XLF - Deutsche Bank: Buckle Up For Trifecta Of Tailwinds

Summary

- DB has risen more than 50% in the last 6 months.

- Even so, it is still very cheap trading at only 0.45x tangible book value.

- There is a trifecta of tailwinds in play.

- Expect a very strong Q4 earnings report.

Many investors believe that European banks are simply uninvestable. In fact, in the last decade or so, it was clearly a widow-maker trade with some short-lived false rallies along the way. Deutsche Bank ( DB ) has rightly earned its reputation as the "sick bank of Europe". Many investors are still beholden to recency bias and are failing to recognize that this time it is truly different.

Deutsche Bank is a self-help story as its current management team executed brilliantly in its strategic transformation and appears like it is on track to meet its RoTCE return of 8% for 2022. However, DB has also benefited from a positive market and macro environment that plays very well to its business mix. These macro tailwinds are picking up strength in recent weeks and thus I believe that DB is set to outperform in 2023.

The DB share price has been on an absolute tear in the last 6 months as can be seen from the below chart:

As can be seen, it has outperformed the Financial Select Sector SPDR ETF ( XLF ) by a factor of 5x in the last 6 months. Still, it is only trading at 0.45x tangible book value and is anticipated to generate >10% RoTCE by 2025 (I believe it will get there considerably earlier powered by higher interest rates).

Tailwind 1: Interest Rates

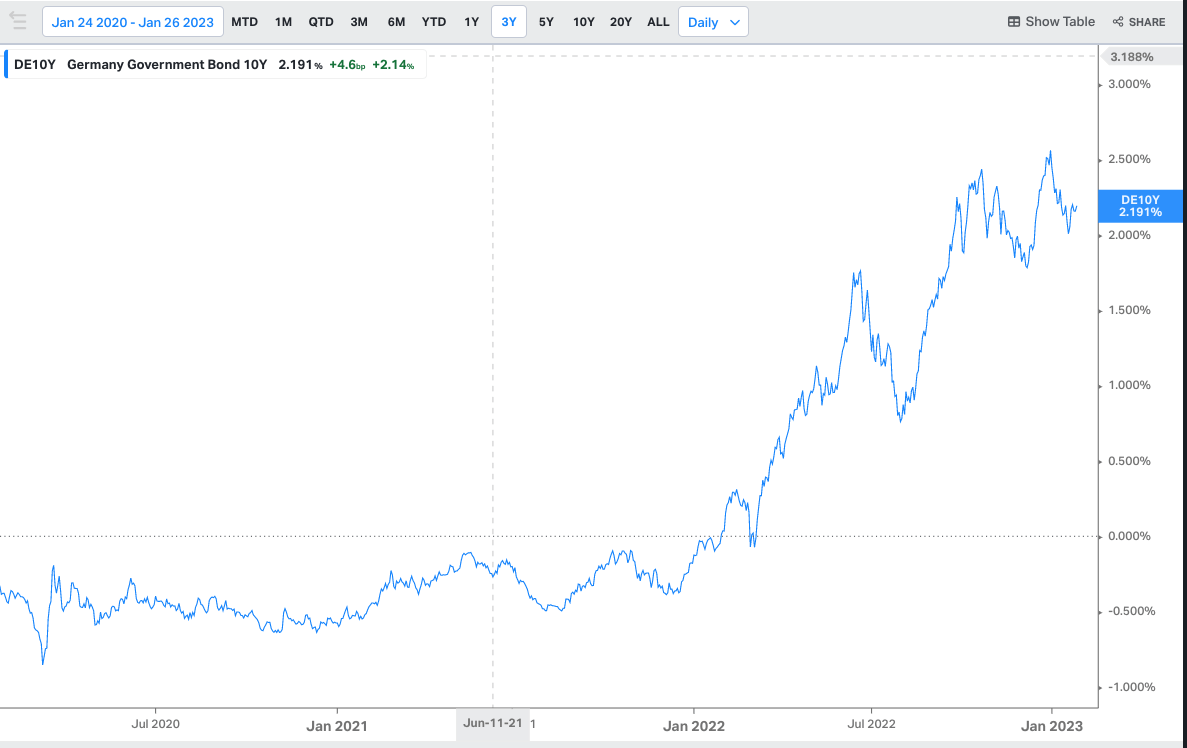

Many investors completely underestimate the recent paradigm shift in the interest rate environment in the eurozone. A year ago, the euro overnight rate was deeply negative whereas now it is expected to exceed 3% in 2023. The 10-year bund yield over the last 3 years is absolutely astounding:

{kind=link}

So both short and long rates have gone up massively within the last 12 months and are expected to remain so for longer. The ECB has grown even more hawkish since December and is telegraphing an additional 50 basis point rate hike next week as well as in the March meeting.

Rising rates (especially on the short end) are an absolute bonanza for a bank like DB. All of a sudden, DB's deposit franchise is worth significantly more than anyone could have envisioned 12 months ago.

In my last article on DB, I highlighted the likely benefits based on the then-current yield curve:

The latest update from DB on the impact of rates was provided at the UBS European conference several weeks ago:

"The guidance we gave a couple of weeks ago was that relative to 2022, interest rates alone should support revenues by about 2 billion euros. And then that would be offset by something in the high single digits, hundred millions of euros by the year-on-year impact of no TLTRO, higher funding costs, and some of the benefits we had this year, for example, debt repurchases and so on. So the net of those things should give us something between say 1.1, 1.2 billion euros of revenues next year relative to this year"

Since then, rates expectations have clearly moved higher and the net benefit for 2023 should be much higher. By 2025, the further upside from rates should play out fully and benefit the revenue line by as much as $3 billion. Clearly, this is exceptionally material given DB's current market cap of only ~EUR24 billion.

Tailwind 2: FICC Is Exceptionally Strong

DB's investment bank is predominantly comprised of FICC trading. DB has benefited strongly in recent years from the secular resurgence of FICC trading volumes and expanding margins. The strong FICC trading wallet has finally profited from rising rates, investors' repositioning of portfolios, and the removal of financial suppression by central banks. DB has been a major beneficiary as it doubled down on investments in this area and also from the fact that numerous counterparties are looking to diversify away from U.S. money center banks. Additionally, given the success of DB's strategic transformation, in recent years DB's CDS spreads and cost of funds normalized in line with peers and thus no longer have a competitive handicap.

Based on the read across from the U.S. banks, I expect DB to deliver a very strong Q4'2023. Citigroup ( C ), JPMorgan ( JPM ), Goldman Sachs ( GS ), Morgan Stanley ( MS ), and Bank of America ( BAC ) all delivered very strong year-on-year growth in FICC trading income (between ~10% to 50% growth with BAC and GS delivering the best performance in the mid to high 40% growth year-on-year). JPM and Citi pulled reduced RWA allocated to trading books given the capital constraints they are facing due to the Fed's CCAR stress tests.

I fully expect DB to outperform this quarter and deliver exceptionally strong results in FICC trading. The read across from the U.S. banks is a strong bullish signal.

Tailwind 3: The Eurozone May Avoid A Recession

One of the key concerns for DB coming into 2023 was the expected deep recession in the eurozone driven by high energy prices. This could have manifested in outsized credit losses in 2023 and beyond. It looks like Germany and the eurozone have caught a lucky break in the form of warm weather as energy prices ease following the initial shock of the energy crisis triggered by the Ukraine war.

The German government is now forecasting that the economy will avoid a recession and projects GDP to increase by 0.2% compared with a 0.4% decline forecast in the autumn. Inflation in 2023 is also seen to ease from the prior forecast of 7% to the current 6%.

This is likely to mean that DB will benefit from lower loan losses in 2023 than previously contemplated. This is another strong bullish signal for the stock.

Final Thoughts

DB is targeting a RoTCE of >10% by 2025. Given the trifecta of tailwinds highlighted in this article, I expect it to have a good chance of meeting this target earlier. The stock is trading at only 0.45x tangible book and with a very conservative loan book (very limited exposure to unsecured personal credit).

Whilst the stock has run up by over 50% in the last 6 months, given its still distressed valuation, the stock has a long runway ahead.

DB is my #1 pick in the European banking space and I remain very bullish.

For further details see:

Deutsche Bank: Buckle Up For Trifecta Of Tailwinds