PFF - DFP: This Fixed-Income CEF Is Likely To Struggle In The Near-Term

2023-09-06 09:30:03 ET

Summary

- Flaherty & Crumrine Dynamic Preferred and Income Fund offers a high distribution yield of 7.08%, but it has underperformed in the past year.

- The fund primarily invests in preferred stock and bonds, but its focus on total return is questionable for fixed-income securities.

- The fund employs leverage, which amplifies both upside and downside movements and makes it more vulnerable to rising interest rates.

- The fund tends to outperform comparable indices over long periods, but its short-term performance is disappointing.

- The fund is struggling to maintain its distributions, despite several cuts over the past year.

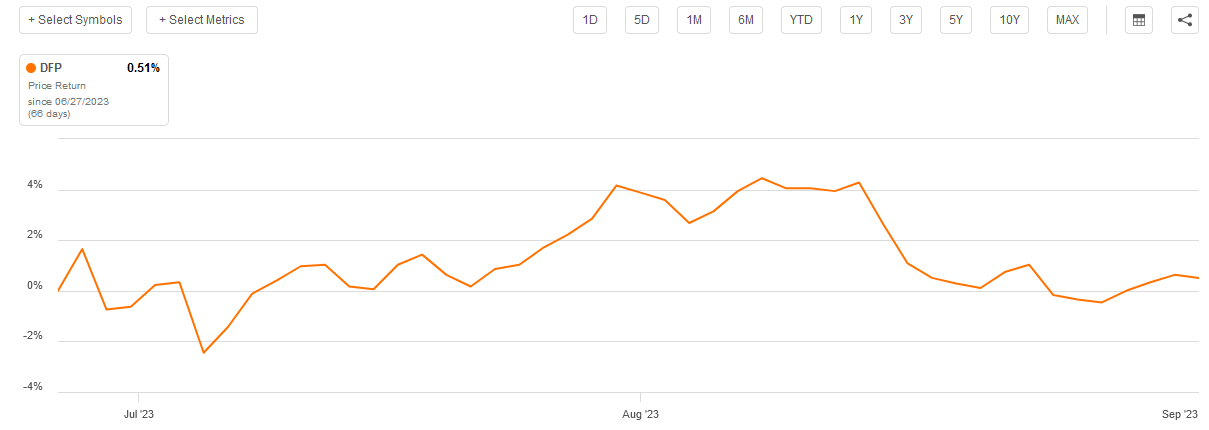

The Flaherty & Crumrine Dynamic Preferred and Income Fund ( DFP ) is one of several fixed-income closed-end funds, or CEFs, that investors can use to earn a high level of income. This is immediately apparent in the fund’s 7.08% distribution yield, which is significantly higher than most other things in the market. Unfortunately, it is not quite as high as the 7.49% yield that this fund had the last time that we discussed it . This is due to the fund delivering a fairly strong performance over the past few months. Indeed, as we can see here, the fund’s shares are up by 0.51% since my previous article on this fund was published around the end of June:

{kind=link}

This is just a short period of time, though, and in general, the fund’s performance this year has not been particularly attractive. It is down 7.85% year-to-date and is down a whopping 16.14% over the past twelve months. While this is discouraging, it is not out of line with other fixed-income funds as rising interest rates have devastated the sector. There is no real reason to believe that things will improve for the sector anytime soon, unfortunately. As such, we may continue to see funds like this one struggle even though they have somewhat adapted to the “new normal” high-rate environment.

About The Fund

According to the fund’s webpage , the Flaherty & Crumrine Dynamic Preferred and Income Fund has the objective of providing a high level of total return. This is somewhat surprising considering that the name of this fund implies that it invests primarily in preferred stock and other fixed-income securities. Its portfolio confirms this, as 59.69% of the fund’s assets are currently invested in preferred stock with most of the remainder invested in bonds:

CEF Connect

We do see a bit of money in cash and convertible securities, but the fund has nothing invested in common stock. This fits well with the fund’s own description of its objective and strategy from its webpage:

“The fund’s investment objective is to seek total return, with an emphasis on high current income.

Under normal market conditions, the fund invests at least 80% of its managed assets (defined below) in a portfolio of preferred and other income-producing securities issued by U.S. and non-U.S. companies. Preferred and other income-producing securities may include, among other things, traditional preferred stock, trust preferred securities, hybrid securities that have characteristics of both equity and debt securities, contingent capital securities, subordinated debt, and senior debt.”

In summary, this is a fixed-income fund that invests in preferred stock and bonds, which is exactly what we see in its asset allocation. This makes the company’s focus on total return rather strange, as fixed-income securities are not considered to be total return vehicles. As I explained in my last article on this fund, neither bonds nor preferred stock delivers net capital gains over their lifetimes because they lack any connection to the growth and prosperity of the issuing entity. Thus, investors should purchase these securities for income and not capital gains or total return.

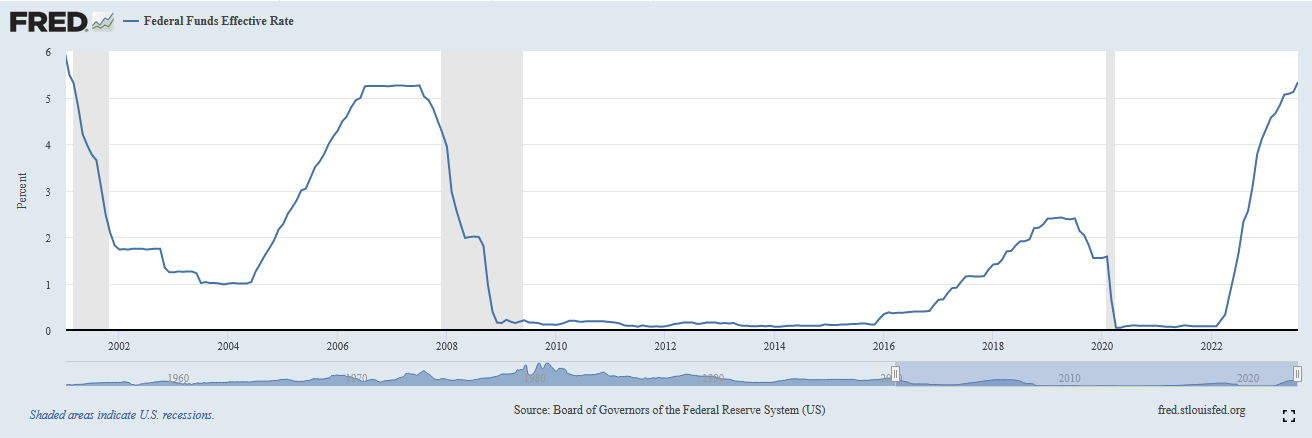

With that said, it is possible to obtain some profits by exploiting price fluctuations and trading fixed-income securities prior to maturity. It has been very difficult to accomplish this recently, though. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates to combat inflation. As of the time of writing, the effective federal funds rate is 5.33%. That is the highest level that we have seen since 2001:

Federal Reserve Bank of St. Louis

{kind=link}

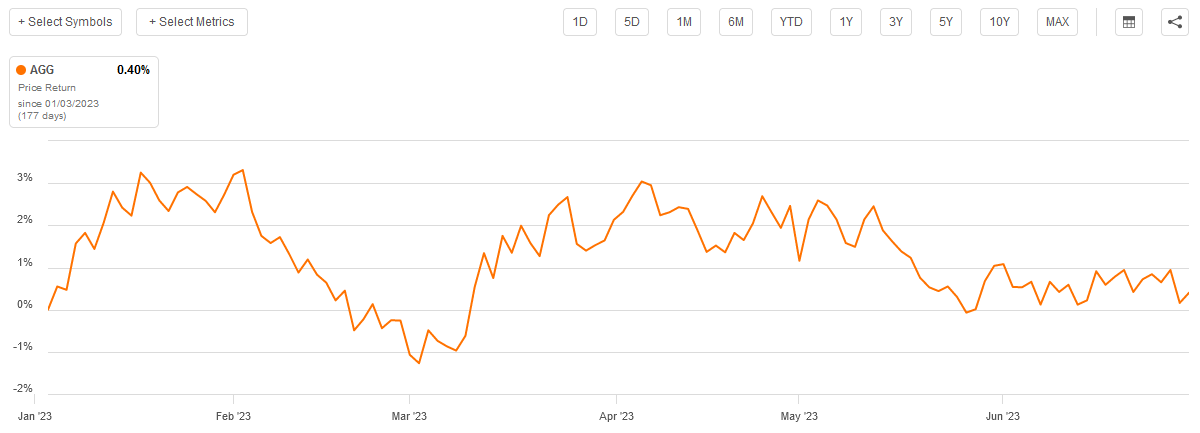

Obviously, this is quite a bit higher than the effective federal funds rate that we saw the last time that we discussed this fund. It is therefore somewhat curious that the fund’s stock price would be up, albeit barely. Then again, the market’s reaction to rising interest rates over the course of 2023 has been curious, to say the least. For the first six months of 2022, the Bloomberg U.S. Aggregate Bond Index ( AGG ) was actually up, despite the fact that the Federal Reserve did raise rates a few times during that period:

{kind=link}

This was mostly due to the expectations of numerous market participants that inflation would quickly be brought under control and the central bank would be able to cut rates during the second half of the year and into 2024. Obviously, thus far this has proven to be wrong. In fact, Chairman Powell’s recent speech at Jackson Hole implied the exact opposite. It currently seems more likely that we will see further rate hikes than a near-term rate cut. This can be expected to have a negative impact on the price of the fund’s assets, which will probably cause its share price to perform somewhat poorly. However, the severity of this will depend on the market’s perception of how long the high rates will be with us. As of the time of writing, the two-year Treasury has a higher yield than the ten-year Treasury, so the market still appears to believe that rates will not remain at today’s levels for an extended period.

In my previous article on the Flaherty & Crumrine Dynamic Preferred & Income Fund, I stated that the fund was highly weighted to the banking sector. This continues to be the case, as we can see here:

Flaherty & Crumrine

This actually represents an increase compared to the level that we saw at the end of June. At that time, 58.3% of the fund was invested in the banking sector and 21.4% was invested in insurance. So, the fund has seemingly increased its banking exposure at the expense of insurance. That is not necessarily a bad thing, particularly from the perspective of risk-averse investors. After all, banks generally receive unprecedented support from central banks and governments, which we saw earlier this year when three American banks collapsed, and the central bank stepped in to prevent further problems. Insurance companies do not generally enjoy such open-ended government support. With that said, the fund has 201 holdings so the actual risk of loss should some major institution fail is pretty low as the fund only has limited exposure to each individual issuer. The biggest risk with this fund is the market’s perception of the direction of interest rates.

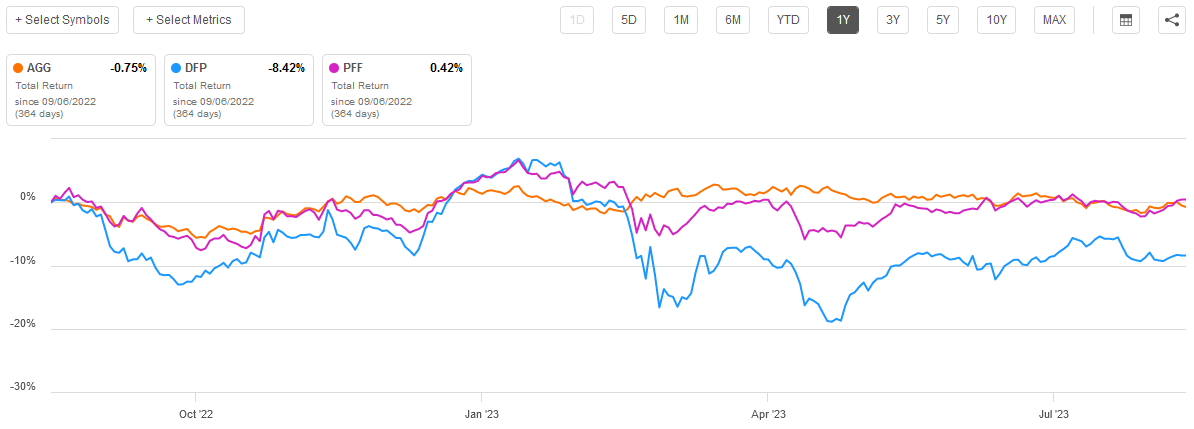

One of the most disappointing things about this fund is its performance relative to the comparable indices. These are the Bloomberg U.S. Aggregate Bond Index and the ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ). This chart compares the total return of these indices to the Flaherty & Crumrine Dynamic Preferred and Income Fund over the past year:

{kind=link}

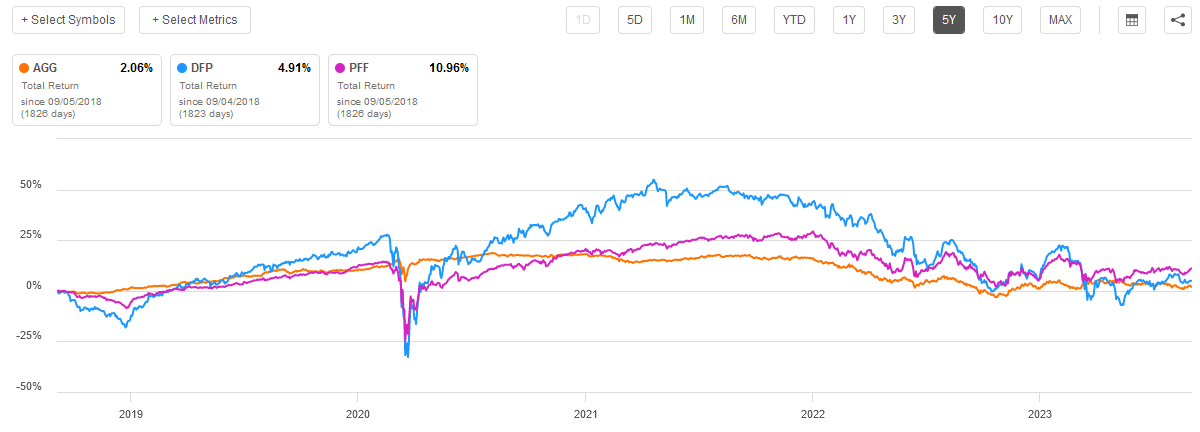

As we can see, investors in the fund would have been much better off in either of the indices than they were in the fund. This is despite the fact that the Flaherty & Crumrine Dynamic Preferred and Income Fund has a higher yield than either of the indices. We see the same thing if we look at longer periods of time, although the comparison becomes more balanced. For example, here is the fund’s total return against both indices over the past five years:

{kind=link}

In this case, the Flaherty & Crumrine Dynamic Preferred and Income Fund manages to outperform the bond index, but it still underperforms the preferred stock index by quite a lot. This is not necessarily surprising, as the above chart implies that all dividends and distributions are reinvested. This results in investors acquiring more shares of each asset over time. The yield on bonds was incredibly low relative to most preferred stocks over the past five years, which allowed the closed-end fund and the preferred stock investors to more rapidly compound their wealth. This continues over the ten-year period:

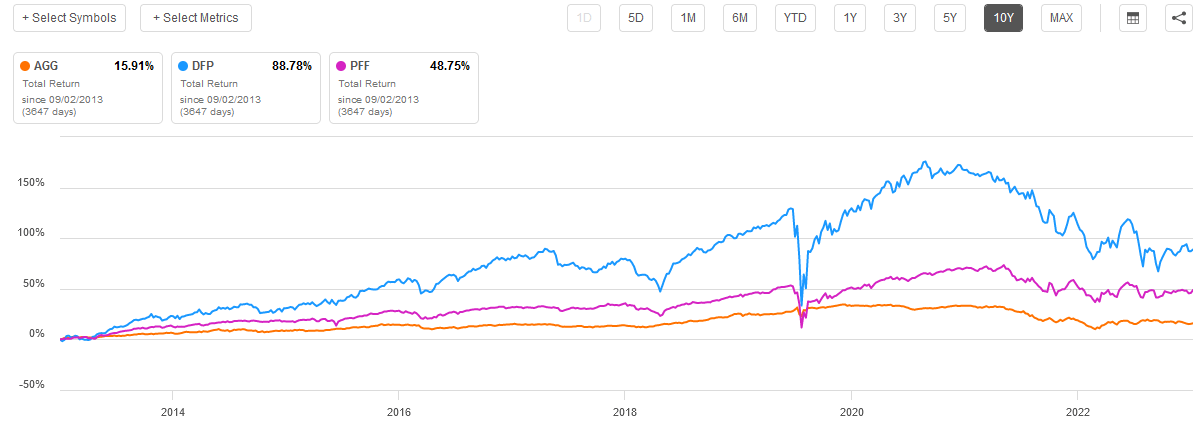

{kind=link}

Here there is almost no real comparison, as the Flaherty & Crumrine Fund completely dominates both of the indices. In fact, we can even see a marked difference between the preferred stock and the bond index, which shows the advantages of the higher yield over time.

While past performance is no guarantee of future results, we will probably see similar results going forward, at least in terms of where each of the three assets compare over the long term. The caveat here is that the Flaherty & Crumrine Dynamic Preferred and Income Fund is going to be punished much more than either of the indices when interest rates rise. Thus, if we continue to see rising interest rates going forward, investors will probably be better off in something that does not employ leverage, such as either index. Personally, I doubt that interest rates will rise over the long term due to the problems that such a scenario would impose on the Federal Government’s ability to pay the interest on the national debt. However, an interest rate cut could very easily reignite inflation.

Leverage

As just mentioned, the Flaherty & Crumrine Dynamic Preferred and Income Fund employs leverage as a method to boost the effective yield of the assets in its portfolio. I described this technique in my last article on this fund:

“In short, the fund borrows money and then uses that borrowed money to purchase preferred stock and other income-producing assets. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.”

The downside here is that the leverage amplifies both upside and downside movements. This is why this fund will decline more than the indices when interest rates rise. Unfortunately, this fund is very highly leveraged, as its leverage ratio stands at 40.65% of its assets. That is a lot higher than I normally like to see and it firmly places this fund in the high-risk, high-reward category.

Distribution Analysis

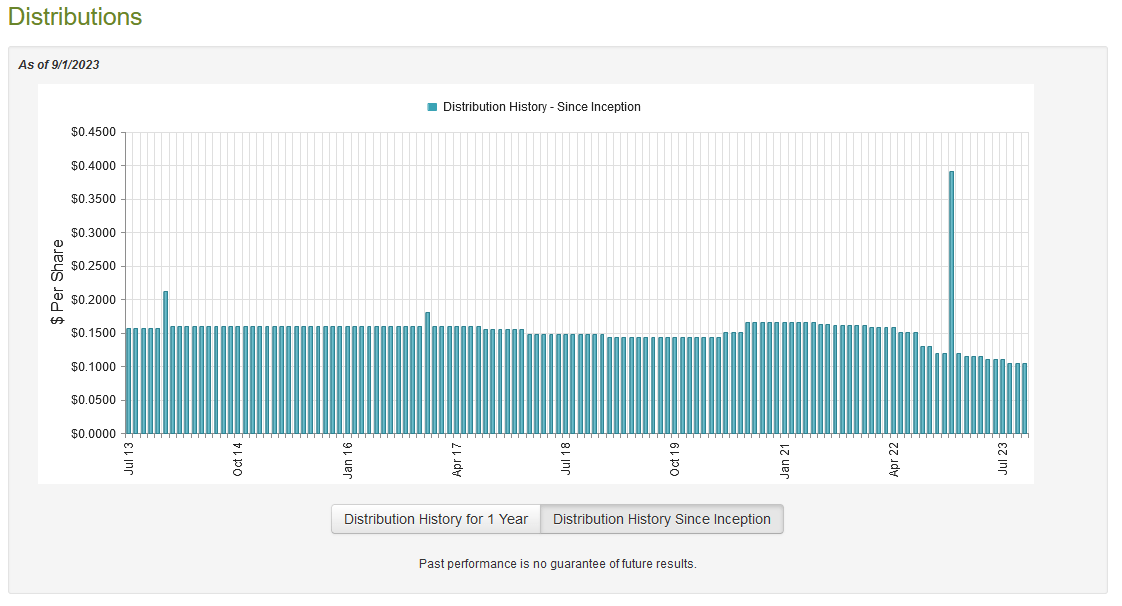

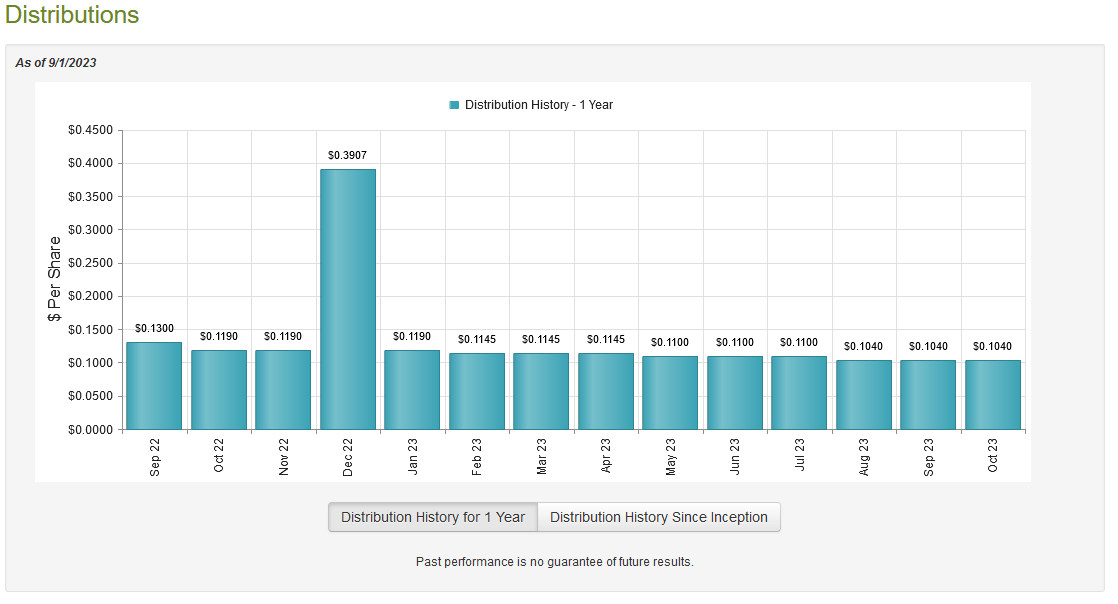

As stated earlier in this article, the fund’s primary objective is to provide its shareholders with a high level of total return. However, it seeks to accomplish this by purchasing income-producing securities that have high yields such as preferred stocks and bonds. The fund applies a layer of leverage to boost the effective yield of its portfolio and then pays most of its net investment profits to the shareholders. We might expect that this has allowed the fund to have a fairly high yield itself. This is indeed the case as the Flaherty & Crumrine Dynamic Preferred and Income Fund pays a monthly distribution of $0.1040 per share ($1.2480 per share annually), which gives it a 7.08% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over the years. As we can see here, the distribution has varied quite a bit over time:

{kind=link}

The fund has cut its distribution multiple times since the start of 2022, including four times in the past twelve months:

{kind=link}

This is almost certainly going to be a turn-off for anyone who is seeking a consistent source of income to use to pay their bills or finance their lifestyles. The majority of fixed-income funds have had to cut their payouts over the past year or two though due to the losses that rising interest rates inflicted on the portfolios of pretty much any fund holding fixed-rate securities. Knowledge of this is unlikely to be much comfort though, especially since the losses could continue to pile up if interest rates rise further.

However, anyone buying the fund today will not be affected by the fact that the fund had to cut its payout in the past. After all, they will receive the current distribution at the current yield. The most important thing for any new investor today is the fund’s ability to sustain its current payout. Let us investigate this.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a newer report than the one that we had available to us the last time that we discussed this fund. This is quite nice as it should give us a good idea of how well the fund was able to take advantage of the optimism in the bond market earlier this year. It should also give us some insight into the events that caused the fund to cut its distribution multiple times over the past several months.

During the six-month period, the Flaherty & Crumrine Dynamic Preferred and Income Fund received $8,853,281 in dividends and $14,164,955 in interest from the assets in its portfolio. When we combine this with a small amount of income that was received from other sources, the fund achieved a total investment income of $23,119,244 during the period. It paid its expenses out of this amount, which left it with $13,112,702 available for shareholders. This was, unfortunately, not nearly enough to cover the $19,782,334 that the fund actually paid out in distributions. At first glance, this is likely to be concerning as we usually like a fixed-income fund to be able to cover its distribution solely out of net investment income.

However, the fund does have other methods that can be employed to obtain the money that it needs to cover the distribution. For example, it might have capital gains that can be paid out to the investors. Unfortunately, this fund failed miserably at this task during the period. The fund reported net realized losses of $13,065,588 along with another $19,301,873 in net unrealized losses. Overall, the fund’s net assets declined by $39,037,093 after accounting for all inflows and outflows during the period. That is very concerning, but it does explain why the fund had to cut its distribution multiple times during the period. It is uncertain how sustainable the new distribution will be, but the weakness that we saw in the fixed-income market over the past month is not encouraging.

Valuation

As of September 1, 2023 (the most recent date for which data is available as of the time of writing), the Flaherty & Crumrine Dynamic Preferred and Income Fund has a net asset value of $19.64 per share but the shares only trade for $17.47 each. This gives the fund’s shares an 11.05% discount on net asset value at the current price. This is better than the 8.29% discount that the shares have traded for on average over the past month. As such, the current price certainly appears to be quite reasonable.

Conclusion

In conclusion, the Flaherty & Crumrine Dynamic Preferred and Income Fund appears likely to struggle in the near term. Its relatively high level of leverage will amplify any market weakness and it seems that interest rates are more likely to rise than fall in the near term. This will punish the fund much more so than similar funds or indices that do not have such leverage. The fund could be a good holding over the long term as it seems unlikely that rates will remain high forever, but it will be a rough ride. At the moment, potential purchasers may want to sit on the sidelines until we have some more certainty about the direction of interest rates and the broader economy.

For further details see:

DFP: This Fixed-Income CEF Is Likely To Struggle In The Near-Term