DBOEY - Deutsche Börse: Plenty To Like About Undervalued Stock Market Companies

2023-10-04 06:51:52 ET

Summary

- Deutsche Börse is a deep-value company with a strong credit rating, minimal debt, and high profitability metrics.

- The company's 1H23 results show increased net revenue and EBITDA, driven by profitability, revenues, and cyclical tailwinds.

- Deutsche Börse's diverse income streams and plans for European expansion make it an appealing investment despite potential volatility and slower growth.

Dear readers/followers,

Stock market companies are among the more interesting finance investments that I engage in. One of the investments I've spoken about often is Deutsche Börse ( DBOEY ). I've been covering this business for about 1.5 years at this point, and this is a continuation of my thesis for the company, which was updated on July 24 this year and can be found here.

So, why do I like Deutsche Börse?

Simple. Deep-value companies with AA-credit rating, minimal debt, and high profitability metrics, are likely to deliver solid performance in the near and in the longer term. Even if volatility and fear and greed, or the VIX, stay relatively high, I still believe this company has so much to offer longer-term investors.

In this article, I'll update that for 2Q23, and see what we can expect for the remainder of the year as well as going forward into the next few years. Despite the recent set of stock market movements, I'm still up double digits for the year, and this is despite having very low exposure to the tech-heavy NASDAQ.

Let's look at what we have here.

Deutsche Börse - Plenty to like

These sorts of companies such as Deutsche Börse have a high correlation to the overall stock market. Usually, when the stock market is up, they're up, and when it snaps down, Deutsche Börse does the same - though not as extremely as some companies. The same trends have been able to be observed for the past few months - the company is down, even somewhat more than the S&P500, but has nonetheless managed to stay above a double-digit drop which we've seen in other companies.

Fundamentals remain one of the major arguments for this company. It's AA-rating is one that's hard to beat - and I remain very clear about that while DBOEY exists, I would primarily invest in the native ticker, which in this case is the DB1 ticker. Fundamentals also include an extremely attractive business model, where the company manages over 50% gross margins and over 27% net margins, even today. The company's lack of any relevant or significant debt is yet another point firmly in its favor.

The latest set of results we have for the company is the 1H23 results - and despite a relatively negative set of valuation and share price trends, this is not at all reflected in the company earnings.

Net revenue was up 18%, and the company's cost developments, the second most important factor, are within expectations, low double-digit (10%). Company EBITDA meanwhile, is up 18% as well YoY, and these increases are driven by above-expectations profitability and revenues, key innovations, and cyclical tailwinds. The company enjoys profitability increases during rising interest rate environments, above all in securities and fund services. In addition, Q1 resulted in an increase in hedging needs, which is yet another thing Deutsche Börse has good profitability.

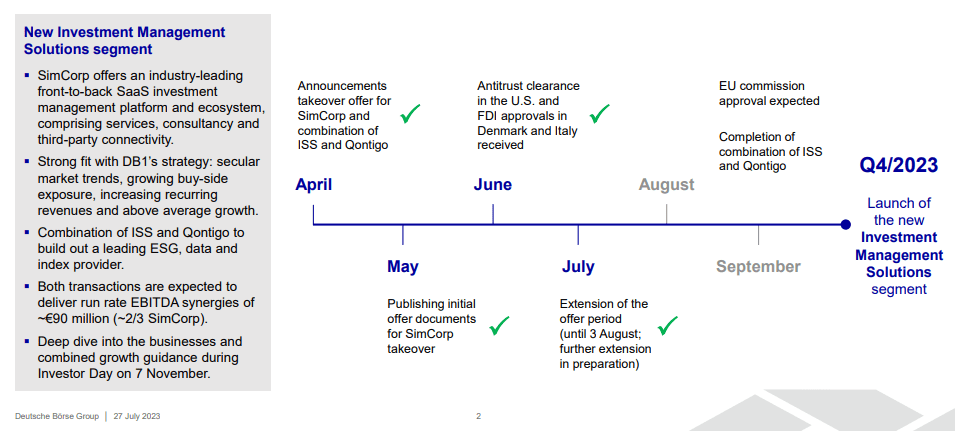

A near-full-service provider such as this company has a significant upside. The company is also in full force, developing its Investment Management Solutions segment.

2Q23 Deutsche börse (Deutsche Börse IR)

{kind=link}

As you can see, a launch for 4Q23 is likely at this point. Company Cash EPS is even better, with an increase of 19% YoY for the half-year, and 27% up for the YoY quarter. YoY on a quarterly basis, the company is seeing significant positive results, even better than on a half-year basis.

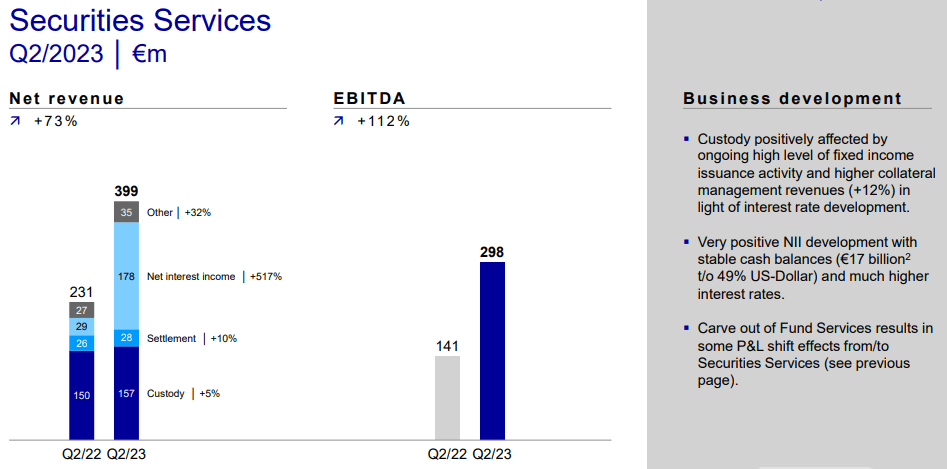

But we can look at these results on a more granular level as well. The company has a number of segments, and not all of them are positive. Trading and clearing as well as Data & analytics were both impacted and saw negative EBITDA due to commodities decline, valuation effects, and FX. Revenue was up, earnings/EBITDA not so much.

Most of the EBITDA growth for the 2Q23 quarter came from a smashing quarter in the securities services segment.

Deutsche Börse IR (Deutsche Börse IR)

{kind=link}

Also, the weakness in the various segments, if near-flat results can be called a "weakness", isn't expected to impact the company's net revenue or EBITDA levels. These are, in fact, expected to remain at a growing level which we've seen since 2019, in accordance with the following overall levels.

Deutsche Börse IR (Deutsche Börse IR)

This is in fact an increase from the previous set of guidance for the company. If you look at both revenue and EBITDA, the original target was with both those numbers being the top end of a guidance range - now the guidance is officially above the top end of that guidance range.

This is due to very positive results for the first half of the year and expectations for this to persist going into 2H23.

Let me be clear. What you and I see on the market day after day in terms of ups and downs, this is what the companies and other companies like this one live every day - they have long since found ways to ensure that regardless of the market situation, they will continue to make money.

Markets go up?

Great, Deutsche Börse makes money one way.

Markets go down?

It doesn't matter that much, Deutsche Börse still makes money from other things and other services that become more important in a downtrend market.

How could you not like a company such as this? Basically, no matter which the wind blows, making money is in the company's cards.

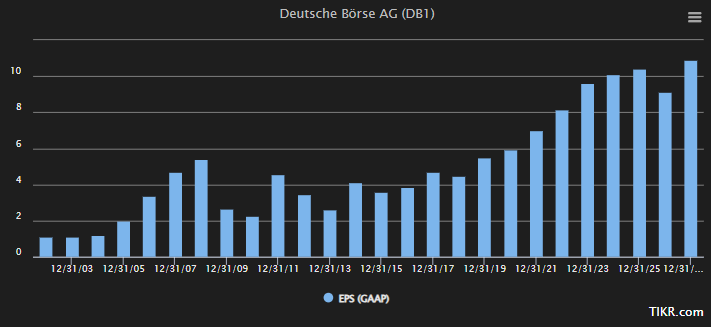

Is it completely stable in the way that some companies are? No, it's not. If you go back far enough, you can see what happens to the company during a recession, such as the GFC. For this, I like GAAP EPS as a measurement.

Deutsche Börse GAAP EPS (Tikr.com/S&P Global)

{kind=link}

Would we be wrong to expect more volatility and perhaps less growth going forward? No, I think that would be a very logical and correct expectation to have. I believe EPS growth will be more muted now that we're out of ZIRP.

However, I believe the company will come in at about the 5-year growth rate that's being implied here.

This company also has a very profitable mix of trading/clearing, services, volume costs, and analytics as well as some other incomes. Deutsche Börse adds to this with a very impressive overall set of income streams and is without a doubt, one of the cash-heaviest and least net-debt-inflicted companies I have ever reviewed.

This is a superb combination for the current environment and for, as I believe, the next few years. It's in fact a company that is "better" than many other businesses here.

Why is that?

Because the company, for one, has things like Clearstream. Clearstream, the European leading supplier of post-trading services (including things like dividend payouts), is a wholly-owned subsidiary of Deutsche Börse. The company's plans to increase the Europeanization of its operations are going well and will put it in an increased (because it is already there), almost monopoly-like position in the stock market in Europe.

The appeal of this should not be understated.

Risks? They exist. I would look at the valuation for risks here, not buying the company at too expensive multiples. Rather than the historical growth rates, I would perhaps look at growth rates about 60-70% of what we've seen historically, to be "safe" here.

However, the valuation here remains very appealing.

Deutsche Börse - Why the Valuation is Interesting

I did not call the company cheap at the time of my last article. My cost basis is well below €150/share, so even after the drop, we're well above my own buy-in price. This does not make the business unbuyable. It is in fact attractive - not just from a historical perspective, but from a forward-looking perspective.

Simply put, the company historically on a 10-year basis has been trading at a premium to a standard 15x P/E, and usually has trended at 20x P/E. The company isn't a massive dividend yielder. After an 8% decline, we're talking about a 2.2% yield - so the primary upside or appeal here, is fundamentals, valuation, and capital appreciation.

I won't call the company "cheap" here. That's reserved for when/if it goes below €150/share. My PT is still at €175, and I'm not shifting or changing it here.

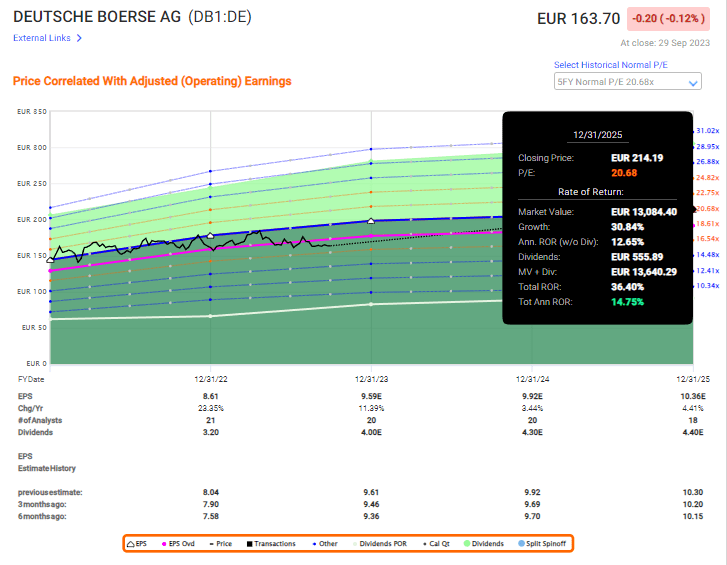

This is the first time in over 7 years that the company, for an extended or longer period of time, has traded below an 18.5x P/E - and this deserves to be highlighted.

I believe Deutsche Börse can be forecasted at a 17-21x P/E, with 21x P/E marking the 15%+ annual upside as the growth upside tapers off in 2025E (according to current expectations).

Deutsche Börse Upside (F.A.S.T Graphs)

{kind=link}

Is Deutsche Börse the best investment on the market today?

No, I'd say that isn't the case. The valuation isn't that low yet. But it may, if this decline continues, see a very interesting trend, to where a 20% annualized RoR is not only possible but conservative.

At that point, I would increase my conviction for the company. At this point, I'm still positive about the company - even moreso than before, but I would still say that other companies have a better upside. Safety is the reason to invest in this one - safety and growth, and that's why I continue allocating capital to this name.

S&P Global targets?

Still positive relative to current valuations.

We have 17 analysts following the company, with ranges from €170 to €233, so most of these are extremely forward-looking. However, most of them have moved to a hold - a full 11 now at this point, expecting the company to experience near-term pressure despite an average PT of € 193.06/share (Source: S&P Global). Literally, none of these analysts believe the company is worth as little as €160/share, and yet only 5 are at the "BUY" recommendation.

This shows a lack of and problems with analysts' convictions.

I have stock in the company. I'm adding more - albeit slowly. It's not the best opportunity out there, but it's still a solid business.

My current thesis for Deutsche Börse looks like this.

Thesis

- Deutsche Börse is a leading, European stock market operator with a compelling thesis and a very attractive portfolio. It's AA-rated and it owns some of the most significant processing assets in the European market. I view it as a timeless investment at the right price, and I bought in at below €145/share, making me a long-term shareholder.

- The company's recent targets confirm the intact margin and decent upside, and I'm shifting my target to €175 on a per-share basis, which is the highest possible I would consider paying for the native.

- As of this article, I am not shifting my conservative price target for Deutsche Börse. That means that it's still at a positive rating, albeit with an even lower upside than previously. If the 2023 Q2 report does anything to change this, I will provide an update as to that fact - but my current forecast is that it will be another beat and another report in a line of upsides for this company.

- The company is still a "BUY" here, in September of 2023.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized):

- This company is overall qualitative.

- This company is fundamentally safe/conservative and well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills 4 of my 5 criteria but cannot rightly be called "cheap".

For further details see:

Deutsche Börse: Plenty To Like About Undervalued Stock Market Companies