DTEGY - Deutsche Telekom: Still Attractive Investment Proposition

Summary

- We remain positive about Deutsche Telekom's prospects and reaffirm our "BUY" initial rating.

- Financial performance and the balance sheet remain strong.

- Despite recent capital appreciation, we believe the risk-reward proposition remains accretive to investors.

Reaffirming Our Rating

We initiated coverage of Deutsche Telekom ( DTEGF ) on September 2, 2022 with a "BUY" rating based on the company's strong financial performance, attractive dividend policy, and management's active preparation against inflation in a recession-resistant industry. Since the coverage, the stock price has appreciated nearly ~20% compared to S&P 500's return 3.73%. Despite the greater than five-fold increase in the stock price since September, we still believe Deutsche Telekom provides good risk/reward opportunity for investors. We also update our valuation model in light of the recent increase in dividend guidance. In all, we reaffirm a "BUY" rating on the stock.

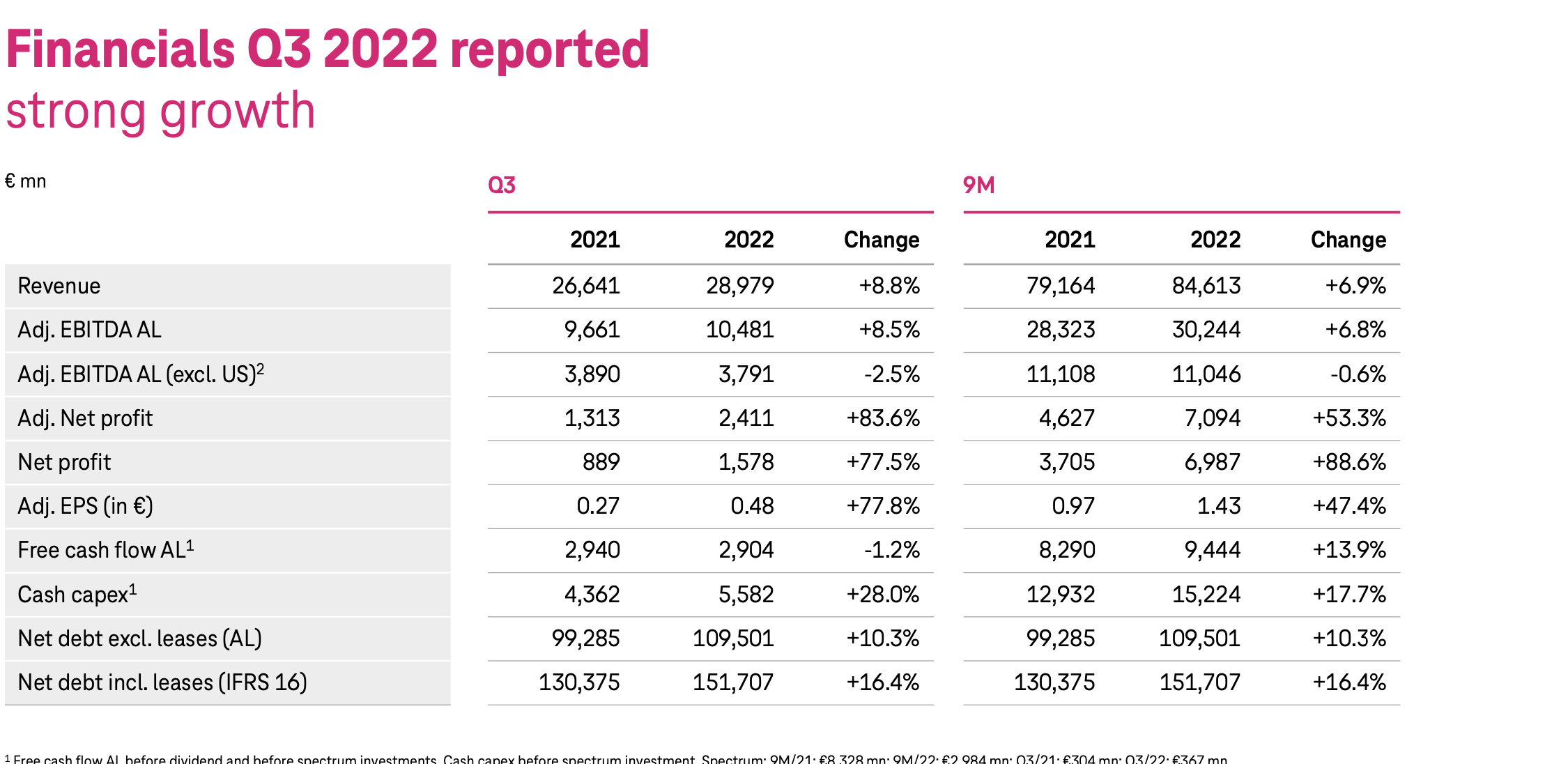

Strong Q3 2022 Results

Deutsche Telekom reported strong Q3 2022 earnings. The company reported a YoY increase 8.8% in its net revenue and raised end of year 2022 guidance along with 2023. The company's adjusted net profit also rose 80% YoY from $1.3 billion euros to $2.4 billion euros this quarter. U.S. part of the business appears to be integrating well within the company, as the U.S. business has posted strong subscriber numbers despite a slowdown in the top line. Other regions have fared better, with Germany and Europe showing strong EBITDA growth for a mature company. As seen below, the YoY growth metrics are largely all positive, and management has done a good job expanding on the bottom line despite inflationary pressures and macroeconomic headwinds.

{kind=link}

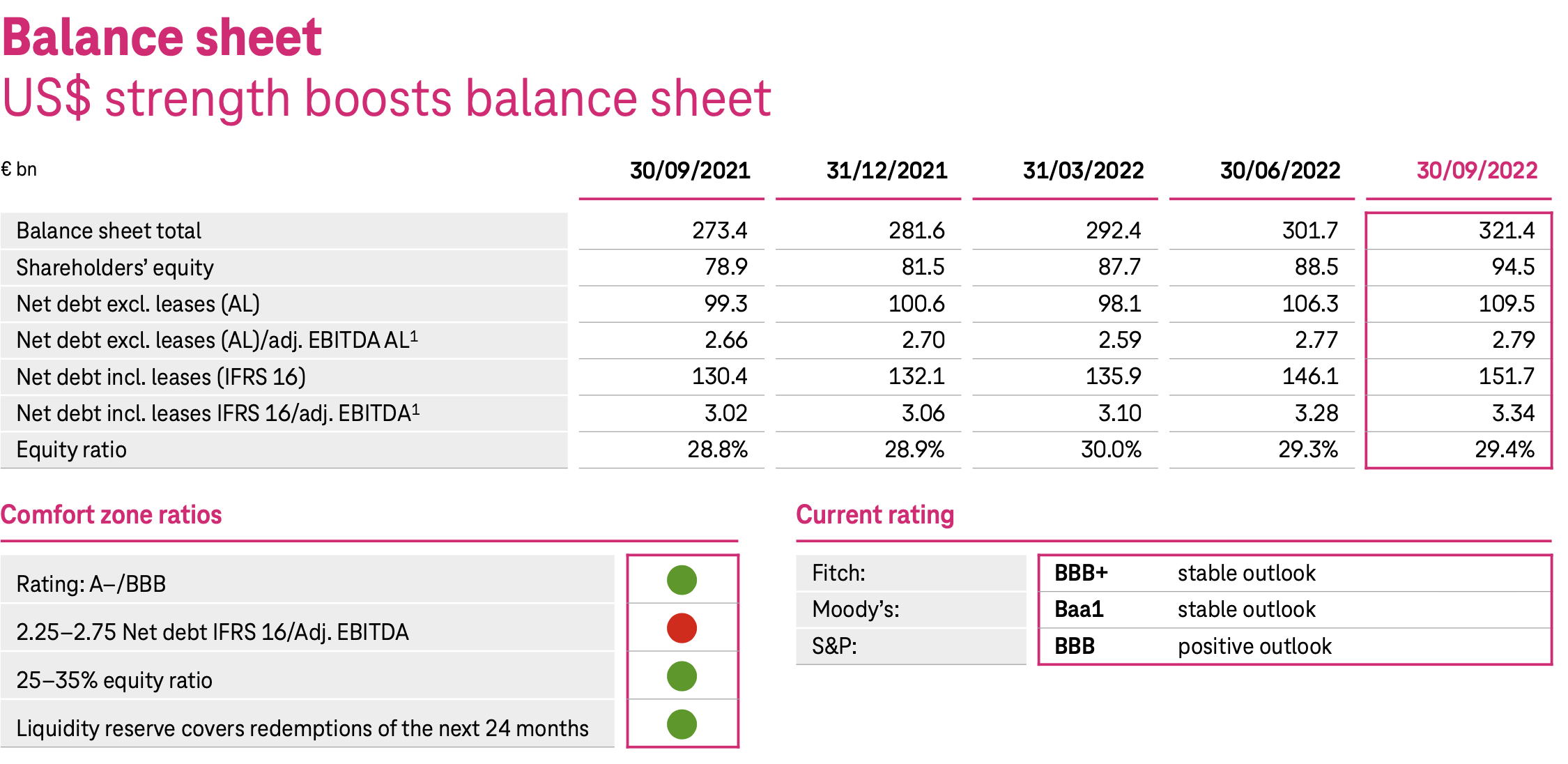

The crux of our initial thesis relies on strong balance sheet to provide steady dividend distributions for the long-term and protect shareholder value. Management has continued to make strides in this area, finding additional access to liquidity and keep its leverage ratios stable. Below is a summary of its balance sheet along with credit ratings, and the company remains in comfortable range of leverage ratios and shareholder equity buffer. The company also discussed its maturity profile, and management projected confidence as it stated $13.4 billion euros in non-US liquidity, including credit lines and liquid assets.

{kind=link}

Updated Valuation Model

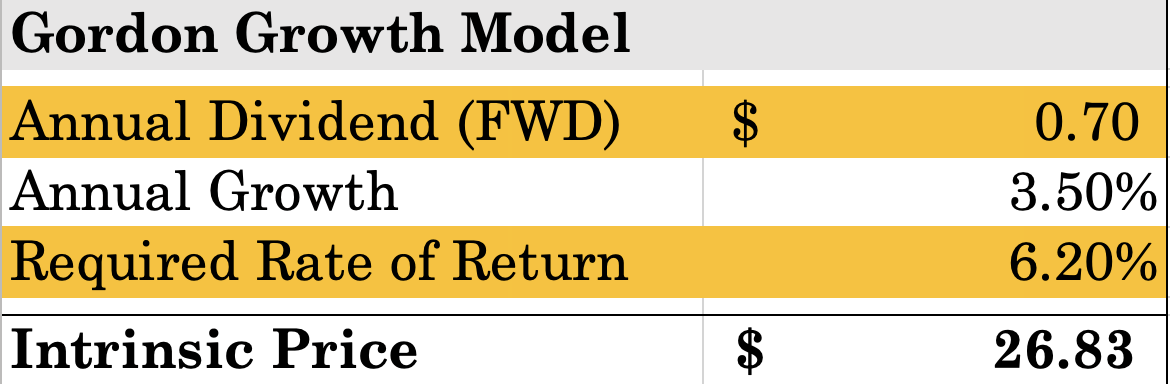

The company raised its dividend to 70 cents per share, from 64 cents per share, which is a 9.3% increase on a YoY basis. Our previous model used company's guidance of 68 cents per share, but due to strong performance, management has increased that to 70 cents per share for 2022. We assume annual growth and required rate of return to be the same as equity risk premiums and our assumption of the company's growth remains similar to our previous coverage. Based on the dividend update, our target price for the stock has increased slightly to $26.83 per share, which represents a 21.1% upside from current levels. We believe this valuation model is conservative, as the company's profit growth rate has been robust, and the dividends should grow in line with the company's growth as management aims 40% to 60% distribution of its profits in the form of dividends.

Sweet Minute Capital Valuation Model

{kind=link}

Good Risk Management

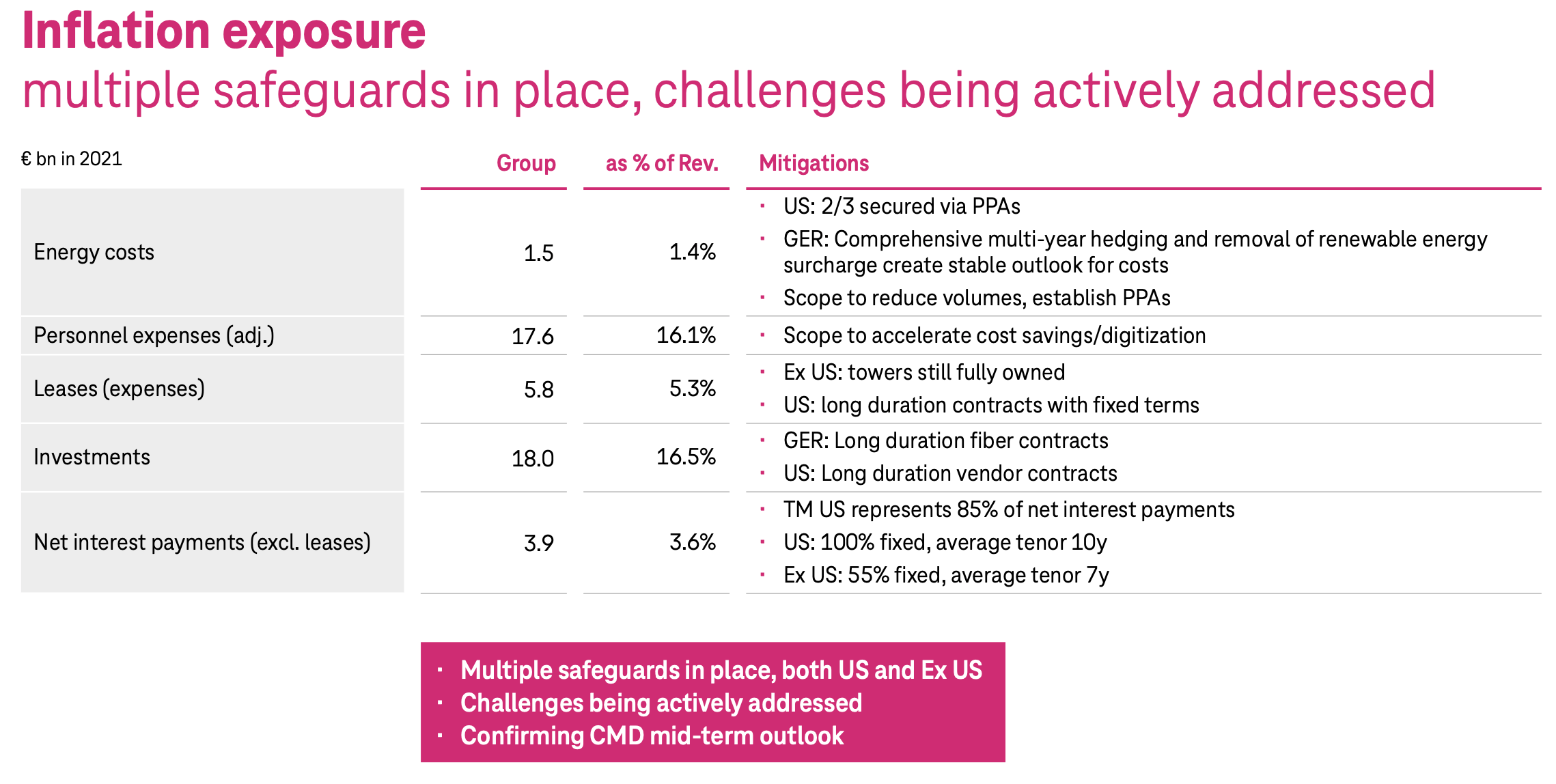

Management has also done a great job actively forecasting and managing risk. As outlined in the initial coverage article, management has shown firm willingness to minimize the impact of inflationary pressures and minimize leverage as interest rates rise. The company has worked to minimize its costs and extend debt maturity profile as a way to safeguard against interest rate risk. Though interest rate risk and recessionary risk persists, we have confidence in management to mitigate these risks and protect shareholder value during uncertain times.

{kind=link}

Conclusion

We remain bullish on Deutsche Telekom and we believe the stock will provide good dividend distributions and capital growth over a long-term investment horizon. Management has done a great job increasing the company's top line and bottom line along with increasing shareholder distributions to enhance shareholder value. We reiterate our "BUY" rating and will continue to monitor the stock in the near term.

For further details see:

Deutsche Telekom: Still Attractive Investment Proposition