XOP - Devon Energy: A Decent Quarter Revised Dividend Policy Still A Buy

2023-05-10 11:55:57 ET

Summary

- Energy stocks have lost ground lately as oil and natural gas prices have turned lower.

- Still, Devon Energy is plenty profitable with WTI in the $70s, but I have reduced my price target considering weak commodity prices.

- With a revised dividend policy and increased buyback program, there are reasons to be bullish.

- The chart is less optimistic, and I highlight price levels to watch now that the Q1 report is in the rear-view mirror.

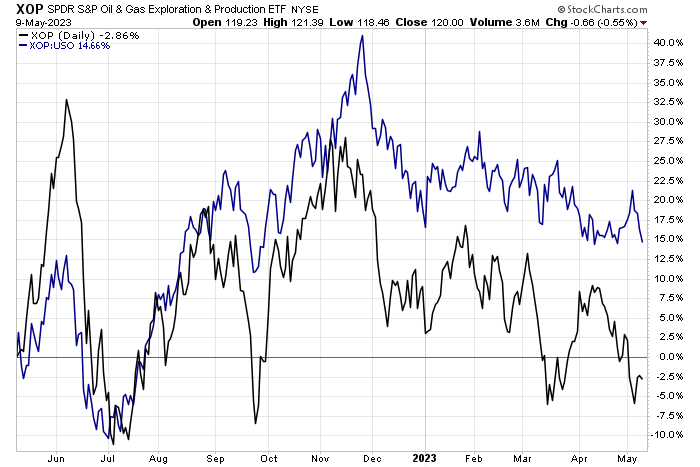

Energy-sector stocks have underperformed oil prices over the last six months. The blue line below shows relative performances between the SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ) and the US Oil Fund ( USO ). It's a key risk barometer for me when assessing the energy equity space.

Right now, it’s bearish. Still, I reiterate my buy rating of Devon Energy ( DVN ) but I'm lowering my price target given reduced commodity prices.

Energy E&P Equities Underperforming Oil ETF

{kind=link}

Stockcharts.com

According to Bank of America Global Research, DVN is an independent energy company that explores for, develops, and produces oil, natural gas, and natural gas liquids in the United States. It's a diversified large cap US exploration and production company with 2.0Bboe of reserves and 611 mboe/d of production from core assets during 2016. Production is weighted toward crude oil while growth opportunities are liquids focused - anchored by the Delaware Basin, SCOOP/STACK, Eagle Ford Shale, and Canadian Oil Sands, and the Barnett.

The Oklahoma-based $31.7 billion market cap oil and gas exploration and production industry company within the energy sector trades at a low 5.3 trailing 12-month GAAP price-to-earnings ratio and pays a high 5.9% dividend yield, according to The Wall Street Journal.

DVN beat on Q1 earnings expectations , but shares drifted lower. Numbers were solid, but BofA noted an 8-cent tax benefit. I do like, however, that the company increased its share repurchase authorization by 50% to $3.0 billion – that's a positive sign that the company views its stock as attractively valued (and I do too).

Disappointing capex and production figures did not help the street’s view of the quarter, and lower YoY oil and natural gas prices do not help annual (and sequential operating earnings). A new fixed-plus-variable dividend policy is a mixed signal in my view - while ample share buybacks are shareholder accretive, the company might give itself an out on dividends if the macro picture deteriorates (perhaps that's a too negative stance, but it's an interesting move nonetheless). Since DVN is a dividend investor stock, that could cause apprehension among its owner base.

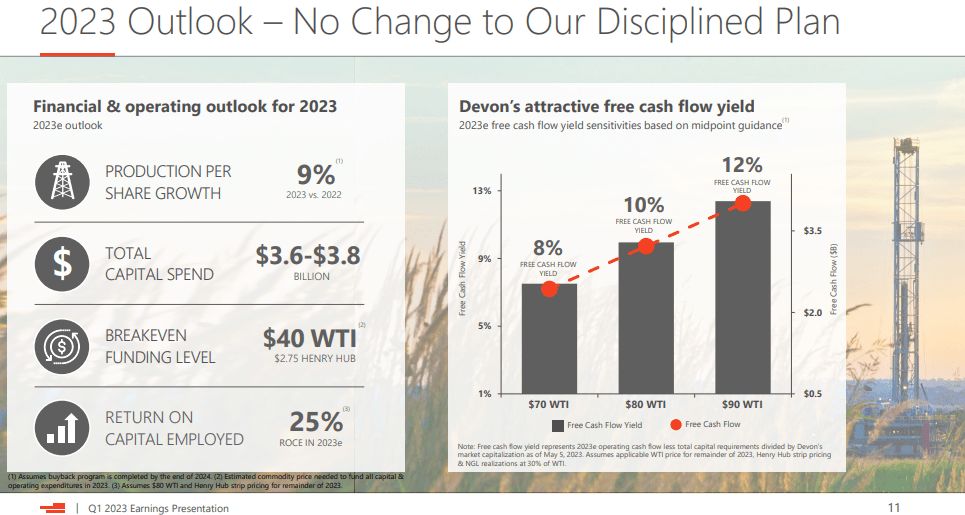

Devon's 2023 Guidance: Continued Strong FCF, Production Could Be Better

{kind=link}

Devon Energy

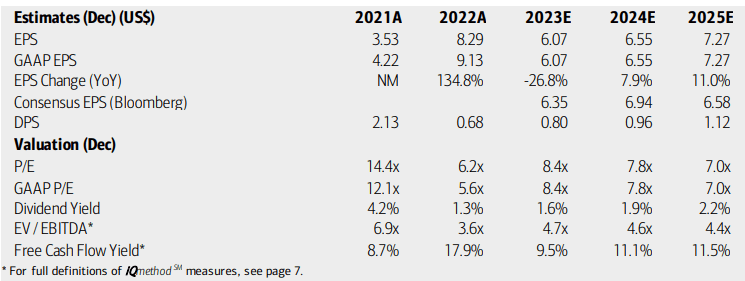

On valuation , analysts at BofA see earnings rising sharply this year then moderating to a high single-digit to low-teens EPS growth rate in 2024 and 2025. The Bloomberg consensus forecast is less sanguine but still shows ample bottom line growth over the coming quarters.

I continue to like the stock on valuation given its single-digit P/E multiples (GAAP and operating) while its EV/EBITDA ratio is less than half that of the broad market. DVN remains a free cash flow machine – shares trade at just 10x FCF and operating cash flow minus capex is seen as rising in the coming years.

Devon: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

BofA Global Research

Overall, following an EPS beat that was driven by a tax benefit and lower oil and natural gas prices today versus earlier this year, I'm trimming my price target from $84 to $77 – basically taking the P/E multiple from 12 to 11.

DVN: Attractive Valuation Metrics, But Softer Sequential Commodity Prices

Seeking Alpha

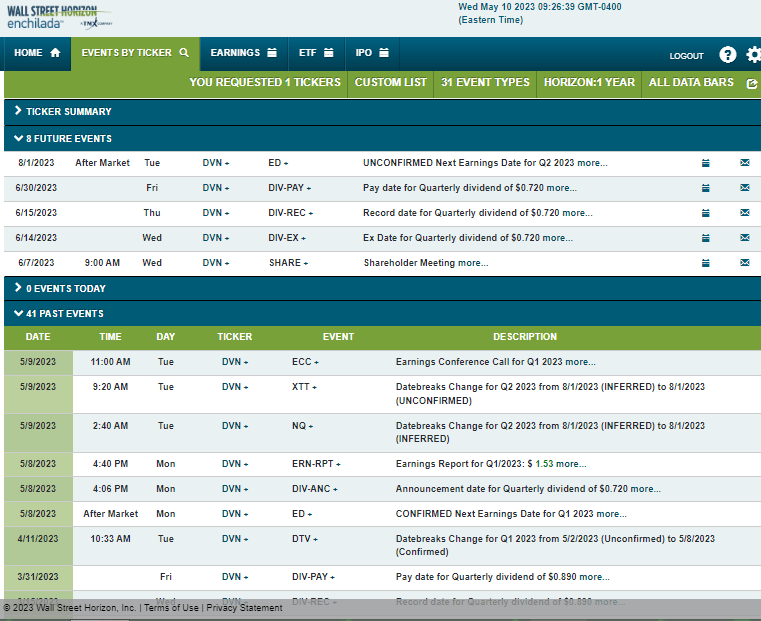

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2023 earnings date of Tuesday, Aug. 1 after market close. Before that, the company holds its annual shareholders’ meeting on Wednesday, June 7, which could drive some share-price volatility if news about the company or industry is discussed.

Corporate Event Risk Calendar

{kind=link}

Wall Street Horizon

The Technical Take

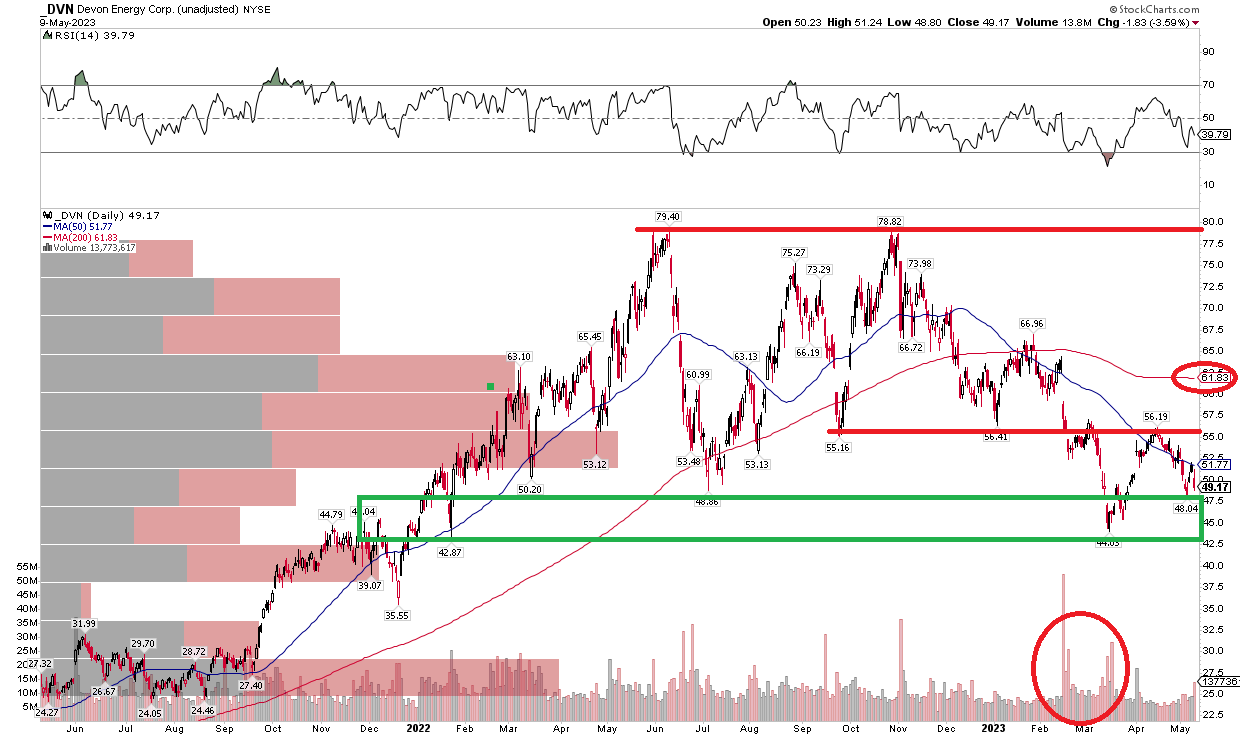

I'm growing more concerned about DVN’s chart. Notice in the graph below that shares bounced off a support range but were rejected at the March high near $56. Also take a look at the volume profile – there was a spike as shares plunged back in Q1 and a recent jump around the earnings report earlier this week. Moreover, the 200-day moving average is going to be negatively slopped before soon and the RSI momentum gauge is in the bearish 20 to 60 range. I would like to see DVN climb above $56 for the chart situation to match my sanguine intrinsic value of the stock. For now, I reiterate my buy call, but the chart is not the bulls’ friend.

DVN: Bearish Price Action, Shares Again Testing Support

{kind=link}

Stockcharts.com

The Bottom Line

I reiterate my buy rating on Devon but I'm reducing my price target. I also am growing more concerned about the chart given the downtrend that has now been going on for more than six months.

For further details see:

Devon Energy: A Decent Quarter, Revised Dividend Policy, Still A Buy