DBOEY - Deutsche Börse Still A Safe 'Buy' With A 15% Annualized Upside

2023-07-24 04:23:48 ET

Summary

- I've increased investment in companies like Deutsche Börse in 2023 due to its strong fundamentals and valuation despite market volatility.

- Deutsche Börse, a traditional dividend-paying stock, is considered a safe business with an AA credit rating, high profitability, and minimal debt.

- The company's diverse income streams and low net debt make it one of the "cash-heaviest" and most profitable companies in its sector.

Dear readers/followers,

There are companies I have started investing more in during 2023 as they've fallen - and honestly, my 2023 thus far has been pretty great, seeing that I am up double digits and that I am not even close to 10% invested into Nasdaq-equivalent investments or the tech sector, which frankly is what has been outperforming for much of the year.

No, if you know my work you'll know that the bulk of my investments are in traditional dividend-paying stocks from various sectors - and that's where I intend to continue putting my overall capital. Deutsche Börse ( DBOEY ) (DBOEF) is one such company, and a good example of a business I believe is going absolutely nowhere (in the sense of negative development, disappearing, or bankruptcy).

While the company previously wasn't the best-timed investment, even if it was decent in terms of timing, the real upside was in the fundamentals and the actual valuation you bought for.

I like acting on market opportunities where people are calling things "trash", essentially, and that is what I am about to show you here again.

Updating on Deutsche Börse and its upside

As any stock market operator, Deutsche Börse has correlated to the overall development and appeal of investing in the stock market. it does generate revenues and EBITDA in the billions - and at a very high margin, but it also comes with a not-inconsiderable amount of inherent volatility.

The company is an incredibly safe overall business. It has an AA credit rating , and its subsidiary has an AA credit rating. The stock trades under the native DB1 ticker and scores a very high combined profitability, fundamentals, and valuation score. It has no debt worth noting, it has 52.75% gross margins, over 40% operating margins, and over 28% net margins.

From this perspective, and given the various costs and OpEx numbers here, this business is one of the most profitable companies in this entire sector.

Deutsche Börse Revenue/Net (GuruFocus)

{kind=link}

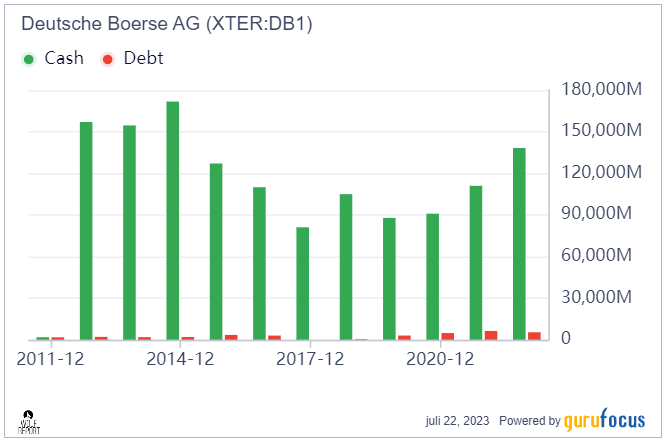

As you can see, the company also has a very profitable mix of trading/clearing, services, volume costs, and analytics as well as some other incomes. The company has thoroughly impressive overall income streams and is without a doubt, one of the cash-heaviest and least net-debt-inflicted companies I have ever reviewed.

Deutsche Börse cash/debt (GuruFocus)

{kind=link}

Deutsche börse has multiple other respects where I view it as being "better" or superior to other stock market-based investments/operators. The perception I want you to have when considering the company though is that this is a very profitable and very low-leveraged stock market operator, that owns some of the core technologies needed in Europe. This includes services like Clearstream. Clearstream, the European leading supplier of post-trading services (including things like dividend payouts), is a wholly-owned subsidiary of Deutsche Börse.

The company's past aim has been increasing the Europeanization of its operations, divesting non-core services in the USA and other parts of the world while adding European operations or M&As, including things like Axios.

Deutsche Börse is in an essentially monopoly-like position in the segment. It does not matter as much if services like FlatexDEGIRO compete with Deutsche Börse in some respects, because the former also needs post-trading services, which is what Deutsche Börse can be said to actually focus upon. Because of this, its appeal is high regardless of what some of its peers do in trading/brokerage operations.

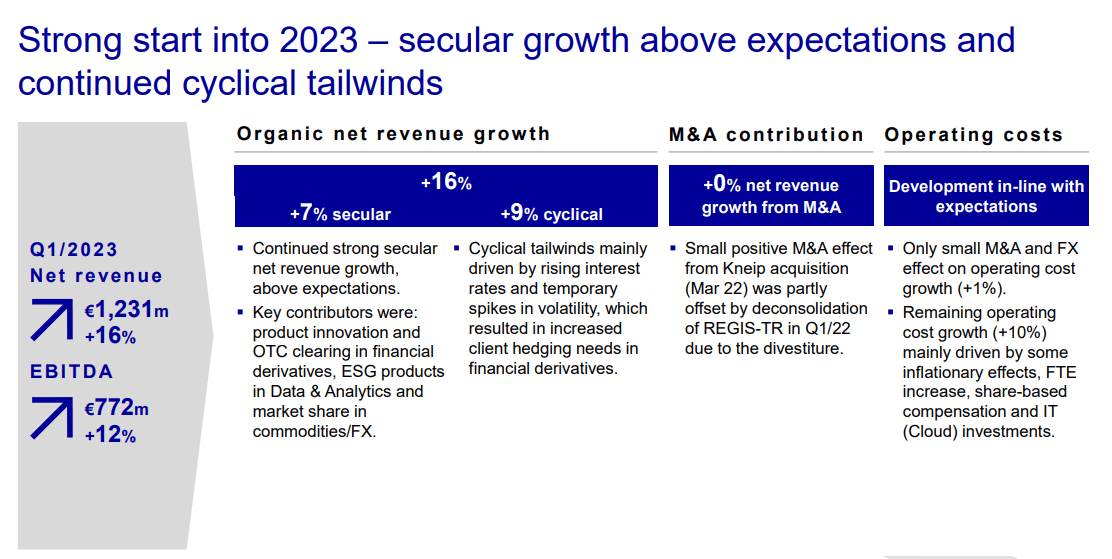

The latest results were positive in nature. Revenue grew by more than 15% YoY, and EBITDA grew double digits by 12% to a quarterly EBITDA of almost €775M, with a net profit of over €470M, up 12% as well. The company updated its guidance in conjunction with this report as it represents a very strong set of results, now expecting the 2023E results to be close to the higher end of its 2023E guidance range. It's even possible for the company to exceed this, provided that the cyclical tailwinds in some of these areas continue.

Why is this the case, given that the overall volatility of the market certainly has increased?

{kind=link}

Well, Deutsche Börse has a fairly large portion of net interest income in its finance business. With derivative trading activity high, net interest income is higher - and trading volumes haven't yet cycled down either, another positive.

The overall insolvency crisis and banking headwinds in the US and Swiss sphere did have some impact in the form of uncertainty. But as with many other things in finance, this drove an increased activity towards hedging , which in turn acts as income for the company as well. Deutsche Börse makes money both on the down and on the upside. In this case, these incomes are found in the Trading & Clearing segment.

Operating costs were also up significantly, at 11% YoY. This is due to a mix of inflation, an overall larger workforce, increased IT investments, increased pricing for investments, and other price increases - including in projects like cloud computing.

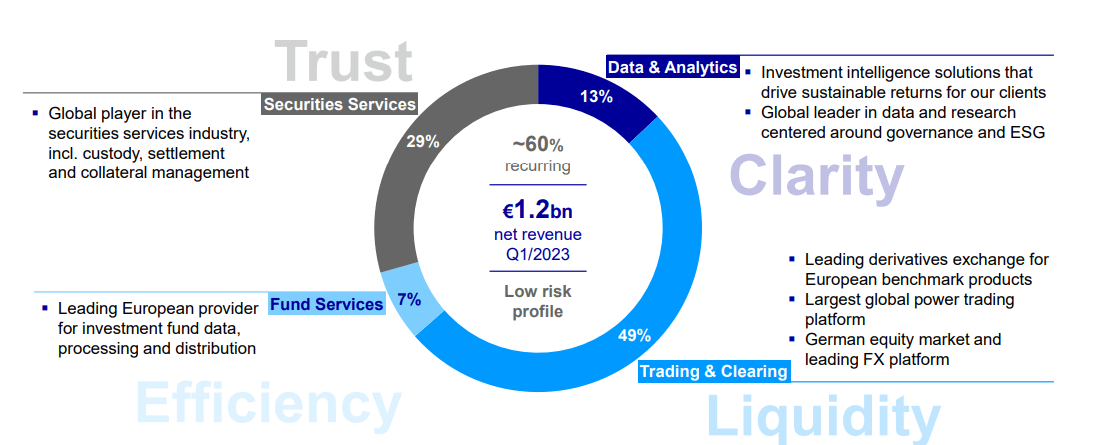

The company's current mix as of May 2023 is a very attractive one.

{kind=link}

The company has a very low-risk business model, reflected by its AA credit rating, which sees an upside/potential for great profit during both declines and upsides in the market.

Deutsche Börse has a high payout - 40-60% of net profit, and that payout ratio is steadily declining with increasing profits, with the remains of net profit reinvested into growth/M&A.

Unlike banks and insurance businesses, Deutsche Börse has a very low capital requirement, mainly operational risks in the banking units. Furthermore, all of these areas you see above are scaleable, with trading/clearing being perhaps the most scaleable of all.

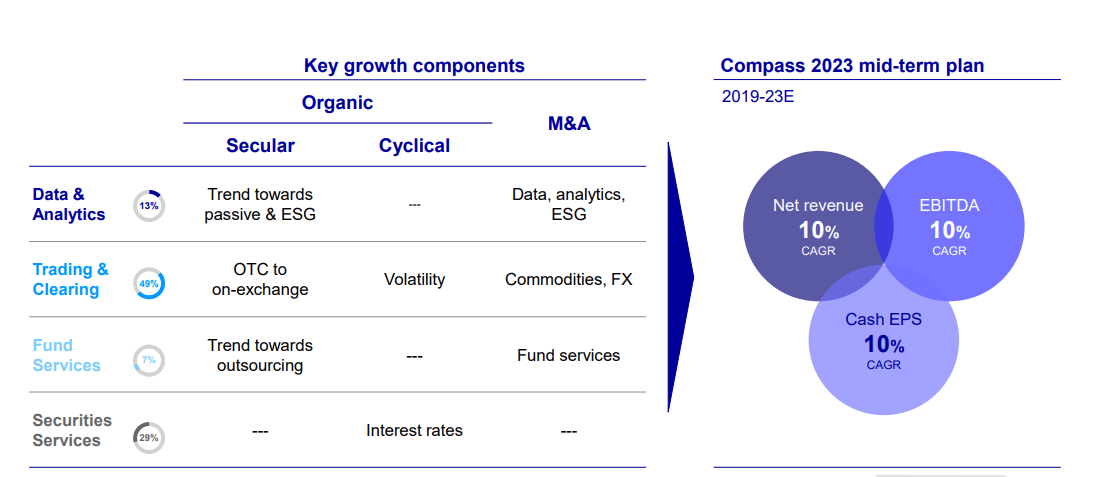

The company has the fundamentals to grow double digits on an annual basis - both in net revenue, in EBITDA and in cash EPS.

{kind=link}

Its superior execution can be confirmed based on the financial targets being reached 9 months in advance. The combination of secular growth and cyclical tailwinds is what delivers the double-digit upside here (cyclical tailwinds being the reversal of low-interest rate, low volatility). Remember, some business models want high volatility and high-interest rates in order to see their full potential. Deutsche Börse is not the only example of this, but it's one example that should not be underestimated.

The fact that Brexit has actually gone through is another fundamental advantage for Deutsche. Given London's previous importance as a financial gateway (and yes, I've heard the arguments for why it won't change), business is likely to shift financial weighting to Frankfurt above London in the long term - and this has in fact happened. More than 60 financial institutions have applied and set up in Frankfurt since Brexit, and 30 of these have made Frankfurt their main EU hub, including four out of the six biggest US banks, and four out of the biggest six Japanese banks ( Source ). Again, Deutsche is a winner of these trends, and I expect these trends to continue.

What I can say though is that Deutsche Börse investors are "winners" on the market.

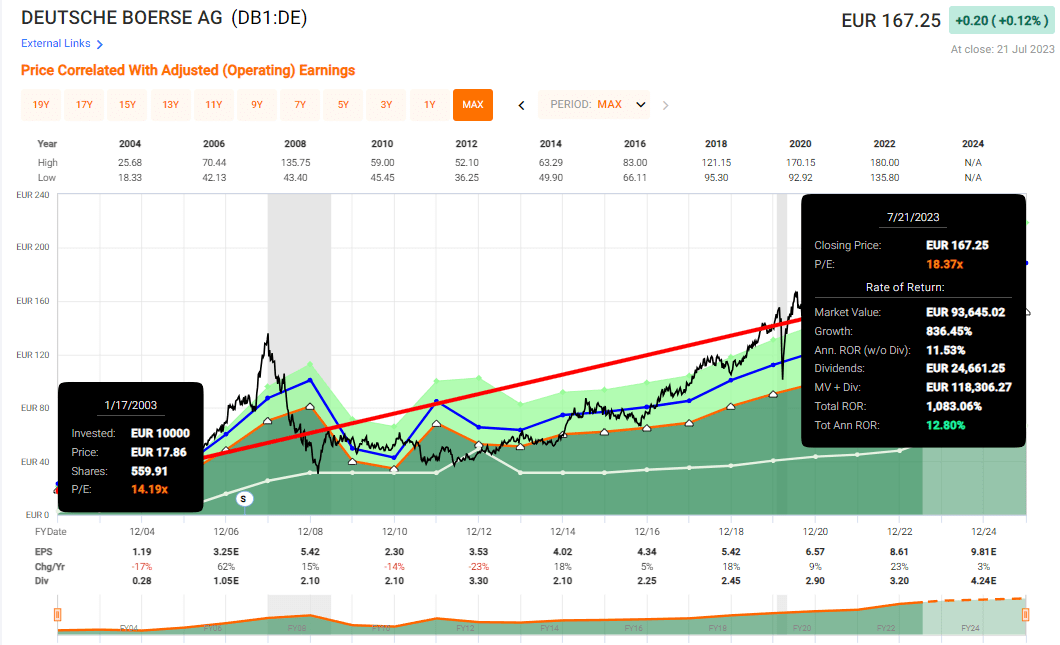

Deutsche Börse RoR (F.A.S.T graphs)

{kind=link}

Is Deutsche Börse the cheapest financial on the market? No, it certainly isn't. Is it the highest-yielding? No, not that either.

Is it a quality AA-rated company with an upside worth considering if you're in the market for safety?

It absolutely is.

Let me show you the valuation and what you may expect from the company on a forward basis.

Deutsche Börse - Plenty to like even at this valuation

The company has the somewhat unfortunate tendency to trade at a relatively high premium, with a relatively low yield in the finance sector, a sector that usually gives us a very decent amount of yield - usually under 3.5% isn't even interesting to me here.

But for DB1, it's somewhat different.

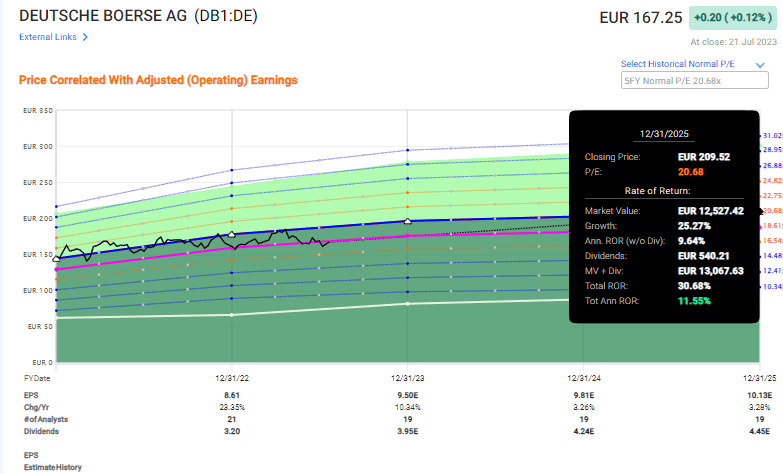

At a 5-10% forward growth rate, I consider an 18-20x P/E to be valid for this business. Even though the company currently trading at around 18x, I see a double-digit upside potential at somewhat above 20x, given the credit rating, the market position/moat, and other fundamentals here.

Remember, I own a fair share of Deutsche Börse in my portfolio. However, I bought it significantly cheaper than it is today. There's still a slight upside to my price target, but it's no longer the "sort" of double digits it once was. It's the fact that the growth rate is still a very favorable and positive one.

I said in my previous article that an equity value on a per-share basis for DB1 is around €185-€200/share - and I stand by this estimate, despite an underperformance relative to most indexes since my last article.

Here is the upside I still see for Deutsche Börse at this time.

Deutsche börse Upside (F.A.S.T graphs)

{kind=link}

S&P Global analysts tend to be favorable towards this company as well. While they don't see my upper range target of €200/share, the 17 analysts following Deutsche börse give the company an average of €170 to €207, with an average of €192, which gives us a 14.4% upside at a share price of €167.25. 8 out of those 17 have a "BUY" rating or equivalent here, with 10 at "HOLD", which doesn't really match the overall average PT or rating.

I believe these analysts are underestimating this company's conservative upside, as well as the company's well-above-average fundamentals.

Deutsche Börse won't make you rich. It can't really double your money within the next 2-3 years - in fact, I'd wager money on that fact that it cannot. But it can take your money and give you what I see as a conservative upside while paying you a decent interest rate for your money until that time.

Not every company can do this as safely as Deutsche Börse can, and for that reason, the following is my thesis for the company at this time.

The company is set to report 2Q23 shortly. My expectation for 2Q, given what we've seen since March, is a continuation of the positive trend that we've seen at the beginning of 2023 - because the positive underlying trends have only continued since 1Q23. Analysts following the company, including me, are expecting company EBITDA to rise double digits this year - this would entail high single-digit growth in all of the quarters. If the set of earnings in 2Q brings about any surprises or changes, I'll provide an edit on this article that reflects this.

For now, here's my current thesis.

Thesis

- Deutsche Börse is a leading, European stock market operator with a compelling thesis and a very attractive portfolio. It's AA-rated and it owns some of the most significant processing assets in the European market. I view it as a timeless investment at the right price, and I bought in at below €145/share, making me a long-term shareholder.

- The company's recent targets confirm the intact margin and decent upside, and I'm shifting my target to €175 on a per-share basis, which is the highest possible I would consider paying for the native.

- As of this article, I am not shifting my conservative price target for Deutsche Börse. That means that it's still at a positive rating, albeit with an even lower upside than previously. If the 2023 Q2 report does anything to change this, I will provide an update as to that fact - but my current forecast is that it will be another beat and another report in a line of upsides for this company.

- The company is a "Buy".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized):

- This company is overall qualitative.

- This company is fundamentally safe/conservative and well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills 4 of my 5 criteria but cannot rightly be called "cheap".

For further details see:

Deutsche Börse Still A Safe 'Buy' With A 15% Annualized Upside