DLAKF - Deutsche Lufthansa: Travel Is Back Time To Look Ahead (Rating Upgrade)

2023-09-07 04:14:35 ET

Summary

- Post Q1, here at the Lab, we had some concerns. The agreement of the pilot contract is a significant development.

- Global demand is expected to grow, and Deutsche Lufthansa has a better balance sheet vs. the pre-COVID-19 level.

- Lufthansa increased the guidance and will be back to pay a dividend. We decided to move our rating to an overweight.

This was the airlines' summer recovery. Despite economic uncertainty and inflation, the industry is booming, considering the high ticket prices. While Wall Street analysts doubt long-term sustainability, airlines see no reduction in this trend and view travel as a consumers' top priority. Business travel is still far from the levels reached before the pandemic; however, it's growing, and the leisure segment is almost back to 2019 numbers. According to IATA (International Air Transport Association), international travel has reached about 90% of pre-pandemic levels this year, and looking at Moody's latest report, air transport global demand estimates will grow by 22% year-on-year in 2023 with a plus 6% in 2024. For the first time, airlines are enjoying this year without a pandemic and strikes. This latter issue was avoided by increasing pilot and staff salaries. Solid demand and double-digit increases in airline tickets pushed carriers to revise the financial results for the current year upwards. This was the case for the German airline company Deutsche Lufthansa AG ([[DLAKF]], [[DLAKY]]).

Lufthansa current upside

- Lufthansa exceeded 90% of bookings compared to pre-pandemic levels. At the same time, Air France-KLM group plans to return to pre-COVID capacity in 2024, a goal already achieved by low-cost Ryanair in the last quarter thanks to 123.5 million passengers transported, up by 23% vs. the pandemic outbreaks. Travel recovery is picking up;

- In Q1, we had some concerns, while Lufthansa's risks are better understood today. In detail, Cargo profitability has weakened, and the market is now forecasting earnings at this cycle;

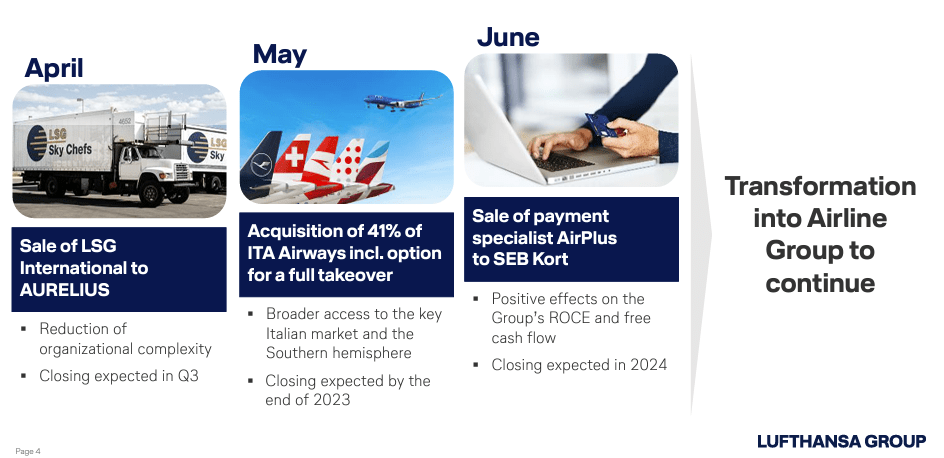

- Even if we view the ITA deal positively , we should report that if the Italian company does not reach breakeven under the current deal terms, Lufthansa will not exercise its option to take majority control. This offers downside protection that cannot go unnoticed and most likely will be appreciated by Wall Street analysts. Going to the disposal, even if LSG might be delayed (Fig 2), we are not discouraged by the current management progress, and we prefer to be patient and achieve a lower price than expected;

- Supportive of the company's development is the new contract renewal. The company concluded a favorable deal with the pilot union. Here are the details of the pay increase: +7% December 2023, +5% January 2025, and +5% January 2026. This is notably less than the renewed contract offered by US carriers;

- To support Lufthansa MACRO investment view is the airline supply constraints development . Aircraft delivery delays and lack of spare parts will favor current airlines that haven't reached total capacity;

{kind=link}

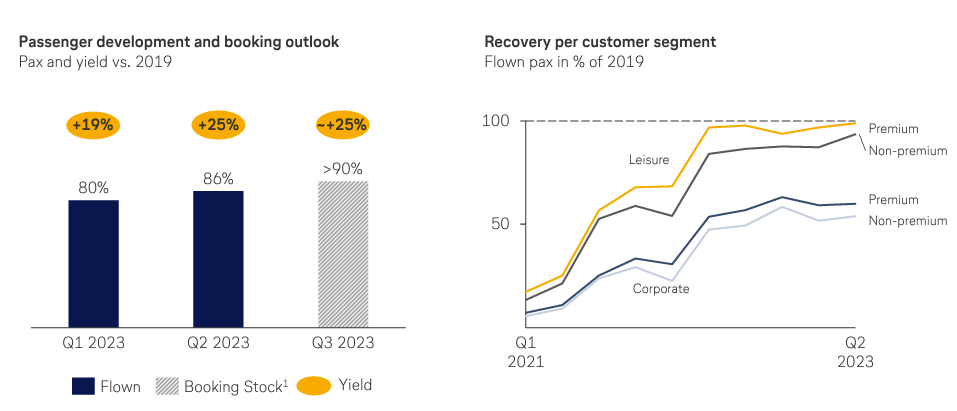

Source: Deutsche Lufthansa Q2 results presentation - Fig 1

{kind=link}

Fig 2

Post Q2 results, these are our main highlights for the following period:

- Despite lowering the company's 2023 capacity plan to 85% (from 85-90%), Lufthansa raised the 2023 guidance with a core operating profit of €2.6 billion. In addition, the group confirmed its 2024 financial objectives (Fig 3);

- Demand remains high even post-summer, with the premium segment currently outperforming;

- Business travel is now recovering, and Q3 booking has a 25% higher yield compared to the pre-pandemic level (Fig 1);

- On a negative basis, the company now expects the unit cost to increase low-single-digit, and the new EBIT estimates are better than expected, supported by the higher yield, which offset the company's inflationary pressure. In the Q&A call, the CEO explained that is confident of reducing 2024 unit costs thanks to productivity gains and capacity ramp-up (Fig 4);

- In our estimates, we are implying an unchanged fuel cost of €7.55 billion;

- Key to note is the dividend evolution, which is expected to be resumed. According to our future estimates, considering a payout of 30% on 2023 numbers, we arrived at a dividend yield of 5%;

- On a negative note, we should see the net pension liability development. Pension increased to €2.3 billion from €2.0 billion due to a lower discount rate. Considering the net debt development, including pensions, we anticipate an improvement of 1.7x. This ratio is better than the 2019 numbers, when Lufthansa had an investment grade rating and a net debt/EBITDA at 2.8x (Fig 5).

For further details see:

Deutsche Lufthansa: Travel Is Back, Time To Look Ahead (Rating Upgrade)