MDT - DexCom: Riding The Growth Wave

2023-03-15 18:32:35 ET

Summary

- DexCom has built itself an impressive market position against large competitors in the diabetes space.

- Future growth should remain relatively easy as reimbursed populations continue to grow, and the overall diabetes market is expanding.

- Despite all that, the company is very expensive today, and it's very possible the space commodifies as Medtronic and Abbott continue to iterate better products.

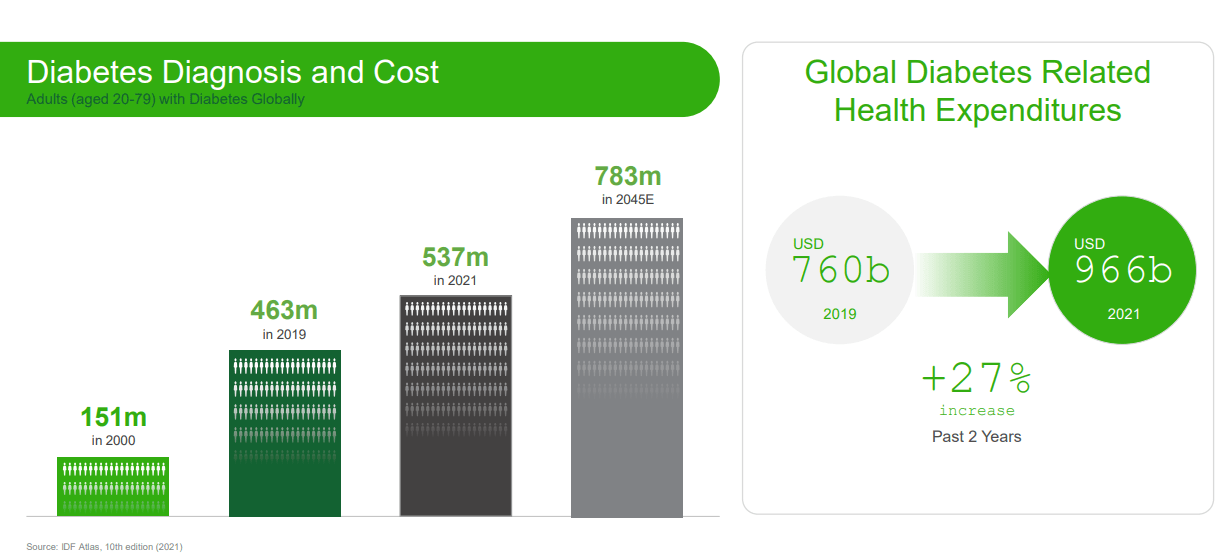

The diabetes market sadly has some of the strongest tailwinds globally today. It's estimated 1 billion people are classified as obese globally today, and growth rates remain strong in Type 2 diabetes, estimated at 5% over the long-term future.

{kind=link}

With that, health expenditures are growing faster than that. A substantial proportion (~35%) of Type 1 diabetes patients are already well entrenched in continuous glucose monitoring through products offered by DexCom ( DXCM ), Abbott Laboratories ( ABT ), and Medtronic ( MDT ). However, the growth runway for Type 2 patients is immense.

Medicare drives the trend in insurance acceptance of new products, and it's likely this year they will begin covering basal insulin Type 2 patients for CGM's. Add that to previous Type 2 approvals, and these patients should keep the growth train rolling for CGM's well into the future.

DexCom has managed incredible growth rates over time. The company has somewhat sacrificed short-term profits as part of its land-grab strategy, which has paid dividends in terms of revenue growth. Despite the company's singular focus on CGM's, it has managed to build a leadership position against heavyweight medical device competitors.

Initially, the DexCom G6 device set itself apart with its integration with insulin pumps offered by Tandem and Insulet. However, Medtronic's new offering (still pending acceptance in the US market) and Abbott's Libre 3 are integrated with pumps, as well, and are showing similar incremental improvements over previous iterations. Despite the DexCom G7 launch this year internationally, improvements in competitors' offerings could commodify the space, driving down prices over time. Medtronic's 780G most recently drove 18% growth internationally, and the FreeStyle Libre 3 has strong reviews. Functionality is similar between all of them, with feature competition in factors like warm-up time, battery life, accuracy, and price.

However, this concern could easily be overcome by sheer volume. This is a massive growth market and now a highly competitive one. There are minimal switching costs for patients, as setup of these products requires only putting it on the skin and downloading a phone app. However, if each product performs as expected, I'd think it's unlikely to see high churn among patient populations. With that, as these companies heavily compete on features, the concern is one bad product iteration will more adversely affect DexCom than Medtronic or Abbott. Both of those companies have significant operations to fall back on, whereas a major flop could crush a singularly focused company like DexCom. The inverse of that is investors are able to buy a diabetes pure-play. Abbott and Medtronic also have plenty of slower-growing business lines that hold back the whole. DexCom as a pure-play should have more focused management, research dollars, and is positioned to provide maximum returns on an investment into the growing diabetes space.

{kind=link}

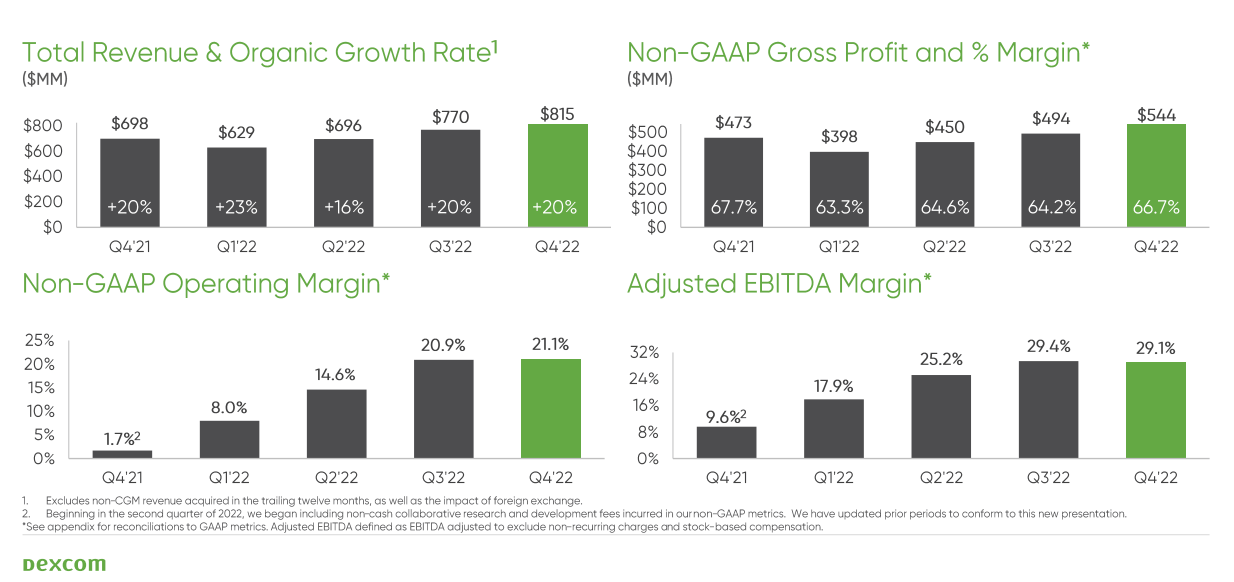

Looking at operating results, the company's metrics are pointed in the right direction. Gross margins are likely to remain crimped in the short term on the rollout of the G7. The company is offering a bridge program to patients pending insurance pay-outs to get them to make the switch. Additionally, the rollout of new manufacturing will result in lower initial margins before reaching full scale.

Ultimately, the proof is in the pudding with the revenue growth rates. Steadily, DexCom has taken advantage of the opportunity in front of it regardless of competition or short term issues and driven strong growth in revenues. With compressed gross margins, it was heartening to see operating expenses relatively flat YOY. They declined from $461M to $372M, or effectively no change when adjusting for a one-time expense last year. This shows impressive expense management and hopes for an even more profitable future as the company matures.

Looking forward, management projects 150-200 bps of operating expense leverage and 15-20% revenue growth in 2023. They are looking at an uptick in growth among the basal insulin population after mid-year, which currently only accounts for around 1% of revenues today. This market should be a rising tide to lift all boats for CGM providers in the space. Early projections are for an additional 3M potential patients, on top of DexCom's efforts having increased international reimbursed populations by 3.5M over the past 18 months. The story is still early here.

As far as financial position goes, DexCom is sitting on $2.5B in cash, plenty to keep the wheels spinning. SBC is low, thankfully, considering the space they operate in, at $126.5M in 2022. R&D comprises a large operating expense, at $484.2M in 2022 against $2.909B in revenues. That number has fluctuated somewhat, but I'd like to see the company continue to organically drive improvements in its devices over time.

The company is profitable, and should not have any issues in servicing its current debt load.

{kind=link}

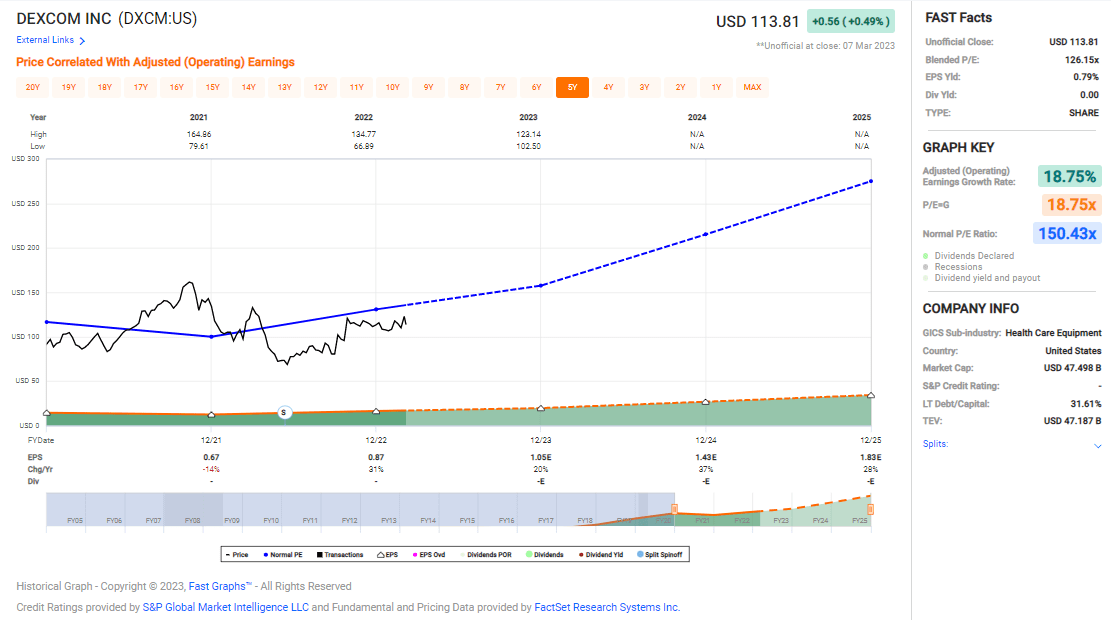

It should come as no surprise at this point that DexCom is expensive. Very expensive. The company is early in its earnings growth story, and trades today at around 126X blended earnings. Earnings growth is projected to increase at a solid 19% clip or so, and operating expenses have been maintained conservatively by management into this year.

DexCom is obviously not a value today. At 16X sales and over 100X earnings, the company maintains a massive premium, although one that's shrunk over the past year or two. I think an investment is built on the massive market growth and DexCom's proven history in grabbing share. However, its competitors are no slouches. Medtronic and Abbott are well-funded, and by all accounts are putting out products that easily compete with DexCom's offerings. It's highly likely prices are driven down over time, which means the CGM providers will have to make up for that in volume. This hasn't been a problem so far, and based on the massive increases in reimbursed populations it shouldn't be for the foreseeable future. DexCom has been a winner, and I think it will remain one. However, the next decade won't be as easy as the last. I'm calling it a buy today. I'm basing this not just on the market opportunity, but on strong expense management that I think will drive meaningful profit growth over the medium term.

Modeling 15% sales growth over the next decade, with an operating margin of ~25%, we'd be looking at a ballpark of ~$3B in profits annually 10 years from now. If valuation compressed to, say, 40X earnings, that's a $120B company compared to $45B today. This is not a prediction, but a way of looking at how the company could grow into today's valuation as it scales and becomes more profitable. With that, it's still early, and risks are high. Investors should pay close attention to the space, and multiple compression is entirely possible leading to dead money despite strong growth. Such is the gamble in growth stocks.

For further details see:

DexCom: Riding The Growth Wave