UBS - Deutsche Bank $42 Trillion Derivatives Book: A Snowflake Away From Financial Meltdown?

2023-03-26 22:50:40 ET

Summary

- Investors are fearful Deutsche Bank is the next domino to fall.

- DB is a picture of rude health coming into this banking crisis.

- Some point to worries around its EUR42 trillion derivatives book.

- I believe the fears over the derivatives exposures are way overblown.

- However, loss of confidence may trigger a self-fulfilling prophecy.

Deutsche Bank's ( DB ) share price has fallen sharply in the last trading sessions as financial contagion fears continued in the wake of the collapse of Credit Suisse ( CS ). There is clearly a lot of nervousness in the market and it seems that no one is really sure what is driving the fears surrounding Deutsche Bank specifically. Some attribute this to its legacy reputation as the sick bank of Europe; others are worried about concerns around its Commercial Real Estate portfolio in the United States.

Bloomberg reports that Autonomous Research cited DB's large notional derivative book currently at EUR42 trillion as a key concern for investors.

As far as I know, DB is in a very healthy state, and on the face of it, these concerns are misplaced. This is very different from the death tailspin CS found itself in after slow death by a thousand cuts over many years.

The risk, however, is that the unsubstantiated fears around DB become a self-fulfilling prophecy that could drive up its cost of funds in the Investment Bank. As a result of this, I took steps to manage the risk in my position even though I remain bullish when it comes to DB stock.

In this article, however, I would like to focus on the fears surrounding its large derivative book and why the concerns are way overblown in this instance.

DB Derivative Book

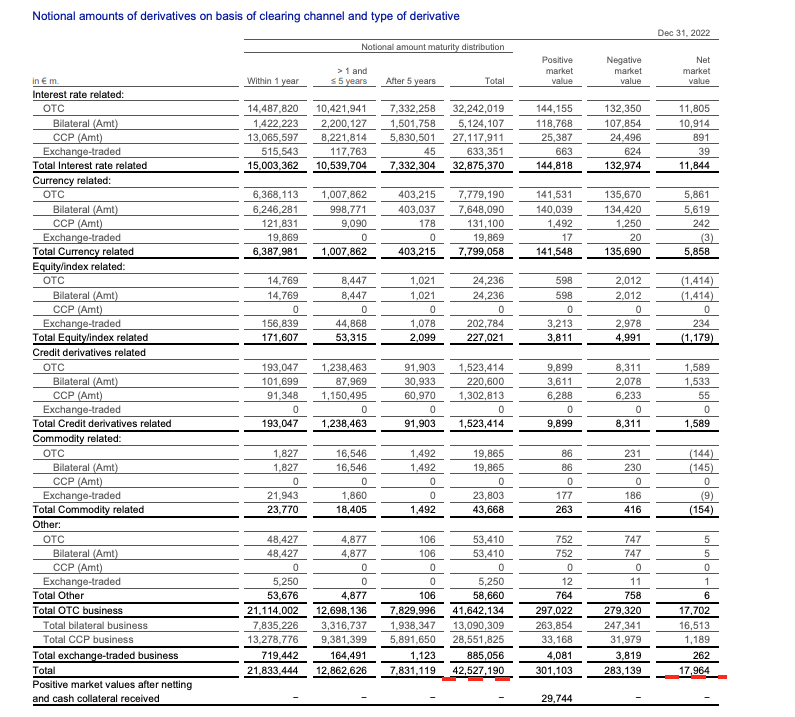

DB discloses the details of its derivative book.

{kind=link}

As you can see, the total notional derivative exposure of DB is a staggering EUR42 trillion. This is what some investors are concerned about, surely, DB is a snowflake away from a financial meltdown, right?

Well, not quite.

To start with the reported number is a notional amount of the derivative contract as opposed to actual exposure. This is best explained as an example.

Say one of DB's large corporate clients is requiring an interest rate swap ("IRS") to protect themselves from rising interest rates on a $1 billion loan. The IRS terms reflect a swap of say LIBOR +100 basis points to a fixed rate of 6%. In such a scenario, DB would be purchasing an identical $1 billion IRS from another banking counterparty (say, JPMorgan).

So from DB's perspective, it likely earned a margin or fee on the transaction. It has no interest rate exposure or market risk either as it is fully hedged. However, for the purpose of calculating its gross derivative exposures (towards the 42 trillion figure), it would count as a $2 billion notional exposure.

This is the key reason why these notional derivatives exposures are so large. These are just notional contract figures and nowhere near the actual exposure. Furthermore, DB carefully manages its book which is mostly hedged for market risk (as well as counterparty risk).

On an overall portfolio basis, DB would not be 100% hedged of course. This could be due to other unrelated positions (for example, hedging its liquidity securities portfolio). As of 31st December, DB has total positive marks of EUR301 billion and total negative marks of EUR283 billion and therefore a total gain of ~EUR18 billion on its derivatives portfolio as of 31st December 2022.

Okay, so now we are clear that DB's market risk is predominantly hedged as described above - but what about counterparty default risk?

Counterparty Default Risk

The obvious next question is what happens if a large counterparty such as Credit Suisse or JPMorgan ( JPM ) defaults?

Firstly, it is important to note that any derivatives that are exchange-traded or cleared by a central party do not pose credit risks. However, as can be seen from above, most of DB's derivatives exposures are Over-The-Counter ("OTC") derivatives and therefore exposed to counterparty default risk.

As such, the industry practice is to enter contracts based on master agreements for derivatives such as the International Swaps and Derivatives Association , Inc. ("ISDA") master agreement. The master agreement allows for close-out nettings of all rights and obligations with a counterparty upon the counterparty's default.

So as an example, if a counterparty (such as CS) defaults then all outstanding derivatives contracts with that counterparty are settled on a net basis on the default date. As such, banks like DB monitor specific counterparty risks daily and ensure that their total exposure (netting) to a particular counterparty is within predefined risk limits. This is a key reason why counterparties reduced their trading with CS prior to its being acquired by UBS ( UBS ) which contributed to its downfall.

Another common way for banks to reduce their counterparty risk is to enter into what is known as credit support annexes (CSAs) to master agreements. These are effectively a form of margin calls and require the counterparty to post collateral when there is an unrealized loss beyond a certain level.

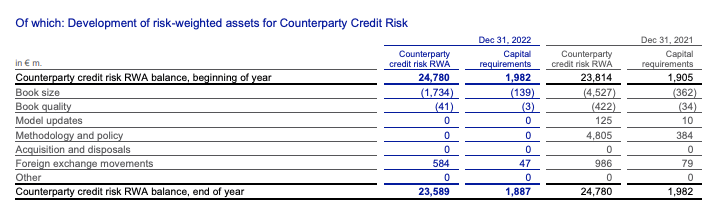

The impact of nettings and collateral posted under ISDA is incorporated in the RWAs and capital allocated for counterparty risk across the bank as can be seen from the below disclosure in the 2022 annual report:

{kind=link}

So in summary, both market and counterparty risks arising from DB are well managed and an appropriate amount of capital is allocated for any residual risks.

Final Thoughts

Investors in banks are clearly very nervous given the crisis of confidence in the U.S. and European banking markets in recent weeks. In the wake of the collapse of CS, investors are looking for the next domino piece to fall. Given its chequered history and past reputation for being the sick bank of Europe, the focus has now quite naturally switched to DB. Mr. Market is shooting first and then asking questions. The risk remains, of course, that this becomes a self-fulfilling prophecy even though DB appears to be a picture of rude health coming into this crisis.

The EUR42 trillion derivative book notional exposure is certainly a very large number that perhaps scares some investors. My conclusion is clear, the actual market and/or counterparty risks are very limited and strictly managed. In my view, the risk of the derivatives book imploding is very low.

However, out of an abundance of caution, I have managed my risk exposure to DB stock in the short term. Although, I intend to put back the risk position once I am clear that the self-fulfilling prophecy scenario is unlikely to play out.

For further details see:

Deutsche Bank $42 Trillion Derivatives Book: A Snowflake Away From Financial Meltdown?