DB - Deutsche Bank: It's The Interest Rates Stupid

Summary

- Deutsche Bank does not deserve to be trading at 0.3x tangible book.

- Interest rates are a huge tailwind.

- Credit risks are overblown.

- DB has a credible path to its 2025 target in spite of the deep recession in the Eurozone.

- It is all 'bout interest rates, stupid!

The phrase "it's the economy, stupid!" became the de facto slogan for Bill Clinton's 1992 successful election campaign. The intention was to deliver a simple message that the economy trumps everything else. Bill Clinton 'got' it and laughed all the way to the White House. In 1992, it was so obvious that the election was all about the economy but George Bush simply didn't get it, even though it was plain to see.

I believe that investors are making the same mistake now with certain European banks. Call it recency bias or perhaps investors are fighting the last war.

There is a paradigm shift in the interest rates environment globally. Specifically, for the Eurozone, in the last 5 years or so banks were operating in a negative rate environment. It is exceptionally challenging for banks to earn their cost of capital when they deposit 100 euros with the ECB and only receive back 99.5 on maturity. It completely disrupts the maturity transformation business model of deposit-taking institutions. Consequently, most European banks were trading at a fraction of tangible books (net tangible assets) whereas the U.S. banks thrived relatively speaking.

Guess what happened in 2022?

This all changed and the ECB is embarking on a strong tightening path with Euro rates are expected to reach ~2% or higher. The 10-year Bund is now trading at ~2.2%.

Deutsche Bank ( DB ) is aiming for an ROTCE of 8% in 2022 and greater than 10% by 2025. For context, DB is currently trading at ~0.3x tangible book value. If it is able to meet its 2025 target, then the share price may triple.

Obviously, the macro environment has deteriorated in the eurozone due to the Russia-Ukraine war and the gas situation. Even Deutsche Bank is forecasting that the eurozone is likely to be in a deep recession. Naturally, investors are concerned that the path to 2025 returns is not achievable. In fact, the stock is priced for an Armageddon scenario including huge loan losses and expectations that DB will need to raise capital.

This is completely misguided in my view. There are clearly headwinds currently including some forgone GDP growth in 2023 and 2024 that was baked in the 2025 forecasts. Additionally, this also translates to weakness in the Asia wealth management business, and given volatility in the bond markets the investment banking industry fee wallet is down ~50%.

However, the tailwinds are strong as well. Trading income ("FICC") is benefiting from the volatility, the corporate bank is growing strongly (26% year-on-year in Q2'2022) and of course the support from higher interest rates. It is all about the interest rates, stupid!

Putting this all together, the CFO recently confirmed that revenue guidance for 2022 of 26 to 27 billion is likely to be achieved at the higher end (I read this as exceeding 27 billion).

The impact of the interest rates

At the recent Bank of America financial conference, the CFO updated DB's interest sensitivity. For 2022, DB expects a benefit of EUR700m+ from the rising interest rates. For 2025, DB expects a benefit of EUR2.5b+ based on the current yield curve.

To provide some context to these numbers, the current market cap of DB is less than EUR17b. The benefit from interest rates is incremental pre-tax profits (there is no cost attached to it). Make no mistake about it - this is a game changer.

Clearly, these numbers are based on a static balance sheet and include assumptions on beta deposits (my back of the envelope comparing it to U.S. peers, suggests that this is a conservative number). However, more importantly, the change from a negative interest rates regime to a positive one completely changes the intrinsic value of the franchise (especially the liability side). The CFO commented on this in the recent conference:

So, then you get into the question of, well, the environment's changed. What are you going to do? How will you shape your business perhaps somewhat differently? And that's something we're, of course, giving a lot of thought to. Today the value of the deposit book is far greater than we would have thought a year ago or even six months ago . And some of the products have changed in their characteristics as well. If you take mortgages, for example, for one thing, the capital requirements on mortgages have gone up. The market has changed and the demand has changed in the marketplace.

What about massive loan losses?

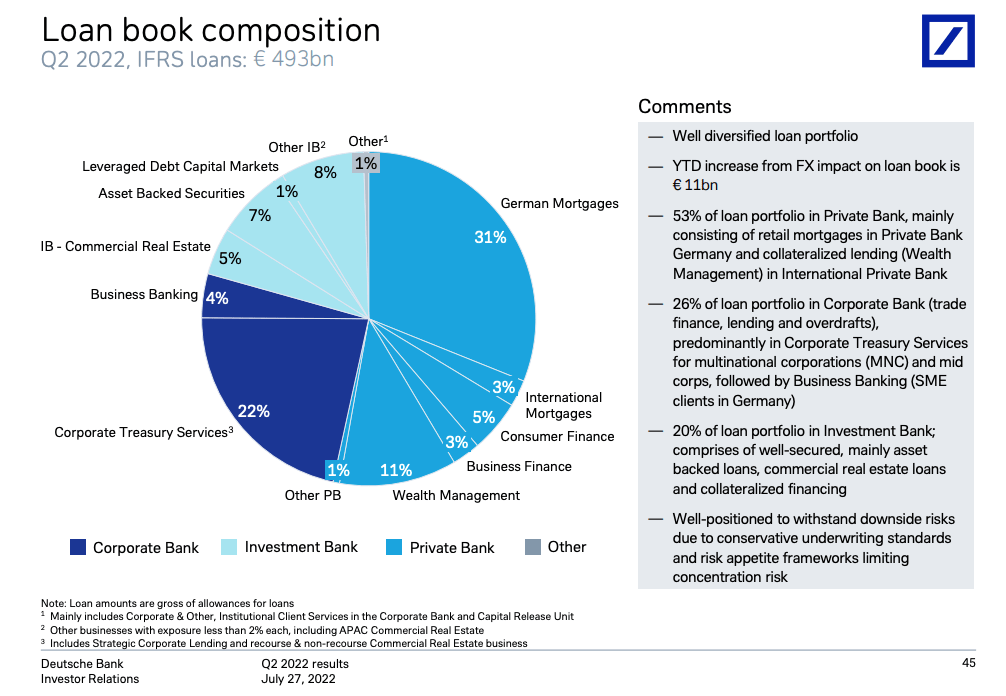

DB's credit risk profile is a conservative one. Much more conservative than many of its U.S. peers, for once, it doesn't have a large unsecured credit card outstanding loans. The biggest part of its book comprises moderate LTV German mortgages as can be seen below:

{kind=link}

The concern in the market of course is on the Russian gas-induced recession in Germany and the eurozone. Previously management guided to about 25 basis points (or approximately EUR1b of provisions), in the recent conference, the CFO added:

First of all, when we gave the-- it was about a billion euros estimate in that scenario. We were very clear it's a scenario conditions timing. Lots of things can change around that. Among other things, the passage of time. We were speaking already at the end of July. The assumption was that gas would have stopped at the end of June. And so, what was clear to us then already was how severe it would be for the German economy and therefore credit was going to depend on time. How much time there would be, how much the gas storage would rise before winter, how the Germans and the rest of the Europeans prepare for this through savings, organizing themselves to be more efficient in terms of energy usage, and also, by the way, government support, which we were not assuming in that 20-basispoint scenario. So, since that time, I think in some ways all of those things have moved to the better. And hence, time really did matter. And you're not seeing the downside scenario really emerge this year.

Considering the potential impact in 2023, the CFO noted the followings:

But you have to remember the prices are still there. And so, households and corporates will react to higher prices. And so that reduces disposable income on the one side, and it also in some cases significantly affects the economic viability of elements of the businesses that our clients do if the energy component of their production is just so uncompetitive. So, we do expect there will be an impact. But at this point, it's very hard to say looking into 2023. Again, 2022, it's quite close. We continue to have that confidence about 2022. How much of this begins to really show itself in 2023, it's too early to say. But we did say at the time, could it be a 35-basis-point credit loss provision year next year in that scenario? Yes, absolutely. Against 25 basis points we guided for this year.

So all in all, it is clear that fears over DB's credit risk book are overblown. There will be an impact but it is very manageable even in a worst-case scenario setting.

Final thoughts

In the recent decade, the key differences between DB and its U.S. peers, the likes of JPMorgan ( JPM ) and Bank of America ( BAC ), were the (lack of) performance of DB's investment bank and the negative interest rates set in the eurozone.

DB fixed the investment bank's performance and it is now earning its cost of capital, whereas inflation fixed the negative rate settings. I am not suggesting DB should trade at a 1.5x to 2x times book, like the U.S. peers but a valuation closer to tangible book certainly makes sense in the next few years.

A housekeeping note, when investing in European stocks, I avoid taking currency risk (unless it is deliberate). I buy DB in the German market. Over the last 12 months, I am in a net short Euro position.

For further details see:

Deutsche Bank: It's The Interest Rates, Stupid