DBOEY - Deutsche Börse: Stock Has Outperformed Time For More

Summary

- I wrote about Deutsche Börse this year, even before Russia invaded Ukraine, and the investment has paid off in the form of market outperformance of 15%.

- There are reasons for this - even if this company is volatile, and I'll show you these reasons.

- I believe the company warrants a continued "Buy" here, and I believe it could be a solid component of your portfolio.

Dear Readers,

At times, I make decent picks even in timing. While Deutsche Börse ( DBOEY ) ( DBOEF ) wasn't the best-timed investment, even if it was decent in terms of timing, the real upside was in the fundamentals and the actual valuation you bought for. In this article, I'll get into Deutsche Börse again and show you why my portfolio has outperformed. Not just because of this company - but because of investments like this company.

Picking cheap, qualitative businesses at great valuation, when everyone else is calling them "trash" - there are far worse ways to go about investing, let me assure you.

Let's look at what we have here.

Deutsche Börse - The Thesis

A quick revisiting of the company first - it's been a while since we wrote about it, after all.

Deutsche Börse is a stock market operator. What it does is operate, as this suggests, the stock market. The business has revenues in the billions, operates at appealing EBITDA/operating margins of around 53-55% on an EBITDA basis, and unlike some of its peers, pays a dividend of over 2% at the current valuation.

The company has an AA credit rating , and its subsidiary has an AA credit rating. Some actually claim that Deutsche Börse goes back over 400 years to 1585, but the clear roots are the "Frankfurter Wertpapierbörse AG", which was a German LLC that changed its name in late 1992.

Its IPO is relatively fresh compared to that. It only went public back in 2001, and its argument was very simple - we offer digital/electronic trading. This eventually went on to almost replace floor trading, and it was known as Xetra back in 1997 - a name that still sticks today. You've probably heard of Xetra - that's that.

Deutsche Börse also has things within its portfolio that you might not know you're in contact with, but that you should be aware of. Things like Clearstream. This one is big. It's the leading European supplier of post-trading services (including things like dividend payouts) and is a wholly-owned subsidiary of Deutsche Börse. Its mission is to ensure effective cash and security delivery between parties and it manages/administers and keeps safe all of the securities it holds on behalf of its investor customers. So, that is also part of Deutsche Börse. This is also the subsidiary that I was referring to, with AA credit from S&P Global.

This combination of services gives it a distinct advantage over most of its competitors because its offerings are broad enough to cover the entire process chain. This means that European banks are customers of Deutsche Börse, as many of their operations for investors are routed through Deutsche.

This is obviously an attractive position to be in.

How does a company like this grow and expand, given its name implying a heavy German-focus?

Well, it can do so in one of several ways - market expansion to other countries, or service expansion to ancillary sectors.

Deutsche Börse does both.

The company's focus has been the "Europeanization" of its operations. It sold the US subsidiary ISE to Nasdaq ( NDAQ ) and its stake in BATS Global back in 2016 and 2017, respectively. It's done a few M&As, such as Axioma, a risk management software provider which was spun into its index (DAX/STOXX) operations back in 2019.

Today, the company makes money through the following segments:

- Eurex (Financial Derivatives)

- Clearstream (Post-trading)

- Xetra (Cash Equities)

- IFS (Investment Fund Servicing)

- IIS (Institutional Services)

- 360T (Foreign Exchange)

- EEX (Commodities Trading)

- Qontigo (Index/Analytics)

Most of the company's annual revenues still come from the Eurex and Clearstream segments - those two together are more than 50% of sales. This sort of company, because of this, makes money from pre- and post-trading services, as well as from trading/clearing itself.

Deutsche Börse IR (Deutsche Börse IR)

{kind=link}

A stock market operator such as Deutsche sits in an essential monopoly position, given that order flows go where liquidity is most prevalent. While low-cost trading platforms do compete with Deutsche, they also require post-trading services and other technologies, all of which Deutsche provides. Monopolies are very attractive overall investments because they're...well, they're monopolies. Deutsche Börse isn't going anywhere, and the fact that we're through Brexit now makes this even more attractive because it increases the importance of non-London markets like Amsterdam, Paris, Berlin, Brussels, and other exchanges.

The company has averaged impressive revenue growth over time with around 6-8% on average, and sometimes in the double digits. Companies like this operate with extremely high margins of 82-93% gross, and as high as 50% pre-tax.

Recent results mostly confirm the positives of this operator. A monopoly means just that - Deutsche Börse can simply increase pricing where necessary to offset most pressures it may be experiencing. Despite market pressures, the company sees organic net revenue growth and double-digit EBITDA growth. Operating costs are up, but income and revenues are up more.

Deutsche Börse IR (Deutsche Börse IR)

{kind=link}

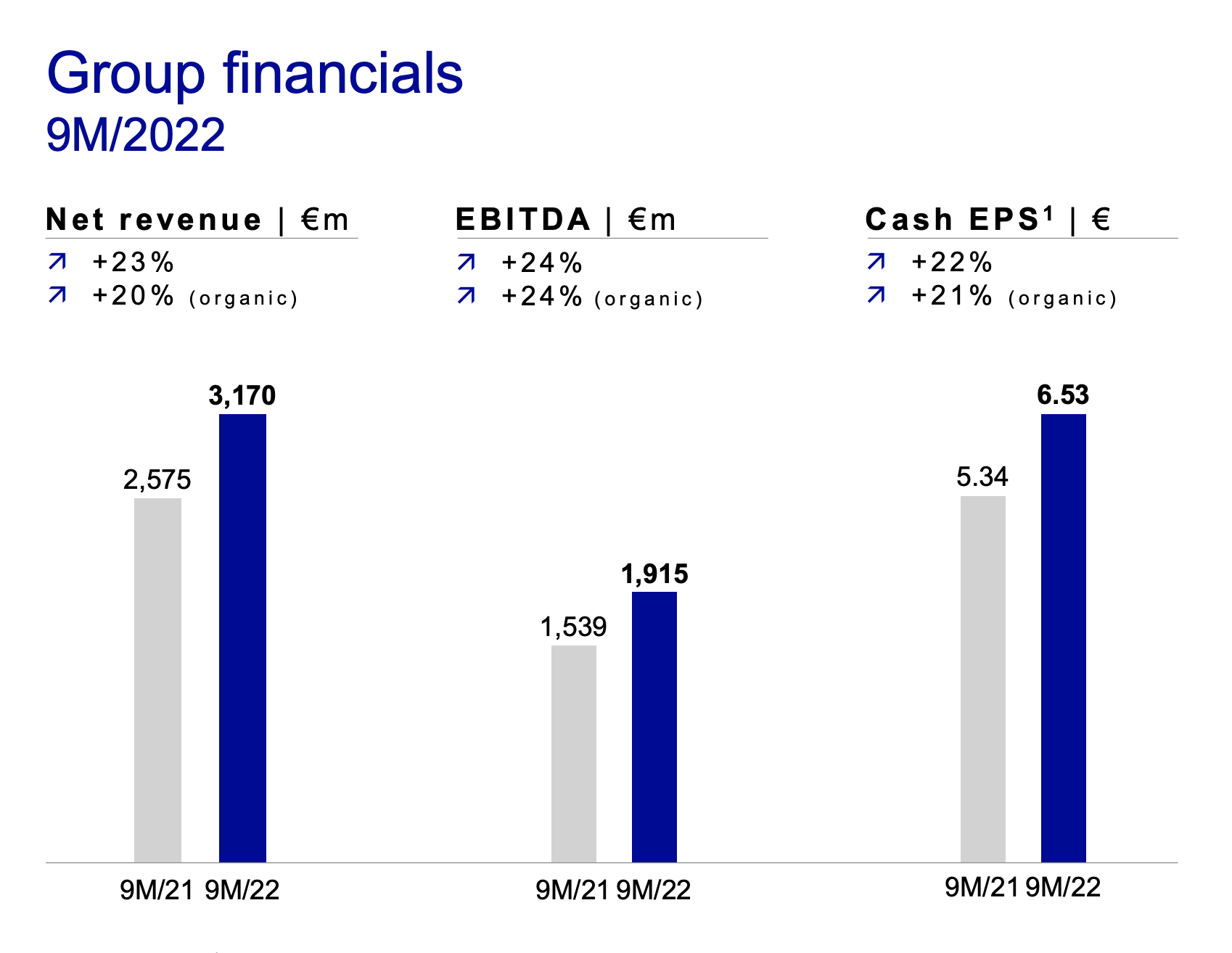

The company also, despite ongoing market pressures, increased its outlook for the year due to tailwinds - one of the few companies in fact experiencing tailwinds here, with EBITDA of over €2.3B on an annual basis. Here are the improvements YoY for the 9M22 period.

Deutsche Börse IR (Deutsche Börse IR)

{kind=link}

Costs are of course up, driven both by increases in things like ISS, but also FX - but positives are simply far higher and better than any sort of input increases here. I also expect these positives to continue for the foreseeable future. The only thing that I as a shareholder hope for is that the company abandons its ventures into the crypto space - but this is so small of a segment that it really doesn't matter in the bigger picture.

Deutsche Börse EPS forecast (TIKR.com)

{kind=link}

The company's current yield is around 2.4-2.5% which is good. Current estimates are for continued GAAP increases until 2024, and stabilization/slight normalization until then. This should be enough to guarantee that the company continues its stable, growing trajectory until then and that shareholders are well-protected here.

Deutsche Börse - The Valuation

The company valuation remains appealing despite significant price improvements since my last article. The average valuation target from S&P Global comes to around €193/share, which implies a nearly 12% upside from today's share price with 13 out of 19 analysts giving the company one or another bullish/"Buy" rating.

I own Deutsche - but I bought it significantly cheaper than it is today. There's still a slight upside to my price target, but it's no longer the double digits it once was - at least that's what I thought until I looked at it, and included the new forecasts and the new reality for this company. Deutsche has been able to retain its growth and margins without any issues despite the complex environment. This calls for a price target improvement for my thesis here.

Still, I forecast Deutsche Börse at no more than a sub-GDP lower range growth rate, up to slightly above GDP of around 1.8-2.1% for the terminal period, with around 4-6% range for the 2021-2025 period. The company has a WACC of around 7.72%, reflecting high expectations for its equity growth. Again, risks for this company are very low - but they do exist in the form of "less growth" than expected. If this happens, you might maintain your capital, but you'll have missed out on opportunity growth.

Based on these relatively conservative growth range estimates, the implied equity value on a per-share basis for Deutsche comes in between €185-€200, a significant improvement over the last DCF analysis I did. The company has advantages in the form of its market size, returns and margins, better coverage than any of its closest peers, and its future growth plans.

I continue to call for a significant upside to Deutsche Börse here - even if that upside isn't as massive as some investors might want.

But what you get when you invest in Deutsche, like with some other of my investments, is safety. There is significant safety to be had here.

I would argue that we're at the apex of what I would consider an acceptable valuation for investing in the company here. There is still an upside to be had, but I would suggest that only investors that truly want the safety this company offers and are willing to accept the lower yield, and the potential for only low-double-digit returns, do invest here.

The realistic upside to a 22-23x P/E, which is where I consider the company's DBOEY ADR to be justified, is around 8-10%, which is the lowest acceptable RoR I'm willing to accept for an investment.

For that reason, I'm still positive - but if the company were to climb up to say €175/share, that's when I would cut my recommendation to "Hold".

For that reason, here is my current thesis on Deutsche Börse.

Thesis

- Deutsche Börse is a leading, European stock market operator with a compelling thesis and a very attractive portfolio. It's AA-rated and it owns some of the most significant processing assets in the European market. I view it as a timeless investment at the right price, and I bought in at below €145/share, making me a long-term shareholder.

- The company's recent targets confirm the intact margin and decent upside, and I'm shifting my target to €175 on a per share basis, which is the highest possible I would consider paying for the native.

- The company is a "Buy", but barely here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized):

- This company is overall qualitative.

- This company is fundamentally safe/conservative and well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills 4 of my 5 criteria but cannot rightly be called "cheap".

For further details see:

Deutsche Börse: Stock Has Outperformed, Time For More