AMZN - Deutsche Post: No More Significant Upside Potential From Here

2023-04-20 18:01:15 ET

Summary

- Deutsche Post is a high-quality and well-managed European company that benefits from the growing e-commerce sector.

- In 2022 Deutsche Post delivered a record financial performance, however, the management lowered their forecast for 2023 and 2024.

- Considering the significant rise of the stock by over 40% in recent months, it seems there may not be any further upside potential for Deutsche Post right now.

Geographical diversification is essential for investors who want to manage risk, smooth out portfolio performance, tap into different industries and sectors, and provide currency diversification. While we all know, investing in stocks can be risky, spreading investments across different countries can help mitigate these risks and provide more opportunities for investors to achieve their investment goals. That's why I am constantly on the lookout for investment opportunities outside of the US, as most of my portfolio is currently allocated there, approximately 85%.

I think Deutsche Post ( DPSTF , DPSGY ) can generally be such an investing opportunity since the company is poised to benefit from the tailwinds of e-commerce and the ongoing globalization. However, the current valuation and the projected declining financials over the next two years suggest that DPSGY is a Hold right now.

Overview

Deutsche Post, commonly known as DHL, is a German multinational package delivery and supply chain management company. It is one of the world's largest courier companies and provides a wide range of logistics services to customers in more than 220 countries and territories. The company has a market capitalization of approximately $52B.

Geographically, DPSGY's business breaks down as follows:

Geographical Diversification DHL (Data: marketscreener.com)

Currently they still heavily rely on their home market in Germany, but the management is increasingly trying to position the company more globally. In 2007 more than 50% of DHL's EBIT came from Post and Parcel in Germany, while for 2022 it was only 14% of the EBIT .

Looking at the revenue of the different business in which Deutsche Post operates its business can be divided like this:

Diversification DHL (Data: marketscreener.com)

Industry And Competitive Analysis

The logistics industry has experienced strong growth over the past few years, driven by the growth of e-commerce and especially due to Covid-19. As a result, there is intense competition in the market, with major players like FedEx ( FDX ), United Parcel Service ( UPS ), and Amazon ( AMZN ) also vying for market share.

You can see how the revenue of FedEx, UPS and DPSGY jumped from around $70B in 2019 to almost $100B now in 2023.

Despite this competition, Deutsche Post has maintained its position as a leading player in the logistics industry and was also able to constantly increase their operating margin over the years. As a result, DPSGY has achieved an great operating margin ((TTM)) of roughly 8.6%, which comfortably surpasses one of its major competitors, FedEx. However, as illustrated below, the company still trails behind another significant competitor, UPS, by a comfortable margin.

Nevertheless, a remarkable development up from 4% in 2016. That's why it's no surprise that Seeking Alpha gives Deutsche Post currently a Profitability Grade of "A+":

seekingalpha.com/symbol/DPSGY/profitability

To further put the competitors in context with DHL, I created the following matrix with additional key metrics.

Data: seekingalpha.com

The comparative analysis shows that UPS outperforms the other two companies in terms of quality. Deutsche Post secures a strong second place with more of a tendency towards first place than towards FedEx, which currently appears to be the company with the lowest quality out of the three.

As a quick side note, it's worth highlighting that DPSGY is deeply committed to achieving net-zero emissions by 2050 through their " Mission 2050 " initiative, and they are prepared to invest €7B by 2030 to bring this vision to life. Already, they have made significant strides by integrating electric vehicles into their package delivery operations. One of these EVs can be seen above in the title picture. This impressive plan illustrates the dedication of Deutsche Post's management to innovation.

Financial Performance And Outlook

In its most recent quarterly report , DPSGY reported strong financial performance. The company's revenue for 2022 was €94B, which represents a 15.5% increase compared to last year. The company's EBIT was €8.4B, which represents a 5.7% increase year-over-year and Deutsche Post's EPS for 2022 was €4.4, which is a 7.6% improvement YoY.

Their latest and future predicted Finances can be seen in the visualization below:

Top and bottom line of DHL (Data: marketscreener.com)

The upward trajectory depicted in the chart above is truly impressive, particularly from 2019 to 2022. However, upon extending the time horizon, it becomes apparent that the growth during these years was an anomaly, and the revenue has grown at a Compound Annual Growth Rate ((CAGR)) of approximately 5.5% over the last decade.

Data: aktie.traderfox.com

That's why we see the also above indicated decrease in projected revenue and operating profit for 2023 and 2024, which can be attributed to a range of macroeconomic challenges and to the reversion to the means after the extraordinary growth from 2019 to 2022. Deutsche Post has proactively acknowledged these issues and addressed them in their latest investor presentation . Furthermore, Tobias Meyer , the incoming CEO as of May 2023, has expressed confidence in the company's ability to weather the downturn, stating that the management team "know[s] which levers to pull during downturns and [they] are going into the current cycle in [their] best shape ever. Thus, [they] aim for a balanced approach between stringent mitigation actions and continued targeted investment."

Meyer also mentioned that even in the "Great Financial Crisis" volumes returned to year-over-year growth after four to six quarters and they explained their internal modelling assumptions for 2023. These can be seen below:

Q4 2022 Investor Presentation

Based on these different modelling assumptions for 2023, Deutsche Post gave the following EBIT guidance for 2023:

- V-shape: ~ €7.0B

- U-shape: ~ €6.5B

- L-shape: > €6.0B

Overall, the Group EBIT guidance for this year is therefore €6.0-7.0B. Down from €8.4B in 2022.

The management also mentioned their strong globally diversified portfolio. The key metrics are summarized here:

Q4 2022 Investor Presentation

Last but not least the management laid emphasis on the high ROCE the company achieved over the last years. DHL managed to increase their ROCE from 9% in 2018 to 18% in 2022 and even 25% when excluding goodwill:

Q4 2022 Investor Presentation

Considering all the factors mentioned, it is apparent that DHL will struggle over the next two years. However, I still generally maintain a positive outlook on the future of the company, even though projected financials may decline. Although pandemic-fueled growth will certainly cool down and will lead to a decline in both top and bottom line, DHL remains in a good position to capitalize from the still growing e-commerce segment after 2024.

Global E-Commerce Growth (Data: statista.com)

However, I anticipate that the future growth trajectory after 2024 will align more closely with the stable Compound Annual Growth Rate ((CAGR)) of 5.5% witnessed over the past decade, rather than the extraordinary surge that was observed from 2019 to 2022.

Things To Like

Backed by the German Government

One interesting thing about the shareholders of Deutsche Post is, that the biggest shareholder, holding roughly 20% of the company, is the government of Germany . This is also where the name "Deutsche Post" comes from, which translates to "German Postal Service". As a result, DHL is backed by the German Government.

The fact that the German government is the largest shareholder in Deutsche Post is significant for several reasons. One of the most notable implications of this ownership structure is that the government has a direct stake in the success of the company. This means that the government is likely to be more invested in the long-term growth and sustainability of the company than other shareholders who may be primarily focused on short-term returns.

The fact that Deutsche Post is backed by the German government provides a level of financial stability and security for the company. This is particularly relevant in times of economic uncertainty, when investors may be more cautious and risk-averse. The government's backing could help to reassure investors and provide a measure of stability to the company's operations and financial performance.

Decreasing Uncertainty In Europe

Europe's geopolitical problems with the Russia-Ukraine war and the high inflation in Europe have negatively influenced almost all European stocks.

The near-term outlook for European stocks is expected to become clearer over the coming years, as inflation begins to ease due to a more relaxed energy sector, which can be seen here in this summary of the inflation trends in Europe and its primary components:

Development Of Inflation In Europe (Source: ec.europa.eu)

The positive shift in the European stock market can already be seen below as the downturn resulting from the war, which started in February 2022, has almost already been fully recuperated.

Dividend

DPSGY also pays a hefty and continuous dividend. With a current Payout Ratio of 37% this dividend also seems to be safe:

The management also announced a new yearly dividend of €1.85, up from €1.8, which represents a current dividend yield of 4.0% .

Buybacks

Furthermore, the company extended their share buyback program from €2B to €3B, which will be executed until December 2024 which might boost the stock price. This also underlines the management's confidence in the company and could also express that the company is currently attractively valued according to the management.

Q4 2022 Investor Presentation

Risks To Consider

Highly Cyclical

As one of the world's largest logistics companies, Deutsche Post relies heavily on the demand for shipping and delivery services from businesses and consumers alike. If the economy experiences a slowdown or recession, businesses may reduce their orders and consumers may cut back on their purchases, resulting in a decrease in shipping and delivery volumes. In addition, the logistics industry is highly cyclical and tends to be closely tied to economic conditions. If there is a downturn in the economy, it could lead to a decline in global trade and a reduction in the movement of goods, further reducing demand for Deutsche Post's services. A decrease in demand for its services could have a direct impact on Deutsche Post's revenue and profitability, which could cause its stock price to decline. This could be further exacerbated if the company is unable to adjust its cost structure to align with the reduced demand, leading to margin pressure and further financial challenges.

However, as already mentioned above, the management of DHL is aware of the potential risks of a macroeconomic downturn and is already taking the following measures to mitigate risks:

Q4 2022 Investor Presentation

Impacts of COVID-19

The COVID-19 pandemic has disrupted supply chains and logistics operations globally, posing significant challenges for companies like Deutsche Post. This includes labor shortages and transportation disruptions, which have led to delays and increased costs for shipping and delivery services. Furthermore, the pandemic has spurred a trend towards localization and re-shoring of production, as many companies seek to reduce their dependence on global supply chains and mitigate the risk of future disruptions. This could have a negative impact on Deutsche Post's business, particularly if more companies choose to produce goods locally instead of relying on international shipping and delivery services. However, despite these challenges, there are reasons to believe that Deutsche Post will be able to weather the storm and continue to grow its business. The growth of e-commerce has been a major tailwind for the company in recent years, and this trend is expected to continue as more consumers shift toward online shopping, which is illustrated in the chart below.

statista.com

Moreover, while the pandemic has created short-term challenges, it has also highlighted the importance of resilient and flexible supply chains , which could drive increased demand for Deutsche Post's services in the long run.

Competition

Investors considering an investment in Deutsche Post should also be aware of the growing competition in the logistics sector, particularly from companies like Amazon. It's worth noting that Amazon happens to be a major customer of DHL, but the e-commerce behemoth is gradually relying more on its own logistics network for package delivery. This development is visualized in this graph, which shows the Amazon packages by shipping provider in Germany.

Data: statista.com

In addition, it's worth considering that Amazon presently only delivers its own packages. However, given the excess warehouse capacity resulting from overbuilding , it's not entirely implausible for Amazon to utilize its additional logistical capacity to deliver packages for competitors and other businesses as well.

Valuation

After gaining a comprehensive understanding of DHL's diversified business segments and geographical presence, its competitors and their relative performances, along with the company's recent track record and future prospects, taking into account the management and shareholder structure, as well as potential risks, we can now jump right into the most exciting part of every stock analysis: The Valuation

Deutsche Post is an exceptional company, but it is expected to face challenges in the coming years. The management has taken notice of these issues and has publicly addressed them. As a result, the stock price should reflect the uncertainty surrounding the company's future and the projected decrease in both top and bottom lines in 2023 and 2024.

Despite these challenges, the company can still present an attractive investment opportunity if the valuation is appropriate. As investors, we could benefit from purchasing the stock at a discounted price, or we could enjoy a substantial dividend while we wait for the company to turn things around.

At the first glance this is also the case:

In their latest earnings call the management of DPSGY confirmed an EBIT-guidance of €8B for 2025. With a market cap of roughly $56B (€51B) , that means that the company is trading at a low valuation of 6.3x 2025 expected EBIT. With considering the 5y average EV/EBIT of 8.7 from DHL, this implies a upside of around 35%.

Deutsche Post is currently trading at a PE of around 10.5. This seems also cheap considering the average PE-ratio over the last 5 years was at 14.6.

Even when looking at its peers, DPSGY remains to look attractively valued. With FedEx (FDX) trading at a PE of 19.1 and United Parcel Service (UPS) trading at 14.4.

Even Seeking Alpha currently gives Deutsche Post an attractive valuation metric and rates it with a Valuation Grade of "B+":

seekingalpha.com/symbol/DPSGY/valuation/metrics

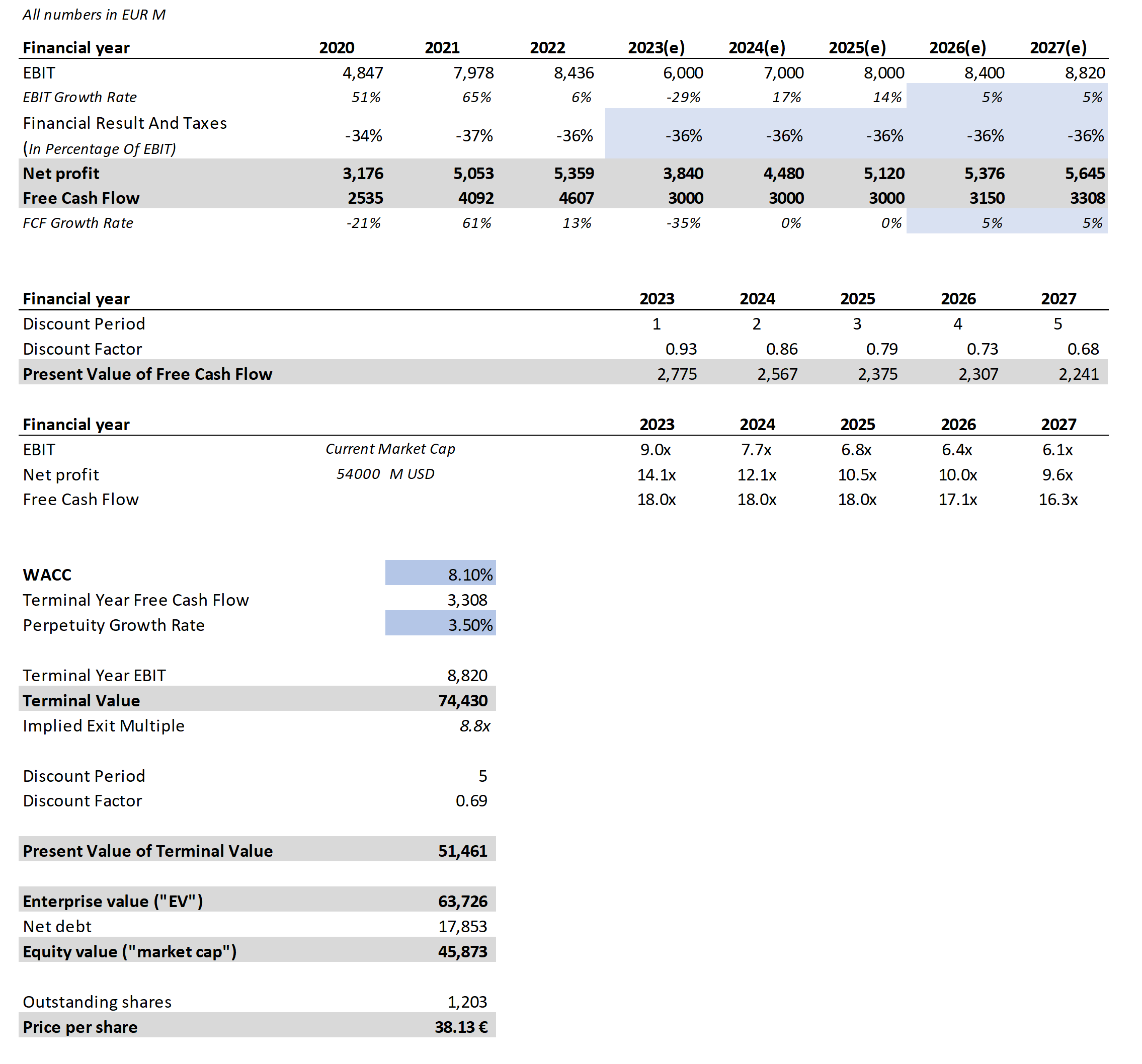

However, to perform a comprehensive valuation of DHL, taking into account the anticipated decline in financials over the next two years, I conducted a DCF analysis. The blue cells in the analysis represent the assumptions made to evaluate DHL. Here is a brief overview of how I calculated and predicted the future prospects of Deutsche Post:

- EBIT: 2023: €6.0B is the worst case EBIT scenario (L-shape) for 2023 according to the latest investors presentation. 2024 - 2025: €8.0B EBIT is the management's mid-term guidance for 2025. Therefore €7.0B, so the middle between €6.0B and €8.0B, seemed an suitable assumption. 2026 - 2027: I assumed a 5% EBIT-CAGR for this period because DHL's EBIT before Covid-19 grew an average of 7% .

- Financial Result And Taxes: I averaged the values of the last three years and therefore used 36% to predict the net profit for the years 2023 to 2027.

- Free Cash Flow: 2023: A free Cash Flow of around €3.0B is the current guidance of DHL.2024 - 2025: For the years 2023 to 2025 the management expects a cumulative Cash Flow of €9.0B to €11.0B to stay conservative, I used €3.0B in all three years, so a cumulative Cash Flow of € 9.0B. 2026 - 2027: For this period I predict a CAGR of around 5%, which is a bit lower than their current 10y CAGR of 7,6% .

- WACC: As per Gurufocus , DHL's WACC is currently at 8.1%.

- Perpetuity Growth Rate: The perpetuity growth rate assumed for the analysis is 3.5%.

Data: seekingalpha.com, https://reporting-hub.dpdhl.com/en/

{kind=link}

Based on this Discounted Cash Flow analysis, the calculated share price for DHL is €38.13 or currently $41,85. This suggests that DHL is currently trading around 10% above its fair value.

Taking into account all the uncertainties, risks, and facts mentioned earlier, my rating for Deutsche Post at present is a HOLD. If the valuation expands in the next months, I would even consider to further downgrade the stock to a Sell rating.

Conclusion

In summary, Deutsche Post is a well-managed company with a robust financial position and a leading presence in the logistics industry. While the company witnessed exceptional growth from 2019 to 2022, it is currently facing growth challenges.

Although facing upcoming challenges, the company's valuation remains relatively high, leaving investors without appropriate compensation for the potential risks of investing in DHL. Investors looking for exposure to the logistics industry and high-quality European and/or German stocks however may consider adding Deutsche Post to their watchlist and wait for a potential entry point at a lower valuation. While waiting for this opportunity I rate the stock as a HOLD.

For further details see:

Deutsche Post: No More Significant Upside Potential From Here