DXCM - DexCom: Stelo Stellar Outlook

2024-01-17 08:20:00 ET

Summary

- DexCom's not just a diabetes company anymore. They're at the forefront of wearable health tech, blurring the lines between medicine and lifestyle.

- DexCom might not be the flashiest stock, but their focus on long-term growth and responsible expansion is music to any value investor's ears. Think marathon runner, not sprinter.

- DexCom's foray into the non-insulin market is a bold move. It could be a game-changer, but it also carries some risk.

In past articles, my central thesis on DexCom (DXCM) was based on the radical transformation that the G7 suggested. Almost a year after its full-blown release, it is an excellent time to evaluate if the G7 delivered everything it promised, what the prospects of DexCom are, and if it is time to reap the reward or wait for the fruits to mature.

DexCom announced preliminary results of Q4 and showcased its accomplishments for 2023 and plans for 2024 and beyond. We will go through:

- A brief overview of DexCom

- Highlights of the G7

- The future of DexCom and its new launch, "Stelo."

- Valuation and Risk Implications

DexCom Overview

DexCom's business is the tracking of glucose levels in diabetes patients. It has been arguably leading the way in Continuous Glucose Monitoring (CGM) in the last decade with innovations like the real-time alert of hypoglycemia (low sugar), integration with Automated Insulin Delivery ((AID)) systems, and smartphone data sharing, among many others.

Another difference between DexCom and other CGM alternatives is the true nature of CGM. Other products require manual operations to check the glucose level. While theoretically, the sensor checks glucose levels continuously, it does not alert or provide real-time data.

The G7 is the much anticipated "new" version of the product, which required a complete overhaul and change of the manufacturing process and promised to deliver better cost, reduced size, higher accuracy, and factory calibration, among other significant benefits. The company began developing this new technology in 2018, and the G7 was finally launched fully in February of last year.

There are two significant growth opportunities for DexCom:

- The shift from traditional finger prick devices to CGM

- The adoption of CGM in Type 2 diabetes patients

Finger Prick vs CGM

The apparent advantages of CGM versus finger prick are reduced discomfort and increased data, while the main disadvantage at first glance is the higher cost.

The company has made studies comparing the effectiveness and actual costs of managing diabetes with and without CGM, which show promising results on both fronts. However, using CGM is still not economical for many people worldwide, and DexCom's availability is limited to a few countries.

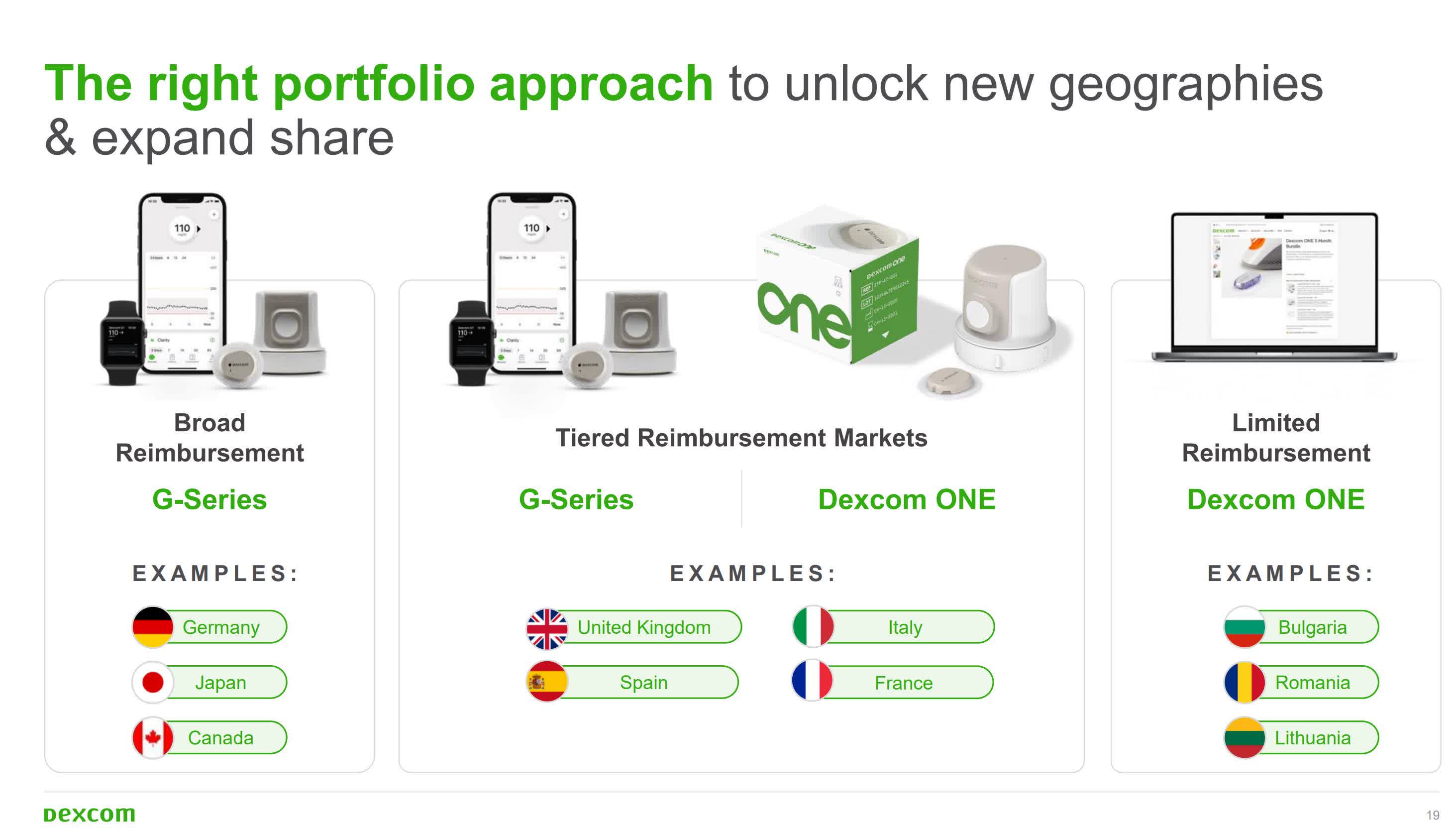

Dexcom Current Reach (Investor Relations)

{kind=link}

Partly because of this, DexCom's business has historically been based on healthcare reimbursements; the geographical expansion of the products was complex, as the company required negotiations on the reimbursement of products to launch.

Interestingly enough, DexCom launched cash pay in several European countries, and now most of them (seven, to be precise) allow for some form of reimbursement. This strategy of cash-pay introduction and subsequent adoption of insurance reimbursement might ease the path toward the geographical expansion of DexCom's products.

Adoption of CGM in Type 2 Diabetes

Originally, CGM was only targeted to Type-I diabetes patients, as they need to administer insulin to control their glucose. However, the use of CGM has many health advantages for Type 2 diabetes patients, who might or might not be required to administer insulin but do require the control and monitoring of their glucose level.

The number of people who have Type 2 diabetes is approximately 10 times larger than that of Type 1. Reaching this market would substantially increase DexCom's TAM.

Simplifying the medical aspects, there are six types of prospective users of CGM.

- Type 1 Diabetes

- Type 2 Diabetes that require insulin

- Type 2 Diabetes Only Basal Insulin.

- Type 2 Diabetes Non-insulin administration

- Pre-diabetes or at-risk Diabetes

- Health & Wellness (Athletes, for example)

The G7 and DexCom

Ending the suspense, the G7 delivered or over-delivered my expectations and arguably the expectations that DexCom had set forward in its reports from the start of its development.

It has become the lowest out-of-pocket cost option in the US, increased the prescriber base by 40%, and received astounding reception in international markets.

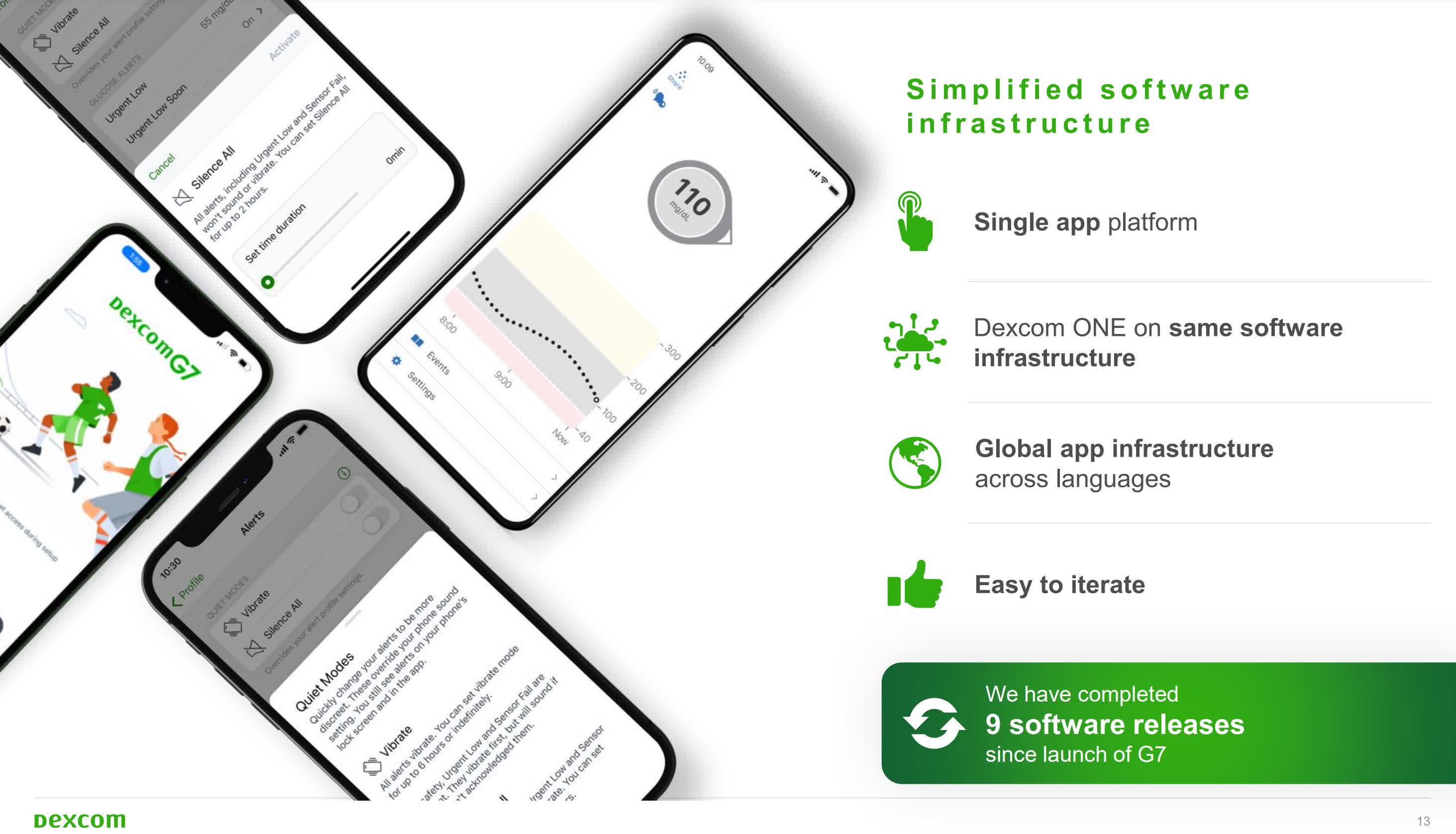

Not only did the G7 deliver on its promise, but DexCom has made substantial efforts in the software development front, which complements the G7 benefits well.

Dexcom Software progress (Investor Relations)

{kind=link}

Some improvements were basic but essential; for example, the app was different in each language. Now, it is a single app, while others are more complex, like the unification of the tracking in one single app.

These changes showcase an essential shift in DexCom. They are transitioning from a primarily medical company to a more comprehensive merge of medical and technological. This shift, while subtle for now, is exemplified by the stories shared by the CEO at the last conference . He pointed out the anecdotal story of a girl with diabetes who decided to share her CGM live results with her classmates so they could help her manage her glucose levels.

While anecdotal and not representative of the large-scale behavior of users now, these features, paired with social media and the health and wellness sector, could be a significant catalyst for DexCom and a differentiator to its "peers" in CGM.

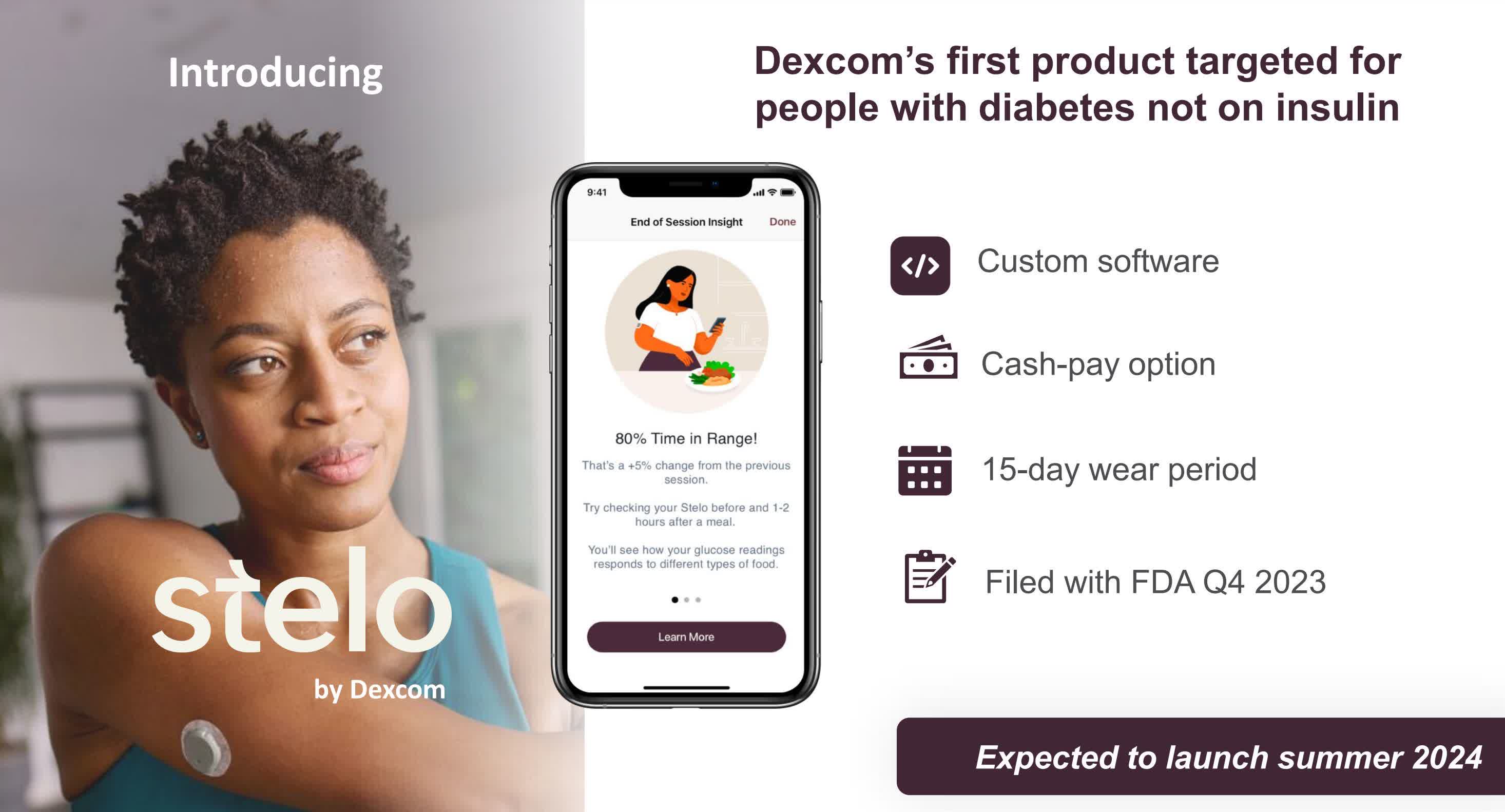

The Future of DexCom

Pending approval of the FDA, DexCom is launching a new product targeted to people with diabetes, not on insulin.

Stelo The new Dexcom Product (Investor Relations)

{kind=link}

This is groundbreaking because it will allow for a cash-pay option, broaden DexCom's reach and penetration, and, if successful, allow DexCom to increase its scale radically and prove its claims on CGM efficiency and savings.

While the approval of the FDA is not guaranteed, it is likely to occur as the G7 has already been approved for much higher accuracy requirements, as the integration with insulin pumps, so approval for monitoring should be smooth.

The story of the girl showcased in the section above, where the girl uses the DexCom app to share her glucose level with her classmates, hints at what we might see with Stelo. Why it might initially reflect negatively in the P&L. It could prove to become a catalyst for DexCom's Market penetration. Broadening the audience with CGM, connectivity, and social media could catalyze DexCom's adoption and trust.

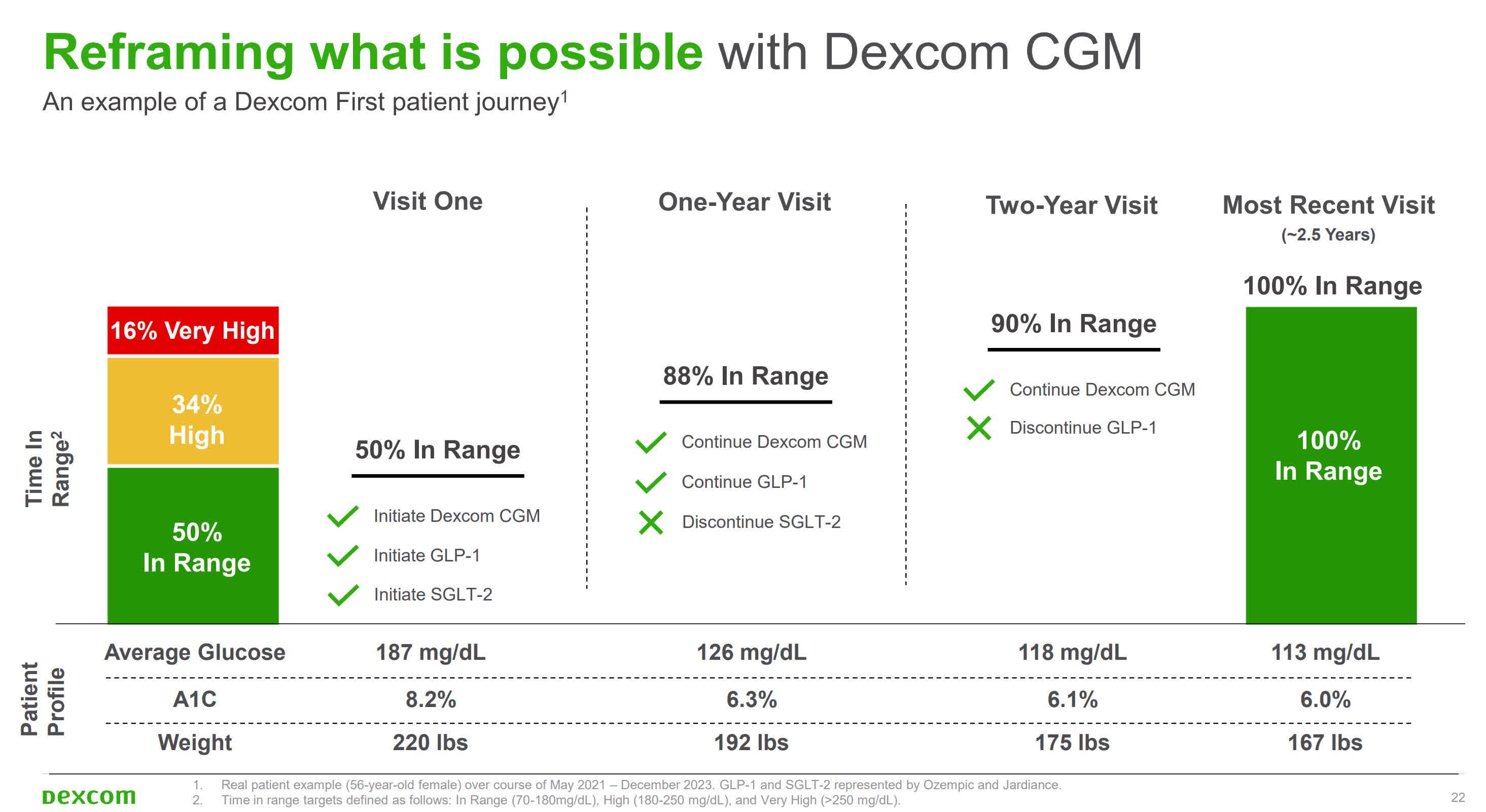

Will it be affordable? According to DexCom studies, non-insulin Type 2 diabetes patients could save around 500/month per patient using CGM. With a cash price of around $200-$400 a month, it would be logical that patients preferred saving $100-$300/ month and have improved health prospects. An example of how these savings materialize was exemplified by the progression of a patient for three years.

Dexcom Patient results (Investor Relations)

{kind=link}

After three years of using DexCom, the patient improved their glucose and A1C levels and stopped requiring GLP-1 and SGLT-2. While a fantastic showcase for DexCom, the savings will likely not be on day 1 for patients. It would require an "initial investment" for some time before the savings materialize. I believe DexCom's social and communication aspects will play in its favor. The "trust" that the G7 requires will be easier to obtain if more data is available in the Diabetes community and for primary care physicians.

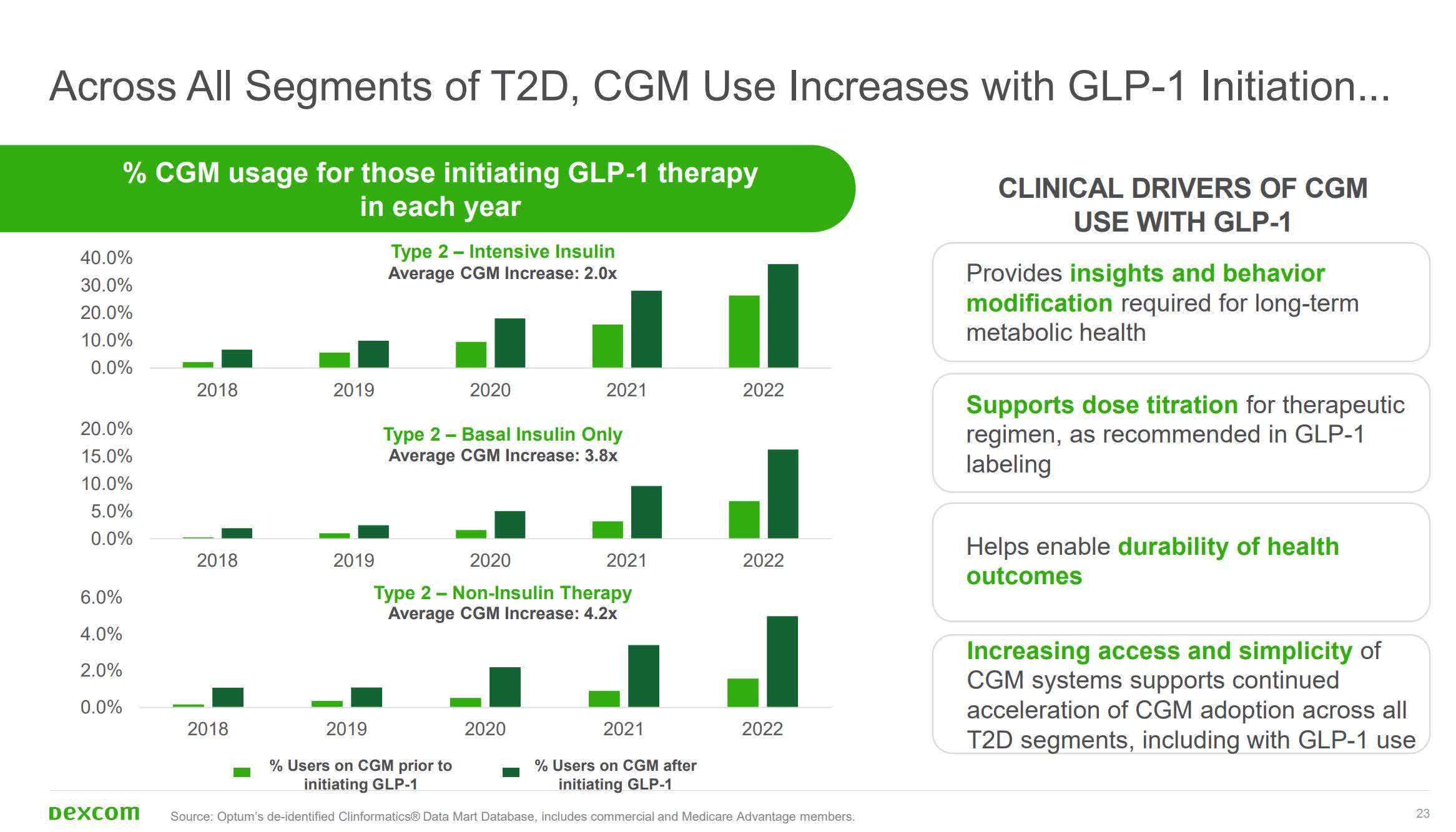

The adoption of CGM in Type 1 diabetes is, according to DexCom, around 60% in the US, Type 2 with intensive insulin is around 40-50%, and from that, there is a substantial drop to 15-20% in Type 2 Basal insulin and the single digits in Type 2 non-insulin therapy. While the percentages drop, the number of potential patients increases as there are many more Type 2 diabetes non-insulin than Type 1. So, the potential growth for DexCom entering the Type 2 Non-insulin, which Stelo targets, is gigantic.

CGM Market Penetration (Investor Relations)

{kind=link}

The objective of Stelo in the short term is not to improve the P&L but to increase the reach of DexCom and "test the waters" of this relatively new market.

If somebody came to my office and said, we are going to make money, I would fire him. - Kevin Sayer CEO

In the long term, however, it could provide the benefits of scale, a better insight into the market, and the ability to collect broader data sets going forward.

Valuation

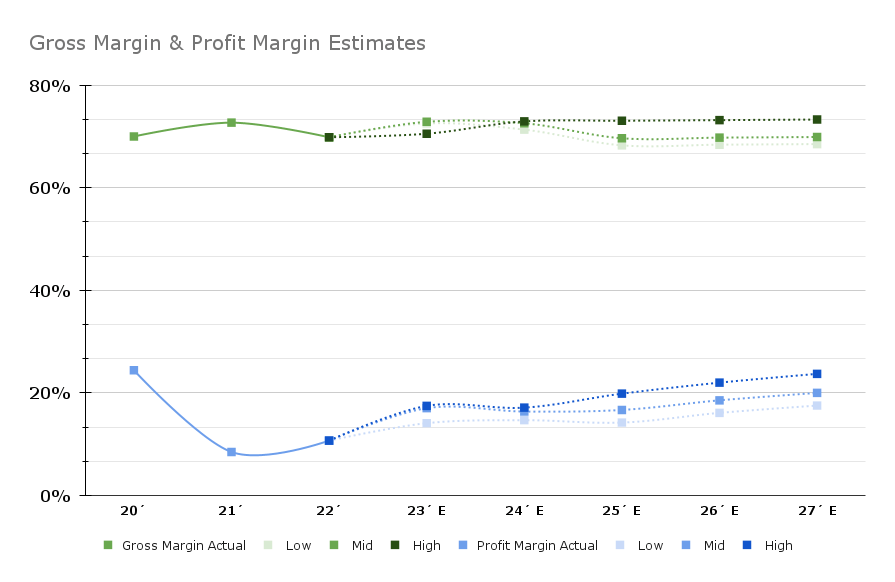

For the valuation, we will use the guidance of 2024 adjusted for volatility and projections of Gross Margin and Profit margin according to the evolution of G7 technology. The shift in the G7 from 10 days to 15 days is not included in any scenario as it has ambiguous effects on pricing, volume, and growth.

Gross Margin and Profit Margin Estimates (Author´s Charts)

{kind=link}

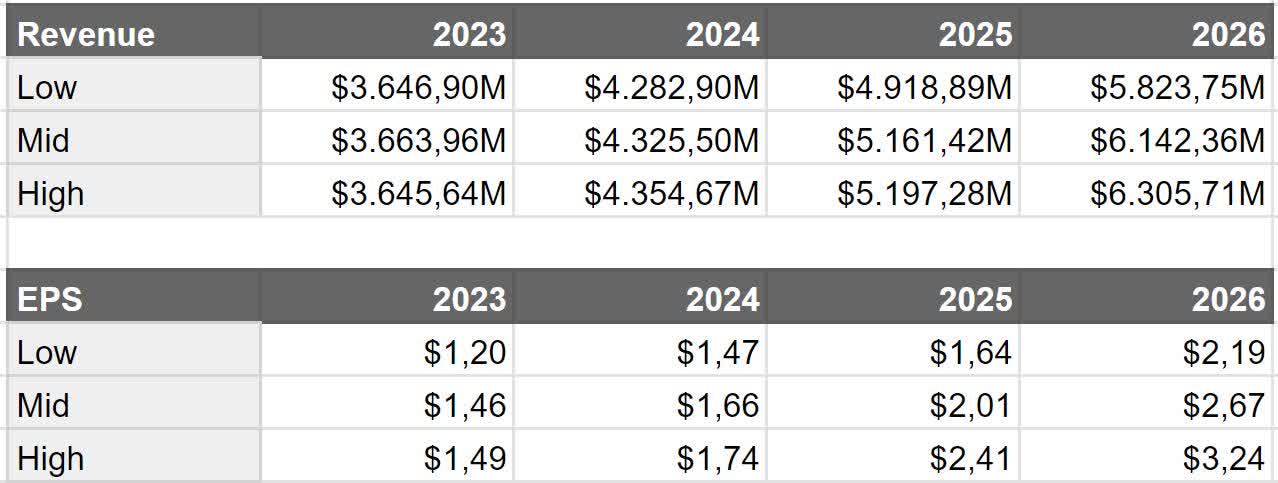

We have the following estimates for Revenue and EPS with the above assumptions.

Revenue and EPS Estimates (My Charts)

{kind=link}

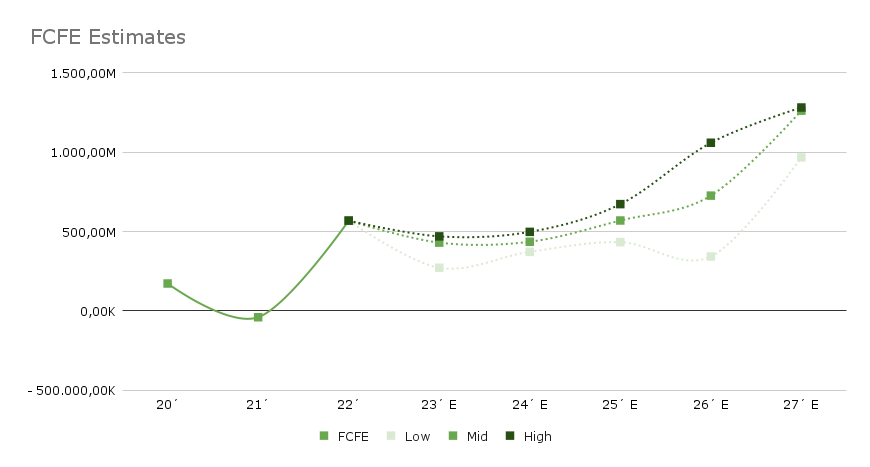

To make the valuation, we will use the FCFE methodology, traditionally with high single digits PGR and the growth consistent with current G7 Technology, leaving aside the prospects of Stelo even in the long term, as it is unclear how the business will modify scale and profitability.

{kind=link}

It is important to note that these estimations are adjusted to eliminate noise and unusual expenses, so numbers may differ from reported FCFE. Still, trends like the Capex investment for the Plants and future capital investment estimates are considered statistically.

On the balance sheet, DexCom has over 3 Billion in cash and long-term debt of only 2.1 Billion, so it is in a healthy state, which is essential considering the current high-yield environment.

With the above considerations, DexCom is likely in the fair value range. While there is some upside, considering the known, It is a risky play on the downside.

Dexcom Fair Value Estimate (My charts)

It is to be noted that the valuation aims to be conservative in the low range as a measure of risk in the stock.

Conclusions

DexCom is one of the stocks I am most passionate about. The technological edge it has developed over the years and its ability to shift manufacturing capabilities while maintaining production and evolving its Global manufacturing capabilities is truly impressive. But the most remarkable aspect is the testimonies and experiences of the users of DexCom, especially compared to the ones I have observed about competing solutions.

While observations and testimonials are biased, DexCom's numbers and prospects speak for themselves and are pretty loud. The G7 is a great example; for as long as its development lasted, from initial hints to actual results, it seems that the company was overstating the significance of the product or overpromising the results. Still, to their credit, they even over-delivered by some metrics.

The valuation reflects a fair value as the company prioritizes the technological advancements and proper expansion of its new offerings to the immediate capitalization of its technological edge. I believe that is the correct strategy for the long term. As the company evolves in its software and hardware offerings, its technological edge will become evident in the market and the P&L.

The Tortoise and the Cat Portfolio

I have been making two dummy portfolios to showcase the importance of risk profile and portfolio construction in the selection of stocks. I am building Dummy portfolios of a Tortoise and a Cat to do so.

The Cat portfolio: The stock would not be a good fit for this portfolio, as it relies on the immediacy of catalyst despite the added risk those may present. While the upside is attractive long-term, it would not justify an allocation. This could change depending on the results of Stelo or other emerging technologies or offerings. If the technology is promising enough, it may be reconsidered by the portfolio.

The Tortoise portfolio: The Tortoise portfolio would make an allocation, not a significant one at this point, because of the downside risk, but the long-term view of the company and the solid ESG considerations make it an ideal candidate for a long-term holding.

As for my portfolio, I will maintain my current allocation to DexCom for now. While I am passionate about the stock, and Stelo seems to be an amazing step forward, the current upside potential and the risk and uncertainty of how Stelo will play out do not justify an increase in allocation. There is no rush or need to fear to miss out. While emotionally, I am rooting for its success; I prefer logical-based allocations in the portfolio.

For further details see:

DexCom: Stelo Stellar Outlook