XOP - Devon Energy: Robust Free Cash Flow But Technicals Suggest Downside Ahead

Summary

- The oil & gas space struck gold in 2021 and 2022.

- A new narrative could be playing out with WTI tumbling to near multi-month lows.

- Devon Energy features a low valuation, no doubt, but momentum and price action might rule the day in the near term.

Did Energy stocks top out on a relative basis in early November? With WTI moving into the low $70s and some positive development in the Russia/Ukraine situation, investors seem to be taking serious profits in once high-performing oil & gas names.

Devon Energy (DVN) is among them. Is the stock’s valuation enough to offset some bearish momentum? Let’s drill deeper.

Oil Stocks Sliding

{kind=link}

According to Bank of America Global Research, Devon Energy is a diversified large-cap US Exploration and Production company with 2.0Bboe of reserves and 611 mboe/d of production from core assets during 2016. Production is weighted towards crude oil while growth opportunities are liquids focused - anchored by the Delaware Basin, SCOOP/STACK, Eagle Ford Shale, Canadian Oil Sands, and the Barnett. Devon also owns equity in the publicly traded midstream MLP, EnLink.

The Oklahoma-based $38.5 billion market cap Oil, Gas & Consumable Fuels industry company within the Energy sector trades at a low 6.3 trailing 12-month GAAP price-to-earnings ratio and pays a high 8.7% dividend yield, according to The Wall Street Journal .

Clearly a primary risk for Devon and other Energy firms is what happens with oil prices – Fed policy and goings on in China might dictate that. There was more uneasy news in early November when the company topped earnings expectations , but cut its dividend .

On valuation, analysts at BofA see earnings having more than doubled in 2022 before per-share profits slow to a still-solid 15.5% growth rate in FY 2023. The oil boom could then slow with EPS dipping in 2024. The Bloomberg consensus forecast is about in line with what BofA sees. Investors should consider that dividends may not be as high in the coming quarters compared to the $2.13 total from 2021. A yield near 1% is expected (and shown by Seeking Alpha ). Still, both DVN’s operating and GAAP P/Es look attractive both now and in the years ahead.

Moreover, the firm’s EV/EBITDA ratio is about half that of the market’s average while free cash flow is remarkably high. Overall, I like the valuation situation here, and with a forward operating PEG ratio of just 0.32, shares appear very cheap.

Devon: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

Looking ahead, corporate event data from Wall Street Horizon shows an unconfirmed Q4 2022 earnings date of Tuesday, February 14 after market close. Later next month, the firm’s management team is slated to speak at the Credit Suisse 28 th Annual Vail Summit 2023 – often industry news breaks at these conferences, so shares could be on the move if key business updates are given.

Corporate Event Calendar

{kind=link}

The Options Angle

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $2.03 which would be a strong 46% advance from $1.39 in per-share profits earned in the same period a year ago. Also in Devon’s favor is a positive earnings report beat rate history – the firm has topped analysts’ estimates in each of the previous seven quarters. Finally, there has been one analyst upward EPS revision since the last report and one downgrade.

In terms of the expected stock price swing post-earnings, the at-the-money straddle that expires soonest after the Valentine’s Day report shows a 6.6% implied move. With a pair of double-digit percentage changes in the last three quarters, those options could be on the cheap side.

DVN: Cheap Options Ahead Of Earnings

{kind=link}

The Technical Take

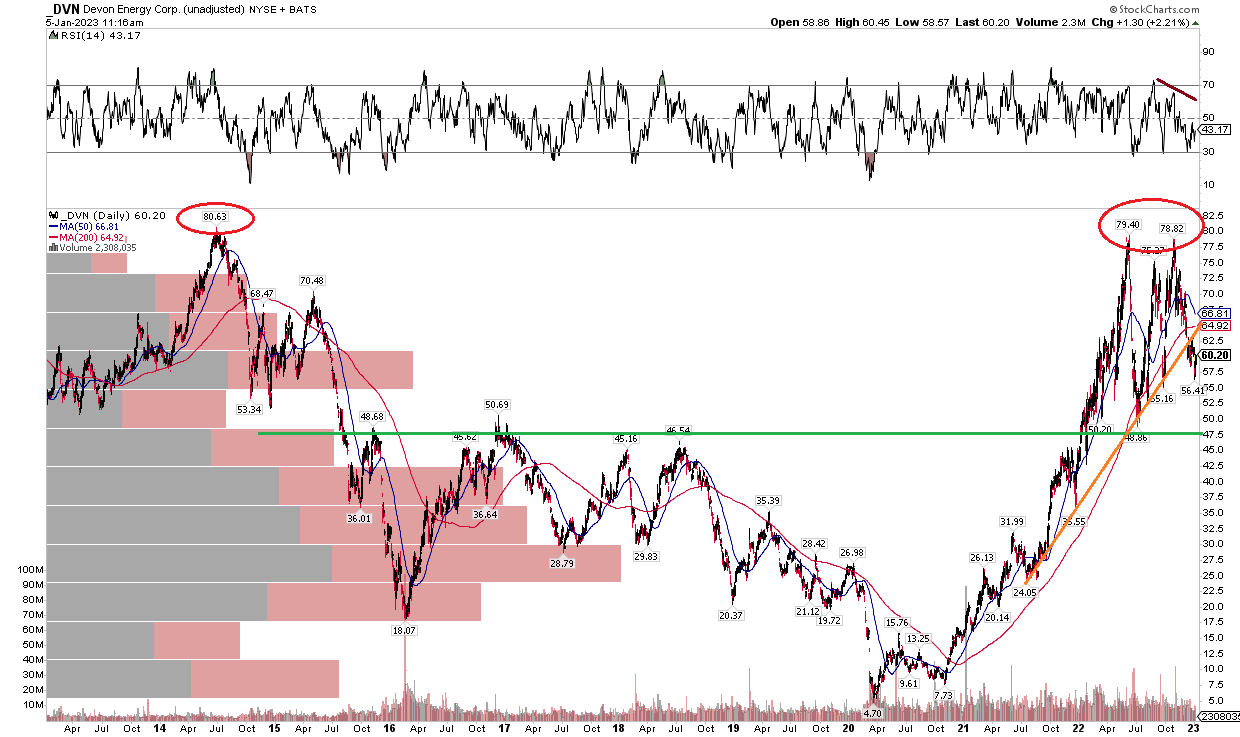

I went long-term on the chart of DVN. The chart below illustrates that the stock struggles near the $80 mark. Not only was there a bearish double-top put in last year, but that’s also where shares petered out way back in the mid-2010s. I see support on the multi-year view in the upper $40s, and that’s where shares could be headed in the interim.

Zooming in, the 200-day moving average has flattened and may turn downward as the stock trades below that key long-term trend indicator. DVN also broke an uptrend support line that began many months ago. So, the technicals are not great here, and I would look for about a 15% to 20% retreat from here.

DVN: Shares Rally To Resistance. More Downside Ahead.

{kind=link}

The Bottom Line

I very much like the valuation situation with DVN given low earnings multiples and high free cash flow. Unfortunately, the chart screams caution right now after a strong couple of years. I’d look to buy the dip near $50.

For further details see:

Devon Energy: Robust Free Cash Flow, But Technicals Suggest Downside Ahead