DBI - Designer Brands: Near Term Challenges In A Fiercely Competitive Industry

2023-10-12 09:53:44 ET

Summary

- Designer Brands Inc. has seen a 31.64% increase in stock value this year, but there has been a substantial rise in short interest.

- The approaching holiday season may not fully offset the overall decline in sales, with stagnant sales growth expected across the industry in 2024.

- Despite strategic shifts and improved gross profit margins, industry headwinds and a year-on-year sales decline suggest caution in buying the stock.

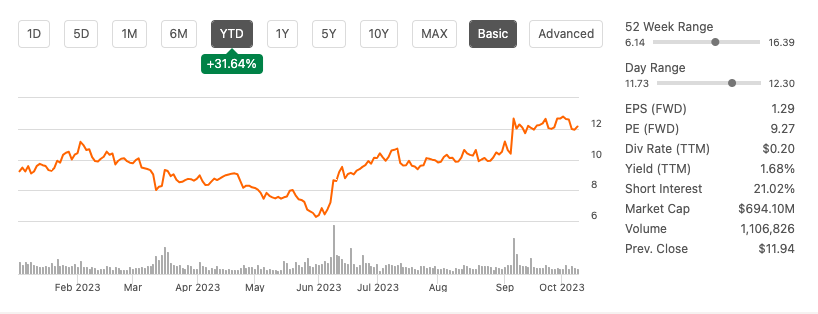

As the twenty-third largest footwear company, Designer Brands Inc. ( DBI ) has experienced an impressive 31.64% stock value increase year to date. However, it's worth highlighting a substantial rise in short interest in the stock since my previous article . Additionally, industry reports suggest that the approaching holiday seasons may not fully offset the overall decline in sales, with expectations of stagnant sales growth across the industry in 2024.

Stock trend year to date (SeekingAlpha.com)

{kind=link}

In the fiercely competitive footwear industry, Designer Brands has executed significant strategic shifts to enhance its position as a small-cap stock. Its unwavering commitment to doubling the sales of in-house brands from 2021 to 2026 has notably contributed to improved gross profit margins. Nonetheless, given industry headwinds, a year-on-year sales decline, rising costs, and the stock price hovering close to its average price target of $12.67, I would advise against buying at this juncture. Therefore, I maintain a hold rating on the stock.

Company update

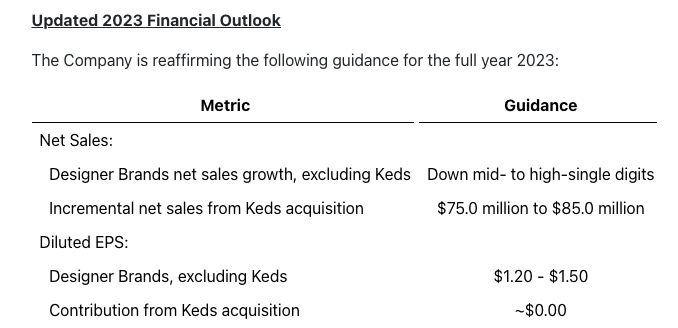

In my first article , I discussed Designer Brands' recent transformative journey in both its business model and leadership. The company has embarked on several promising initiatives. Its strategic shift towards in-house brands has bolstered gross profit margins. Designer Brands is also tapping into the thriving athletic and athleisure market with new offerings from Le Tigre and Keds, and reinforcing its collaboration with Nike (NKE) in response to increasing demand in this segment. These strategic moves leverage the synergy between its retail business and brand portfolio, enhancing overall resilience. However along with industry headwinds there are expected short-term challenges associated with transitions, including costs related to CEO changes, restructuring, and integration. In Q1 2023, Designer Brands reduced its full-year forecast, and its most recent guidance maintains expectations of single-digit sales growth, with diluted EPS projected to range between $1.20 and $1.50.

FY 2023 financial outlook (Sec.gov)

{kind=link}

Financials and valuation

In Q2 2023, Designer Brands exhibited a mixed performance. While there was an improvement in sales compared to the prior quarter, a year-on-year analysis reveals a decline in both the top and bottom lines. The company reported a 7.8% decrease in net sales, totaling $792.2 million, compared to the same period in 2022. Total comparable sales also declined by 8.9%. Gross profit for the quarter amounted to $273.4 million, slightly lower than the previous year's figure of $295.7 million, though there was a marginal increase in gross margin, rising from 34.4% to 34.5%. Reported net income attributable to Designer Brands Inc. stood at $37.2 million, resulting in diluted EPS of $0.56.

Income statement (SeekingAlpha.com)

Designer Brands Inc. has maintained positive levered free cash flow, amounting to $242.8 million TTM, and has demonstrated an upward trend over the past four fiscal years. This robust cash flow not only enables the company to reward its investors but also provides the resources for reinvestment in the business and the ability to reduce debts.

Annual levered free cash flow ( SeekingAlpha.com )

{kind=link}

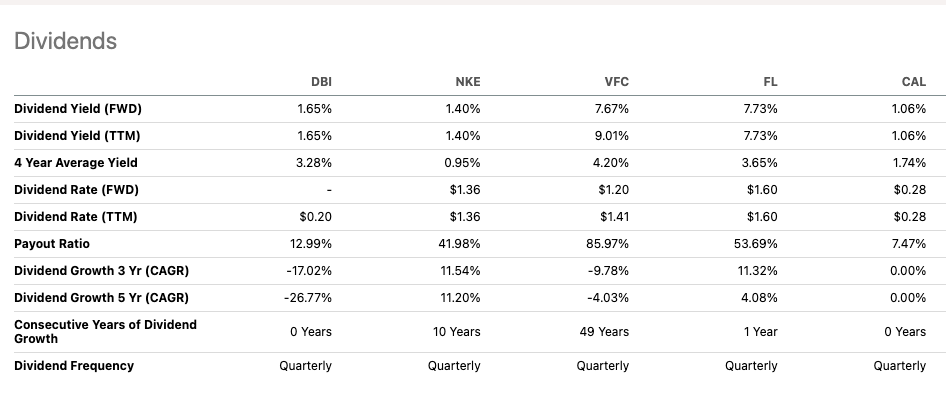

The company's current quarterly dividend yield of 1.68% falls significantly below its four-year average of 3.28%, raising concerns. A comparison with larger footwear peers like Nike, V.F. Corporation ( VFC ), Footlocker ( FL ), and Caleres ( CAL ) reveals that their dividend yields, except for Caleres, have not only increased but also demonstrated better consistency. Additionally, the company's dividend has shown a negative growth rate with a CAGR of -26.77% over the last five years. If you're seeking a dividend-producing stock, exploring more promising alternatives within the same industry may be worth exploring.

{kind=link}

As of Q2 2023, Designer Brands Inc. held $46.2 million in cash, down slightly from the previous year. The company had access to $233.7 million through its revolving credit facility and an additional $85.0 million from a new term loan credit agreement. Total debt decreased from $387.4 million to $331.0 million year-over-year. Inventory also decreased from $694.0 million to $606.8 million. The decrease in total debt and improved inventory management for Designer Brands Inc. in Q2 2023 signal stronger financial health and effective resource utilization, which can boost investor confidence and the company's ability to pursue growth opportunities. Additionally, having access to significant credit resources provides financial flexibility for future investments and operational needs.

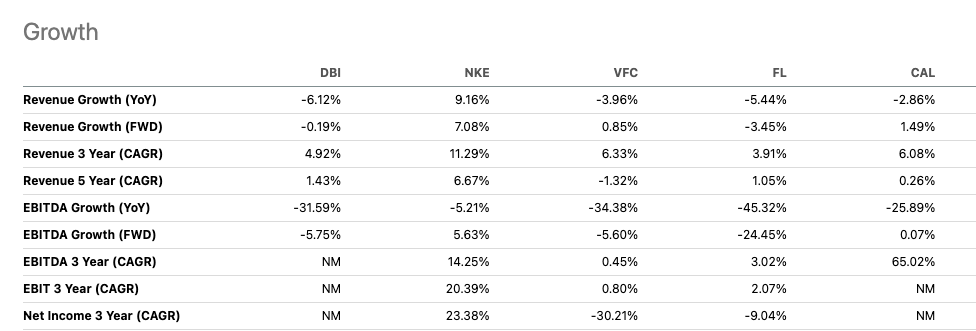

Designer Brands' stock experienced substantial growth momentum following a share buyback in June and benefitted from an improved financial performance in Q2 2023. However the stock is currently hovering near its average price target of $12.67 and has a high short interest of 21.02% which indicates negative sentiment towards the company. The ongoing decline in sales growth compared to the previous year is expected to persist due to the current promotional retail environment which raises concerns. If we compare revenue growth to some of its larger footwear peers we can see that Designer Brands experienced a steeper decline in sales.

{kind=link}

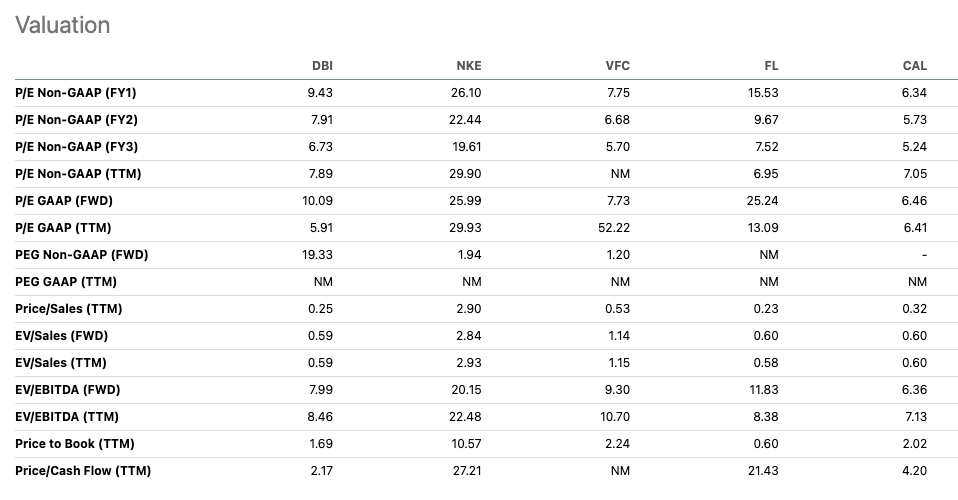

When analyzing the forward price-to-earnings ratio, it's evident that the company falls below larger peers like Nike, indicating a potentially attractive valuation. However, when we consider growth prospects and examine the price-to-earnings-to-growth ratio of 19.33, it becomes apparent that this valuation metric is significantly higher than that of most of its peers, suggesting the stock may be overvalued. In addition, it's essential to note that the management lowered its FY 2023 forecast in Q1 2023 and has maintained this position. This cautionary approach is warranted, given the declining sales, and it's worth highlighting that the promotional environment could further impact profitability, making it a potential area of concern for investors.

{kind=link}

Risks

Designer Brands operates within a fiercely competitive industry grappling with a highly promotional retail environment, as evidenced by its 7.8% decline in sales. Experts anticipate that the industry will persist in facing significant challenges ahead. The ongoing macroeconomic pressures on consumers pose a potential threat, with the possibility of intensifying and affecting the broader retail sector. In this landscape, the company may encounter hurdles related to consumer discretionary spending and increased competition, which could impact its performance, particularly in the near term. Navigating these challenges and adapting to changing consumer behaviors will be key for Designer Brands to maintain resilience and drive future growth.

Final thoughts

Designer Brands has undertaken promising initiatives, including introducing new brands such as Le TIGRE, fortifying partnerships with established brands like Nike, and expanding through exclusive licensing agreements like Hush Puppies. These actions underscore the company's commitment to diversifying and enriching its brand portfolio. Additionally, the effort to enhance gross margins and provide returns to shareholders through dividends and share repurchases highlights confidence in its long-term vision. Nevertheless, the company has witnessed a year-on-year decline in sales, and it anticipates ongoing challenges in the competitive retail landscape. Furthermore, the stock currently hovers around its average price target, coupled with a significant short interest, which may reflect underlying negative sentiment. Therefore, I recommend exercising caution, maintaining a hold rating

For further details see:

Designer Brands: Near Term Challenges In A Fiercely Competitive Industry