DLAKY - Deutsche Lufthansa: Nope Stock Is Still Overvalued

Summary

- Since my last article, Lufthansa has seen significant market outperformance of 31% compared to the 2.35% of the S&P 500. That makes my "HOLD" rating factually wrong.

- At least, if you don't consider the company's risk profile. Lufthansa was 20% cheaper in my last article - now it's expensive again.

- However, some things have changed - here is why I am not revisiting my "Sell", but also not raising this one to a "Buy".

Dear readers/followers,

I've written a number of articles on Lufthansa ( DLAKY ) at this point. The company has the dubious honor of being one of the very, very few companies I've ever assigned a "Sell" rating to, and one that paid off for quite some time. It's been some months since my last update on the company, and we've seen improvements that have caused the share price to appreciate and technically beat the market.

This does not mean though, as I believe, that the company should be considered a "Buy".

Rather, let's look at what we have going here.

Lufthansa - A 2023 Update

Going into 2023, Lufthansa might seem like an interesting play. The company controls attractive Swiss, Austrian, and Brussels airlines. It has the Star Alliance brand, and through it offers its travelers one of the most extensive networks of destinations on the planet. Even with Ukraine and the geopolitical and economical macro, none of the company's overall geographical exposures are in themselves unattractive.

Combine this with Eurowings, and a capable logistics/freight operation as well as the oft-mentioned catering business, and you have an interesting mix even if that mix is heavily weighted towards passengers, giving readers the impression that Lufthansa is a freight-heavy operation is completely wrong.

{kind=link}

It's also only somewhat international - over half of the mix is Europe, and very Germany-heavy, with a quarter of the entire revenue base in the largest economy in Europe.

The fact is, the last set of news out of Lufthansa HQ have all been pretty positive overall. We're talking about things like earnings forecast increases, salary increases for 19,000 cabin personnel, and overall pretty good 3Q22 results - which we'll go into here.

It was never the case that Lufthansa would "always" remain unattractive as a play. What it did mean when I wrote my first article though, was that it simply was too risky a play, owing to its airline sector and the way macro and the volumes looked.

But we actually have a bit of a turnaround as we start to see things in 3Q22.

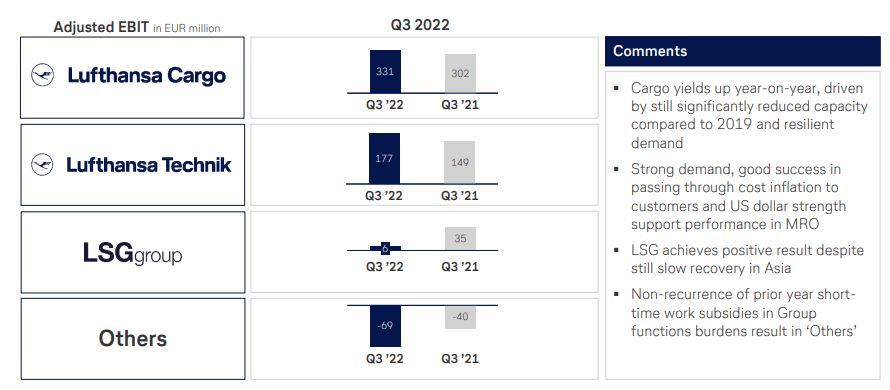

The company managed to turn pre-tax profit around, flew over 33M passengers, and delivered record results in Cargo as we did, with impressive improvements in yields.

Most importantly, business volumes are back to 90% of the pre-crisis level, which makes a pretty strong case for a beginning turnaround overall.

{kind=link}

I think it's pretty strong wording to say that the company "leaves the crisis behind", but I'm willing to say that Lufthansa is now looking a lot better. To put it simply, if it was at the level of my previous article, and the results were somewhat forecasted here, with the reversal in play, then I could have been convinced to potentially call Lufthansa a high-risk bullish play - if the financials looked better than they do.

I'm talking about things like yield, I'm talking about things like credit ratings. The company pays for 3 different credit ratings, and only one of them, the least relevant from the Scope Rating company, is even IG. The other two are BB/Ba2.

Any characterization that the risk is "over" at this time would be wrong, despite some really superb 3Q22 results. The company managed to generate free cash flow (on an adjusted basis) for both 3Q and 9M, and the ever-important seat load factor is back to near-2019 levels, which indeed suggests a bit of a reversal.

Meanwhile, non-core business earnings are humming - and that's saying something.

{kind=link}

These are record-level profits - but again - any sort of characterization of a full reversal being done here is wrong. The company is still under massive pressure. Liabilities for unflown tickets are over a billion euros for the quarter alone. Granted, this has never been a small number even historically, but I want to see better over time before stating this as a finished turnaround with investment potential.

Nonetheless, from a YoY perspective, we have negative €500M+ for 9M21, and over €3.3B positive in adjusted FCF for the 9M, which is good. These numbers are naturally also reducing debt stress. net debt is down nearly €3B, and the company has plenty of liquidity available - almost €12B, should it choose to use it.

Increases in the discount rates also mean that pension obligations decline - they're down by nearly two-thirds since last year, which in turn increases company equity. A+B=C - simple math.

What I am saying is that these results and trends are positive, and I understand why the market is suddenly giving Lufthansa some love again. However, I'm more interested in pointing at structural improvements and cost reductions - things that will actually matter going forward.

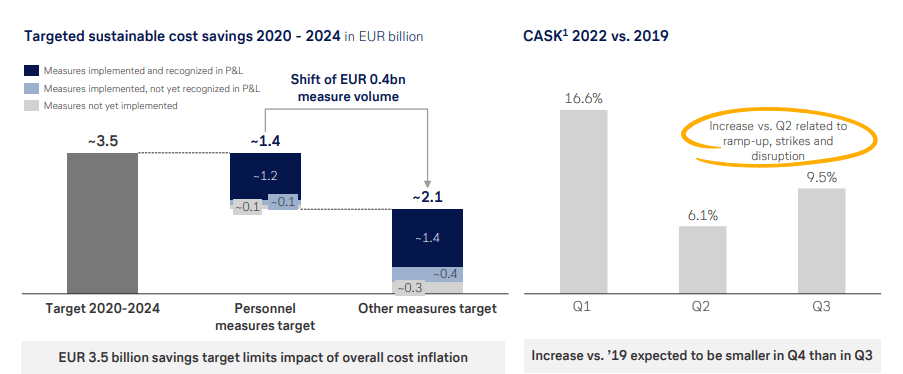

Lufthansa has targeted over €3B of them until 2024E.

{kind=link}

The company also expects some very impressive numbers for the full year, with adjusted FCF above €2B and over €1B in adjusted EBIT. Capacity is expected to climb to 80% of the 2019 level.

However, none of this positivity will result in shareholders getting any sort of dividend in the coming year - at least, I don't see that happening. The company is executing on all the right "soft" targets - improved relationships with labor unions, better CO2/ESG, and improved seating and comfort for all classes...

{kind=link}

...and all of that is good stuff. But I'm more interested in the question of when those bottom-line adjusted FCF euros turn into dividends and more capital appreciation for me, due to company stability.

I do believe Lufthansa is well-positioned to take advantage of trends here, and the company is one of the European airlines that's well-positioned to take advantage of the "new normal". Few European lines can compete with it - the local Scandinavian one, SAS ( SASDQ ) certainly can't.

So, all in all, I'm still cautious, but that caution has turned somewhat optimistic here, and I'm willing to give Lufthansa a bit more of the benefit of the doubt.

The company has seen improvements over the past few months. The most crucial is that Lufthansa is private once again. The economic stabilization fund of Germany sold all remaining shares of Lufthansa back in mid-September. The WSF held around 6.2% of the company, down from an original 20% to save the company back in 2020. This marks an early divestment of the shares, about 1 year early compared to the overall plans for the company.

Let me reiterate once again though - Dividends for Lufthansa still do not exist, and investors should not expect a change all that soon. Lufthansa was cut to junk (BB-) by S&P Global, and a Ba2 by Moody's. Lufthansa did have an appealing capital payout up until 2018 but there are still significant reasons why investors shouldn't expect anything from Lufthansa for some time, and that goes for this time, even after these positive trends.

Revisiting Lufthansa's valuation for 2023

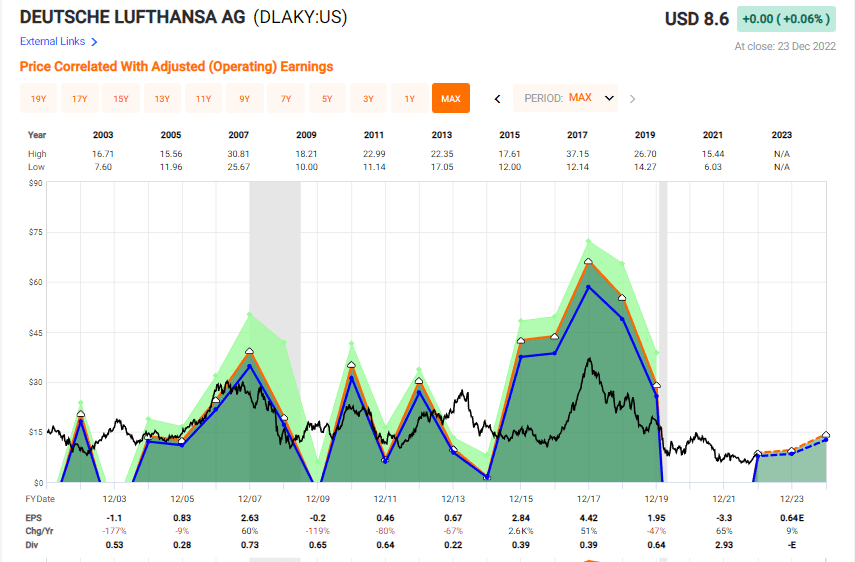

If we look at the company forecasts compared to my last article in terms of expected earnings and dividends, you'll note that we have very little improvements in these. Also, remember just what you're investing in. A picture speaks louder than so many words, and here's a picture that illustrates how earnings flow to this company. It's not a flattering picture.

Lufthansa Valuation (F.A.S.T graphs)

{kind=link}

That's why even if I had forecasted more positively in my last article, I wouldn't have bought Lufthansa here. Buying a company that has these sorts of ups and downs is something I've found to be contrary to my investment style. It's not the sort of stability and long-term potential I'm looking for. The 20-year returns for DLAKY are less than 2% per year, and less than 40% in 20% - and it's negative without the dividends.

That's something you need to keep in mind if you go for this.

Airlines are a very tricky sort of investment, and in my experience, people take what they invest in far too lightly. They don't give risk considerations the same attention they should, and they also don't ask the fundamental question if a company is really that much more attractive than a far safer alternative. I know that because I work with this professionally, and I used to be similar when I started investing.

I write about another company on a similar path - Rolls-Royce ( OTCPK:RYCEF ). These two companies are fairly alike, even in similar segments in some ways. Both are storied giants with plenty of history and notches on their belt - both of them fell on hard times. The main difference between RYCEF and Lufthansa is that Rolls-Royce's recovery is further, and I believe the visibility for profitability for the company is actually very good here, even as early as 2022. We may even get a dividend - and not just a token one - as early as next year.

I'm not opposed to investing in turnarounds. Not at all. But if I do it, I do want good visibility and a solid expectation for when I might see returns. The absence of a yield makes this a must. And for Lufthansa, this visibility remains low.

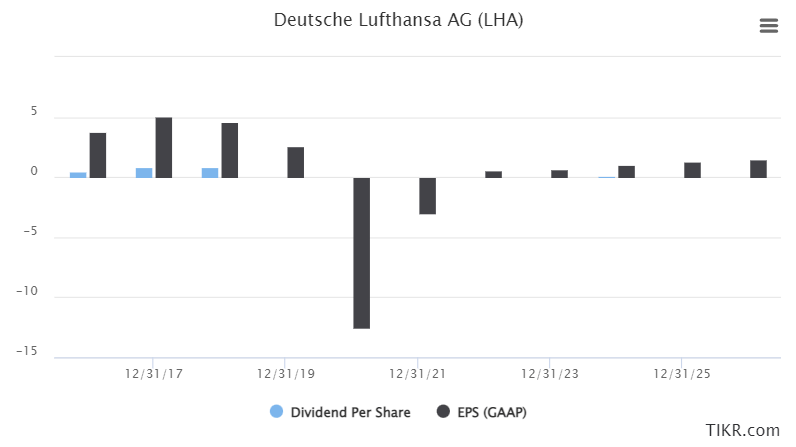

If we go by current 5-year averages for Lufthansa, it does not allow for a positive 2024E, not even with the massive EPS improvements that are expected, and not with the dividend reintroduction as is expected based on current forecasts either.

Lufthansa EPS/Dividend Estimates (TIKR.com/S&P Global)

{kind=link}

2023E is the earliest we're currently expecting this. Again, this just doesn't work for me. Current forecasts and PTs call for an analyst average of €5.25 on the low side to €9.8 on the high side, and we're currently at €8.1. That means Lufthansa is overvalued to current average PTs of around €8, if only slightly. I agree with the overvaluation. Only 1 out of 13 analysts has an "outperform" rating on Lufthansa here, with 10 at "Hold" and more than 1 at underperform/sell.

While Lufthansa had a great quarter, it has not convinced me - or the broader market analysts following the company. The company is still above €6.5/share. This just doesn't work for me - and I wouldn't buy it above €6.5. Even if it were to drop to that, I would first look at alternatives.

The recent outperformance and expectations for 2022E mean that I'm paying much closer attention to Lufthansa here. But I'm nowhere close yet to changing my thesis on the company to be a bullish one.

There are too many quality companies for sale for that.

Thesis

My thesis on Lufthansa is as follows:

- This incumbent airline has been on a rollercoaster ride since early 2002. 20-year returns for Lufthansa are negative without the dividend, making it a terrible investment.

- There is the real potential for a turnaround somewhere between 2023-2024, but this does not yet warrant a change in my Lufthansa thesis.

- Because of this, I am continuing my coverage on SA on Lufthansa with a "Hold" rating. I still believe that Lufthansa should not be part of any conservative portfolio, even at the risk of some sort of upside here.

Remember, I'm all about :

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company still fulfills none of my investment criteria, dictating the "Hold".

For further details see:

Deutsche Lufthansa: Nope, Stock Is Still Overvalued