DXCM - Dexcom Denies Weight Loss Drug Threat To CGM Sales - I'd Be A Little Concerned

2023-09-07 11:41:22 ET

Summary

- DexCom is a major player in the continuous glucose monitoring space, with steadily growing revenues and a breakout year in 2020.

- DXCM's market cap valuation has reached $40 billion, leading to high expectations for future growth.

- Dexcom faces new competition from GLP-1 agonist drugs, which could potentially eliminate a significant portion of its target market in the Type 2 Diabetes (T2D) space.

Investment Overview

Dexcom shares rose by >7% yesterday as the company released an investor presentation in which it claims that continuous glucose monitoring ("CGM") use will only increase with the introduction of "miracle" weight loss drugs Mounjaro and Ozempic into the Type 2 diabetes market.

Dexcom stock had been on the slide despite a strong set of Q2 2023 earnings , but the market is clearly reassured by data suggesting CGM use increased in line with GLP-1 therapy use. That may be true in the short term, but long-term, will these therapies prove as compatible as Dexcom hopes?

In this post, I discuss Dexcom's history as a company, traditional competitive threats, and market opportunity, then discuss what impact the introduction of GLP-1 agonists into the T2D market may have on CGM sales long-term, and what that may mean for Dexcom's valuation.

Brief Company History - Has The Market Become Complacent About Growth?

DexCom, Inc. ( DXCM ) is a major player in the continuous glucose monitoring ("CGM") space, alongside Abbott Laboratories ( ABT ) and Medtronic ( MDT ). The company IPO'd in 2005, launched its first CGM product in 2006, and received marketing clearance for the 7th iteration of its core product, the G7, in December of last year.

After steadily growing revenues - from $160m in 2013, to >$1bn in 2018 - the company's stock enjoyed a breakout year in 2020. Shares rose in value from ~$35 in late 2019, to ~$100 in early 2021 after the company reported revenues of $1.5bn and $1.9bn in 2019 and 2020.

The demands on the company to keep showing substantial top and bottom line growth led to a downward correction in March 2022 - despite the company reporting FY21 revenues of $2.5bn - up >30% year-on-year - as management set expectation for FY22 revenues of $2.82bn - $2.94bn - below analysts' expectations.

Ultimately, revenues came in at $2.9bn, and operating income at $391m, and shares recovered to trade at ~$137 in July, before experiencing another correction on the back on Dexcom's Q223 earnings release . Revenues grew 25% year-on-year, to $871.3m, while operating income increased 66% year-on-year, to $128m. Non-GAAP EPS of $0.11 outperformed analysts' expectations. FY23 guidance was for $3.5bn - $3.55bn - up 20-22% year-on-year, with gross margin of 63%, operating margin of 17%, and adjusted EBITDA margin of ~26.5% (all non-GAAP figures).

On the face of it, Dexcom enjoyed another stellar quarter of growth and profitability, but with its market cap valuation reaching $40bn, the market's expectations may have begun to run ahead of what Dexcom is capable of delivering, even if, as company CEO Kevin Sayer told analysts on the Q2 2023 earnings call :

Our results this quarter read like a highlight reel. Q2 was our highest revenue quarter ever and represented the largest year-over-year dollar growth in our company's history. We again delivered record new customer starts worldwide and gained market share in nearly every major reimbursed geography.

Dexcom's forward price to sales ratio is currently ~11.3x - a high figure, although not unusual for a company with high growth expectations placed upon it by the market - and its forward price to earnings ratio - if we use operating margin of 17% to guide to net income of ~$600m, implying FY23 EPS of ~$1.54 - ~69x.

In summary, in some ways Dexcom has become a victim of its own success - with the market's expectations for future growth set so high that, no matter how impressive quarterly and annual results may be, they will struggle to live up to expectation.

Traditional Competitive Threats & Market Opportunity

For most of the past decade, Dexcom has been involved in a 3-horse race for market supremacy, its widely circulated G6 and newly launched G7 CGMs competing against Abbott Laboratories Freestyle Libre Device, and Medtronic's MiniMed 780G.

All 3 devices are similar in nature - a bodyworn sensor sends real-time glucose readings to a compatible display device, i.e., a smartphone app (Dexcom has its own dedicated "Clarity" app), around every 5 minutes via a transmitter, allowing users to continuously monitor their blood glucose levels, and take necessary action to avoid hyperglycemic (too much glucose) or hypoglycemic (too little glucose) events.

The G6 is also compatible with certain types of automated insulin pumps, creating the integrated continuous glucose monitoring system, or iCGM - Medtronic and Abbott's devices also have this functionality. Dexcom's sensors can be worn for ~10 days consecutively before being replaced, while transmitters have a battery life of ~3 months.

Last year, Abbott recorded $4.3bn of revenues from Freestyle Libre devices, while Medtronic reported $2.3bn of revenues from its diabetes division - primarily driven by its CGM devices.

Freestyle Libre is the cheapest of the 3 products, although it has been dogged by some accuracy and technical issues, while Dexcom's product is arguably the best on the market, but also the most expensive - a G6 transmitter costs ~$150 dollars, according to Healthline, with a 3 pack of G6 sensors costing ~$320.

The majority of users may not have to pay that much, however, as Dexcom's devices are reimbursed through Medicare durable medical equipment ("DME") coverage - Dexcom says that all major Pharmacy Benefit Managers ("PBMs") cover Dexcom G7, and that out-of-pocket costs for customers are just $20 - substantially cheaper than the competition.

According to a Centers For Disease Control ("CDC") report from 2022, cited in Dexcom's 2022 10K submission ( annual report ), there are ~1.8m people in the US diagnosed with Type 1 diabetes - the more serious version of the condition that requires regular, careful monitoring and frequent insulin injections.

The issue for CGM makers is that the Type 1 diabetes ("T1D") market may soon reach saturation - with 3 major companies competing within a market forecast to be worth $13bn by 2030, and already earning ~$10bn of revenues per annum between them, growth needs to come from the Type 2 Diabetes ("T2D") market.

This is a far larger market - although most T2D sufferers do not require regular insulin injections Dexcom estimates that 5-6m people with T2D must use insulin to manage their conditions. This has become a key target market for Dexcom - tripling its current T1D addressable market overnight.

T2D users require "basal" - less regular, longer acting - as opposed to the faster acting "bolus" insulin used by T1D users - and Dexcom has already secured reimbursement coverage for T2D users requiring basal insulin. CEO Sayer told analysts on the latest earnings call that:

We have already established greater than 60% commercial coverage for the basal population, which we view as a validation of Dexcom's value proposition by payers.

Q2 was our highest new patient quarter within the Medicare channel in the history of our company. Considering this was only a partial quarter of expanded coverage, we view this as a very positive sign of things to come.

In summary, expansion into the T2D market opens up a massive new opportunity for Dexcom - management believes there will be >780m people diagnosed with diabetes by 2045 - and with only 2 significant rivals in this space, Dexcom - theoretically at least - ought to be able to grow revenues >$10bn per annum before the end of the decade - a figure that comes much closer to justifying the current >$40bn market cap - and quite possibly double that figure by 2035.

A New Competitive Threat Looms Large - The Rise Of The Weight-Loss Drugs

Going forward, it is becoming increasingly clear that Dexcom - and Abbott and Medtronic, although the latter 2 companies have many other products and business divisions, unlike Dexcom - faces a major new competitive threat in the form of a new type of drug known as a GLP-1 agonist.

The best known GLP-1 agonists are Eli Lilly's ( LLY ) tirzepatide and Novo Nordisk's ( NVO ) semaglutide. The 2 Pharma giants' drugs have delivered sensational results in clinical studies - tirzepatide achieved an average weight loss of 15% in patients in a Phase 3 clinical trial, versus 3.2% in the placebo arm, whilst semaglutide's results are broadly comparable. In its pivotal T2D study , Mounjaro lowered patients hemoglobin A1c (HbA1c) level (a measure of blood sugar control) by 1.6% more than placebo when used as stand-alone therapy

Semaglutide has already been approved to treat T2D, under the brand name Ozempic, and is approved to treat weight loss, under the brand name Wegovy. Ozempic drove ~$8.6bn of revenues in 2022, and the demand for Wegovy has been so great, there is currently a global shortage of the higher dose formulation. Tirzepatide has also been approved to treat T2D under the brand name Mounjaro, racking up revenues of $569m in Q123, only its second quarter since launch. Approval in weight loss is considered a formality and will likely happen this year.

Faced with a choice of injecting a miracle weight loss drug a couple of times per day, or using a connected body worn sensor to monitor glucose levels, it seems possible the vast majority of people would opt for the former, so where does this leave Dexcom's ambitions for the T2D market?

The bearish take is that tirzepatide and semaglutide are the future, while Dexcom's G7 - only just launched - is already becoming the past. Of course, people with T1D will still have a need for Dexcom's products, and some T2D users too, but the market of 5-6m patients that the company has ambitions to conquer may be partially, or even wholly eliminated by the rise of the "miracle" weight loss drug.

If that were to happen - and some of the jaw dropping peak sales estimates that have been provided for Wegovy, Mounjaro et al of >$25bn per annum, suggesting they will become all-time best-selling drugs, suggests there is a good chance that it will - then Dexcom will likely find it much harder to meet its own expansion goals.

To justify a >$40bn market cap valuation, as mentioned above, Dexcom needs to show a clear path to a double-digit billion per annum revenue opportunity in my view, and that means that expansion into the T2D market is a "must," not a "nice to have." When not one, but two challengers emerge with peak sales expectations of >$50bn per annum in your target market, it is arguably time to panic.

Dexcom's Take On GLP-1 Agonists - Bullish, Nor Bearish

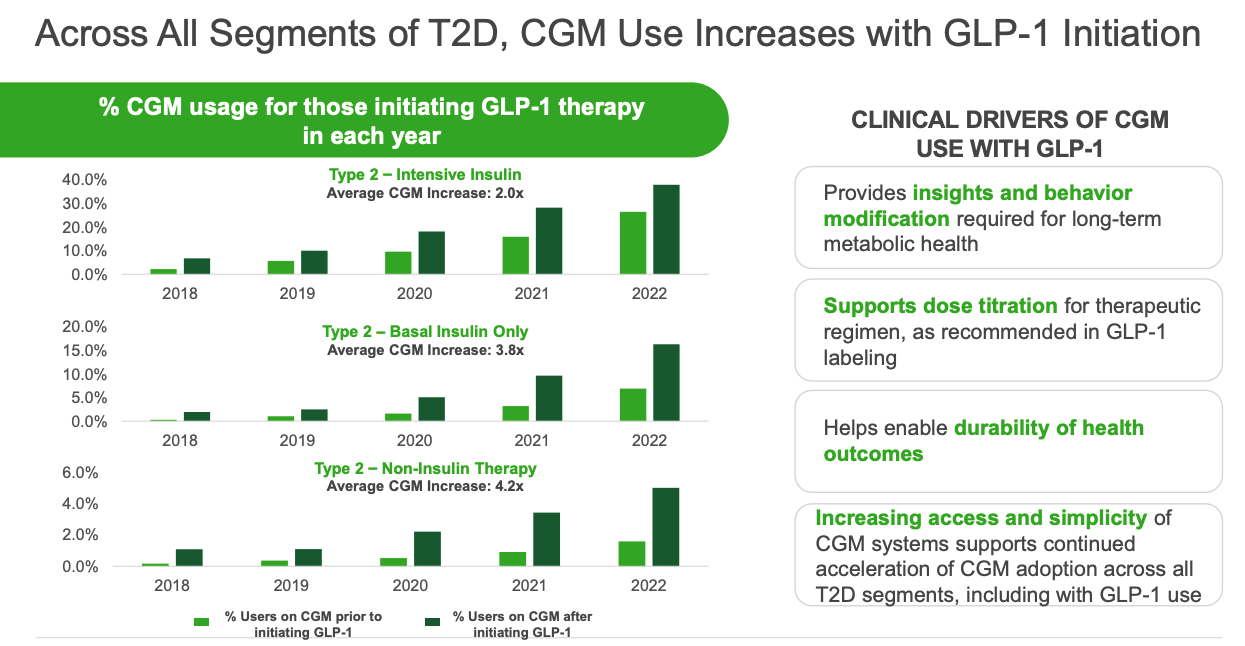

Dexcom management sees things very differently, however, as this slide from its latest investment presentation reveals.

Dexcom's interpretation of GLP-1 "threat" (Dexcom presentation)

{kind=link}

Dexcom believes its devices are complementary to GLP-1 agonist use and apparently has the data to prove it. As shown above, Dexcom is confident there is a positive correlation between use of GLP-1 and use of CGMs, noticeable in intensive insulin users, even more so in basal insulin users, and most of all in non-insulin T2D users.

In many ways the data makes sense - why wouldn't a GLP-1 user also use a CGM to manage their condition optimally, and benefit from the additional data collected? The market certainly seemed to buy Dexcom's arguments, pushing the company's share price up by >7% yesterday after Dexcom's latest investor deck was released. The share prices of Abbott and Medtronic also rose slightly.

I have a couple of concerns with Dexcom's argument however. Firstly, it's hard to believe that over the long term, a patient with T2D would prefer to keep using a CGM if the GLP-1 agonist worked and they were able to get by without one. As cleverly as the devices are designed to be as unobtrusive as possible, the regular replacement of sensors and transmitters is a chore - and an expense - people may feel they could do without. The goal of ultimately becoming CGM free may actually incentivize many users to try a GLP-1 agonist.

Secondly, it seems unlikely that a health insurer would want to keep paying for a CGM if a GLP-1 agonist is proving its worth. The positive results that studies show can be achieved with these drugs cannot be matched by a CGM, which is not a curative device, so the likelihood is that if a patient can continue with one or the other, they will likely opt for the agonist.

Thirdly, if GLP-1 agonists prove to be as successful as is hoped, the pool of patients that require a CGM theoretically ought to shrink - even Dexcom would probably admit a world where fewer people require a CGM is a positive development from a healthcare perspective.

Concluding Thoughts - GLP-1 Agonists & CGMs - Uneasy Bedfellows Or Love At First Sight

It is interesting to note that Dexcom did not field a single question on GLP-1 agonists on its latest earnings call, so we can probably conclude that although CGMs and GLP-1 agonists are on a collision course, the threat posed is not significant at this time.

Dexcom's valuation is very much based on "jam tomorrow," however. Very few investors will buy a stock trading at a P/S ratio of >10x, and a P/E ratio of >60x without expecting revenues to grow substantially over time. Even Dexcom's incredible Q2 2023 results - arguably the company's best ever, with 25% annual revenue growth - disappointed the market. As stated, I believe most Dexcom bulls have a double digit billion revenue target in mind and expect it to be achieved sooner, rather than later.

All things considered, my take would be that the introduction of GLP-1 agonists into the T2D market will not prove to be a positive for CGM makers over the long term, as despite the initial synergies, as Ozempic, Mounjaro, and next-generation agonists - already in development and showing superior weight loss potential than their predecessors - become increasingly prevalent, those who can afford to stop using a CGM, probably will.

When a market threat as significant as tirzepatide / semaglutide emerges, companies can either try to partner with them, as Dexcom clearly believes it can do, or try to make sure they cannot establish a foothold in the marketplace. The latter option is more or less unavailable to Dexcom thanks to the unexpectedly strong performance of semaglutide / tirzepatide in the clinic across all major endpoints, and rapid commercial uptake. The former may work in the short term, but it is hard to see a GLP-1 agonist / CGM combo working in the long run.

In fairness, while CGMs have been around in one form or another since 2006, semaglutide / tirzepatide are the new kids on the block, and it could be that safety concerns (mental health has already been cited as one potential issue), disappointing efficacy, or an aversion to self-injecting may dampen enthusiasm, and that the hype around weight loss drugs will dissipate.

In my view, the signs are not pointing to that scenario at present - Ozempic revenues will likely exceed $10bn this year, with Mounjaro not too far behind, and I suspect this will inevitably damage the appeal of Dexcom's key product in the T2D market, making it much harder for the company to drive its own double-digit billion revenues.

As such, I see a price correction coming for Dexcom, a company whose stock price is regularly heavily punished by the market for perceived underperformance and competitive threats.

For further details see:

Dexcom Denies Weight Loss Drug Threat To CGM Sales - I'd Be A Little Concerned