PTA - DFP: This Is A Popular Fund But Investors Should Look Elsewhere

2023-11-14 09:37:22 ET

Summary

- Flaherty & Crumrine Dynamic Preferred and Income Fund's distribution yield is no longer impressive compared to other fixed-income closed-end funds.

- The DFP closed-end fund's performance over the past few weeks has been strong, but it may have been run up too far.

- The fund's use of leverage and declining distribution raise concerns about its sustainability and ability to generate returns.

- Interest rates may remain higher than many market participants expect, which would weigh tremendously on this fund's returns.

- The fund is trading at a double-digit discount on NAV, but there are better options out there.

The Flaherty & Crumrine Dynamic Preferred and Income Fund ( DFP ) is a very popular closed-end fund, or CEF, among those who are seeking to earn a high level of income from the assets in their portfolios. This is partly because of the fund’s 7.58% distribution yield, which used to be considered fairly high. However, this yield is nowhere near as impressive as it once was, as pretty much any closed-end fund that invests in junk bonds or floating-rate securities can beat this yield today. In fact, we can even find other preferred stock funds that boast higher yields:

| Fund |

| Current Yield |

| Flaherty & Crumrine Dynamic Preferred and Income Fund |

| 7.58% |

| Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund ( PTA ) |

| 9.30% |

| John Hancock Preferred Income Fund ( HPI ) |

| 10.43% |

| First Trust Intermediate Duration Preferred & Income Fund ( FPF ) |

| 8.69% |

| Cohen & Steers Select Preferred and Income Fund ( PSF ) |

| 8.40% |

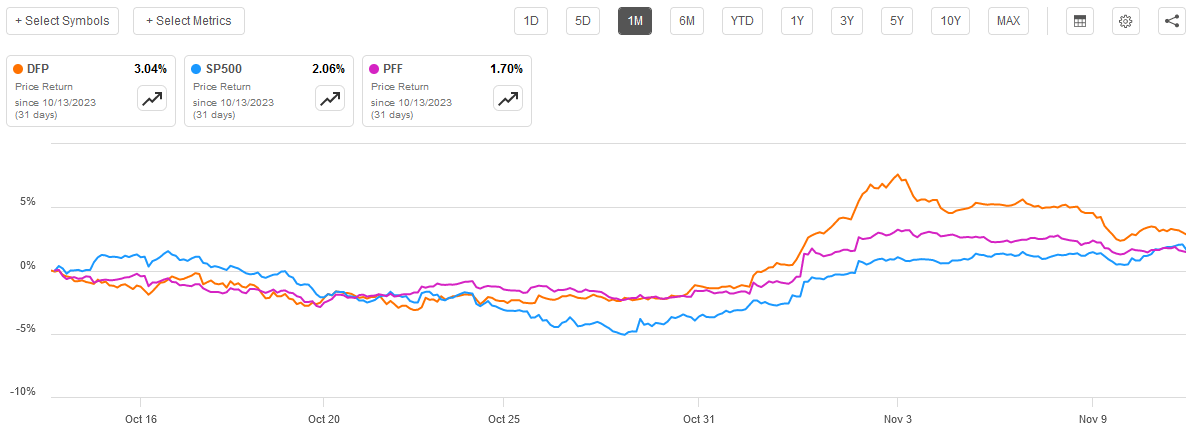

Clearly, this fund’s current yield is nowhere near as attractive as it once was. That does not seem to have hindered the fund’s popularity though, as its shares went up 3.04% over the past month. This was a better performance than either the S&P 500 Index ( SP500 ) or the iShares Preferred and Income Securities ETF ( PFF ) over the same period:

{kind=link}

Unfortunately, this strong recent performance may be a sign that the fund’s shares have gotten ahead of themselves. We will discuss this over the course of this article.

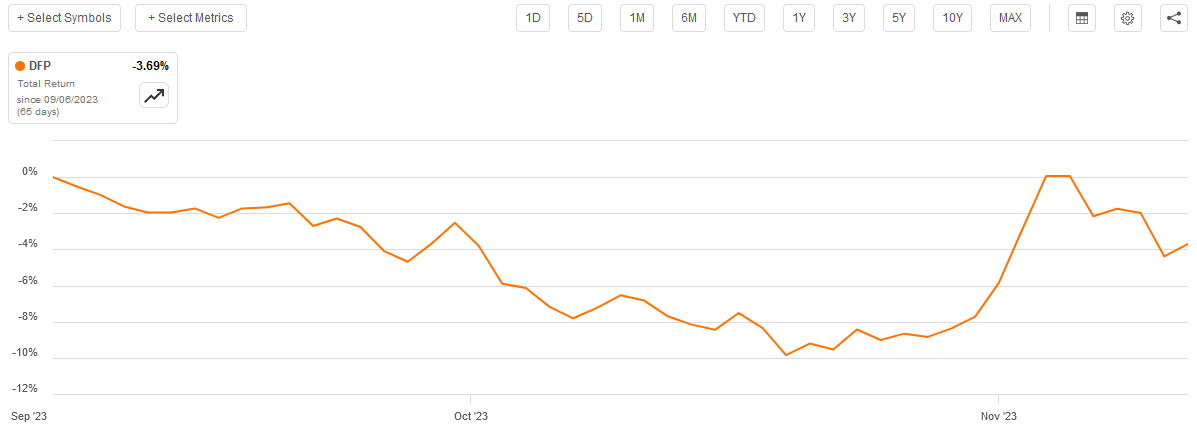

As regular readers may recall, we last discussed the Flaherty & Crumrine Dynamic Preferred and Income Fund in early September. The market has been interesting since that time as most of the months of both September and October were characterized by rising interest rates and falling asset prices. However, that trend reversed in late October as investors started to expect that rates would decline in the near term and resumed their aggressive buying of income-producing assets. This includes the shares of this fund, which shot up in price around the final week of October. However, investors in the fund have still realized a negative total return since the last time that we discussed it:

{kind=link}

That is certainly a performance that seems unlikely to appeal to any investor, although we all know that past performance is no guarantee of future results. Unfortunately, there are some reasons to believe that this fund may continue to struggle in the near term as recent events make it unlikely that rates will be reduced anytime soon. That is, of course, what this fund would need in order to deliver a reasonably impressive forward performance.

About The Fund

According to the fund’s website , the Flaherty & Crumrine Dynamic Preferred and Income Fund has the primary objective of providing its investors with a very high level of total return, although it expects much of that total return to come in the form of distributions paid to shareholders. This focus on total return is a little surprising for a closed-end fund that focuses on investing in the fixed-income market. We would ordinarily expect that a fixed-income fund will simply focus its efforts on achieving a high level of current income. After all, bonds do not provide any net capital gains over their lifetimes because they are both issued at and redeemed for face value and have no inherent link to the growth and prosperity of the issuing company. The same thing is true for preferred stocks, although they may not have a maturity date.

The name of this fund suggests that it invests primarily in preferred stock. That is currently the case, although its weighting is not exactly as heavily tilted to preferred securities as might be expected. As we can see here, only 61.37% of the fund is invested in preferred stock:

CEF Connect

In addition to the expected preferred stock, we see a large 32.20% allocation to bonds or similar debt securities. This is in line with the fund’s description of its investment strategy as provided on the website. This description reads:

Under normal market conditions, the Fund invests at least 80% of its Managed Assets in a portfolio of preferred and other income-producing securities issued by U.S. and non-U.S. companies. Preferred and other income-producing securities may include, among other things, traditional preferred stock, trust preferred securities, hybrid securities that have characteristics of both equity and debt securities, contingent capital securities, subordinated debt and senior debt.

As I have discussed in numerous previous articles, bonds provide all of their net investment returns in the form of direct payments to the investors. Thus, they certainly qualify as income-producing assets under this definition. The majority of them are considered to be either subordinate or senior debt in the above description.

One thing that we noticed above is that the fund’s allocation to both preferred stock and bonds has increased since the last time that we discussed it. The fund has also acquired a very small allocation to common stock, which may be due to it exercising the option to convert some of the convertible securities to common stock of the issuing entity. This conclusion is derived from the fact that the fund’s weighting to both cash and convertible securities has decreased over the past two months.

It makes a lot of sense that the fund would opt to change its weightings as it did when we consider the time period in question. In the previous article on the fund, the most recent snapshot of the fund’s holdings was dated May 31, 2023. This one is dated August 31, 2023. As everyone reading this likely knows, the market reversed its bear market bounce around mid-July and went into a period of decline as both bond and preferred stock yields started to rise. This period of rising yields continued over the course of both July and August. The fund’s management may have seen fit to buy some income-producing securities around that time and lock in a high level of income for the portfolio. The fund’s 7.00% annual turnover suggests that it does not trade very much, so this easily could have been a long-term position that provides the fund with a very high level of income over the next several years. If indeed that was the case, this is a rather shrewd maneuver on the part of the fund’s management. The general popularity of this fund here at Seeking Alpha and elsewhere suggests that many investors have a positive opinion of this fund’s management and moves such as the one described could be a reason why this is the case.

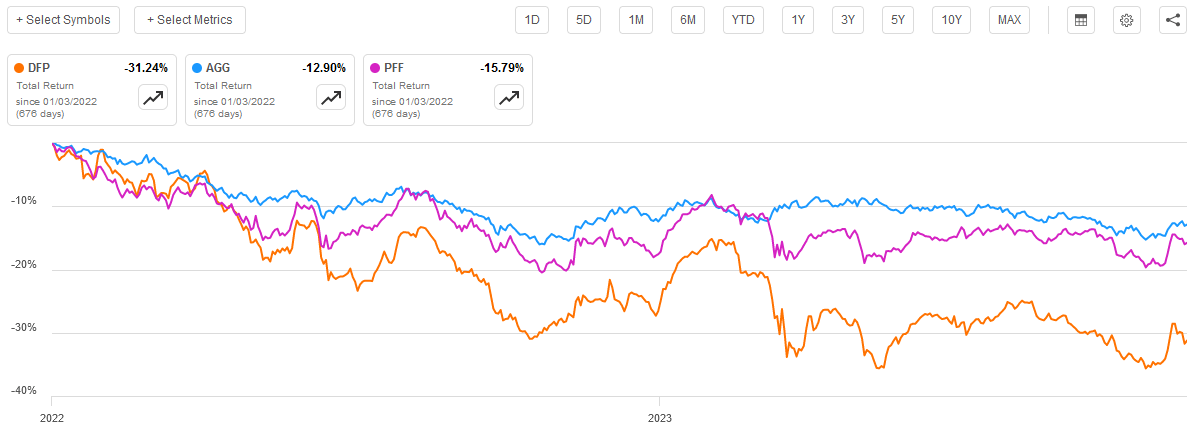

As everyone reading this is no doubt well aware, the Federal Reserve’s monetary tightening policy over the past two years has had a detrimental effect on the prices of just about every asset. However, bonds, preferred stocks, and other assets that pay out a fixed amount to investors on a regular basis have had a pretty terrible time. We can see this in the fact that the Bloomberg U.S. Aggregate Bond Index ( AGG ) has delivered a negative 12.90% total return since January 1, 2022. The ICE Exchange-Listed Preferred and Hybrid Securities Index delivered a negative 15.79% total return over the period. This fund performed even worse than either index, as it delivered a negative 31.24% total return since the start of 2022:

{kind=link}

One thing that we see is that duration has had a significant impact on the total return provided by each of the three assets. Preferred stocks tend to have higher yields than bonds, but because they have either no maturity date or a maturity date that is very far off into the future, it takes them longer to return an investor’s money than bonds, which pay back their face value at maturity. The maturity of most corporate bonds is usually not nearly as far into the future as most preferred stocks so ultimately, they return the investor’s initial investment more rapidly and so hold up better when interest rates rise.

This fund would appear to be an exception to the rule that we just discussed, however. As this fund invests in both preferred stocks and bonds, it might be expected that it would have a total return between the two assets. However, this was proven to not be the case.

The fund’s net asset value is down 30.01% since the start of 2022, so this is not the case of a fund’s share price substantially underperforming its net asset value, as we may sometimes see. This fund’s problem is its use of leverage, which we will discuss later in this article. This leverage means that both gains and losses are amplified, and of course over the period in question losses were much more prevalent. Thus, investors were left with a very disappointing total return.

Interest Rate Trajectory

However, that is the past, and past performance is no guarantee of how a fund will perform in the future. In addition, anyone who buys this fund today will not be hurt by the fund’s disappointing performance over the past two years. They will only be impacted by how well this fund performs going forward. The fund’s forward performance will almost certainly be determined by the direction that interest rates go from here.

It is almost a fool’s errand to try and predict what the Federal Reserve will do as far as interest rates go. After all, the ability of the central bank to properly evaluate the economy is much less than some people want to believe. For example, this is the same central bank that claimed that the subprime mortgage crisis in 2008 was nothing worth worrying about and that inflation was likely to be transitory in 2021. As such, the central bank’s track record of identifying macroeconomic events is not especially good.

With that said the members of the Federal Open Market Committee are currently projecting that interest rates have peaked and are likely to head downward soon. The members of this committee expect that the federal funds rate will decline in 2024, 2025, and 2026:

{kind=link}

That would ordinarily point to a likelihood that interest rates will be lower in the future. If that prediction proves to be the case, then the Flaherty & Crumrine Dynamic Preferred and Income Fund will likely benefit as falling rates will cause the value of the securities in its portfolio to go up.

However, interest rates are a function of more than just Federal Reserve policy. They are actually driven by the supply and demand for money. This may unfortunately suggest that interest rates will be higher going forward no matter what the Federal Reserve does. For example, it would be an understatement to say that the Federal Government is demanding an extremely high amount of money right now and will almost certainly continue to do so for the foreseeable future. Here is what the Congressional Budget Office has to say on the matter :

CBO projects a federal budget deficit of $1.4 trillion for 2023. In the agency’s projections, deficits generally increase over the coming years; the shortfall in 2033 is $2.7 trillion. The deficit amounts to 5.3 percent of gross domestic product in 2023, swells to 6.1 percent in 2024 and 2025, and then declines in the two years that follow. After 2027, deficits increase again, reaching 6.9 percent of GDP in 2033 – a level exceeded only five times since 1946.

Historically, the Congressional Budget Office underestimates deficits so it seems likely that the actual outcome will be worse than the above prediction suggests, and the above prediction is already bad enough.

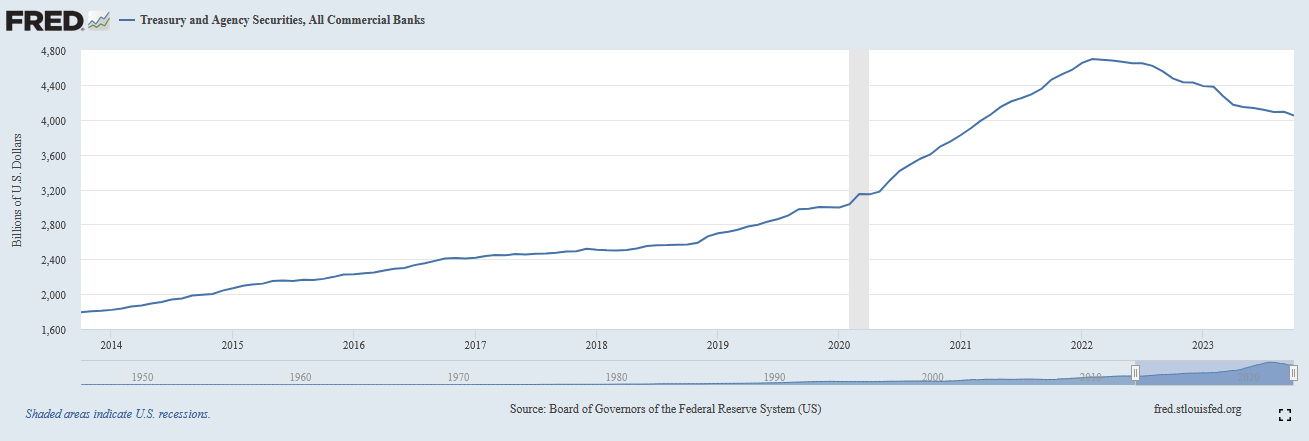

Naturally, the Federal Government will have to finance these budget deficits through the issuance of bonds. That requires someone to be on the other side with money to buy them. There are some signs that this is becoming more difficult. Last week, the government conducted a thirty-year bond auction on Thursday that went horribly. The final yield ended up being a lot worse than expected, and various media outlets suggest that this was due to a lack of demand. In addition to this, the Federal Reserve reports that American commercial banks, historically avid buyers of U.S. Treasuries and agency securities, have been dumping their holdings of these securities:

{kind=link}

In short, there is evidence that investors are increasingly unwilling to loan money to the Federal Government at today’s rates. That means that either rates have to go up or some big buyers will need to enter the market to supply the demand for Treasuries and agency securities that private buyers will not. That buyer would have to be the Federal Reserve, which would effectively print money in order to purchase newly issued Treasury securities. This results in inflation.

Thus, regardless of what the Federal Reserve says about the future trajectory of interest rates, it may not be able to get lower rates unless it is willing to accept a much higher level of inflation.

While the Flaherty & Crumrine Dynamic Preferred and Income Securities Fund is investing in corporate securities, not Treasuries or agency securities, it seems unlikely that corporate borrowers will be able to borrow U.S. dollars at a lower interest rate than the government. Thus, its ability to deliver strong near-term capital gains from falling interest rates may be much less than some investors hope for. With that said though, the securities in it should still be able to provide a respectable level of income, it is just that capital gains will be less than some market participants hope.

Leverage

As mentioned earlier in this article, the Flaherty & Crumrine Dynamic Preferred and Income Fund employs leverage as a method of boosting its effective yield beyond that of any of the underlying assets in the fund. I explained how this works in my previous article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase preferred stock and other income-producing assets. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

As of the time of writing, the Flaherty & Crumrine Dynamic Preferred and Income Fund has levered assets comprising 41.35% of its portfolio. This is higher than the 40.65% leverage that the fund had the last time that we discussed it, and it is unfortunately a lot more than the one-third maximum that I typically like to see any fund possess. As such, the fund is almost certainly going to be much more volatile than a comparable fund that does not have such a high degree of leverage. This could be a problem if rates continue to rise and cause the fund’s asset values to decline more rapidly than would ordinarily be expected from such an increase.

While it is possible that this fund will benefit from falling interest rates to a much more substantial degree than a comparable fund that employs less leverage, I do not think that it is likely that rates will fall significantly in the near term. As such, I would prefer a fund with a lower level of leverage in today’s environment.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Flaherty & Crumrine Dynamic Preferred and Income Fund is to provide its investors with a very high level of total return. The fund aims to deliver those total returns by purchasing preferred stock and bonds, which primarily deliver their investment returns in the form of direct payments to the shareholders. It then applies a layer of leverage to artificially boost the total amount of money that it has coming into its accounts from these securities. This fund collects the payments that it receives from these sources and then pays them out to the shareholders, net of its own expenses. As such, we might expect that this fund would have a very high yield itself.

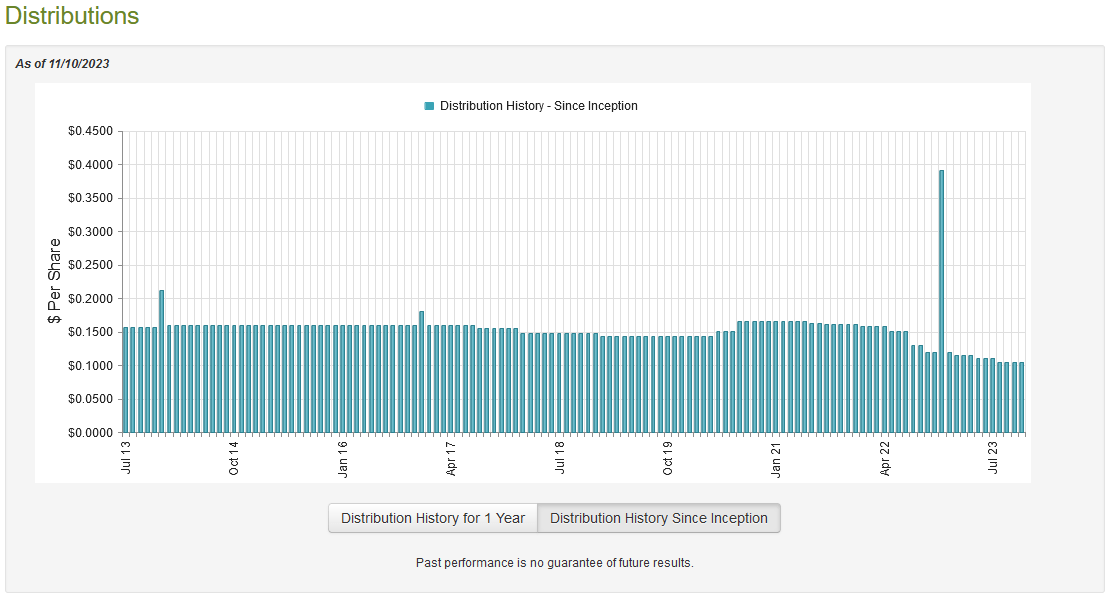

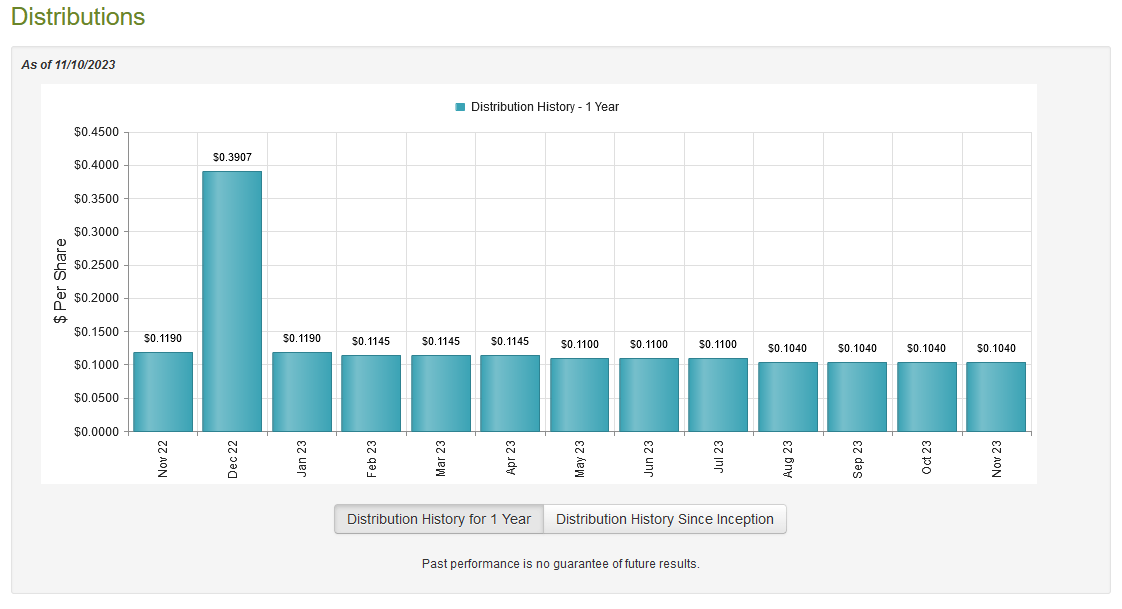

This is indeed the case, as the Flaherty & Crumrine Dynamic Preferred and Income Fund pays a monthly distribution of $0.1040 per share ($1.248 per share annually), which gives it a 7.58% yield at the current share price. This is reasonable, but as mentioned in the introduction, it is a much lower yield than other fixed-income funds have been able to provide in recent months. This fund has unfortunately not been very consistent with respect to its distribution, and it has been steadily cutting it over the past two years:

{kind=link}

This seems highly unlikely to appeal to any income-focused investor today. After all, inflation is causing the price of everything that we purchase to go up, so we certainly do not want a declining income that amplifies the loss of our purchasing power. If these cuts had taken place years ago, we might be able to forgive them, but this fund has cut the payout three times in the past twelve months:

{kind=link}

In short, this past performance is highly unlikely to endear this fund to any income-focused investor today. However, anyone purchasing the fund today will not be affected by these cuts. This is because such an individual will receive the current distribution at the current yield. As such, the most important thing for our purposes today is how well the fund can sustain its distribution at the current level. Let us investigate this.

Fortunately, we have a somewhat recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. As such, it will not include any information about the fund’s performance over the past five months or so. However, it will give us a good idea of how well this fund managed to perform in the reasonably strong and optimistic market that dominated the first half of this year. This was a period in which investors were widely anticipating that the federal funds rate would quickly be cut and so they were grabbing up income-producing assets in order to lock in what they saw as high yields at the time. While this was ultimately proven to be an incorrect assumption, the fund could have been able to generate some profits by selling securities into an overly optimistic and lively market.

During the six-month period, the Flaherty & Crumrine Dynamic Preferred and Income Fund received $8,853,281 in dividends along with $14,164,955 in interest from the assets in its portfolio. When we combine this with a small amount of income that was received from other sources, the fund had a total investment income of $23,119,244 during the period. It paid its expenses out of this amount, which left it with $13,112,702 available for the shareholders. As might be expected, that was nowhere close to enough to cover the $19,782,334 that the fund paid out in distributions during the period. At first glance, this is almost certainly going to be concerning since we usually like fixed-income funds to completely cover their distributions out of net investment income. This one obviously failed to accomplish that task.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, it might be able to realize capital gains by selling preferred stock or bonds at a time when interest rates fall, and asset valuations rise. Unfortunately, this fund failed miserably at that task during the period in question. The fund reported net realized losses of $13,065,588 along with $19,301,873 net unrealized losses during the period. Overall, the fund’s net assets declined by $39,037,093 after accounting for all inflows and outflows during the period.

This certainly explains why the fund’s management has been cutting the distribution repeatedly over the past year. Clearly, this fund is not generating enough investment returns to pay its distribution, so its asset base is deteriorating. This is not sustainable over any extended period of time. The fund did cut its distribution after the most recent financial report was published, so it is not certain how well the fund is able to cover its distribution at the new lower level. This is something that we will want to carefully evaluate once the fund releases its full-year report, which should occur in about two months.

Valuation

As of November 10, 2023 (the most recent date for which data is available as of the time of writing), the Flaherty & Crumrine Dynamic Preferred and Income Fund has a net asset value of $19.08 per share but the shares currently trade for $16.44 each. This gives the fund’s shares a 13.84% discount on net asset value at the current price. That is a reasonable discount, and in fact, I generally consider any double-digit discount to represent a reasonable price to buy shares of a closed-end fund. However, the current discount is not nearly as attractive as the 14.57% discount that the shares have had on average over the past month. Thus, it might be possible to obtain a better price by waiting for a bit. Realistically though, the current price represents a very large discount on the intrinsic value of the shares so it should be a reasonable entry price for the fund’s shares.

Conclusion

In conclusion, the Flaherty & Crumrine Dynamic Preferred and Income Fund is a very popular fixed-income fund that appears to have fallen on some hard times. The fund has been devastated by the rise in interest rates that we have seen over the past two years, and this has caused it to take heavy realized and unrealized losses. The fund has also had to impose multiple distribution cuts on its shareholders as it attempts to maintain its net asset value in the new economic climate.

Unfortunately for Flaherty & Crumrine Dynamic Preferred and Income Fund, it does not appear likely that interest rates will decline in the near future, which is problematic as the fund needs lower rates to reduce its leverage ratio and address the declining net asset value. At least the fund’s price is reasonable, but the low yield and poor performance may make it best to look elsewhere.

For further details see:

DFP: This Is A Popular Fund, But Investors Should Look Elsewhere