DHT - DHT Holdings Is Cheap In The Short Run But Beware Of Its Long-Term Risks

2024-01-17 05:47:18 ET

Summary

- DHT Holdings is thriving thanks to short-term tailwinds in the shipping industry and a positive outlook.

- The company's strong balance sheet and limited new supply of VLCCs contribute to its success.

- DHT stock has rallied 50% off its bottom last summer, but it is still trading at a forward price-to-earnings ratio of only 7.2x.

- Investors should be cautious of the industry's cyclicality and consider selling the stock around its 10-year high.

DHT Holdings ( DHT ) is thriving thanks to some short-term tailwinds in its business. The stock has rallied 26% in the last 12 months but it remains remarkably cheaply valued, as it is trading at a forward price-to-earnings ratio of only 7.2x . Even better, the outlook is positive in its business, as the new supply of VLCCs (very large crude carriers) is low and a significant portion of the existent fleet is old. Given also the strong balance sheet of the company, some investors may rush to initiate a large stake in the shipping company.

However, the shipping industry is infamous for its dramatic boom-and-bust cycles. Therefore, DHT Holdings is not a buy-and-hold stock. While the stock may easily offer an additional 9% capital gain in the near future, up to the technical resistance of its 10-year high of $12, conservative investors should probably sell the stock around that level due to the inherent risks of the company.

Business overview

DHT Holdings is a crude oil tanker shipping company, which was founded in 2005 and now has 24 VLCCs. The company is currently thriving thanks to some tailwinds in its business. First of all, the war in Ukraine, which began almost two years ago, has taken some VLCCs out of the market and thus it has shifted the supply-demand relationship in favor of DHT Holdings.

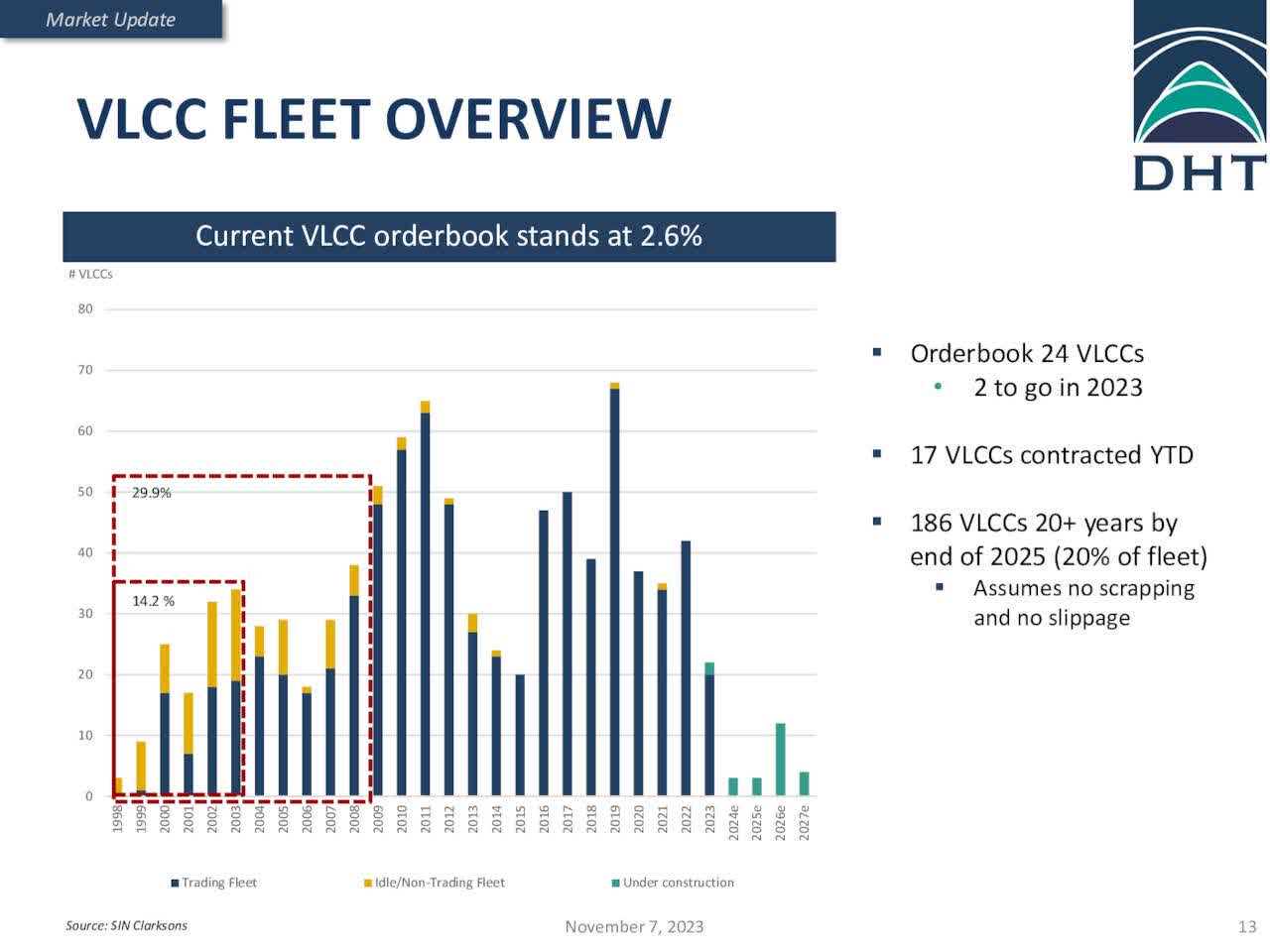

The shipping company also benefits from the limited new supply of VLCCs, while the existing vessels age at a fast pace.

{kind=link}

About 20% of all the existing VLCCs will be older than 20 years by the end of 2025 while the number of the vessels that are under construction is only 2.6% of the total fleet. As a result, the global market of VLCCs is likely to remain tight for the foreseeable future.

Last week, DHT Holdings announced that it estimated its gross earnings around $42,800 per vessel per day in the fourth quarter of 2023. This level is nearly double the average amount per day of $22,200 earned just two years ago. Even better, the company has booked 50% of its spot days at an average rate of $56,300 in the first 10 days of this year. In other words, DHT Holdings is likely to improve its earnings even further in the running quarter, in the absence of an unforeseen headwind. The accelerated momentum this year has resulted primarily from the Middle East crisis, which has led many shipping companies to avoid the Red Sea, thus resulting in much higher freight rates.

The favorable business landscape is clearly reflected in the performance of DHT Holdings in the first nine months of 2023. The company posted earnings per share of $0.77, which was more than triple the earnings per share of $0.25 of the company in the entire year 2022. Thanks to the sustained favorable trends in its business, the company is expected by analysts to post earnings per share of $1.02 for 2023, in line with its performance in the first nine months of the year.

Moreover, thanks to the tension in Middle East and the tight global market of VLCCs, analysts expect DHT Holdings to grow its earnings per share 49% this year, from $1.02 to $1.52. It is also important to note that DHT Holdings secures a great portion of its earnings by time-chartering its vessels, i.e., booking its rates for many voyages in advance. This strategy results in more reliable earnings in the short run than the earnings of companies in other sectors. To be sure, during the last six months, analysts have revised their earnings-per-share estimates for DHT Holdings by just -2% for 2023 and by just +7.5% for 2024. Therefore, given also the positive industry trends, one can reasonably expect DHT Holdings to approximately meet or exceed the above-mentioned estimate of $1.52 this year.

On the other hand, it has proved impossible to make long-term forecasts of the earnings of shipping companies due to the dramatic cyclicality of the shipping industry. During boom periods, such as the current one, many shipping companies tend to expand their fleet by constructing new vessels. Whenever a recession or a downturn in the shipping industry shows up, the excess new supply results in a collapse of freight rates. This is exactly what the shipping industry has been experiencing for decades. While the backlog of new VLCCs is currently limited, it may significantly increase if the current boom persists for an extended period.

The extreme volatility of freight rates is depicted in the performance record of DHT Holdings. First of all, despite its recent rally, the stock is still trading 95% lower than its adjusted all-time high of $216, which was posted in 2007, just before the onset of the Great Recession. In other words, the shareholders who have been holding the stock since 2007 have essentially lost all their capital.

The extreme volatility of freight rates is also evident in the 10-year performance record of the company. DHT Holdings has incurred losses in 3 of the last 10 years while it has also posted low earnings per share (lower than 5% of the current stock price, resulting in P/E ratios above 20 at the current stock price) in another 5 years. To cut a long story short, it is extremely unlikely that DHT Holdings has entered a sustainable growth trajectory. It will almost certainly face a recession or a downturn in its business at some point in the upcoming years, which will probably lead the earnings of the company to collapse.

Balance sheet

Unlike many shipping companies, which carry an excessive amount of debt, DHT Holdings has a strong balance sheet . It has a current ratio of 2.3 and net debt (as per Buffett's formula: net debt = total liabilities - cash - receivables) of $341 million. This amount is only 20% of the market capitalization of the stock and less than twice the earnings of the company in the last 12 months. Moreover, interest expense consumes just 11% of operating income. Overall, DHT Holdings has a markedly strong balance sheet.

This is paramount in the highly cyclical shipping industry, as it will almost certainly help the company endure the next downturn in its business without any problem. More precisely, the earnings of DHT Holdings will inevitably plunge upon the next downturn but the company is not likely to have any problem servicing its debt and thus it will wait patiently for the downturn to subside.

Dividend

DHT Holdings paid total dividends of $1.15 in 2023. This amount of dividends corresponds to an exceptionally high yield of 11.4% at the current stock price. Even if only the dividend of the fourth quarter is taken into account ($0.19), it corresponds to an annualized dividend yield of 6.9%, which is above average.

However, investors should be aware that the dividend of DHT Holdings is much less reliable than the dividends of most stocks in other sectors. To be sure, DHT Holdings offers a different dividend every quarter, depending on its actual earnings and its outlook. Given the high volatility of the shipping industry, it is only natural that the dividend of DHT Holdings has been extremely volatile. To be sure, the company cut its dividend by 91% in 2021, from $1.08 to $0.10. As long as the VLCC market remains tight, the stock will keep offering an attractive yield but the company is likely to slash its dividend significantly whenever the next downturn of the shipping industry shows up.

Valuation

As mentioned in the introduction, DHT Holdings is trading at a forward price-to-earnings ratio of only 7.2x. Even better, thanks to the aforementioned positive outlook of the global VLCC market, analysts expect the company to grow its earnings per share by 18% in 2025, from $1.52 to $1.79. This means that the stock is trading at only 6.1 times its expected earnings in 2025. Therefore, while the stock has rallied 50% off its bottom last summer, it remains cheaply valued from a short-term perspective.

It is extremely hard to identify a stock with such a low price-to-earnings ratio, earnings growth and a solid balance sheet. It is thus likely that the stock will maintain its positive momentum in the near term and gain another 9%, up to the technical resistance of its 10-year high of $12.

On the other hand, investors should be aware that there is a good reason behind the exceptionally cheap valuation of this stock. Due to the extremely volatile and cyclical nature of freight rates, shipping companies are not buy-and-hold stocks. To be sure, DHT Holdings has dramatically underperformed the broad market over the last decade, as it has gained 33% whereas the S&P 500 has rallied 160% . During the last 15 years, DHT Holdings has plunged 85% whereas the S&P 500 has rallied 460%. Overall, DHT Holdings is likely to continue to underperform the S&P 500 by a wide margin over the long run due to the inherent cyclicality of its industry. Therefore, investors should take their profits when the stock approaches its technical resistance of $12. The stock may rally even further but its long-term risk does not compensate investors adequately for holding the stock for a longer period.

Final thoughts

Thanks to favorable business fundamentals, DHT Holdings is on track to post nearly 10-year high earnings per share this year. This helps explain the 26% rally of the stock in the last 12 months, towards its 10-year high. The company should also be praised for maintaining a strong balance sheet, which is paramount in this highly cyclical industry. While the stock appears cheaply valued from a short-term perspective, it is risky around its 10-year high from a long-term perspective due to the fierce downturns that occur in the shipping industry every few years.

For further details see:

DHT Holdings Is Cheap In The Short Run But Beware Of Its Long-Term Risks