DB - Deutsche Bank: The Restructuring Strategy Is Delivering

2023-06-22 04:42:13 ET

Summary

- Deutsche Bank reported a solid performance in a volatile market.

- There is continued progress in all the company's divisions with higher targets in the restructuring agenda.

- The bank reiterated its 2023 outlook with low loan loss provisions and expected share buybacks in the second part of the year. This is supportive of the shareholder's remuneration policy.

- Now, Deutsche Bank stock is a buy.

Our readers know that we have a good grip on European banking, and looking at our geographical coverage divided by countries, you can check out our most recent range:

- Austria: Raiffeisen Bank International , and Erste Group Bank;

- Italy: UniCredit and Intesa San Paolo ;

- Switzerland: UBS and Credit Suisse ;

- France: Société Générale , Crédit Agricole , and BNP Paribas;

- Belgium: KBC Group;

- UK: HSBC.

You have probably noticed that we missed one of the most critical countries in the EU area: Germany (and Spain). Therefore, today we start to analyze Deutsche Bank Aktiengesellschaft ( DB ). Although it is the first time we have provided an update on Seeking Alpha, it is a well-known company by our team. DB does not need any introduction; however, the bank is a German financial services company with an arm in asset management and investment banking. It is headquartered in Frankfurt with a dual listing (in its home country and the NYSE). Before providing a specific update on the German bank, we must recap why we support the EU banking sector.

MACRO EU Upside

Year-to-date, 2023 has been characterized by profound turbulence in the regional banking sector in the United States. Silicon Valley Bank collapsed in March, and in April, the failure of First Republic Bank and the subsequent sale to JPMorgan Chase. Given these developments, the European banking sector has performed poorly. Still, European banks are in a very different situation than US regional banks, and UBS' acquisition of Credit Suisse, which was concluded in June , is a particular case. We have long argued that the market is too pessimistic about European banks. Indeed, the Q1 earnings season proved to be a supportive catalyst and reinforced our overweight thesis on the EU banking sector. Why are we positive? At the MACRO level, we see five crucial takeaways:

-

European banking earnings in the 1st quarter exceeded expectations, so the estimates for 2023 and 2024 have been revised upwards. This is attributable to higher interest margins, thanks to the effect that interest rate hikes have had on banks' balance sheets and profitability;

-

Bank deposits are stable, with very limited outflows. The ratio between deposits and loans generally remains around 80-90%, and the liquidity coverage ratio exceeds 150%, well above the regulatory requirements;

-

There are no signs of credit stress. Provisions for credit losses remain below average. Market attention has turned to commercial real estate, and while we believe there are reasons for concern for this asset class, EU banks' exposure to the sector is contained (much lower than in previous cycles);

-

The return on capital is positive. The total return on distributions (dividends plus share buybacks) for the sector is approximately 12%;

-

Valuations in the sector are nearing historic lows. The industry trades around six times earnings, with solid momentum representing a relative PE of about 50%. It is at its lowest level on record, compared with a long-term average of 80%. Regarding the price-to-tangible value ratio, the sector trades at 0.7x with a RoTE of 12.5%.

Q1 results comment

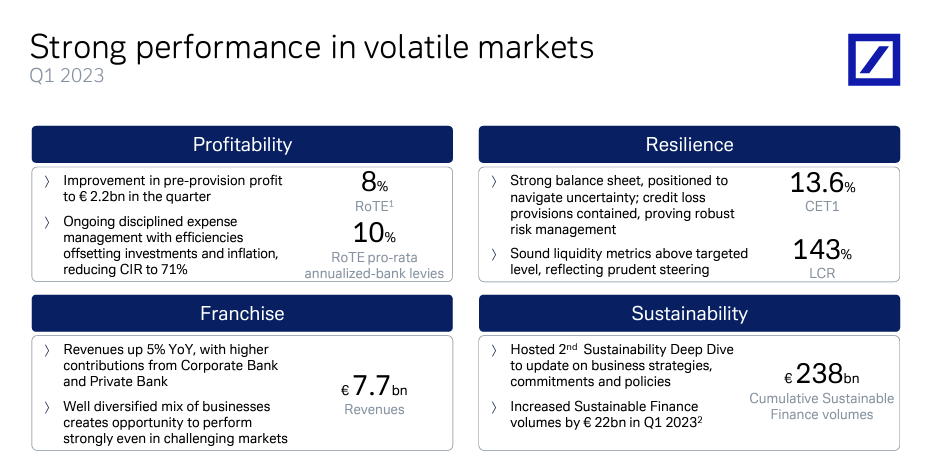

Very briefly, in Q1, Deutsche Bank increased its turnover (the highest since 2016) with net profit growth beyond Wall Street analyst estimates. Indeed, net income attributable to shareholders amounted to €1.16 billion, with an average consensus of €1.12 billion. Following the restructuring plan started in 2019, this is the eleventh consecutive quarter of profit, and we can confirm that Deutsche Bank's strategy is delivering. Top-line revenues grew by 5% to $7.68 billion, with corporate banking revenue rebounding by 35% and private banking revenue up 10%. On the other hand, revenues deriving from investment banking decreased by 19%.

Deutsche Bank Q1 Financials in a Snap

{kind=link}

Source: Deutsche Bank Q1 results presentation

MICRO DB Upside and Changes in Estimates

Going to the primary ratio analysis:

- The Common Equity Tier 1 was up by 20 basis points every quarter, reaching 13.6% versus the consensus estimate of 13.3%. This was helped by stable Risk-Weighted Assets at €360 billion. In addition, we estimated 40-60 basis points of capital headwinds thanks to capital generation. This leaves room for a share buyback with an estimated excess capital of approximately €1.5 billion. We are very confident about a step up in the capital return in H2;

- Corporate center costs were significantly down thanks to a reversal in V&T (a positive one-off that is not included in our long-term projection);

- Deposits fell by 4.7% in the quarter. This was driven by competition and market volatility. James von Moltke, the company's CFO explained that 1% of customers left the bank in the last two weeks of March; however, by April-end, deposits had increased again. In abs value, stakes were down by €30 billion, but the liquidity cover ratio stands at 143% compared to a company target of 130%;

- On asset quality, DB portfolio is well diversified across regions and sectors. In addition, the company confirmed its previous 2023 guidance of 25-30 basis points;

- On a cost basis, the cost-income ratio fell to 71% in the quarter from 73% in 2022. DB operating leverage is critical to getting traction with Wall Street analysts re-rating. We should note that the higher restructuring costs have already been absorbed;

-

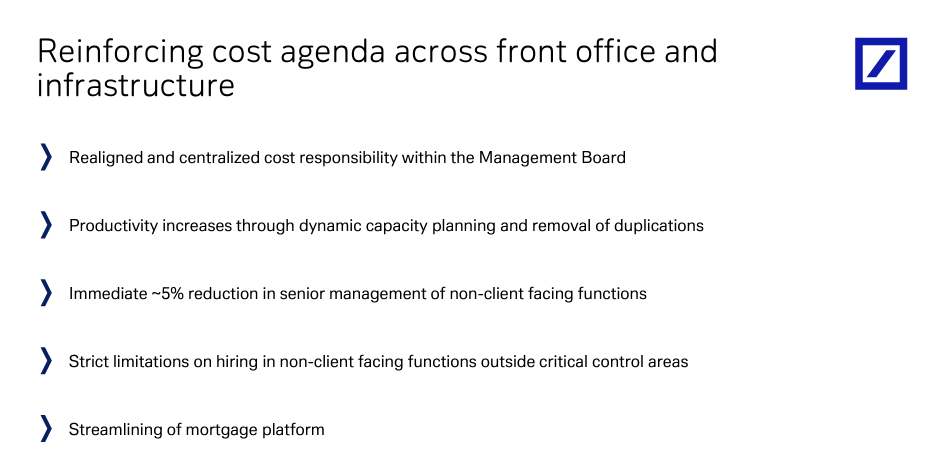

Despite the previous point, the bank intends to continue the restructuring process. The Frankfurt-based group plans to cut around 800 senior back-office employees as part of the German lender's goal of realizing an additional €500 million in cost savings. The company's CEO, Christian Sewing, explained that DB is cutting about 5% of senior non-client-facing staff after raising its cost-cutting target to €2.5 billion.

Deutsche Bank restructuring in place

{kind=link}

{kind=link}

Conclusion and Valuation

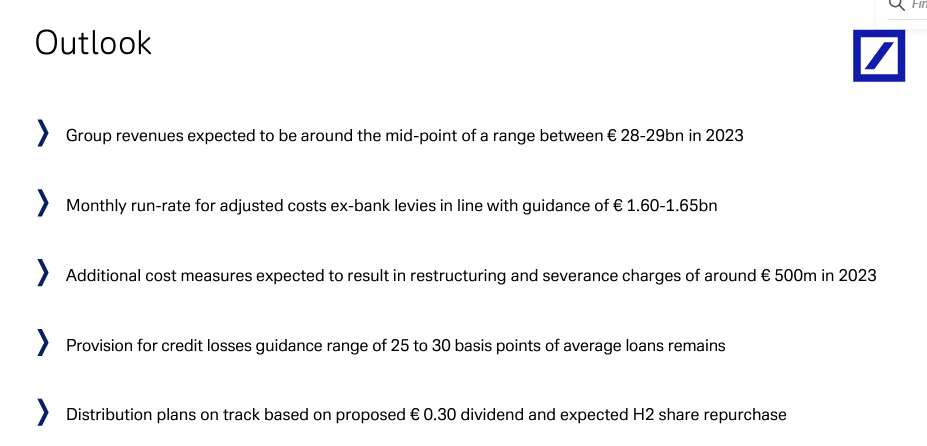

The 2023 guidance was confirmed. Therefore, we are estimating top-line sales at €28.5 billion for the current year with lower costs thanks to €500 million restructuring in place. Looking at the 2024-2025 estimates, we are confident DB could outperform its internal targets. The restructuring strategy is delivering, and we are raising our earnings per share estimates. Looking at the company's tangible book value, the company is trading at 0.3x/0.4x with an 8% in RoTE; we believe this discount is no longer justified. As a reminder, the EU sector trades at 0.7x TBV with a RoTE of 12.5%. Therefore, even applying a discount to the industry (20%), we believe a target price of €11 per share is justified thanks to its profitability improvements and the upside on the capital remuneration policy. Downside risks to our overperforming rating include a decline in the global capital markets revenue pool, lower than expected ECB rate hike, higher competition, litigation costs, and execution risks in the restructuring process.

For further details see:

Deutsche Bank: The Restructuring Strategy Is Delivering