FLC - DFP And HYB: 2 Strong Funds Focused On Paying Sustainable Distributions

Summary

- DFP and HYB cut their distributions recently; DFP had cut several times through 2022.

- This isn't always bad as they focus on the longer term and do not overdistribute more than what they earn from income.

- Both are trading at attractive discounts, which makes them candidates for potential buys.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 13th, 2023.

2022 was a tough year on many investments, excluding if you were an energy investor or fund. The year was largely driven by high inflation, and the Fed aggressively raised rates to fight that inflation. We are still looking at a couple of raises left from the Fed, but most of the damage from rising interest rates should be in already. Now, 2023 seems to be a year dominated by an anticipated recession and whether that recession will be a mild or deep economic hit.

In general, closed-end funds mostly utilize borrowings on credit facilities with floating rates. That means that all else being equal, a portfolio's income generation will take a hit by rising rates. The rising rates will cause their leverage costs to rise, and without an offsetting factor such as a hedge or floating rates, net investment income will take a hit.

Two funds recently cut their distributions; Flaherty & Crumrine Dynamic Preferred and Income Fund ( DFP ) - which cut several times throughout the year - and New America High Income Fund ( HYB ). I own both, and I would add even more to either position despite what is seemingly negative for these funds.

Nobody wants to see a distribution or dividend cut, but in this case, it is focusing on longer-term sustainability over shorter-term gratification. The reason for the distribution cuts for these funds is quite simple, their income took a hit in 2022, and they focus on sustainable distributions. That means they want to cover their payouts to investors with cash coming in and not eroding their capital. When a recovery happens, they will have a larger capital base to bounce back with.

Flaherty & Crumrine Dynamic Preferred and Income Fund

The whole Flaherty & Crumrine suite of funds has a focus on paying out sustainable distributions sourced from the income generated in the portfolio. So seeing cuts across the board here isn't too surprising.

Ycharts

Yet, you might also notice a bit of an unusual spike for DFP on the chart above. That's the result of a year-end special capital gain distribution that the fund paid out.

| Year-End Long-Term Capital Gain |

| December |

| January |

| (PFD ) |

| -- |

| $0.0610 |

| $0.0610 |

| (PFO ) |

| -- |

| $0.0555 |

| $0.0555 |

| (FFC ) |

| -- |

| $0.1000 |

| $0.1000 |

| (FLC ) |

| -- |

| $0.1035 |

| $0.1035 |

| (DFP ) |

| $0.2717 |

| $0.1190 |

| $0.1190 |

This a good reminder that just because we have a down year doesn't mean that capital gains can't be found somewhere. These funds have been around for years and could have embedded capital gains on long-term held positions. Additionally, not everything goes down the same, as these are diversified funds.

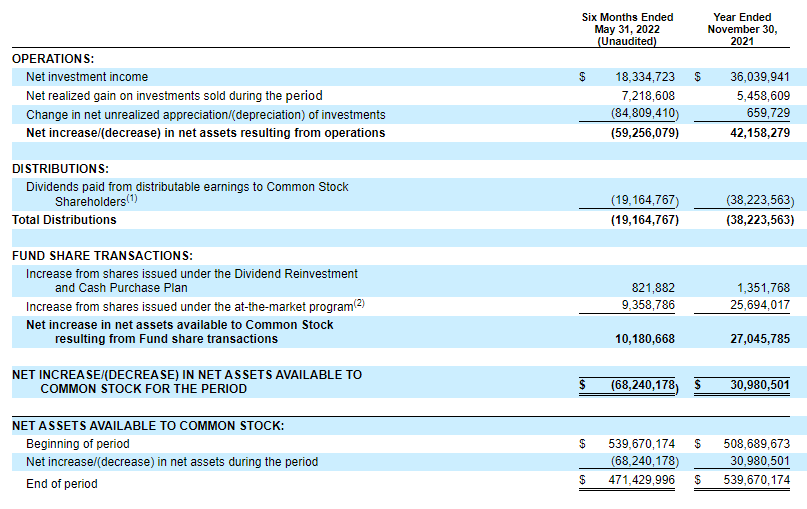

For DFP, we can see that they realized around $7.2 million in capital gains in the first half of their fiscal year. The assumption here is they didn't sell off other assets subsequently to the end of the year to offset these realized gains, which is why we would see a year-end special. We can also see that NII was slightly below the distributions paid to shareholders. Thus, directly the cause of why we've seen trims in the distribution.

{kind=link}

These funds didn't have any direct hedges in their portfolio, such as interest rate swaps or going short U.S. Treasury Futures to negate the negatives of rising rates. Therefore, they have taken the entire hit of rapidly rising interest rates.

When setting up hedges, there is a cost. The downside can be realized if the hedge doesn't end up being needed, which could have been a drag on performance. In hindsight, we know that funds that were hedged were ultimately rewarded. Whether F&C made a poor call here or not is for each investor to decide. No one can predict the future. Here's what they had to say specifically about their call not to hedge:

In general, hedging is done for two reasons: first, to reduce absolute exposure to a particular risk; and second, to reduce volatility associated with a particular risk. When considering a hedge against a rise in short-term rates, one must weigh cost versus benefit. If we knew exactly when rates would rise and by how much, then we could evaluate the explicit costs and determine if it would be a winning trade.

Since we don't know the exact timing or magnitude of higher short-term interest rates, a hedge is really another investment decision - one in which we would be betting that the cost of a hedge now (in the form of higher leverage costs today) will be lower than the actual cost of leverage (unhedged) over the hedge's timeframe. In other words, the Fund's distributable income would be lower today if we were to hedge the cost of leverage very far into the future. This is because today's upward-sloping yield curve means the market already expects rates in the future to be higher, so that expected cost is reflected in hedging cost today.

We should get their next annual report in a month or so, but until then, we know that interest rates have only risen even further since May 31, 2022. Therefore, it is safe to presume that the NII has continued to decline even further as leverage costs rose. That is supported by the latest distribution for the next quarter, once again being cut by another 3.8%.

At the end of their six-month report, they were paying one-month LIBOR plus 0.80%. That worked out to an average annualized rate of 1.101% in that period. One-month LIBOR comes in at 4.43% today , meaning they're paying 5.23% on their borrowings. The average coupon for their underlying portfolio came to 6.54% at the end of 2022. That means there is still a slight benefit, but it is a slim spread. Of course, that's only risen due to depreciation in the underlying portfolio as well.

While that doesn't sound positive, we should be nearing the end of interest rate hikes, as mentioned above. That means going forward from here, DFP is a much better choice. The fund's discount is quite attractive, too, as the fund spent a good amount of time trading at premiums in recent years. We are now seeing the fund much closer to its historical average.

Ycharts

New America High Income Fund

HYB is quite an old high-yield bond fund that has its inception going back to 1988. During this time, interest rates have essentially only gone lower and lower. Thus, the direction of their distribution has only gone lower and lower.

Ycharts

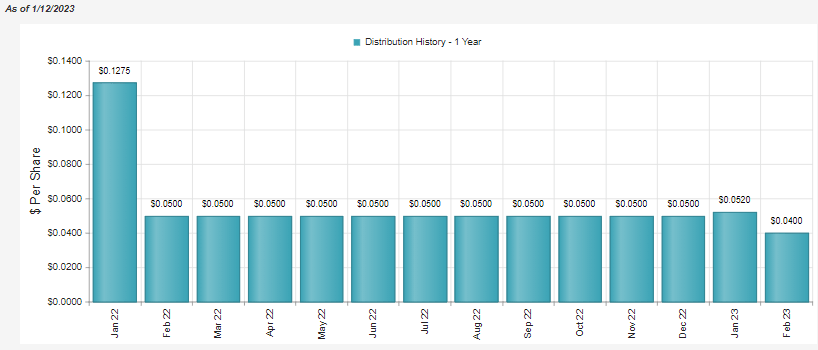

It's hard to see on the chart above, but the fund did announce a cut of $0.05 per month to the new $0.04 per month in January to the start of 2023. Interestingly, this is also after announcing a small special at the end of 2022, too.

{kind=link}

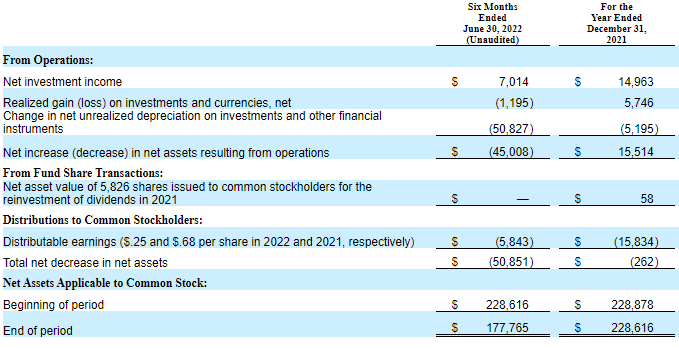

In this case, it would seem that they didn't pay out enough NII to meet the required distribution levels for a regulated investment company. They collected over $7 million but distributed less than $6 million in their six-month report . Admittedly, I would have thought that would have been enough cushion, but ultimately it wasn't. The Fed was much more aggressive as the year went on.

{kind=link}

With HYB, we will be getting a full annual report in a couple of months, giving us a better idea of what happened throughout the year in greater detail.

With rising rates, they feel the pinch of higher leverage expenses before the boost from higher yields. That's always a risk of utilizing short-term leverage and investing in longer-term debt securities. At the end of their last report, they were paying an interest rate of 2.47%. They noted that it was more than double the 0.95% they were paying at the end of 2021.

Again, it highlights the impact of the Fed's rate hikes on floating rate borrowings. They also noted the difference or spread between their borrowings and the weighted average current yield on the portfolio has narrowed, which is what we touched on above for DFP as well.

The difference between the market-value weighted average current yield on the portfolio and the rate paid on the Facility has narrowed to 4.68 percentage points at June 30th, compared to a yield spread of 5.06 percentage points as of December 31, 2021.

Given the trajectory of rates since this update, the spread here would have narrowed further. Once again, that means the actual benefit of leverage here will be limited further.

The distribution cut didn't seem to have too much of a negative impact on the fund's discount. The fund continues to trade at a fairly large discount, with the latest discount coming in line with its longer-term average. Though I would note that HYB doesn't report an NAV daily, it gets updated weekly. The discount is what makes it a particularly attractive investment, along with the fact that the Fed should be nearing the end of its rate hikes.

Ycharts

Conclusion

Distribution cuts aren't necessarily fun, but they aren't necessarily destructive to funds. In fact, they can often be more constructive to funds as that means they aren't over-distributing. Distribution cuts also don't mean that the funds haven't provided positive total returns, either.

For performance comparison purposes, I've included both the iShares Preferred & Income Securities ETF ( PFF ) and iShares iBoxx High Yield Corporate Bond ETF ( HYG ) in the performance charts below.

Ycharts

DFP and HYB focus on paying distributions from the income generated in their portfolios. A CEF can essentially pay out whatever they'd like, for as long as they'd like, without it ever being covered. The higher the distribution, usually the higher the destruction of the underlying capital.

As rates were rapidly rising, these two took a hit on their income. With rate hikes nearing an end to their cycle, the cuts going forward should slow. I believe what is more important is the current valuation of these funds in determining if they are worthwhile investments. On that basis, both of these funds are choices that investors can consider as they are at relatively attractive discounts.

For further details see:

DFP And HYB: 2 Strong Funds Focused On Paying Sustainable Distributions