DB - Deutsche Bank: Profitability And Turnaround Progress Are Simply Impressive

2023-05-08 00:44:19 ET

Summary

- Deutsche Bank closed an impressive Q1 2023, reporting EUR 7.7 billion of revenue and EUR 1.9 billion of pre-tax profits.

- Management voiced confidence going into 2023, expecting further revenue growth, OPEX saving, and potentially share buybacks.

- DB continues to enjoy a supportive interest rate environment and a solid business model/strategy execution from CEO C. Sewing and team.

- In light of all the positivity, I argue that a valuation of ~4x P/E and ~0.3 P/TBV is clearly underpricing the German bank.

- I upgrade my EPS expectations for DB through 2025 and I now calculate a fair implied share price equal to 37.04.

I have previously argued that Deutsche Bank's ( DB ) earnings before tax in 2023 could expand to somewhere around EUR 7-8 billion, after closing FY with EUR 5.7 billion of profits, the highest level of earnings since 2007. And following an impressive Q1 2023 report, I am confident to reiterate the thesis.

In the January quarter, not only did DB beat analyst's expectations with regards to both revenue and earnings, but also did the bank manage to surprise investors with the potential for share buybacks, which may start as early as Q3 2023.

Considering DB's impressive profitability, paired with the company's leading position in global FIC trading and corporate banking, I argue that a valuation of ~4x P/E and ~0.3 P/TBV is clearly underpricing the German bank. According to my residual earnings valuation model, I estimate more than 200% upside.

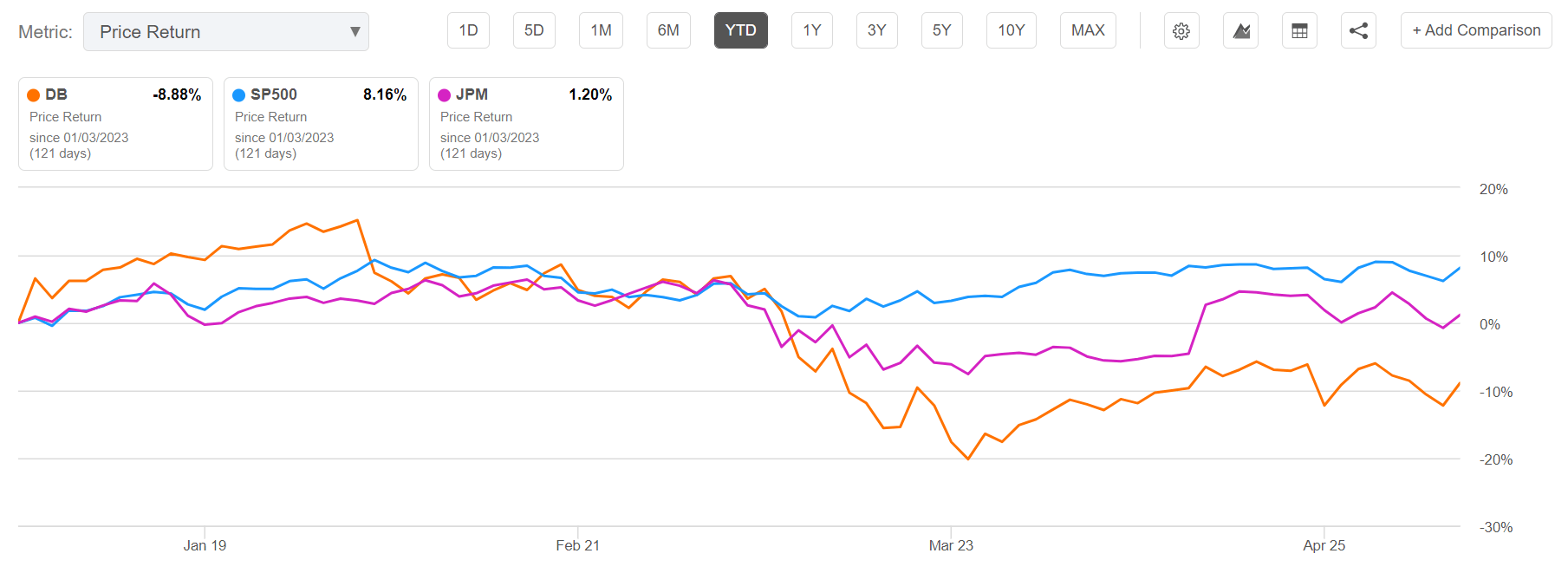

For reference, Deutsche Bank stock has underperformed YTD: Since the start of the year 2023, DB shares are down about 9%, as compared to a gain of 1.2% for U.S.' competitor JPM and a gain of approximately 8% for the S&P 500 ( SP500 ).

{kind=link}

Seeking Alpha

Deutsche Bank's Strong Q1 2023

In Q1 2023 , Deutsche Bank delivered another quarter of solid strategy execution, business momentum and profitability.

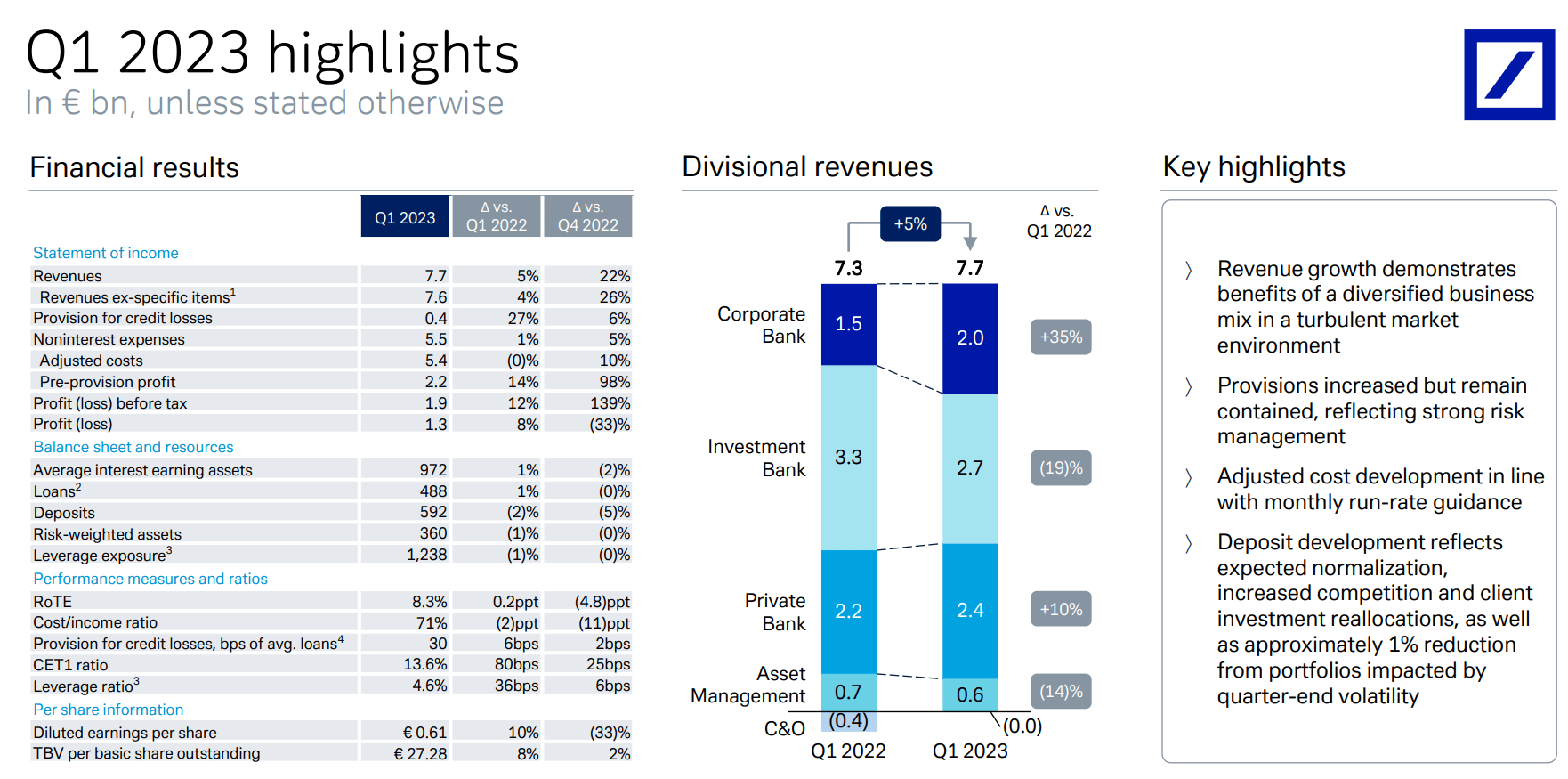

During the period from January to the end of March, DB generated about EUR 7.7 billion of revenues, which compares to EUR 7.3 billion for the same period one year earlier (5% YoY growth), and beating analyst estimates by close to $250 million. With regards to profitability, quarterly profit before taxes was recorded at EUR 1.9 billion, almost EUR 500 million above analyst estimates, and close to 12% above respective Q1 2022 profitability; net income was reported at EUR 1.3 billion (up 8% YoY).

Deutsche Bank's Q1 2023 profitability reflects a post-tax return on tangible shareholders' equity ((ROTE)) of 8.3%, and the bank reported a cost-to-income ratio of 71%, down 200 basis points versus the previous year. Also noteworthy is that DB's deposit flows in April show signs of stabilization, even improvement, and the bank's costs of unsecured credit funding have been running below the planned levels YTD, according to management commentary.

{kind=link}

DB Q1 2023 reporting

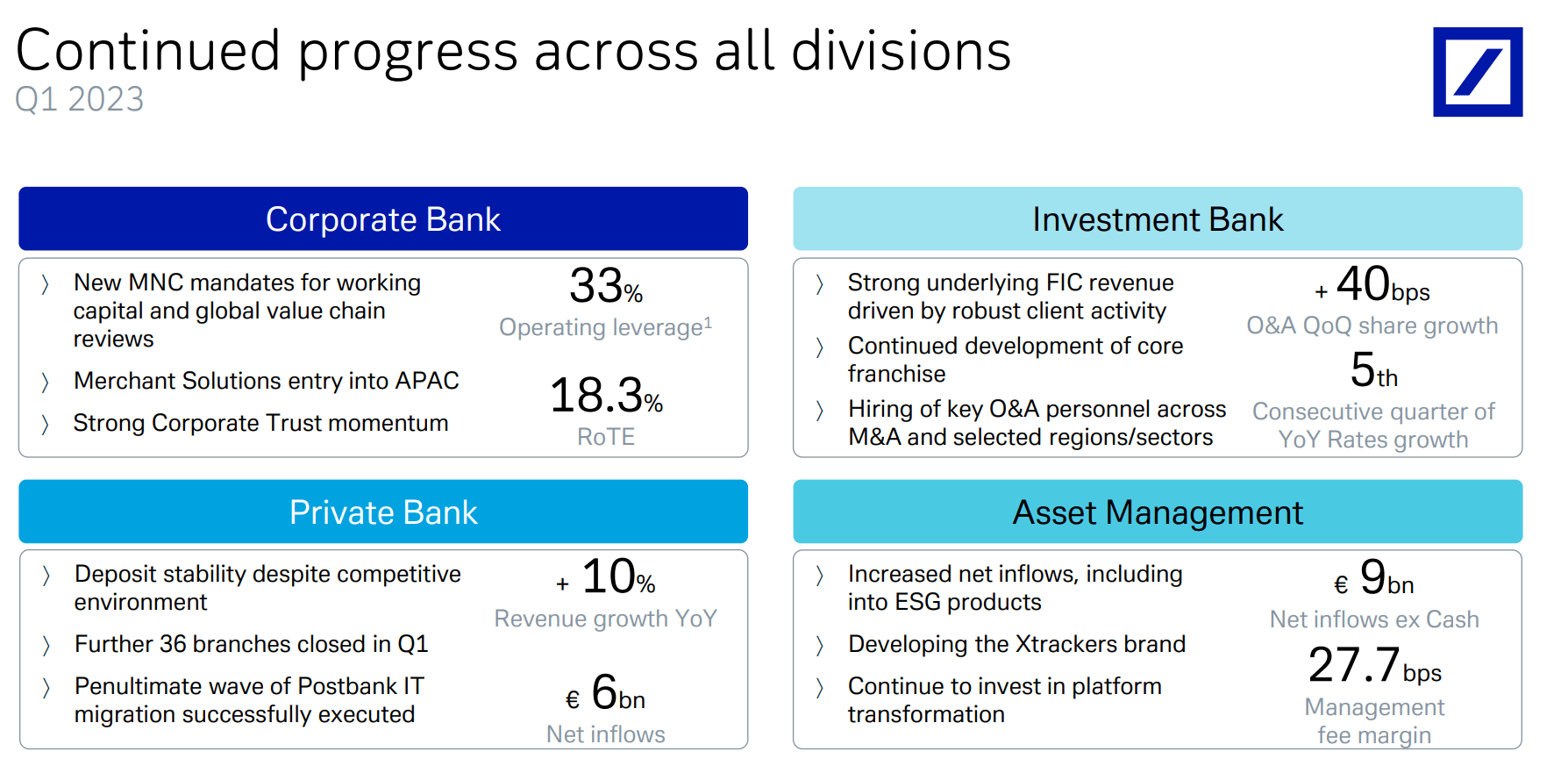

Notably, Deutsche Bank performed strongly across all operating units, considering the challenging macro environment.

- The Corporate Bank recorded EUR 2.0 billion of revenue (up 35% YoY)

- The Investment Bank remained resilient versus 2021, generating revenue of approximately EUR 2.7 billion

- Revenue from DB's Private Bank increased to EUR 2.4 billion; reporting EUR 6 billion of net inflows

- The Asset Management generated EUR 0.6 billion of revenue; reporting EUR 9 billion of net inflows

{kind=link}

DB Q1 2023 reporting

Reflecting on excellent Q1 2023 results, Deutsche Bank CEO Christian Sewing suggested to investors that the bank is on-track 'to meeting or exceeding our 2025 targets', which would imply revenues of about EUR 30 billion and a CIR of below 63%, suggesting earnings before tax above EUR 10 billion (for reference, Deutsche Bank is currently valued at a market cap of around EUR 20 billion).

Moreover, Sewing outlined a series of measures that could further expedite the execution of the bank's strategy. These measures, worth about EUR 500 million of annual savings, may include pushing for further operational and capital efficiency that may ultimately lead to 'share buybacks later this year'. With that frame of reference, Deutsche Bank management said that the bank has already initiated talks with regulators and the ECB about the potential for buybacks, which I estimate may fall in the range EUR 350-500 million.

Together with Q1 2023 results, Deutsche Bank also communicated the takeover of the UK investment bank Numis for about EUR 500 million. To me, this decision came as a strong surprise, because M&A is clearly not what I like to see at ~0.3 P/TBV, when capital should be allocated to buybacks, in my opinion. Moreover, I struggle to see the strategic rationale for the acquisition, as Numis is an equity brokerage firm, a vertical that DB wanted to shrink. That said, investors should definitely keep a sceptical eye on Deutsche Bank's (future) M&A ambitions.

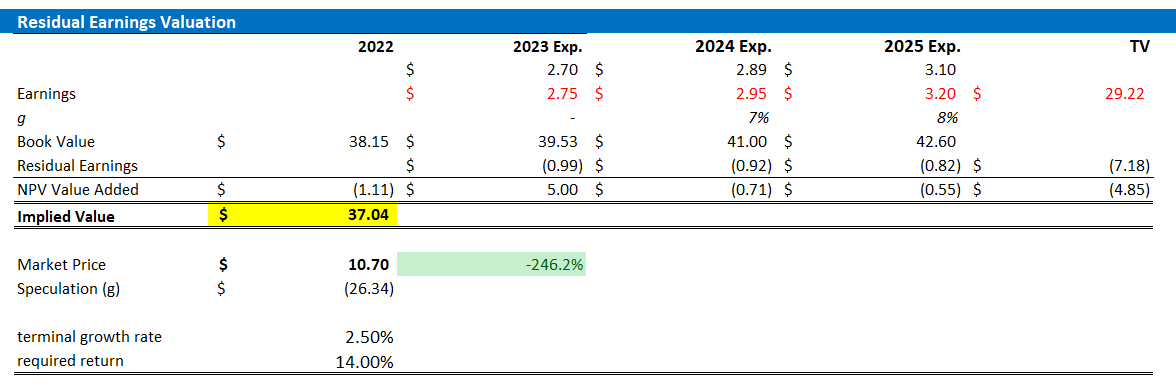

Target Price: Raise To $37.04

Reflecting on a supporting interest rate environment for all asset classes, paired with solid business model/strategy execution from CEO C. Sewing and team, I upgrade my EPS expectations for DB through 2025: I now estimate that DB's EPS in 2023 will likely expand to somewhere between $2.7 and $2.8. Moreover, I also raise my EPS expectations for 2024 and 2025, to $2.95 and $3.2, respectively.

I continue to anchor on a 3.5% terminal growth rate (approximately in line with nominal global GDP growth to reflect conservatism), but I increase my cost of equity estimate by 200 basis points, to 14%, reflecting the most recent stress in the U.S. banking sector.

Given the EPS update as highlighted below, I now calculate a fair implied share price for DB equal to $37.04.

{kind=link}

Author's EPS Estimates and Calculation

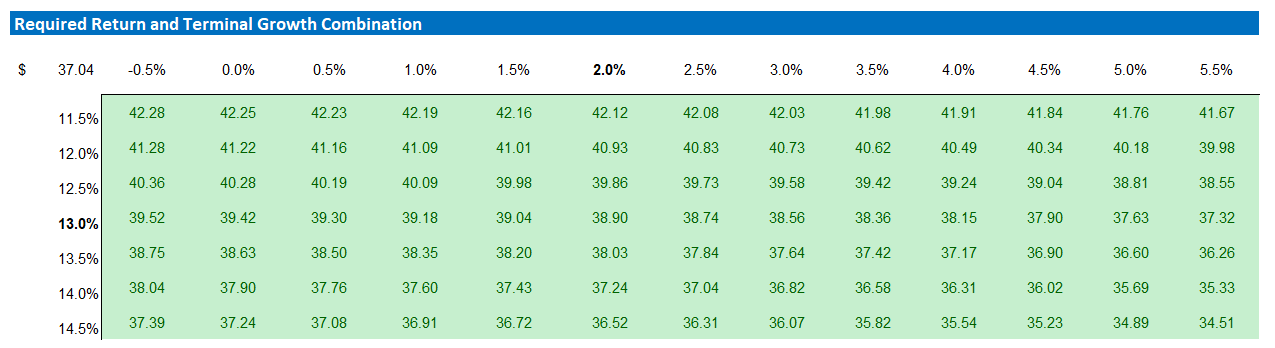

Below is also the updated sensitivity table.

{kind=link}

Author's EPS Estimates and Calculation

Risks Associated With DB

Regarding the risks associated with investing in Deutsche bank, which applies to banks in general, I would like to emphasize that while I maintain the belief that investments in banks carry lower risks than what the market suggests, it is important to acknowledge the possibility of elevated tail-risk exposure. In the event that this risk materializes, it could lead to a significant depreciation in Deutsche Bank's share price. In that context, it is worth pointing out that the company's share price levels from before the great financial crisis have not yet been fully recovered. Nevertheless, it is reassuring to know that Deutsche Bank's Common Equity Tier 1 (CET1) ratio stands at 13.6%, providing a considerable buffer for the company against most market stress scenarios, including severe ones.

Conclusion

Deutsche Bank closed an impressive Q1 2023, reporting EUR 7.7 billion of revenue and EUR 1.9 billion of pre-tax profits. Moreover, management voiced confidence going into 2023, expecting further revenue growth, OPEX saving, and potentially share buybacks.

DB continues to enjoy a supportive interest rate environment, and a solid business model/ strategy execution from CEO C. Sewing and team. And in light of all the positivity, I argue that a valuation of ~4x P/E and ~0.3 P/TBV is clearly underpricing the German bank.

I upgrade my EPS expectations for DB through 2025, and I now calculate a fair implied share price equal to 37.04.

For further details see:

Deutsche Bank: Profitability And Turnaround Progress Are Simply Impressive