DTEGY - Deutsche Telekom Q2 Earnings: Still A Gem In The Telecom Industry (Upgrade)

2023-08-10 13:22:07 ET

Summary

- Deutsche Telekom AG's Q2 results show operational stability and resilience, allowing management to upgrade the FY23 outlook.

- The company once more showed in the first half of the year that it is very well capable of continuously growing customers across all regions and taking market share.

- Deutsche Telekom's impressive EPS growth outlook, proactive debt reduction efforts, and strong financial position make it well positioned for substantial and enduring growth.

- Following another solid quarter and a 10% drop in the share price since I last covered the company, the risk-reward profile has improved, allowing for a rating upgrade.

Investment thesis

I upgrade my rating on Deutsche Telekom AG ( DTEGY ) from a Buy to a Strong Buy and update my revenue and EPS estimates following the company's Q2 results , which once more showed operational stability and resilience. Furthermore, with the share price down 10% since my previous article following an overreaction on a news headline, I believe shares offer incredible value once more, allowing for a rating upgrade.

Positioned as a global leader in the telecommunications sector, this company holds the distinction of being the largest in Europe and a prominent player on the global stage. What truly captures my enthusiasm is its extensive footprint spanning both Europe and the United States. With strategic ownership of over 50% in T-Mobile US, Inc. ( TMUS ), Deutsche Telekom has strategically established its presence across both continents. Operating across various telecommunications segments, including mobile subscriptions, fixed-network lines, and wireless networks, this industry giant showcases a robust competitive advantage. This advantage ensures revenue stability and predictability and empowers it to thrive during challenging periods.

Though, Deutsche Telekom's appeal as an investment goes beyond its stability, competitive advantage, and essential product offerings. The company's impressive EPS growth outlook is underpinned by the expectation of significant margin expansion in the years ahead. Additionally, its proactive debt reduction efforts have strengthened its financial position. Today, in my eyes, Deutsche Telekom stands out as one of the most strongly positioned telecom corporations globally, poised for substantial and enduring growth.

Furthermore, Deutsche Telekom has demonstrated resilience and steady performance throughout the first half of 2022, even in the face of challenging macroeconomic conditions. The H1 performance surpassed expectations, leading to an upgraded FY23 EBITDA AL outlook.

Considering DT's prudent management, consistent growth, and impressive margin profile, the company's outlook remains promising. A bullish stance is further supported by the European and German telecom markets' growth potential, coupled with DT's strategic investments. The overreaction to Amazon-related rumors presents an attractive entry point, especially as the company's valuation appears undervalued compared to peers.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

Deutsche Telekom continues to perform steadily

The first half of the 2022 fiscal year has been a solid one for Deutsche Telekom, leaving investors with very little to complain about, especially when considering the number of macroeconomic headwinds, including inflation and monetary tightening, we have seen over the last year. DT management indicated that high inflation levels continue to pressure consumer purchasing power, which has a negative effect on the amount consumers are willing to spend on DT mobile and broadband contracts. Furthermore, DT continues to act diligently as it sees a number of headwinds and risks remain in the second half of the year, with inflation turning out to be sticky and more aggressive tightening of monetary policy. Still, this did not stop management from upgrading their FY23 EBITDA AL outlook for the second time this year. The H1 performance exceeded expectations and allowed for this upgrade despite the number of headwinds.

Net revenues decreased by 1% in H1 (0.4% organic) to €55.1 billion as the company was lapping a strong 1H22 (in part due to strong currency tailwinds that year) and was impacted by lower revenue from T-Mobile US and the sale of T-Mobile Netherlands. Positively, service revenue was up 2.5% YoY (2.9% organically) as the reported revenue decline was primarily driven by weakness in equipment sales following the weakness in consumer spending power. Growth in the more valuable service revenue was more resistant due to longer-term contracts and the simple necessity of mobile 4G and 5G services.

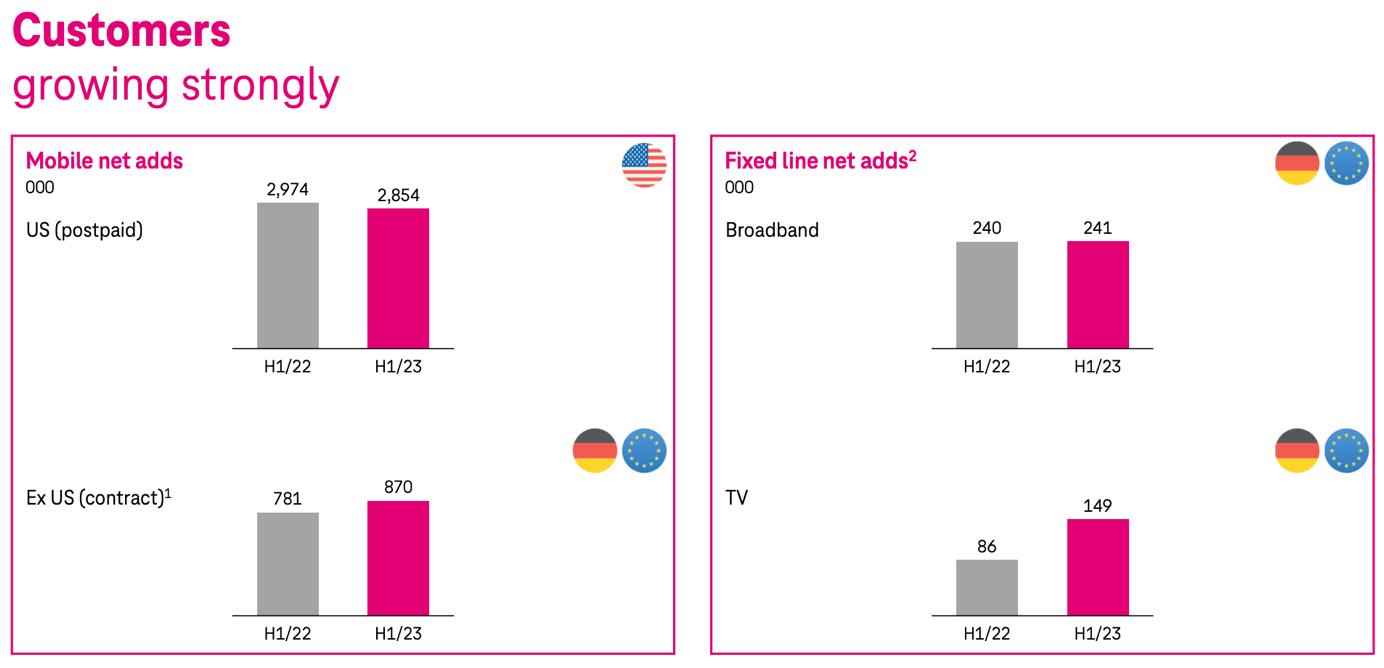

Meanwhile, the Germany and Europe segments reported impressive growth of 2.4% and 5%, respectively. The solid performance was driven by strong subscriber numbers that keep growing as mobile customers were up 2% YoY, and broadband customers up 2.8% YoY, which are solid numbers when considering the company already is one of the largest telecom providers in the world.

At the same time, the company has meaningfully improved its profitability in the first half of the year as the adjusted EBITDA AL margin expanded by 80 basis points, driving adjusted EBITDA AL up 1.2% (2.4% organic), despite the top-line decline, to €20 billion. Even more impressive, free cash flow for H1 came in 15.7% higher than the same period last year at €9.7 billion. The excellent free cash flow generation combined with the sales of GD Towers allowed DT to lower its debt position by 6.3% to €137 billion, against a cash position of €8.7 billion, also up 3% since the start of the year. This shows that DT’s excellent performance has resulted in a significant improvement in its balance sheet health. As a result, S&P Global upgraded its long-term rating of Deutsche Telekom AG from BBB to BBB+ with a stable outlook.

As indicated before, Deutsche Telekom sold 51% of the cell tower business in Germany and Austria for a total of €10.7 billion. Deutsche Telekom still owns the remaining 49% of the business, valued at €6.1 billion. This also significantly benefitted its reported EPS results, but excluding these special factors, DT reported an EPS of €0.77, down 18.1% YoY as a result of positive one-time benefits in the year-ago first half.

Overall, this quarter once more confirmed my bullish stance toward the company. It shows that it is able to report strong results through the economic cycles and that its offering is sticky. Furthermore, it is rapidly improving its financial position and margin profile, which should drive impressive growth in EBITDA, EPS, and free cash flow going forward, allowing the company to deleverage its balance sheet further. Also, it continues to report solid customer growth numbers and strong respective positions across its regions. As a result, I continue to view the company as the best choice in the telecom industry.

All regions contributed to growth, but I remain especially bullish on the German and U.S. segments

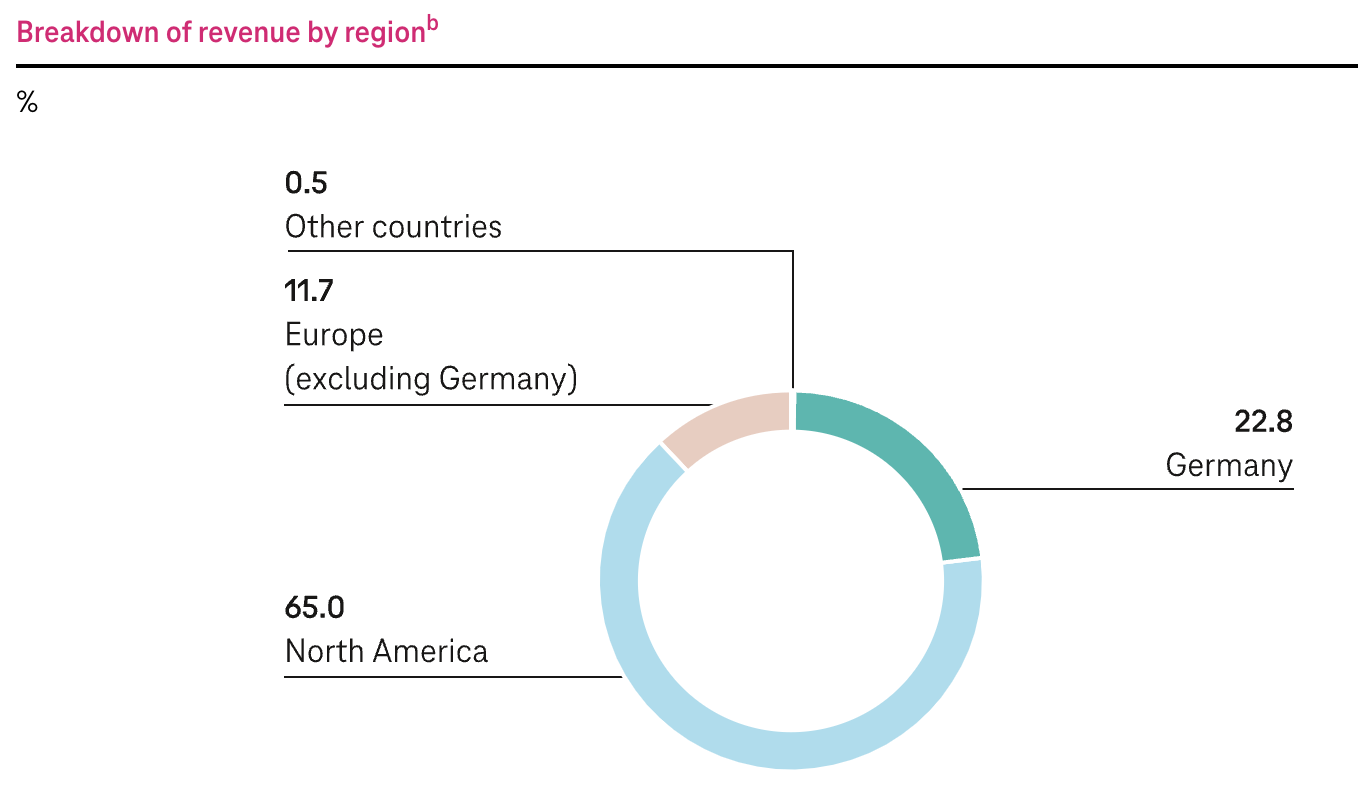

Diving a little deeper into the H1 performance by region, as indicated before, the Europe segment was the strongest performing one as this reported revenue growth of 5% YoY to €5.7 billion, now accounting for 11.7% of DT’s total revenue. A strong increase in mobile services revenues mainly drove H1 growth in Europe. Mobile customers increased by 2.4% YoY and broadband customers were up 5% YoY, driven by the rollout of 5G coverage and state-of-the-art optical fiber. In terms of profitability, EBITDA AL for this segment was up 2.3% to €2 billion, making it the slowest growing segment in terms of EBITDA AL. The margin stood at 35%, down 1pp.

The European market is expected to grow at a CAGR of slightly below 3% through 2028 . Yet, I expect DT to grow at a slightly faster rate as it keeps investing in expanding its European offering and continues to take market share. I believe we could see DT grow its European revenues at a CAGR of between 3% and 3.5% over the remainder of the decade. Still, it will most likely remain its smallest and slowest growing segment. The company could potentially sell its business in more European countries, after already selling the telecom business in the Netherlands last year, if it feels the offer is right and growth potential is limited. Focusing investments on the German and U.S. markets could potentially be a better strategy. If the company goes in this direction, growth rates will fluctuate as a result.

Deutsche Telekom revenue by region as of 1H23 (Deutsche Telekom)

{kind=link}

Moving to the Germany segment, this one also reported very decent revenue growth of 2.4% to €12.3 billion (1.7% organic growth), now accounting for a significant 22.8% of DT’s H1 revenue. Growth in the first half was driven by solid growth in service revenues for both fixed and mobile networks, up 2.4%. Mobile customers increased by a significant 5.8% YoY, highlighting that the business is still capable of growing its customer numbers in its home region despite already holding a significant 37% market share in the country. Furthermore, the number of broadband customers increased by 1.9%, with the industry-leading optical fiber solution growing over 15% YoY as Deutsche Telekom is migrating its customers to this improved, but also more expensive, solution.

With the German telecom market expected to grow at a solid 5.53% CAGR through 2028 , I expect Deutsche Telekom to keep reporting decent growth in the country as it is well-positioned to increase its market share. The company has the best 5G coverage among its competitors as this is now available to 95.3 % of the German population and after rapidly expanding its fiber-optic network over recent years, a total of 6.2 million households have the option of a direct connection, which should continue to boost broadband growth over the next several years for DT. As a result of these aspects, I would not be surprised if DT will be able to report revenue growth at a CAGR of above 5% through 2028 for the German segment.

Finally, the EBITDA AL all for this segment was up a more impressive 4% to €4.8 billion in H1, driven by growth in higher margin service revenues and improved cost efficiencies, driving the margin up to 40.8%. The company lowered its headcount in Germany and drove further efficiencies by new technology integrations. I expect the margin for this segment to keep expanding over the next several years as efficiencies improve.

1H23 data Deutsche Telekom (Deutsche Telekom)

{kind=link}

The U.S. segment, which practically is T-Mobile US, reported a revenue decline of 1.4% in H1 to €35.8 billion or 65% of DT’s H1 revenue as T-Mobile US reported a decline of 2.5% YoY. The decline was driven mainly by lower equipment revenues as consumers are less willing to spend large sums of cash on new phones, for example. Up 3.9% YoY service revenues could partially offset the equipment revenue decline.

Meanwhile, customer growth remained very impressive as this grew 6% YoY to 116,602, easily outpacing all of its peers. Net customer additions of 1.6 million in Q2 even allowed management to raise its FY23 guidance and was driven by 760 thousand postpaid phone net customer additions, which was the best Q2 result in 8 years. Also, churn came in at 0.77% and stood at an all-time and industry-leading low. Furthermore, T-Mobile US’ 5G network now covers around 98% of the U.S. population, giving it excellent coverage to grow its customer base. Finally, while revenue growth for the U.S. segment came in negative, the same can’t be said about growth in the EBITDA AL as this was up a very strong 4.6% YoY to €13 billion.

Crucially, DT increased its stake in the first half of the year to over the 50% target and now holds a stake of 51.3% in the T-Mobile US business. The exposure to T-Mobile US is something I continue to view as very positive. The company is the best-performing telecom company in the U.S., reporting incredible customer growth across all product categories, massively outperforming peers. This makes me confident in the company’s long-term growth prospects and as this continues to outgrow peers and take a larger market share in the U.S. telecom market, this will benefit Deutsche Telekom financially as well.

With the U.S. telecom services market expected to grow at a CAGR of 6.5% through 2030, I believe T-Mobile US should be able to report growth of around that level as well, potentially even slightly higher if it remains able to outgrow peers and take a larger market share. With DT already holding a stake of over 51% in the business, this will meaningfully benefit this company as well. The U.S. will most likely remain its most important growth engine.

Rumors of Amazon entering the telecom arena caused a massive overreaction

During the last quarter, the news surfaced that Amazon ( AMZN ) might be considering offering a cheap or even free mobile subscription for its Prime customers. As a result, telecom stocks plummeted, including Deutsche Telekom which lost over 10% in a couple of days’ time and has since had trouble recovering these losses. According to the Bloomberg report, Amazon would be negotiating with the likes of T-Mobile US, Verizon (VZ), and Dish Network (DISH), all of which have denied these claims stating that there are no ongoing negations whatsoever with Amazon. Even Amazon denied these rumors and has said to have no interest in entering the telecom industry at this point in time. Still, this does not mean it is not happening.

From certain aspects, a move like this makes sense for Amazon. It could strengthen its prime offering to lure more consumers into subscribing to the service, which would not hurt the company as it is seeing increased competition from the likes of Walmart (WMT), for example. The most obvious way to execute here is to purchase data from a carrier like Dish or T-Mobile with a strong network without owning a network itself. This would make it a virtual network operator. Yet, this will cost Amazon quite a bit if it wants to offer such a subscription for below $10 or even free. This would increase costs for Amazon and expose it to a highly competitive business at a time when it is looking to boost margins and profits to satisfy investors.

So, while I can see the upside for Amazon, a move like this is highly unlikely anytime soon. Furthermore, I believe the impact on Deutsche Telekom should be relatively limited as it has absolutely no impact on the European business, and I expect it to have a limited effect on T-Mobile US as well. T-Mobile US should have enough firing power and room for growth to keep growing at a decent pace. Yet, it could cost some percentage points in annual growth if Amazon starts to compete. Still, a 10% share price drop is a clear overreaction to these rumors and as all parties have denied these negotiations or plans, I do not yet see a reason to discount the company because of it. These types of overreactions are the ones investors should benefit from.

Outlook & valuation

Following the strong and better-than-expected first-half performance, management has raised its adjusted EBITDA AL guidance for the second time this year and now expects to report an adjusted EBITDA AL of €41 billion, up from a €38.8 billion expectation at the start of the year and representing 4% YoY growth. In addition, management also expects the free cash flow ("FCF") to come in above previous expectations but has maintained its guidance of FCF above €16 billion, although a level of €16.2 billion seems likely. Furthermore, management maintained its EPS guidance of above €1.60, up 6% from the FY22 level when excluding one-off benefits.

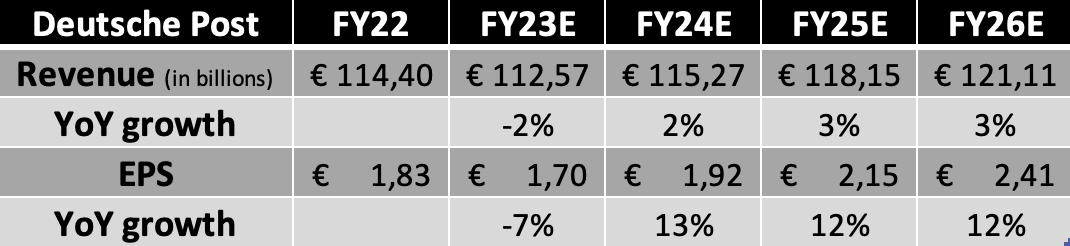

Following this guidance upgrade and the steady Q2 and H1 performance, I now expect the following financial results through FY26.

Financial estimates (By Author)

{kind=link}

Shortly explaining these estimates, I have slightly lowered my revenue growth estimate for FY23 by about 40 basis points as revenue last quarter was slightly below my estimates and I expect revenue growth to remain subdued in the second half of the year. Meanwhile, I have quite significantly upgraded my EPS estimate as margins so far this year have come in way higher than I previously anticipated and this allowed for a meaningful EPS upgrade. The margin development for DT is incredibly promising and should drive significant EPS and FCF growth over the next several years as well.

My revenue estimates for the following years remain unchanged, but my EPS estimates have increased slightly due to the earlier-mentioned positive margin development. DT has already guided for recurring EPS of above €1.75 for FY24, projecting significant margin improvement, especially from its stake in T-Mobile US and positive developments in its German business. This creates a stellar EPS and FCF growth outlook, which should also allow for meaningful growth in its share price.

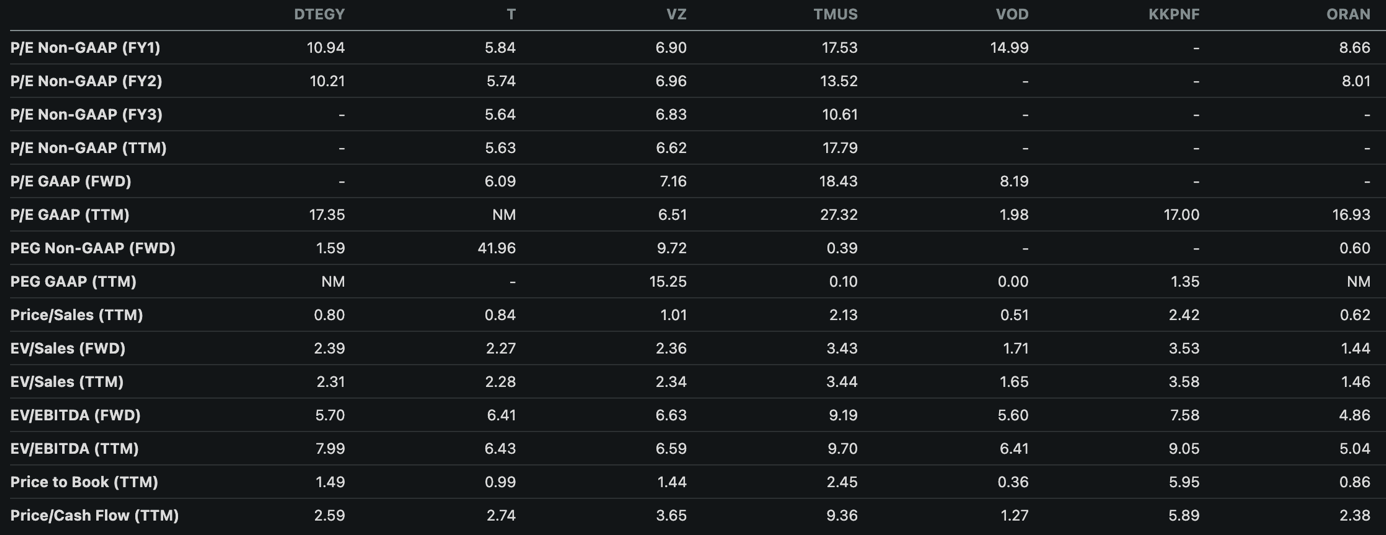

Moving to the valuation, shares are currently valued at a forward P/E of 11x, down from 13x three months ago as the share price has dropped by over 10% (largely due to the Amazon rumors), while the EPS estimates from both analysts and myself have come up. When comparing DT’s valuation to that of its peers, the company remains one of the cheapest options out there when looking at metrics like price/FCF, EV/EBITDA, and P/S. This is even though the company has by far the strongest earnings and FCF growth outlook and remains an industry leader in its respective regions.

Peer comparison (Seeking Alpha)

{kind=link}

As I previously stated:

“considering the impressive EPS growth projected for the next couple of years by me and analysts alike, the excellent consistency in the business, the strong outlook, and product necessity, I believe shares are still attractively priced.”

I believe a P/E of at least 13x is fair for this high-quality telecom giant.

Based on this belief and my FY24 EPS estimate, I calculate a target price of €25, up from a previous €24, and leaving an upside of 33.5% from a current share price of €18.70.

Conclusion

Deutsche Telekom delivered very steady quarterly results that contained very little surprises and I believe investors have very little to wish for. The company consistently delivers decent results, takes market share, invests, and continues to grow its customer base despite its already incredibly large size and the fact that it operates in a very mature industry.

Following these quarterly results, I remain very bullish on the company. It seems excellently positioned to benefit from industry growth and take market share over the next several years. Especially its exposure to T-Mobile US through a 51% stake in the company should mean that it will continue to grow steadily. Furthermore, the company is focused on increasing cost and operational efficiencies, which should lead to meaningful margin improvements and rapid EPS and FCF growth. Also, since management reached its target of acquiring a stake in TMUS of over 50%, I expect more significant dividend hikes over the next several years to boost the dividend yield and possibly some share repurchase programs to further boost shareholder returns. And yet, despite all this, the company remains valued on par or below its peers, especially after a 10% share price decline over the last three months.

Based on my target price and going with a 7% annual return (close to 11% when including a dividend yield of around 4%), I believe a fair share price currently sits around €22.60, meaning shares are currently valued at 21% below their fair value. As a result, I upgrade my rating on Deutsche Telekom AG from a buy to a strong buy. The current risk-reward profile is incredibly attractive following an upward-revised EPS guidance and a 10% share price decline following an overreaction to the Amazon news.

For further details see:

Deutsche Telekom Q2 Earnings: Still A Gem In The Telecom Industry (Upgrade)