KIO - DHY: There Could Be A Good Argument For Buying This Junk Bond CEF Today

2023-12-08 17:21:36 ET

Summary

- The Credit Suisse High Yield Bond closed-end fund aims to provide a high yield to income-seeking investors through investments in speculative-grade bonds.

- The DHY fund's current yield of 9.64% is higher than the benchmark index, but it slightly underperformed the index over the past three months in terms of total returns.

- The fund's portfolio consists primarily of junk bonds, but it takes precautionary measures to mitigate default risks and has a diversified issuer base.

- The fund appears to be fully covering its distribution.

- The DHY fund is trading at a reasonably attractive entry price.

The Credit Suisse High Yield Bond ( DHY ) is a closed-end fund, or CEF, that can be employed by income-seeking investors to achieve their goals. As the name of the fund suggests, it aims to provide its investors with a very high yield by investing in a portfolio that primarily consists of speculative-grade bonds (“junk bonds”). It generally does fairly well in this task, as the fund’s current yield of 9.64% is higher than the 8.31% yield of the Bloomberg High Yield Very Liquid Index ( JNK ), although it is quite a bit lower than the double-digit yield offered by many funds that invest in floating-rate leveraged loans and similar assets. However, a yield very close to 10% is generally sufficient for most income-focused investors.

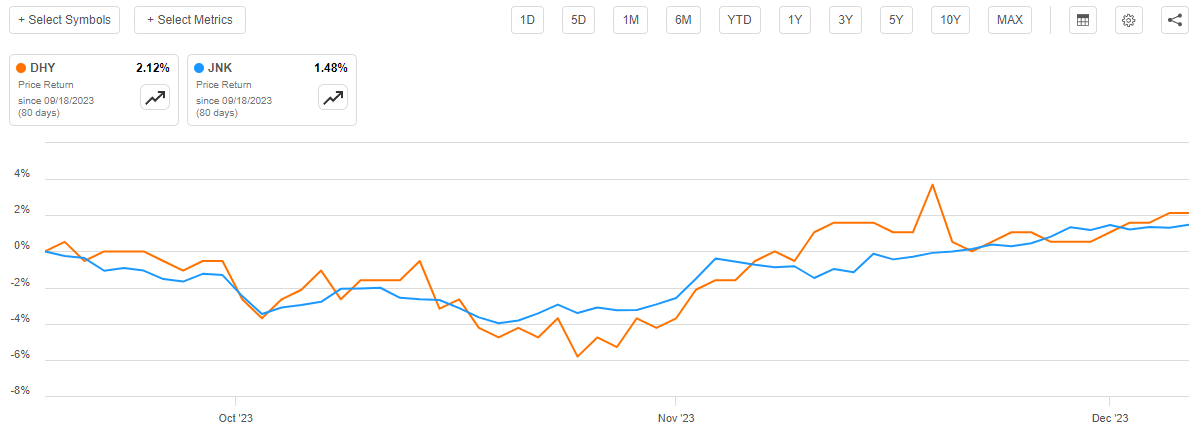

As regular readers may recall, we last discussed this fund back in the middle of September. Its performance since that time has been quite reasonable as the fund’s shares have appreciated by 2.12% over the period of time since the previous article was published. This is a better performance than the Bloomberg High Yield Very Liquid Index has managed to achieve:

{kind=link}

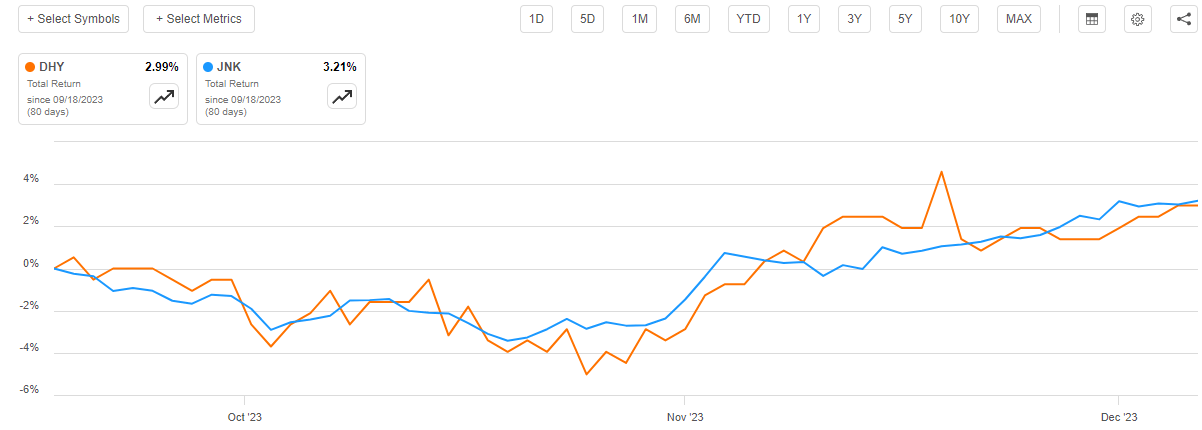

Investors in the fund have actually done much better than this figure suggests, however. This is because the Credit Suisse High Yield Bond Fund operates like most closed-end funds and pays out the overwhelming majority of its total returns to investors in the form of direct payments. In short, the basic business model is to keep its net asset value relatively stable and pay out all of the investment profits. As such, it is important to consider the distributions that the fund pays out when determining how well investors have actually done. When we do that, we unfortunately see that the fund has slightly underperformed the benchmark index:

{kind=link}

As we can clearly see, investors in this fund have received a 2.99% total return since the date that my previous article on the fund was published. This is not quite as good as the 3.21% total return that investors in the index fund have managed to accomplish. With that said though, this is partly due to the timing of distribution payments, as the higher yield of the Credit Suisse High Yield Bond Fund should have allowed it to outperform the index during other periods. In short, we can very quickly see that there is not a whole lot for investors to be disappointed about with respect to this fund’s performance.

However, the fund’s strong performance over the past two months or so begs the question of whether or not now is a good time to acquire shares. Let us investigate further and attempt to answer that question.

About The Fund

According to the fund’s website , the Credit Suisse High Yield Bond Fund has the primary objective of providing its investors with a high level of current income. As the name of the fund suggests, it aims to achieve this objective by investing in a portfolio that primarily consists of high yield bonds. The website provides a much more detailed description of the fund’s strategy:

The High Yield team seeks to deliver attractive returns from U.S. high yield bond markets to investors. The platform offers access to a deep team of credit professionals, including sector analysts covering over 1,000 corporate issuers. The strategy aims to maximize total return from monetizing macroeconomic themes and exploiting sector and issuer performance and rating dispersion. The team’s proprietary credit ratings, trend outlook and spread volatility evaluation drive a disciplined portfolio construction process that has powered outperformance in the high yield bond asset class.

The fund’s description strongly suggests that it will be investing solely in speculative-grade fixed-coupon bonds. However, that is not exactly the case. The fund’s fact sheet states that the actual portfolio right now consists of a combination of high-yield bonds, asset-backed securities, and senior loans:

Fund Fact Sheet

The majority of the fund’s portfolio consists of fixed-coupon junk bonds, however, as these securities account for 70.90% of the fund’s portfolio. As such, this fund is almost the reverse of a fund like the Apollo Tactical Income Fund ( AIF ) or the KKR Income Opportunities Fund ( KIO ) which consist primarily of floating-rate senior loans alongside a smaller allocation to junk bonds. This could be a very good thing for investors who are invested in one of those other funds. After all, combining either of those funds inside a portfolio with this one should have the effect of providing the investor with strong exposure to securities that will benefit from either rising or falling interest rates. This could be a good thing considering that there is a risk that the market will prove incorrect about interest rates being significantly lower by the end of next year than they are today.

As everyone reading this is no doubt well aware, the market is currently pricing in a series of reductions to the federal funds rate over the next five years. For example, ING Economics is projecting as many as six rate cuts in 2024. For its part, the federal funds futures market is projecting a total of 125 basis points of cuts by December 2024, which would place the target federal funds rate at 4% to 4.25% in December 2024. As Simon White, Bloomberg’s macro strategist points out , there has only been one situation in its history that the Federal Reserve has cut rates to that degree in a single year absent a severe recession:

Zero Hedge/Data from Bloomberg

The analysts who are projecting 125 basis points of rate cuts seem to agree, as many of their reports do mention a recession beginning in March as the driving force behind the predicted rate cuts. It is difficult to believe that stocks will actually perform well in a recession though, so the stock market’s reaction to these predictions is rather strange, but this article is about a fund that invests in bonds, so the stock market is not particularly relevant. I suppose that it is possible that a recession will occur next year as one of the biggest problems with the cheap money policy over the past fifteen years is that a number of zombie companies emerged.

Investopedia defines a zombie company thusly:

Zombies are companies that earn just enough money to continue operating and service debt but are unable to pay their debt. Such companies, given that they just scrape by meeting overheads, have no excess capital to invest to spur growth. Zombie companies are typically subject to higher borrowing costs and may be just one event – market disruption or a poor quarter performance – away from insolvency or a bailout. Zombies are especially dependent on banks for financing, which is fundamentally their life support.

The incredibly low-interest rate environment that has dominated the economy since the Great Recession of 2009 has generally allowed these companies to remain in business, as they could keep rolling over debt at incredibly low rates and earn just enough money to stay afloat and meet their obligations. However, the much higher interest rates today could very easily push these companies into financial distress as they will not be able to afford the higher interest rates demanded by investors as they roll over their debt. Goldman Sachs estimates that 13% of American companies are zombies, so it is certainly possible that today’s high-interest rates could ultimately trigger a wave of bankruptcies and a surge in the unemployment rate. That might be a severe enough economic shock to induce the Federal Reserve to reduce rates to the degree predicted by the market right now. However, this is by no means certain, and it seems highly likely that the Federal Government will do everything that it can to avoid such a recession during an election year.

At the same time, a few Federal Reserve officials have suggested that interest rate hikes are still on the table due to the market’s recent activities. The market has pushed down long-term interest rates over the past six weeks and has loosened financial conditions sufficiently to significantly soften the impact of the Federal Reserve’s tightening policy. Last week, Jerome Powell suggested that this could prompt the Federal Reserve to raise the federal funds rate again. Susan Collins, another Federal Reserve official, made similar remarks in the middle of November.

As such, it is far too early to put all of your eggs in one basket when it comes to betting on interest rate cuts. As most income-focused investors tend to be fairly risk-averse, they would probably be better off holding the Credit Suisse High Yield Bond Fund alongside a good floating-rate debt fund, such as the two mentioned earlier.

The fact that the Credit Suisse High Yield Bond Fund invests primarily in junk bonds is something that might concern risk-averse investors. After all, we have all heard about the high risks that these securities possess due to the fact that they are frequently issued by companies that have strained financial situations or balance sheets. Moody’s Investor Service has stated that these risks are increasing due to today’s higher interest rates that push up a company’s financing expenses following a debt rollover. From Business Insider:

Moody’s analysts expect the US speculative-grade default rate to peak at 5.6% in January 2024, before easing to 4.6% by August 2024.

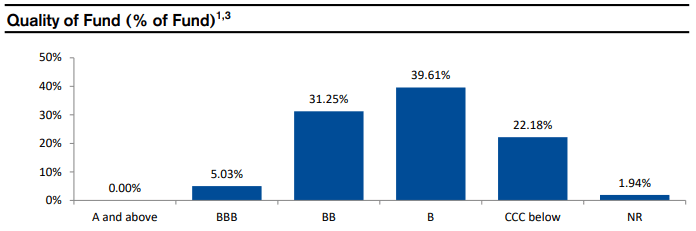

In short, this is a very different environment from what many of us have become accustomed to over the past twenty years of incredibly low-interest rates. Fortunately, the Credit Suisse High Yield Bond Fund is taking some precautionary measures to protect its investors against the losses that could accompany a rising default rate in the junk bond sector. First of all, the fund is investing mostly in higher-quality junk bond issuances. We can see this by looking at the credit ratings of the securities that are held by this fund:

{kind=link}

An investment-grade security is anything rated BBB or higher. As we can clearly see that only accounts for 5.03% of the fund’s total assets. However, we can see a 70.86% weighting to BB and B-rated junk bonds. These are the two highest credit ratings that can be assigned to junk bonds. According to the official bond ratings scale , companies whose securities have been assigned one of these two ratings typically have sufficient financial strength to carry their existing debt even in the event of a short-term economic shock (such as a recession). This could be particularly important today due to the market anticipating that a recession will begin within the next few months. The rating agencies clearly believe that most of the companies that are represented in this fund can weather this event without needing to default.

The fund also diversifies its risk across a number of different issuers. As of the time of writing, there are 218 unique issuers represented in this fund. As such, we can probably assume that there is no single issuer that accounts for an outsized proportion of the fund’s total assets. That assumption is certainly correct, which we can see by looking at the largest holdings in the fund. Here they are:

Fund Fact Sheet

As we can see, there is no single issuer that accounts for more than 1.20% of the fund’s total assets. This is quite nice to see from a risk-management perspective. After all, that 1.20% is far below the yield of a typical junk bond right now. As such, we can assume that any losses due to default will be quickly erased by the money coming into the fund in interest payments from the other securities. As such, any single default should not have a noticeable impact on the portfolio as a whole. There could still be a risk of default-related losses if a substantial number of companies go into default all at once, but in such a case the economy probably has much bigger problems than anyone currently expects, and such events are very rare in any case.

For the most part, the only real concern that we need to have with the Credit Suisse High Yield Bond Fund is that the market is wrong about the direction of interest rates. We have already discussed this risk as well as methods that can be used to hedge yourself against such risks.

Leverage

As is the case with most closed-end funds, the Credit Suisse High Yield Bond Fund employs leverage as a method of boosting its effective portfolio yield and total returns beyond that provided by the assets contained in the portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

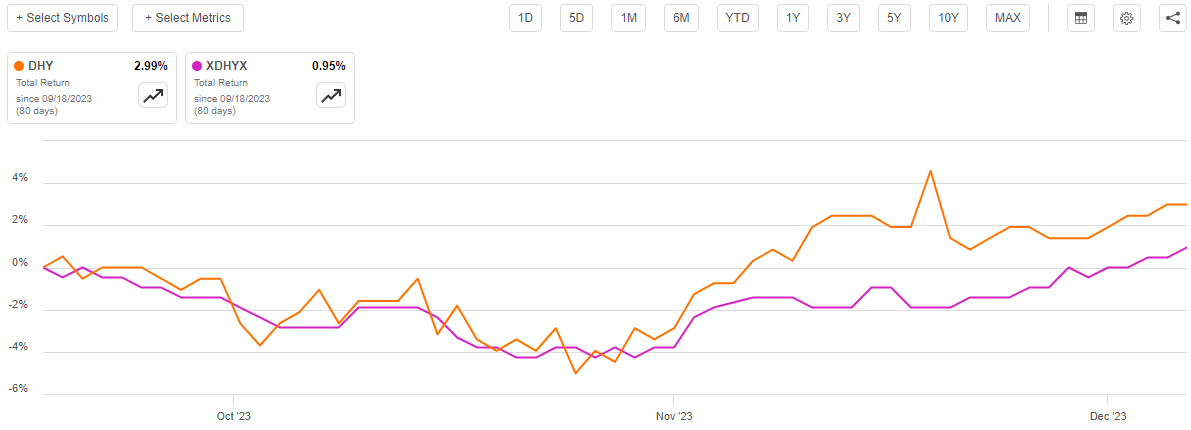

As of the time of writing, the Credit Suisse High Yield Bond Fund has leveraged assets comprising 31.27% of its total portfolio. This is slightly lower than the 31.37% leverage that the fund had the last time that we discussed it. This is probably caused by the fund’s net asset value increasing by 0.95% since the day that the previous article was published:

{kind=link}

The fund’s net asset value has appreciated by far less than the share price over the past three months, which could be a sign that the market is getting too excited about it. However, in terms of leverage, the slight appreciation in the fund’s net asset value means that its borrowings now represent a lesser amount of the fund’s portfolio since it has not borrowed any more money during the intervening period. This is nice to see.

Overall, this fund has somewhat less leverage than many other junk bond funds. It is also well below the one-third maximum that I generally prefer a fund to have. As such, we probably do not really need to worry about the fund’s leverage too much right now, as the balance between the risk and the reward is acceptable.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Credit Suisse High Yield Bond Fund is to provide its investors with a very high level of current income. In order to accomplish this goal, the fund invests in a portfolio that primarily consists of junk bonds, although it does have some leveraged loans and other assets. These securities primarily deliver their total returns through direct payments to their investors, and in today’s monetary environment, they tend to have very high yields. The fund collects all of the payments that it receives from these securities, and it even borrows money to collect payments from more securities than it could otherwise control using solely its equity capital. The fund pools all of the payments that it receives from these securities and combines it with any gains that it manages to realize by selling bonds that went up in price. The fund then pays all of the money in this pool out to its shareholders, net of its own expenses. We can assume that this would give it a very high current yield.

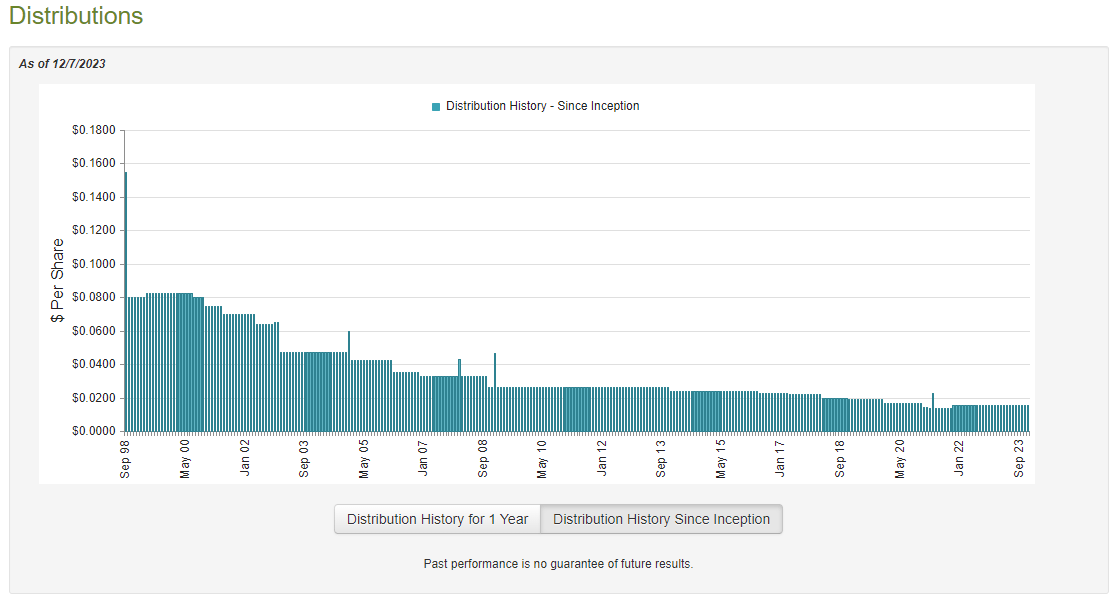

That is certainly the case, as the fund currently pays a monthly distribution of $0.0155 per share ($0.186 per share annually), which gives it a 9.64% yield at the current price. This is, admittedly, not especially high for a junk bond fund in today’s environment but it is still more attractive than the yield of the domestic junk index, as was mentioned in the introduction. Unfortunately, the fund’s distribution leaves a lot to be desired, as it has generally been declining for more than two decades. The fund did manage an increase in late 2021, though:

{kind=link}

This history of distribution declines seems likely to reduce the fund’s appeal in the eyes of those investors who are seeking to receive a safe and consistent income from the assets in their portfolios. This is a category that seems likely to include most bond investors and retirees. The distribution increase in late 2021 does improve the fund’s credentials in this respect though, assuming that it is sustainable. This is something that we want to investigate.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, it will not include any information about the fund’s performance over the past seven or eight months. This is quite disappointing considering that a great many things occurred during that period. For example, the market’s optimism that existed during the first half of this year quickly deteriorated and rates rose from mid-July until mid-October, driving interest rates higher and punishing bond funds like this one. This could actually be very similar to what could happen in 2024 if the nation avoids a recession, so it would be nice to see how the fund managed to handle that situation as part of our investment decision-making process. We will have to wait for the fund to release its full-year financial report to obtain this information, which will probably not occur for a few more weeks.

During the six-month period, the Credit Suisse High Yield Bond Fund received $12,785,891 in interest from the assets in its portfolio. It received no dividends, but it did have $31,073 of securities lending income. The fund thus reported a total investment income of $12,816,964 during the period. It paid its expenses out of this amount, which left it with $8,767,315 available to shareholders. That was, unfortunately, not enough to cover the $9,626,777 that the fund paid out during the period, but it did manage to get fairly close. However, this situation might still be concerning at first glance because we would usually prefer a fixed-income fund to fully cover its distributions out of net investment income. This one obviously failed to accomplish that during the period.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, it might have been able to sell assets for a capital gain given the market’s push for lower interest rates and higher asset prices during the first half of 2023. Realized capital gains are not considered to be investment income for tax purposes but they obviously do represent money coming into the fund that can be paid out to shareholders. Fortunately, the fund did have some success in this area during the period. It reported net realized losses of $14,047,981 but these were more than offset by net unrealized gains of $24,316,327 during the period. Overall, the fund’s net assets increased by $9,408,884 during the six-month period. Thus, the fund did manage to cover its distributions during the six-month period.

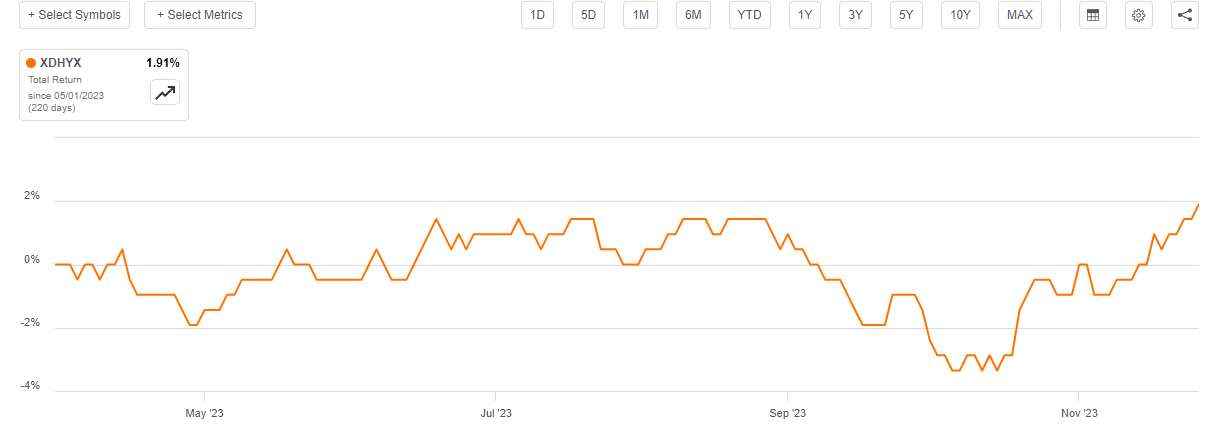

However, we can clearly see that the fund had to rely on its unrealized capital gains to fully cover the distribution. As everyone reading this is certainly well aware, unrealized capital gains can be erased in a market correction, so this is generally not desirable. Fortunately, the fund appears to still be in pretty good shape financially. As we can see here, the fund’s net asset value per share has appreciated by 1.91% since May 1, 2023:

{kind=link}

This suggests that the fund has managed to fully cover the distributions that it has paid out since the reporting period ended. When we combine this with the fact that its distributions were fully covered in the first half of its fiscal year, we can see that it is probably in pretty good shape. The fund should be able to continue to cover its distribution going forward.

Valuation

As of December 7, 2023 (the most recent date for which data is currently available), the Credit Suisse High Yield Bond Fund has a net asset value of $2.13 per share but the shares currently trade for $1.93 each. This gives the fund’s shares a 9.39% discount on net asset value at the present price. That is relatively in line with the 9.52% discount on net asset value that the shares have had on average over the past month. As such, the current price appears to be a reasonable entry point for investors who wish to own this fund.

Conclusion

In conclusion, the Credit Suisse High Yield Bond Fund appears to be a reasonably good way for investors to play the current narrative of declining interest rates over the next year. The fund’s portfolio is mostly positioned in traditional fixed-rate junk bonds, so the fund’s shares should appreciate as interest rates rise. However, there could be some reasons to doubt that interest rates will actually fall to the degree that the market expects, so it may be a good idea to hedge your exposure by holding this fund alongside a good floating-rate bond fund.

This fund is very well diversified to protect its investors against default risk, and it should be able to sustain its current distribution. When we combine this with a fairly attractive valuation, there is a pretty good argument for buying this fund today.

For further details see:

DHY: There Could Be A Good Argument For Buying This Junk Bond CEF Today