DB - Deutsche Bank: Profits Could Expand To 7-8 Billion By 2025

Summary

- Deutsche Bank closed 2022 with EUR 5.7 billion of profits, the highest level of earnings since 2007.

- Deutsche Bank has also voiced confidence going into 2023, expecting revenue growth, while credit losses and OPEX are expected to remain flat as compared to 2022.

- On the backdrop of increasing interest rates, I believe profits could expand to somewhere between EUR 7 billion and 8 billion within the next 3 years.

- Reflecting on a higher yield environment for all asset classes, I upgrade my EPS expectations for DB through 2025.

Thesis

I have previously argued that Deutsche Bank (DB) stock could triple by 2025 ($12/share reference). And reflecting on the bank's exceptionally strong Q4 results, I am confident to reiterate my bullish thesis. Investors should consider that in 2022, Deutsche Bank has generated close to EUR 5.7 billion of profits, the highest profit since 2007. And on the backdrop of increasing interest rates, I believe profits could expand to somewhere between EUR 7-8 billion within the next 3 years, modelling an interest rate sensitivity of 20 basis points per percentage point increase in the ECB's marginal lending facility rate. Deutsche Bank remains a high conviction 'Strong Buy'.

After a decade of enormous underperformance ...

{kind=link}

Deutsche Bank stock has finally started to show relative strength. For reference, for the trailing twelve months, DB stock is down only approximately 6%, as compared to a loss of close to 10% for the S&P 500 ( SPY ).

{kind=link}

An Exceptional Q4 2022

During the period from September to the end of December, DB generated about EUR 6.3 billion of revenues, which compares to EUR 5.9 billion for the same period one year earlier, reflecting a 7% year over year topline growth. Quarterly profit before taxes was recorded at EUR 775 million, slightly below analyst consensus estimates--but very attractive considering the bank's EUR 25 billion market cap.

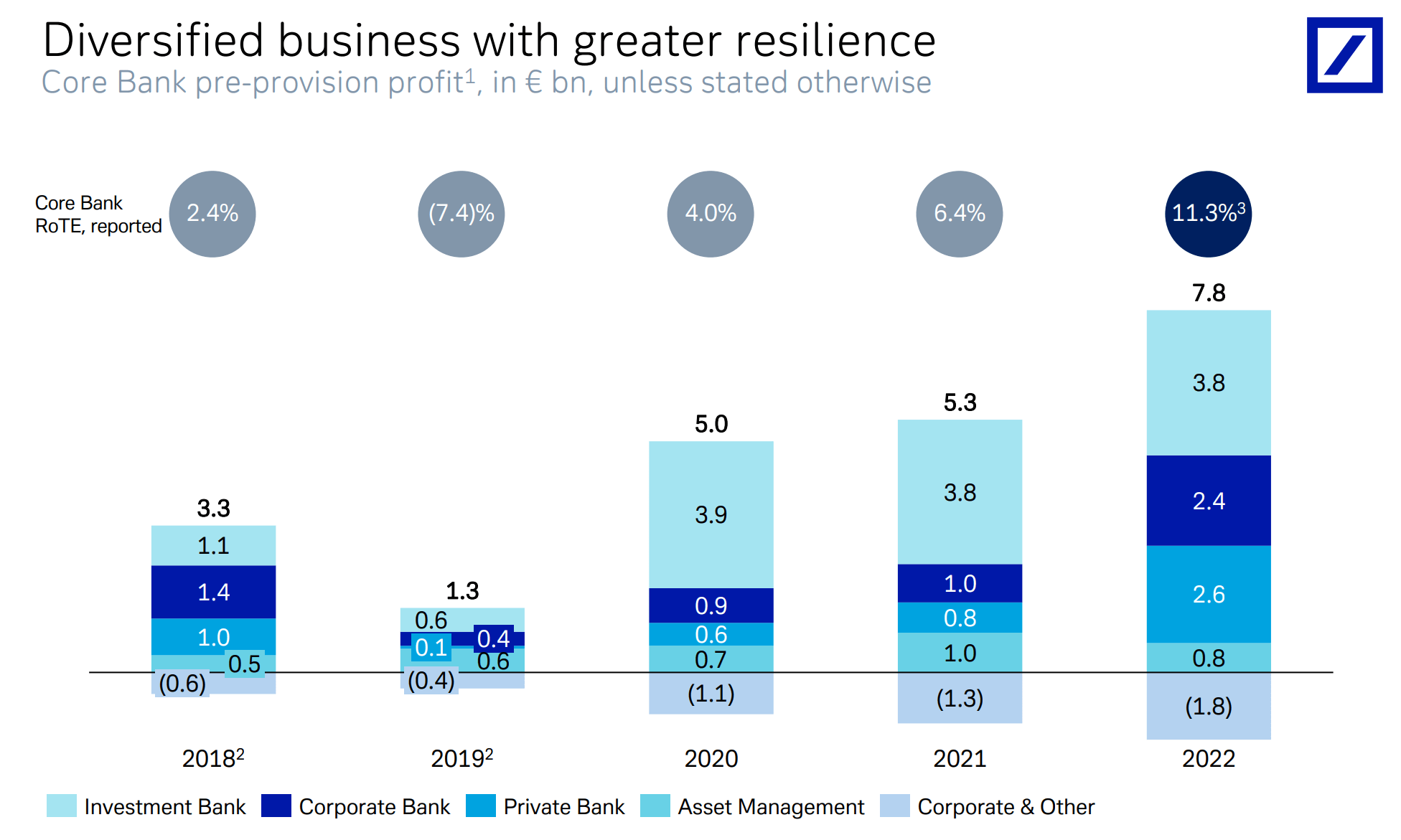

For the full year 2022, Deutsche Bank's revenues grew to EUR 27.2 billion and the bank's profitability jumped to the highest level since 2007: For FY 2022, Deutsche's net profit more than doubled as compared to 2021, growing to €5.7 billion. Although the result was aided by a €1.4 billion accounting exercise, a revaluation of tax assets, the result is still very considerable even absent the non-recurring gain.

Deutsche Bank performed strongly across all operating units, considering the challenging macro environment in 2022.

- The Corporate Bank recorded €2.1 billion of earnings, which is more than double the 2021 level of €1.0 billion.

- The Investment Bank remained resilient versus 2021, generating earnings of approximately €3.5 billion (only down 6% YoY)

- Earnings from DB's Private Bank increased more than x5, up to €2.0 billion.

- The Asset Management generated €0.6 billion of earrings, reflecting a YoY contraction of 27%.

{kind=link}

Confident Going Into 2023

The bank's statement that management had pushed back a decision about additional share buybacks to 2023 pressured market optimism, and DB stock dropped as much as 5% in the trading session following the earnings release. Investors should consider, however, that the bank did announce a dividend increase of 50%, to 30 cents per share in 2023. Moreover, the bank reiterated the pledge to distribute €8 billion in capital to investors by 2025. And the company continues to target distributing close to 50% of earnings thereafter.

Deutsche Bank has also voiced confidence going into 2023, expecting revenue growth, while credit losses and OPEX are expected to remain flat as compared to 2022. CEO Sewing commented:

we expect our revenues to increase again, and our credit loss provisions to remain stable in light of an improving economic outlook ...

... And our aspiration is to keep expenses flat on 2022, even if that requires us to become even more ambitious on costs in an inflationary environment.

A strong profitability jump in 2023 is also highly likely due to the NIM expansion, with DB commenting that

'[interest rate] sensitivity is high in 2023, as the rapid pace of increases in the market-implied curve temporarily amplifies the impact of incremental moves.

Investors should also consider the ECB is still in the process of raising the cost of capital, and rates on the marginal lending facility could likely edge towards 4 percentage points in 2023. With that frame of reference, as compared to 2021 numbers, my model--which anchors on management commentary from Deutsche Bank, Barclays, UniCredit and Societe Generale--calculates that for every 1 percentage point of interest rate increase, European banks are likely to enjoy a 20 basis point increase in NIM expansion. For Deutsche Bank, such a model would assume EUR 7-8 billion in 2025, which would also be approximately in line with Deutsche Banks's cost/income target on a EUR 30-33 billion of revenue assumption.

{kind=link}

For reference, the yield curve in Europe has shifted up by approximately 250 - 300 basis points as compared to 2021.

{kind=link}

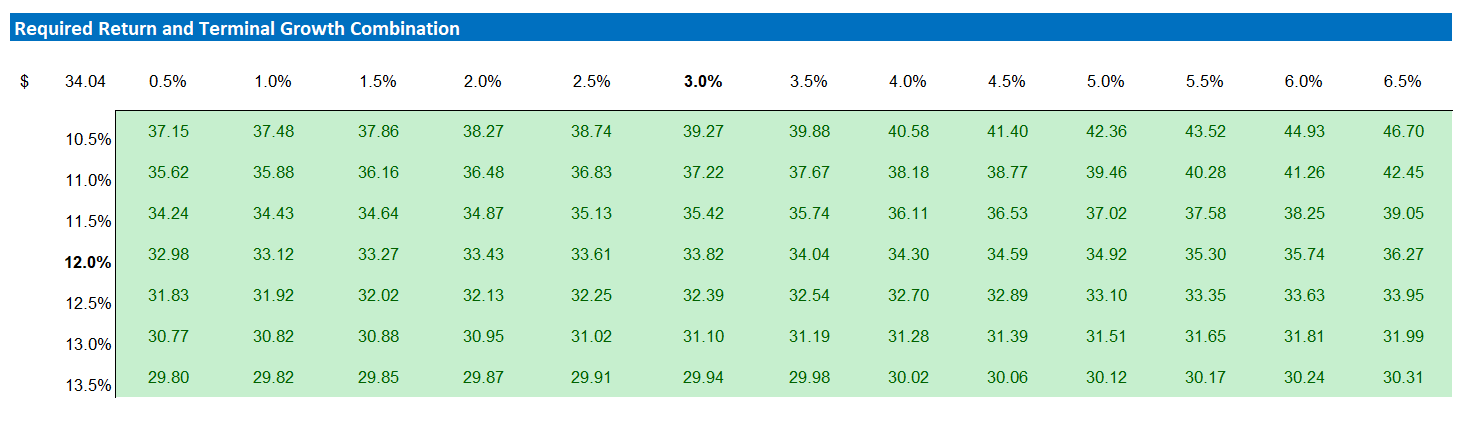

Target Price: Raise To $34.04

Reflecting on a higher yield environment for all asset classes, I upgrade my EPS expectations for DB through 2025. I now estimate that DB's EPS in 2023 will likely expand to somewhere between $2.5 and $2.9. Moreover, I also raise my EPS expectations for 2024 and 2025, to $2.95 and $3.15, respectively.

I continue to anchor on a 3.5% terminal growth rate (approximately in line with nominal global GDP growth to reflect conservatism), as well as on a 12% cost of equity, which I deem a highly conservative estimate.

Given the EPS update as highlighted below, I now calculate a fair implied share price of $34.04.

Author's EPS Estimates and Calculation

{kind=link}

Below is also the updated sensitivity table.

Author's EPS Estimates and Calculation

{kind=link}

Risks

With regards to risks related to investments in banks, I would like to highlight what I have written before :

While I believe that investments in banks are less risky than the market implies, the tail-risk exposure is still elevated and if materialized this might depreciate DB's share price significantly. For reference, the company has still not recovered the share price levels seen before the great financial crisis.

In any case, Deutsche Bank's 13.2% CET1 ratio should buffer the company for most market stress scenarios, even severe ones

I would like to add that Deutsche's CET1 ratio has now expanded to 13.4%.

Conclusion

Deutsche Bank closed 2022 with EUR 5.7 billion of profits, the highest level of earnings since 2007. The German financial institution has also voiced confidence going into 2023, expecting revenue growth, while credit losses and OPEX are expected to remain flat as compared to 2022. On the backdrop of increasing interest rates, I believe profits could expand to somewhere between EUR 7-8 billion within the next 3 years.

Reflecting on a higher yield environment for all asset classes, I upgrade my EPS expectations for DB through 2025. I now calculate a fair implied share price of $34.04. Reiterate 'Strong Buy'.

For further details see:

Deutsche Bank: Profits Could Expand To 7-8 Billion By 2025