DHT - DHT Holdings: Printing Cash At Attractive Valuation

2023-07-19 05:42:27 ET

Summary

- With a dividend distribution of 100% of EPS and a shares repurchase program in place, DHT is ready to deliver enhanced returns to its shareholders.

- One of the lowest leverage plays in the tanker universe with an 18.8% net debt to total asset ratio.

- An attractive valuation entry point with the equity currently trading at a 9.4% discount to its net asset valuation.

Key Takeaway

Despite the market forecasts of growing oil demand, particularly in the second half of the year, the ongoing OPEC+ cuts since May are expected to challenge the market during the seasonally weaker summer months. However, the long-term fundamentals for the VLCC tanker market remain unchanged. With only 11 ships projected to be delivered in 2023 and no substantial VLCC ordering taking place, the risk for the VLCC market is skewed to the upside.

In this context, DHT Holdings ( DHT ), which is about to become a 100% scrubber VLCC play, emerges as a significant player in the industry. By increasing its exposure to the spot charter market, ahead of the seasonally strong winter months, DHT is well-positioned to deliver enhanced shareholder returns.

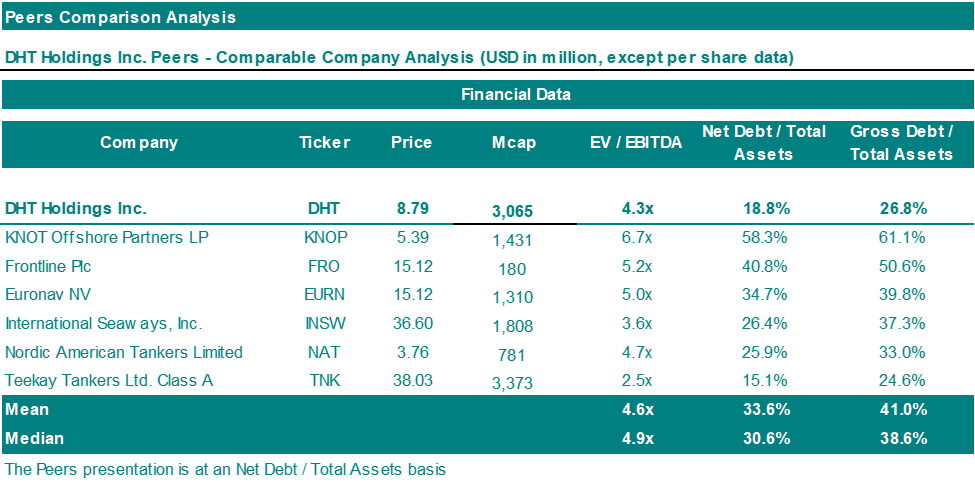

1. The Company has actively managed its capital structure by successfully refinancing its credit facility with ABN AMRO. DHT's net debt to total assets ratio of 18.8% stands as one of the lowest in my tanker equity universe, where the average ratio stands at 33.6%, highlighting the Company's strong financial position.

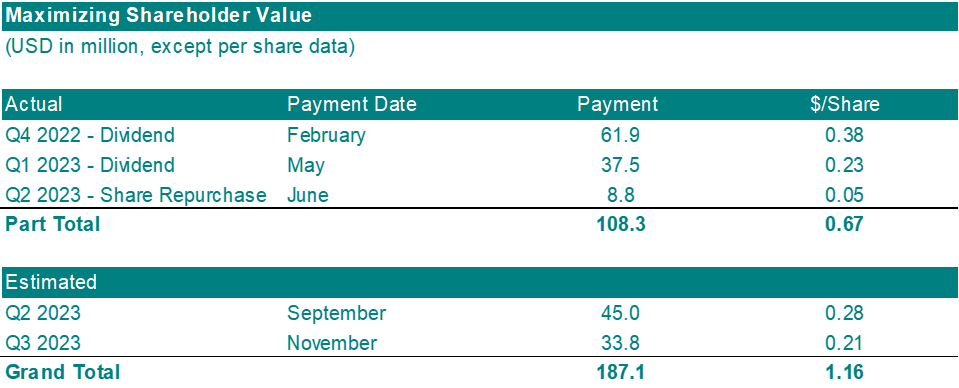

2. DHT has a consistent track record of quarterly cash dividends to its shareholders, demonstrating its commitment to generating value. Additionally, the Company has undertaken share repurchases, further rewarding investors. The total shareholder returns for the year amount to $108.3 million. Looking ahead, these returns have the potential to further increase by 78.8 million to a total of $187.1 million, considering the forecasted second and third-quarter distributions of $0.28 and $0.21 per share, respectively.

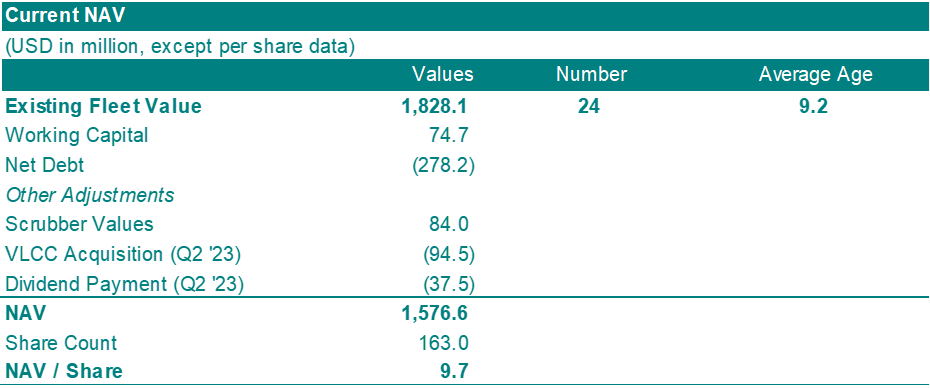

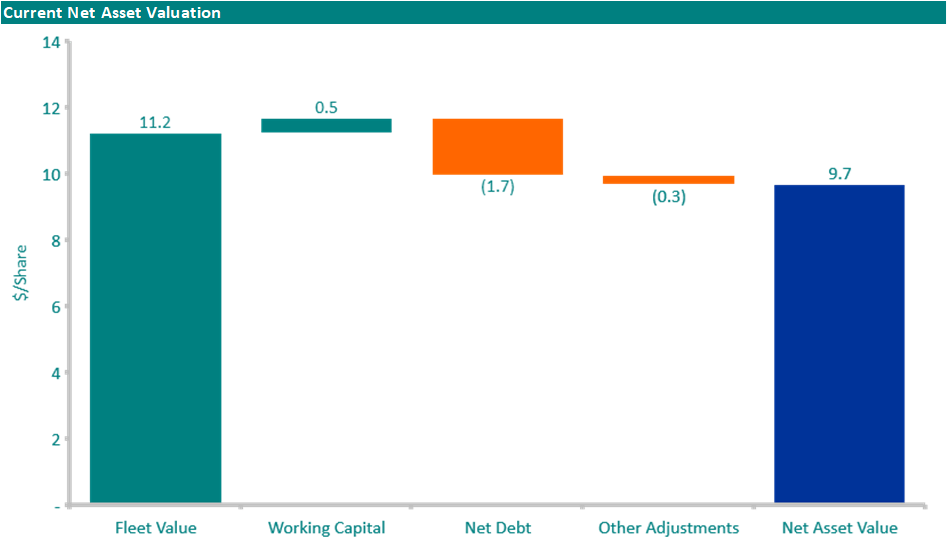

3. Despite the promising long-term fundamentals for the VLCC market, DHT's share price is trading at a discount to its $9.7/share net asset value ((NAV)).

In summary, DHT's robust balance sheet, distribution strategy, and potential for increased shareholder returns make it an attractive investment opportunity. Further, the Company’s focus on capturing opportunities in the VLCC spot market, coupled with its discounted share price, provides investors with an advantageous entry point ahead of a seasonally strong winter.

Robust balance sheet and financial resilience

For another quarter DHT successfully executed its capital allocation policy. The Company made $625,000 of scheduled repayments and completed the refinancing of the ABN AMRO credit facility more than a year ahead of its maturity. This was achieved by securing a facility from ING which offers more competitive pricing at 190 bps compared to the previous rate of 240 bps from ABN AMRO. Additionally, the new ING facility includes a $100 million incremental facility, albeit uncommitted. The amortization profile of the ING facility is broadly consistent with that of ABN AMRO’s facility. As a result, the refinancing exercise improved the Company’s balance sheet strength.

As of March 31, 2023, DHT maintains a net debt to total assets ratio of 18.8%, which is one of the lowest across my tanker equity universe and below the average of 33.6%. Furthermore, the average gross debt per vessel is $21.1 million which is only 5.1 million higher than my estimated $16.0 million residual value of a VLCC. This demonstrates DHT’s commitment to maintaining a de-leveraged position, which holds significant importance in the current high-interest economic environment, where the 5-year SOFR swap rate stands at 3.7%.

Overall, DHT’s robust balance sheet positions the Company as one of the most financially resilient entities in my tanker universe.

{kind=link}

Strong dividend performance and share buyback program enhance shareholder returns

For the first quarter of 2023, DHT declared a cash dividend of $37.5 million, equivalent to 100% of net income generated during the same period. The $0.23 per share distribution marks the 53 rd consecutive quarterly cash dividend. Further, in June 2023, the Company demonstrated a strong focus on rewarding its shareholders by purchasing 1,072,344 of its own shares equivalent to 0.7% of its outstanding shares, at an average price of $8.2517, deploying an additional $8.8 million. Year-to-date, DHT has delivered shareholder returns totaling $108.3 million or $0.67/share.

Considering the forecasted second and third-quarter distributions of $0.28 and $0.21 per share, respectively, my calculations indicate the potential for total shareholder returns to increase by $78.8 million, reaching a total of $187.1 in 2023 or 6.1% of today’s market capitalization. It is worth noting that DHT renewed its share buyback program in the first quarter, allowing for a total program size of $100.0 million with a 12-month duration. As a result, if management fully utilizes the remaining $91.2 million share buyback program within this year, total shareholder returns could potentially reach $278.3 million or 9.1% of today’s market capitalization. However, this would depend on a stronger-than-expected H2 2023 charter rate environment and a continued dislocation between equity prices and asset values.

{kind=link}

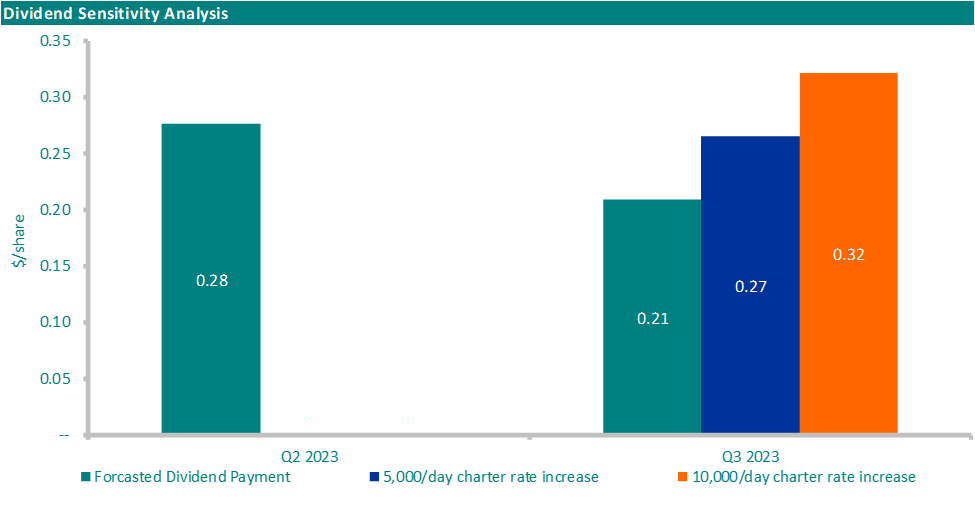

In July, DHT provided a business update where the Company estimates an average charter rate of $64,800 per day for its fleet operating in the spot market and $36,200 per day for the VLCCs employed under a time-charter during the second quarter of 2023. Consequently, I do not anticipate significant deviations from my forecasted distribution of $0.28 per share. However, the expiry of time charter contracts for DHT Mustang, DHT Amazon, and DHT Colt in the second half of 2023, combined with the delivery of a new VLCC vessel in July 2023 ahead of the seasonally strong winter period, DHT’s dividend distribution capacity for the third quarter substantially increases. Specifically, all else equal, every $5,000 per day increase in the charter rate of the remaining spot days results in an approximately $0.06 per share dividend payment.

DHT’s consistent dividend performance coupled with its active share buyback program underscores the Company's commitment to maximizing shareholder returns. With a positive VLCC charter market outlook going into winter, DHT is well-positioned to continue delivering value to its shareholders.

{kind=link}

Buying opportunity ahead of a seasonally strong winter

Despite unchanged long-term fundamentals for the VLCC market, the Company’s share price is trading at $8.79 or a 9.4% discount to NAV. Adjusting for depreciation and assuming a VLCC resale price of $127.0 million and a 5-year VLCC price of $102.0 million (all prices are excluding ~$3.5 million scrubbers value per VLCC vessel), I calculate a NAV at $9.7 per share.

{kind=link}

{kind=link}

Conclusion

DHT currently presents an appealing investment opportunity due to its share price weakness, trading at a 9.4% discount to NAV. In my opinion, the current share price performance is in contrast with the Company’s solid fundamentals and positive outlook. Specifically:

1. DHT maintains a net debt to total assets ratio of 18.8%, which is one of the lowest across my tanker equity universe and below the average of 33.6%, providing financial resilience and increased free cash flow to equity earmarked for dividend distributions and share repurchases.

2. DHT prioritizes shareholder returns by paying out 100% of net income as cash dividends. Looking ahead to the second and third quarters, I estimate cash distributions at $0.28 and $0.21 per share, respectively. Finally, assuming management fully utilized the remaining $91.2 million share buyback program, total shareholder returns may potentially reach a total of $277.9 million in 2023.

For further details see:

DHT Holdings: Printing Cash At Attractive Valuation