DXLG - Destination XL Group: Attractive Valuation But Still Not The Best Time To Buy

2023-06-11 09:47:39 ET

Summary

- Destination XL Group shares have fallen 25% YTD, but the company has shown improved operating and financial performance in the past three years.

- We maintain a HOLD recommendation due to macro pressures on consumer income and apparel spending, but may change to a Buy recommendation if macro factors normalize and strong business trends continue in 1H 2023.

- Risks include competition, margin pressures, and macro factors such as declining consumer confidence and real incomes.

Introduction

Shares of Destination XL Group ( DXLG ) have fallen 25% YTD. I decided to analyze the company's shares because I like the way the company has been able to improve its own operating and financial performance over the past 3 years. In addition, business continues to look confident despite pressure from macro factors and pressure on consumers' real disposable incomes. In addition, the company is still relatively cheaply priced according to multiples.

Investment Thesis

Despite the fact that I am impressed with the company's performance and financial results relative to past results, I currently stick to a HOLD recommendation for the company's shares, as the recent rally and revaluation of the shares partly reflect the positive business trends, we have seen on the company's financial results in 2022 and in the first quarter of 2023. Also, I'm still of the opinion that macro pressures on real consumer income and apparel spending may prevent stocks from rising faster than the broader market. I would like to note that I would happily change my recommendation to Buy if I see a normalization in macro factors such as inflation and consumer real disposable income, and if I see a continuation of the strong business trends in 1H 2023.

1Q 2023 Earnings Review

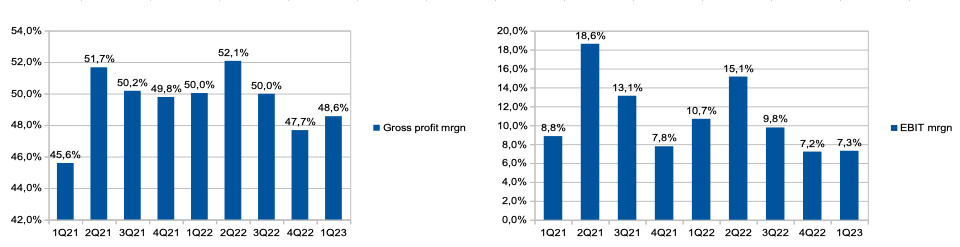

Revenue in 1Q 2023 decreased by 1.7%, gross margin decreased from 50% in 1Q 2022 to 48.6% in 1Q 2023, and EBIT margin decreased from 10.7% in 1Q 2022 to 7.3 % in Q1 2023. You can see the details in the chart below.

Company's information (Company's information)

{kind=link}

The pressure on the gross margin was mainly due to the effect of deleveraging. Decline in business volumes with a constant share of fixed costs led to a decrease in profitability.

Comparable sales grew by 0.6%, which in my personal opinion is not a bad result, although we see some slowdown compared to previous quarters. However, compared to a broad market, comparable sales of the company look strong thanks to the effective positioning of the business (concentration on a narrow segment and a narrow category of customers). The decrease in comparable sales is mainly due to a decrease in traffic, while the average person remains at a stable level.

The share of different business segments remained approximately at the same level. Comparable sales grew by +1.5% from stores, while we see a decline of 1.5% in direct business.

Company's information (Company's information)

{kind=link}

The total number of stores in the chain has decreased from 286 to 281, but here it is worth paying attention to the conversion of Casual Male stores into DXL Retail, which is being carried out by the company's management.

Company's information (Company's information)

{kind=link}

I like the absence of debt on the company's balance sheet and the presence of a financial cushion, which amounted to about $46 million in the quarter. I believe having cash on hand is especially relevant in an uncertain macro environment and rising interest rates.

In addition, in line with management comments, the company is launching a new $15 million share buyback program through March 16, 2024.

My Expectations

I would like to underline the words of management that the company did not carry out a significant price increase in order to support a weak consumer. In my personal opinion, this may create risks of lower profitability due to rising cost inflation. I believe that this may be a risk to financial results in the next quarter.

I still believe next quarter results will be under pressure. If we look at management's expectations, the company expects comparable sales for the year to be around 5%, with 2H 2023 results making the biggest contribution.

I believe that macro factors such as lower consumer spending and high inflation will persist in the first half of 2023, which could have a negative impact on 2Q results. However, then I expect a normalization in the second half of 2023, because, in my personal opinion, the company is well positioned to continue to grow the business (concentration on a narrow segment and type of customers), increase economies of scale and increase profitability.

Drivers

Positioning: concentration on a narrow and specialized market segment with high customer loyalty allows the company to effectively position its own products, meet consumer expectations and increase market share. According to the company's statements, management estimates the total addressable men's big and tall market at $23 billion, which could allow the company to continue to demonstrate strong business growth in the future.

Margin: growth of traffic in the stores of the network, the ability to raise prices more aggressively as real incomes grow could not only boost the business's revenue, but also increase purchasing power and increase economies of scale, which could support the business's operating margin in the future.

Risks

Competition: here I would like to highlight not just competition with other market players, but competition with marketplaces, since the profitability of sales on marketplaces is lower due to commissions on the site. Thus, an increase in the share of revenue from marketplaces can have a negative impact on the merchandise margin, because sales on marketplaces are less marginal for the company due to the site commission.

Margin: in October 2022, the company launched the DXL rewards club loyalty program, which should help the company not only increase the loyalty of its current customer base, but also help increase the average check and purchase frequency. However, additional investments in the loyalty program lead to additional costs, which can have a negative impact on profitability if attracting new users to the loyalty program does not lead to an increase in purchase frequency, average check, and so on. Increased costs for raw materials, freight, additional investment in prices and marketing campaigns can also lead to lower operating margins.

Macro: declining consumer confidence and declining real incomes could lead to lower consumer spending on clothing, which could have a negative impact on the business's revenue growth rate. What I mean is that a decrease in consumer confidence and real incomes can lead to a decrease in the average check, a decrease in traffic in the chain's stores and a decrease in the frequency of purchases.

Valuation

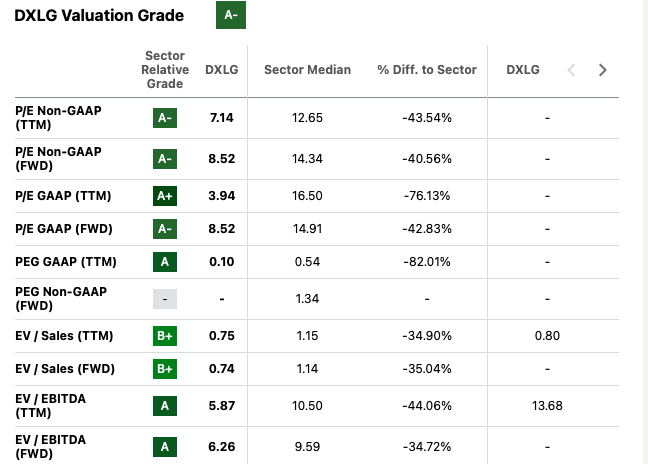

The company is still relatively cheaply valued on multiples, even despite the stock's recent rally following a Q1 2023 report. I believe that the company continues to trade cheap even despite the discount, in view of the relatively small market capitalization of the business. At the moment, FWD P/E is around 9, which in my opinion creates potential for growth in quotes, however, growth will require significant drivers and strong business results. I believe that not Q2, but Q3 and Q4 2023 financials, when the company will be less pressured by macro uncertainties, can serve as a catalyst for the growth of shares.

{kind=link}

Conclusion

I would like to note that I will gladly change my recommendation to “Buy” if I see the normalization of the macro environment and the reflection of management's forecasts and expectations in the financial and operational statements for the quarter. For now, I stick to a HOLD recommendation because I expect the company to continue to face pressure from demand and inflation in the next quarter. However, the company is valued relatively cheaply, which, in my personal opinion, partially limits the downside risks. I will continue to monitor the company closely and may change my recommendation after Q2 and Q3 2023 results.

For further details see:

Destination XL Group: Attractive Valuation, But Still Not The Best Time To Buy