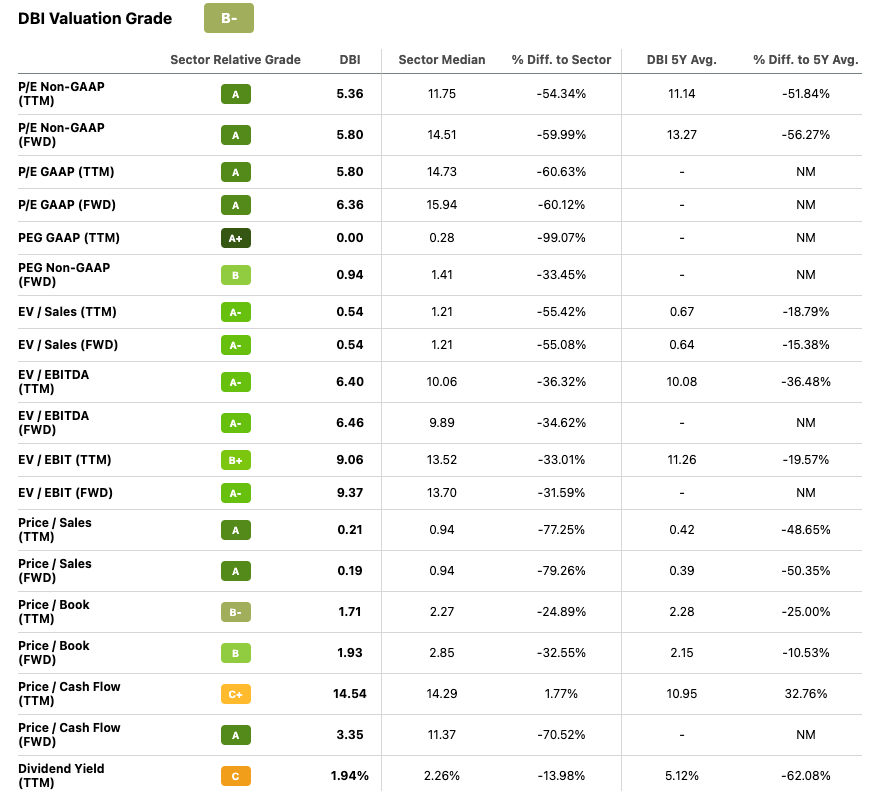

If we look at Seeking Alpha's Quant valuation grade, DBI is given a B-. Compared to the consumer discretionary sector, the company has a desirable FWD price-to-earnings ratio of 5.80, well below that of the industry, indicating that it may be undervalued. Price to sales is very attractive. As a company bringing in billions of dollars in revenue, it has a ratio of 0.21, indicating that investors are paying well below a dollar for every dollar made. The dividend yield took a massive cut, and rightly so, when times were tough. However, this has impacted its grade.

DBI valuation metrics (SeekingAlpha.com)

{kind=link}

Risks

The recessionary economic environment heavily impacts the consumer discretionary industry. Consumers are purchasing less than predicted, which immediately affects DBI in terms of a drop in sales and an increase in excess inventory. It is essential to realize that DBI went through a major downfall due to COVID-19. We can see that the company is slowly recovering and has even made a recent acquisition. In these last years, it has taken on much debt and does not have sufficient liquid assets if it were to have to pay off short-term liabilities. Investing in a company with such a very high debt-to-equity ratio is risky. Furthermore, the company is growing its in-house brand portfolio, which has significant gross margin, cost and speed-to-market benefits. However, integrating different brands can be difficult, time-consuming and costly and potentially impact the company's performance if it is not managed correctly. However, the business is on the right track with new management with vertical brand integration and growth experience.

Final thoughts

DBI has a compelling own brand growth strategy that is starting to show good results. The gross margins have grown from legacy levels. Sales revenue has increased across all segments. The company is expanding its brand sales. Although the company was impacted by an industry-wide drop in discretionary buying and Q3 2023 results were less than predicted, at an attractive price-to-earnings ratio of 6.36 with a clear growth strategy, there is a lot more potential upside for this stock. Therefore investors may want to take a long-term bullish stance on DBI.

For further details see:

Designer Brands: More Profitable In-House Brand Growth Strategy